BBUC - A Short Report Questions Brookfield Infrastructure And Makes Me Rethink My Position

2023-10-28 04:38:47 ET

Summary

- A short report raises concerns about Brookfield Infrastructure Partners (BIP) and its financial disclosures.

- The report highlights discrepancies in BIP's valuation, cash flows, and funding gaps, suggesting the stock may be overvalued.

- While the report may face skepticism, it raises important questions about BIP's operations and could impact the stock price.

In this post, my biggest challenge is to stay honest even when the report I am going to review directly contradicts my previous writings.

I have covered Brookfield Infrastructure ( BIP ) ( BIPC ) for quite some time and most of my reports were bullish. More recently, my reports became more reserved due to growing fees and incentive distributions to Brookfield Asset Management ( BAM ). The last report written just days ago was positive again because BIP became unusually cheap.

This all changed after I read a recently issued short report on BIP. Its author uncovered material that was rarely if ever reviewed before. It took me some time to come to terms with this report. And while I do not agree with all of its statements, my opinion about BIP turned negative. Well-known words attributed to John Maynard Keynes come to mind: "When the facts change, I change my mind. What do you do, sir?".

The background

On October 24th, I was contacted by one of my readers with a terse question: "Can you refute this?". "This" was this video with a short-seller interview about BIP. I watched it, was not impressed, and easily refuted the video. But later on, he emailed me the original report by Keith Dalrymple and I was stunned.

The report consists of 79 pages of condensed text full of numbers and references to original documents. Most of all, it reminded me of a forensic accounting piece. The author's investing and accounting experience seemed self-evident.

I started vaguely recollecting the name: I read his piece about BIP's acquisition of the US railway several years ago. So he has been following BIP at least for some time. A quick search proved that it was not Mr. Dalrymple's first foray into short-selling - you can check this article in WSJ.

I have read several negative reports on Brookfield published in the US, Canada, and Australia and was never disturbed. The reports were either poorly researched and/or had a badly hidden social agenda. But this one was something different. In my opinion, it took several months of hard work by a professional to come up with this content regardless of the ultimate conclusions about it. It was far better researched than anything I have read about or authored on any of Brookfield entities.

The report has two striking features. First, it completely divorces from Brookfield-imposed metrics like FFO. Secondly, besides using BIP's filings for many years, the author checked the independent filings of several significant private BIP subsidiaries (in many countries outside of the US, private companies have to file statements) or filings of BIP's public partners in JVs. This approach creates a framework almost unfamiliar to Brookfield followers.

Brookfield subs like BIP, Brookfield Renewable Partners ( BEP ) ( BEPC ), Brookfield Business Partners ( BBU ) ( BBUC ), Brookfield Reinsurance Partners ( BNRE ), and Brookfield Property Partners ( BPY ) are all based in Bermuda, and their filings are rather opaque and less informative than quarterly or annual reports by US or Canadian companies. Brookfield Corporation ( BN ) and Brookfield Asset Management ((BAM)) are Canadian companies but their reports are not very helpful either.

BN is a giant holding company that omits or consolidates details of subs' operations. So, the level of granularity in BN's annual or quarterly reports is often not sufficient to understand the subs' operations. BAM's filings, on the contrary, are very clear and transparent but they are more focused on fees that BAM charges than on operations.

Under these circumstances, investors rely on the so-called Supplementary filings that all Bermuda-based subs produce quarterly. However, these reports use FFO as their main metric. As a result, FFO (or its derivatives such as AFFO) has become a de facto standard metric for Brookfield investors.

FFO is a non-IFRS/GAAP metric that does not have a unique interpretation. Consequently, certain entries can be included in or excluded from FFO. All Brookfield entities provide a reconciliation of FFO to IFRS Net Income but this is still insufficient. While it is not stated directly in the filings, the readers are led to believe that FFO is a measure of cash flows. And it truly is but in a way that is subject to ambiguity and interpretations. Many investors understand these limitations but are still forced to speak the FFO language because no other common language is applicable as long as one is limited to Brookfield filings.

Mr. Dalrymple overcomes this limitation by turning to independent BIP subsidiary filings or BIP' JV partners' filings whenever they are available. It is a huge effort that is restricted to non-US BIP subsidiaries. However, the results allow us to look at BIP in a new way.

I will not review the report in detail - it is too big. Instead, I will focus on issues that I consider most important. Some parts of the report are less convincing than others. There are small errors here and there and it is not perfectly edited. These issues, in my opinion, do not prevent the report from being a valuable source of information. What follows is mostly my selective reproduction of Mr. Dalrymple's content and logic with modest input by me. From now on, the word "author" means Mr. Dalrymple.

