SRNE - A SPAC Spinoff And Short Squeeze Walk Into A Bar

Summary

- Shares of Scilex could trade higher due to hedging pressure from large Sorrento short positions.

- Scilex's equity offering facilities, mean that the price could fall precipitously at any time via company dilution.

- Scilex's small free float, combined with the two drivers above, implies that the stock will likely be volatile in coming weeks.

Part 1 - The SPAC

The story begins with Sorrento Therapeutics ( SRNE ). The company is generally considered a battleground stock with multiple short-seller reports against the company and a moderately fervent retail base of shareholders. Sorrento is involved in a plethora of lawsuits and legal battles that are not within the scope of this article, but SA marketplace contributor Avisol Capital Partners does a good job summarizing some of it in their article here .

The relevant information regarding this situation is that Sorrento is a ~$600m market cap company that was looking to unlock value from their portfolio of therapies. To do so, they negotiated a deal with Special Acquisition Company Vickers Vantage Corp I (formerly VCKA) to spin off their wholly owned subsidiary Scilex (SCLX) so that it would become its own publicly traded company. Sorrento purchased Scilex back in 2016 for an implied value of $66M .

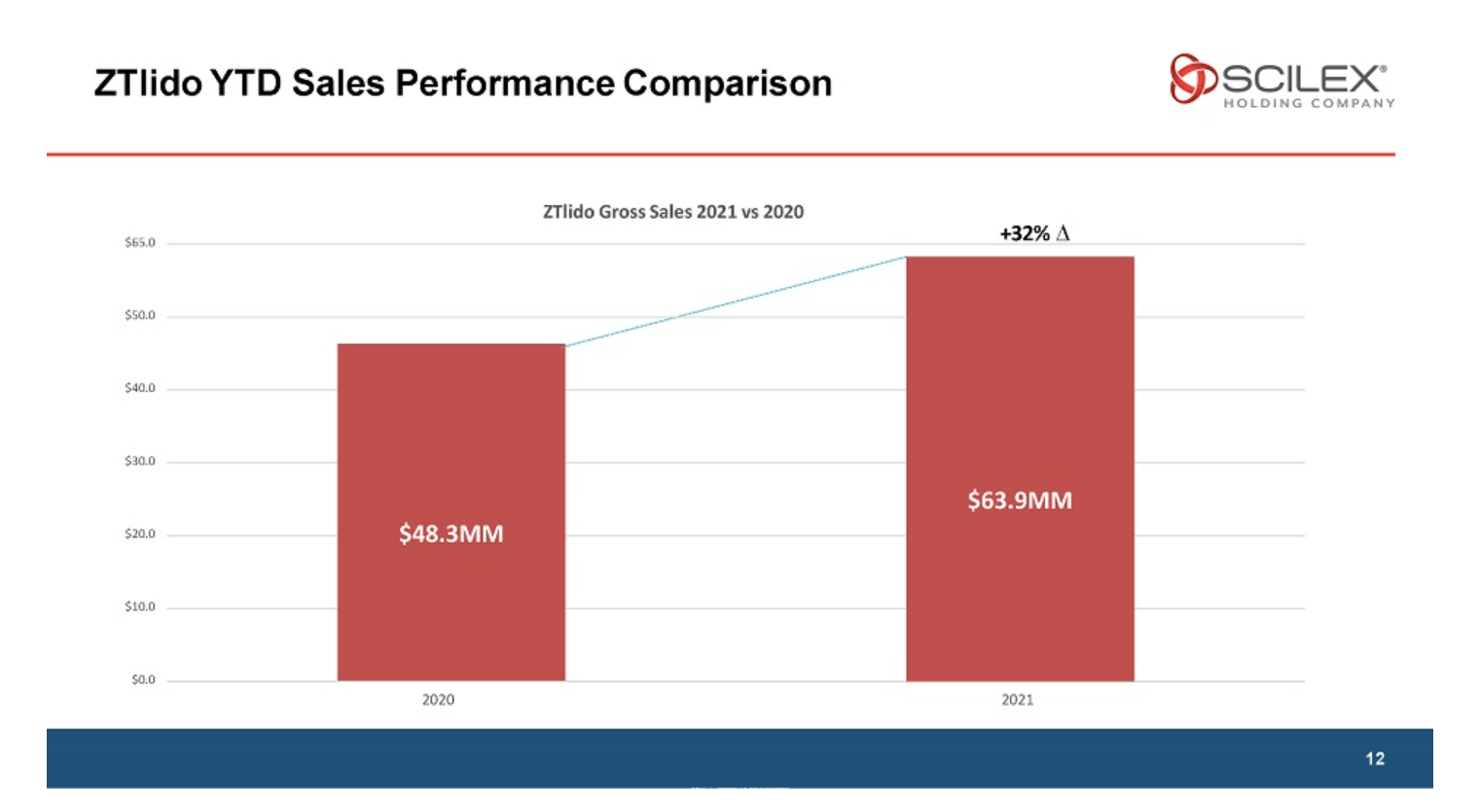

Over the past seven years, Sorrento has nurtured the Scilex subsidiary, got its main treatment ZTlido cleared with the FDA, commercialized it and has started selling it. In 2021, ZTlido generated gross sales of $63.9MM up 32% from 2020:

SCLX ZTDilo Revenues (Company Reports)

{kind=link}

Source: Company Presentation .