To create a proper mood, here is an epigraph to the report from O'Henry:

He is an incorporated, undercapitalized, unlimited asylum for the reception of the restless and unwise dollars of his fellowmen.

BIP as a holding company

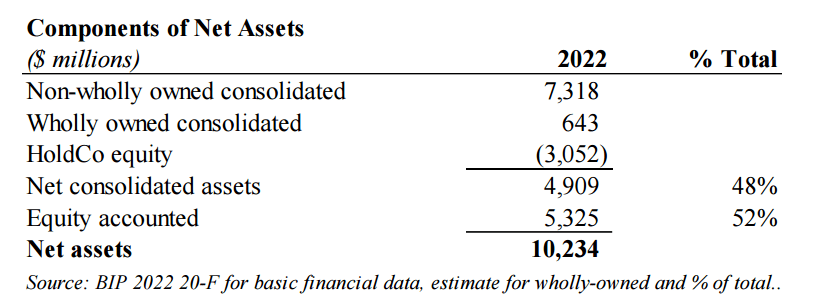

BIP positions itself as a normal company. In reality, it is a holding company or investment vehicle without operations or employees (all management works for BAM). It holds three types of infrastructure assets as depicted in the screenshot:

{kind=link}

Non-wholly owned consolidated holdings are typically held through Brookfield infrastructure private funds that grant BIP a power of attorney to vote on their behalf. Due to this power of attorney BIP exercises control and can consolidate holdings while holding a minority position within a fund.

For future purposes, it is essential to understand that more than half of all assets are equity-accounted in which BIP does not exercise control.

The information on investments is scant:

{kind=link}

In total, BIP discloses some entity-level information on 44% of NAV with no financial information on the remaining 56% of NAV.

How would you value a holding company? The most natural way is via SOTP (sum of the parts) - you value each holding individually, sum them up, and apply a holding company discount. For example, this is how most people value Berkshire Hathaway ( BRK.A ) ( BRK.B ). However, BIP does not provide sufficient granularity to value every entity in the portfolio.

So the author attempts to value individual companies in BIP's portfolio using primarily non-Brookfield sources, namely independent filings outside of the US. The analysis is broken up into four buckets:

- Detailed write-ups of two big holdings that together comprise ~41% of NAV - BUUK in the UK (Brookfield calls it UK regulated distribution operation) and Inter Pipeline in Canada including the Heartland Petrochemical Complex ("HPC").

- Troubled or impaired positions - the smallest bucket consisting of 3 minor assets with a combined NAV of ~7.4%

- Equity accounted segment consisting mostly of transport companies and comprising ~18.8% of NAV. Two companies in the segment are public.

- Summary valuation segment - consists of one company at ~5.7% of NAV.

The author performs a detailed valuation of the first and the biggest bucket and a more superficial valuation of other assets. I will not follow his long valuation process. Let me just tell you that it seems rather convincing for certain investments, especially for BUUK.

In the end, the author claims that his valuation comes up to a 24% discount to the NAV provided by BIP with the most damage attributable to the first bucket (please note that the author is not able to perform this analysis for all BIP assets since the information on parts of the portfolio is not available). The discount is not troubling that much by itself. Unfortunately, BIP is trading at twice its NAV even after a recent decline:

Courtesy of Dalrymple Finance

All but one infrastructure comps investigated by the author are trading at a discount to their NAV (one is trading at a slight premium to NAV). I would also like to remind you that unleveraged BRK is rarely trading above 1.5 of its NAV though it is a poor comp for heavily leveraged BIP. Imagine a leveraged closed-end fund that is trading at a premium of 100% or 200% if the author's valuations are correct. This is not something easy to fathom.

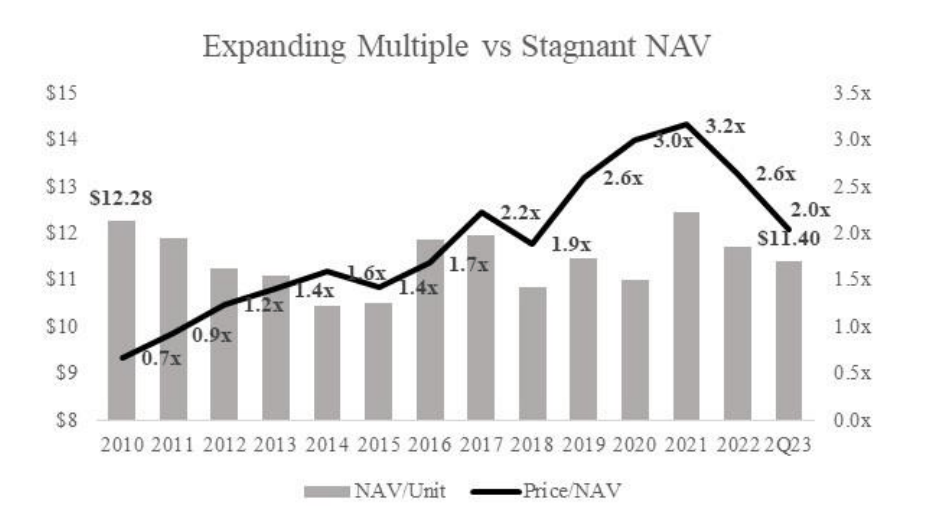

And it was not always the case as follows from the author's slide below:

{kind=link}

Until 2012, BIP was trading in line with NAV. Later on, during the period of low interest rates, BIP's price completely decoupled from NAV. NAV has not changed much or even declined per the author, but the multiple of price-to-NAV has expanded dramatically.

Cash flows

So far, the report does not appear particularly damaging. Who cares about NAVs when BIP produces superior cash flows? It yields a lot and bumps its distributions each year at 6% at least. It seems like a feast for yield-seekers.

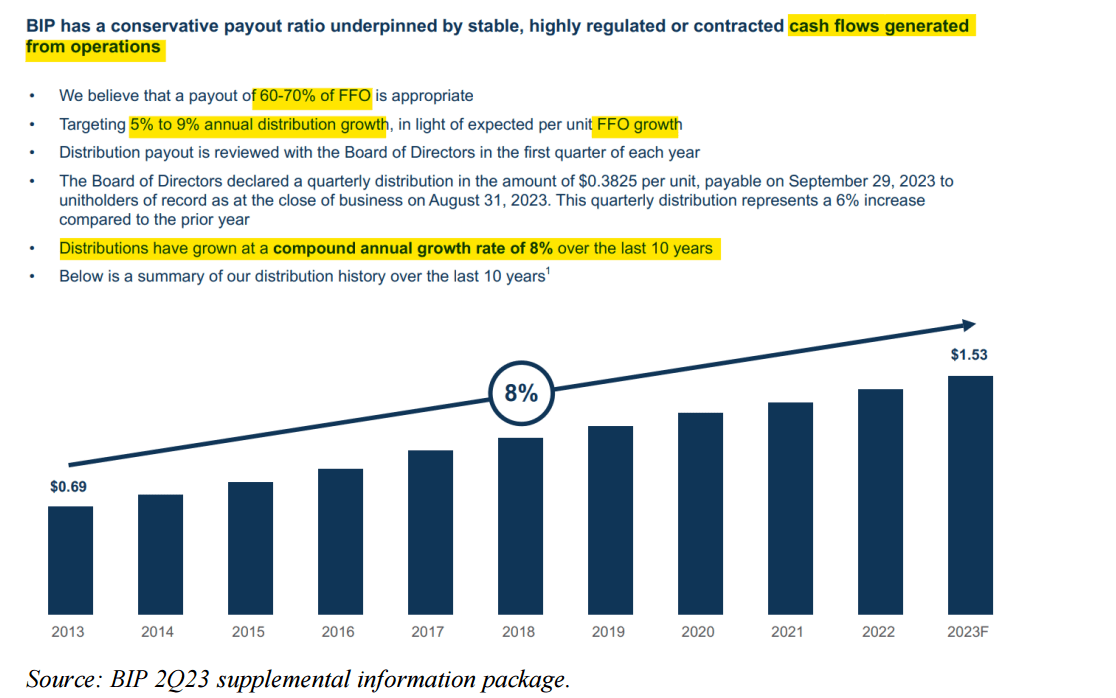

Since BIP is a holding company, its recurring cash flows should consist of dividends payable by portfolio companies. These dividends are supposed to be paid as incentive, common, and preferred distributions to stakeholders. Alas, the information about these dividends is not easily available. Instead BIP positions FFO as a proxy for these cash flows.

{kind=link}

The slide above with highlights by Mr. Dalrymple is quite familiar to all BIP unitholders. The message to the SEC by BIP is different: "FFO is not a measure of liquidity" as quoted by the author from the BIP-SEC correspondence. Here is another quote from the same correspondence:

{kind=link}

It is the second item in this excerpt that is rather revealing. Regardless of what FFO equity-accounted investments generate (remember, more than half of BIP's investments are equity-accounted!), they are unlikely to be paid out as dividends to BIP and BIP cannot control it.