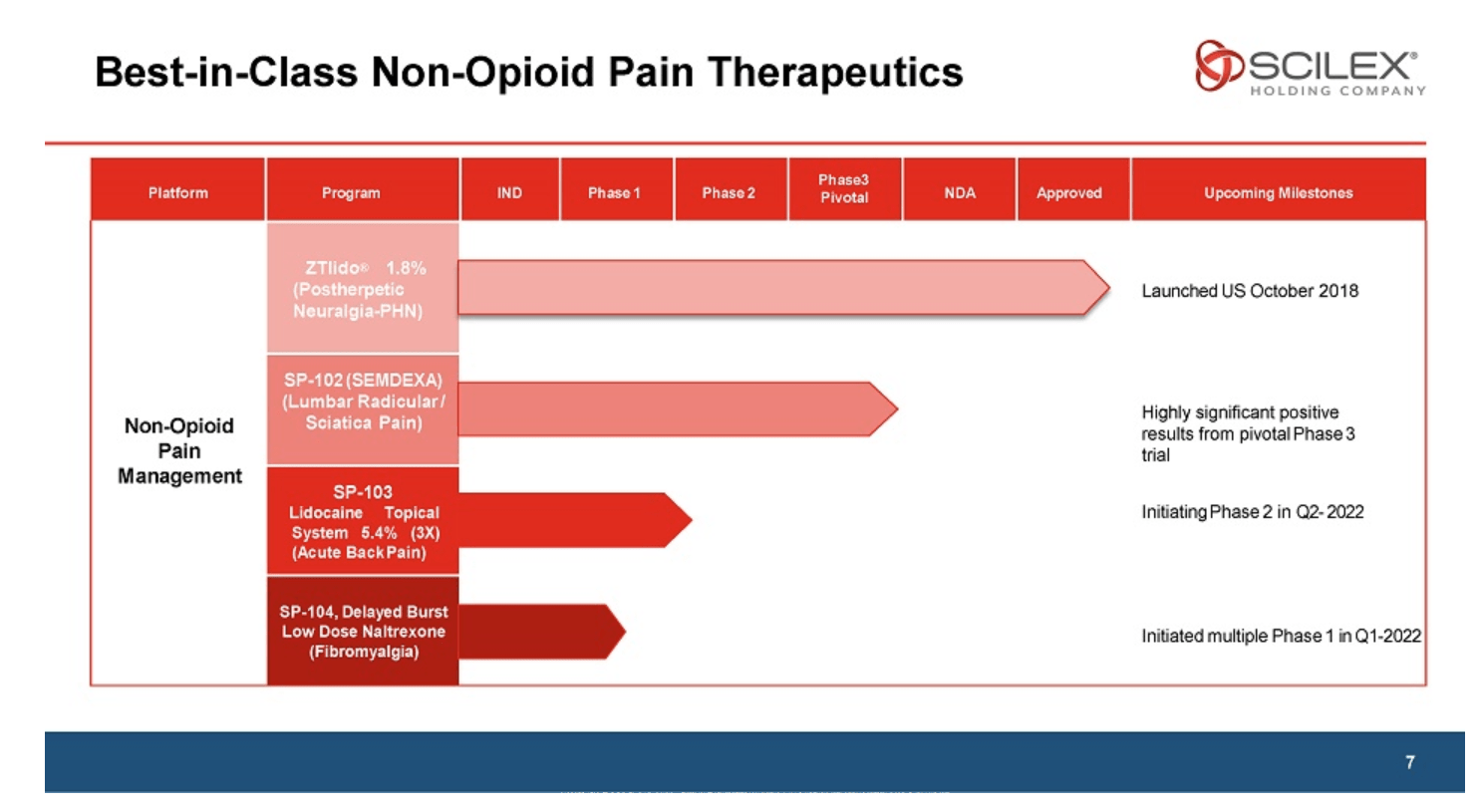

In addition to ZTlido, the company has a pipeline of other therapies that they are currently developing that may have economic value in the future.

SCLX Pipeline (Company Reports)

{kind=link}

Source: Company Presentation .

So it may, or may not be surprising to find out that the deal that Sorrento struck with Vickers SPAC valued Scilex at a whopping $1.5 Billion dollars. In other words, somehow the $600M Sorrento owns an asset supposedly worth $1.5B. This means that either Sorrento is grossly undervalued, or Scilex was grossly overvalued by the SPAC transaction, or some combination of both. The math doesn't add up!