For a better understanding: BRK owns about 20% of American Express ( AXP ). But it can use only AXP's dividends for whatever purposes. The rest of the cash flows are locked within the AXP balance sheet outside of BRK's control. BIP finds itself in a similar situation, and since its fraction of equity-accounted investments is so big, proportional FFO significantly exceeds cash available for distributions!

The author estimates FFO vs distributions received for equity-accounted assets:

{kind=link}

Over the last 5 years, the ratio of FFO booked to distributions received has averaged only 34%. Or in absolute figures: BIP booked $3.4B from equity-accounted investments and received only $1.2B in dividends.

BIP's average payout ratio is about 73% of FFO vs 34% of cash received from the equity-accounted investments which leads to a funding gap of ~$1.24B over the five years.

The author thinks that the situation with cash flows is even worse than has been presented so far and uses Arteris S.A. as an illustration. Arteris S.A. is called Brazilian toll roads operation by BIP and is owned through a JV with public Abertis. Due to Abertis filings, a lot is known about Arteris.

BIP presents Arteris as a toll-road collector. In reality, Arteris has also to build these roads. So it is a construction company as well. As a toll collector, Arteris generates enviable FFO. But as a construction company, it had to invest a lot and was never able to pay material dividends. Per the author's estimates, BIP booked $1B in FFO from Arteris since 2015 which should lead to ~$730M in BIP's distributions. But if one accounts for the capex needed for construction, BIP infused ~$240M into Arteris! The funding gap here is close to ~$1B.

This is nothing more than an isolated example. In total, however, the author estimates that BIP's payout is about 2x of sustainable levels using mostly BIP's filings and certain estimates. The payout ratio has exceeded 100% since 2015 and for 2021 and 2022 was 144% and 130% respectively.

Since recurring cash flows are not sufficient to cover BIP distributions the company covers them via issuing BIP units, BIPC shares, and recourse debt per the author.

Fees, disclosures, and representations

BIP pays management fees and incentive distributions to BAM and combined they are big. It is particularly disturbing that incentive distributions comprise a bigger fraction of total distributions every year and are growing much faster than LP distributions. However, in this regard, the author did not discover anything unknown. I presented the same concerns in my writings about BIP and other Brookfield subs.

A big part of the report is devoted to complaints about BIP disclosures and representations. The author claims that certain steps taken by BIP (such as the adoption of IFRS accounting) were done to obfuscate disclosures. In my opinion, the author proved beyond doubt that BIP disclosures are getting worse step by step. I noticed it myself long before reading the report. It is getting more challenging to understand the nature of BIP cash flows and the author illustrates it with several examples that I will omit here.

The report also addresses some of BIP representations and at times, it overlaps with scant disclosures. For example, BIP tends to rename everything in its filings even when investees are public. Something that is called "our US LNG Terminal" is nothing more than a 6% stake in the public Cheniere Energy Partners ( CQP ) though BIP never mentions it. It may seem rather innocuous but when done systematically across all holdings, it hampers understanding of BIP operations.

One author's revelation appears particularly striking and disturbing from my standpoint. BIP IPOed Dalrymple Bay Coal Terminal ("DBCT" or Australian Regulated Terminal per BIP) a couple of years ago (the public company is now called Dalrymple Bay, DVI ticker in Australia). Before IPO, BIP owned 71% of DBCT with the remaining 29% owned by Brookfield private funds.

The word "coal" does not create any positive associations today and unsurprisingly BIP wanted to exit. They had to IPO it because BIP could not sell the asset outright even though it tried. However, the IPO process required Brookfield to keep at least some possession of DBCT.

When the transaction took place, the Brookfield fund was allowed to sell its entire 29% while BIP sold only 22% of its stake equal to only 30% of its initial holding.

The author interprets it the following way:

...BIP was the safety valve retaining a material portion of its position if investor demand was weak, but allowing the Brookfield sponsored private fund to exit. ...BIPs management, which are also managers at Brookfield and Brookfield-managed funds, can subordinate the financial interests of BIP unitholders to other interests – such as Brookfield private fund limited partners. ... Given the predictably poor post-IPO performance, the 100% sales allocation awarded to the Brookfield fund shifted profits from BIP unitholders to the Brookfield private fund limited partners.

This is all completely legal as the management working for BAM does not have fiduciary obligations to BIP unitholders. In other words, they are not working in the best interests of BIP unitholders. I was well aware of this and mentioned it many times in my articles. But until the report, I did not consider that BIP can be used to beef up private funds' performance!

Coming to terms

I encourage my audience to read the report which is much richer than my review. You can also read the author's SA article . However, it is far inferior to the report itself.

We have to evaluate the report in two dimensions. Is it credible? And how it will affect BIP's stock price? These are two different questions only partially related.

Most readers of the author's article on SA did not accept his article as credible - you can check their comments yourself and there are very few likes. No doubt this skeptical response will be further supported by Brookfield which will try to refute the report in its entirety. Since in the short run, the market is a voting machine, it may lead to the partial recovery of BIP's stock especially if Q3 results are strong in FFO terms (something that I expect). Do not forget, however, that both the skeptical readers (who mostly read only the article and not the report itself) and Brookfield are biased and have vested interests in refuting or ignoring the report.

On the contrary: should we take the report at its face value? I doubt it because the author's attitude is not balanced. He ignored whatever positive one could say about BIP. And there are quite a few things to mention.

BN owns about 30% of BIP so there is a certain alignment of interests despite the lack of fiduciary duties. BN/BAM top management, in turn, owns a significant fraction of BN stock which makes this alignment even stronger. BIP's track record in both acquisition and disposition of assets is almost perfect. I am aware of only one announced acquisition that was not eventually closed. And whenever BIP sells companies it generates enviable IRR and MOC numbers. BIP private infrastructure funds that have mostly the same holdings as BIP are very successful and keep attracting record numbers of institutional clients. Even Dalrymple Bay company today is trading slightly higher than its IPO price several years ago.

I still believe some parts of the report are credible and damaging even besides aggressive accounting, high fees, and poor disclosure.

Let me pose the central question: are dividends from the portfolio companies sufficient to cover incentive, preferred, and LP distributions? I did not find any faults in the author's reasoning and the answer seems negative to me. If we follow the author further and agree that these distributions are financed via the issuance of units, shares, and debt, BIP will suffer. But what if distributions are financed via successful sales of appreciated assets?

This is legitimate and possible. Let me quote from Mr. Fukuda's, Brookfield Infrastructure VP of Corporate Development, response to my inquiry:

- What’s missed in all this is the successful execution of our strategy of buying, enhancing and selling assets. Since its inception, Brookfield Infrastructure has sold 28 businesses for over $8 billion, with an average IRR of nearly 25% (85% of these businesses were above the high end of our targeted 12-15% IRR range). This clearly demonstrates our strong cash flow generation and realized gains above our targets over our entire history.

While true, it completely recategorizes BIP. It makes BIP a traditional private equity outlet that is dependent mostly on capital recycling and risks its capital at every step instead of receiving recurring almost guaranteed, and inflation-adjusted stable cash flows. And we know how these entities are trading - just check BBU. Since BIP is paying material distributions (while BBU does not) we can compare it with stocks like Ares Capital Corporation ( ARCC ) or Blue Owl Captial Corporation ( OBDC ) trading at ~10% yield and having investment-grade bonds yielding ~7% now. I understand that these comps are not perfect but would not ignore them either.

But how about comparing BIP with Enterprise Products ( EPD )? EPD is a transparent, US-based, reasonably leveraged investment-grade MLP with high insider ownership. A big fraction of EPD assets are pipelines producing stable and recurring cash flows that are clearly described in Qs and Ks. Tax-wise, EPD's distributions are superior to BIP's. After the painful switch to an internal financing model, EPD started bumping its dividend at ~5% annually and is currently trading at 7%+ yield. What company - EPD or BIP - should be trading at a lower yield? Surely EPD, in my view.

Scant disclosure is a bad sign once BPY comes to memory. Initially, after the spinoff, BPY's statements and supplementaries were possible to understand. Later on, they were becoming less and less transparent. In the end, I was not able to understand anything. Eventually, as we know, BN had to bail out BPY at a rather low price despite regular annual increases in BPY's distributions.

Conclusion

I held BIP for more than 10 years until I sold everything upon reading and thinking over the report.

Even though his report specifically targeted BIP, all Brookfield companies will be affected if the report is only partially true. In the world of alternative asset managers, reputation means a lot and it is questioned by the report.

However, I do not expect other alt managers to be affected in the long run regardless of the final judgment about the report. It is very Brookfield-specific.

In the end, I would like to remind my audience that this post represents nothing more than my subjective and, perhaps, erroneous opinion and is not a piece of investment advice.

For further details see:

A Short Report Questions Brookfield Infrastructure And Makes Me Rethink My Position