For those familiar with SPAC mergers, overvaluation of the deal is common practice, so it's the author's opinion that the $1.5B number was very generous, and in fact, the market reacted swiftly to confirm this in two ways: over 90% of the SPAC investors redeemed their shares on the merger date instead of investing in Scilex (leaving a 1.1M share float), and the Scilex stock promptly fell from it's $10 IPO price ($1.5B valuation) to a low of $2.87 at the end of 2022. Note that even at $2.87 per share, Scilex was still valued at around $400M market cap, and this is supposedly a small fraction of Sorrento's business.

Following the close of the SPAC transaction, Sorrento held approximately 136M shares of SCLX, which were subject to a 180 day lockup. Sorrento can choose to hold the shares and eventually sell them, or they can distribute them to shareholders via a dividend.

Reviewing the Super 8-K of the closing SPAC transaction, SCLX's investor base looks like this:

- 1.15M shares held by SPAC public shareholders (freely tradable)

- 135.9M shares held by Sorrento (subject to 6 month lock up)

- 4M shares held by SPAC sponsors (subject to 6 month lock up)

The lockup means, subject to certain exceptions, those shares cannot be sold prior to May 11, 2023.

Part 2 - The Spinoff

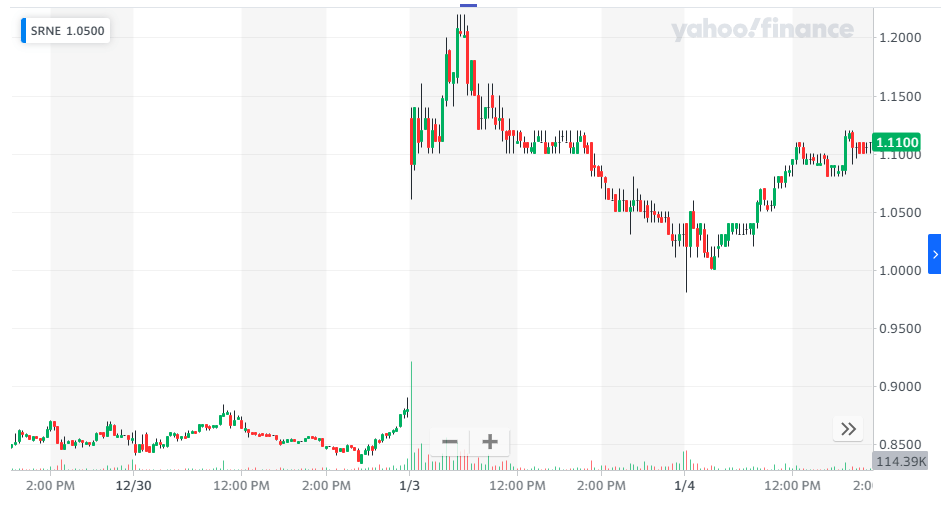

On December 30, 2022 the Sorrento board declared that they were going to distribute 76M of the company's 136M of SCLX shares to Sorrento shareholders. Based on the roughly 500m shares currently outstanding for Sorrento, a shareholder would receive 1 SCLX share for every ~7 Sorrento shares that they held. Given Sorrento shares were trading at around 85 cents at the time, and SCLX was trading around $3, 1/7th of a $3 stock is worth $0.42, or an astonishing 50% of the Sorrento price. To be clear, holding a $0.85 share of Sorrento entitled you to a dividend worth $0.42 of SCLX, or 50% of its value! Hence, Sorrento shares reacted very favorably to the news and the stock gapped up from $0.85 cents to $1.10 to reflect investors excitement about collecting this dividend.

SRNE Stock Chart (Yahoo! Finance)

{kind=link}

Source: Yahoo! Finance (Sorrento Intraday Stock Price)

An important realization is that the dividend stock paid to Sorrento shareholders would still be under lock up until May 11th 2023, and investors were likely assuming the SCLX price would be significantly lower than $3 by then.

Up until this point, the numbers relating to the value of SCLX, Sorrento, the size of the dividend, etc, are all abnormal but somewhat within the realm of "messy, but not remarkable". But this is the point where things get truly bizarre.

On January 3, 2023, Scilex provided a preliminary earnings update for Q4 2023 which was a massive beat to expectations.

The Company estimates that: ZTlido gross sales for December 2022 were in the range of $10.0 million to $12.0 million; the gross sales for ZTlido in 2022 were in the range of $93.0 million to $98.0 million, compared to $63.9 million in 2021, representing growth in the range of 45% to 53%; net sales for 2022 were in the range of $37.0 million to $42.0 million, compared to net sales of $31.3 million in 2021, representing growth in the range of 18% to 34%; and, as of December 31, 2022, the Company’s cash and cash equivalents were in the range of $1.8 million to $2.5 million, and the Company’s accounts receivables were in the range of $18.0 million to $22.0 million.

Source: Company 8K

This kicked off a huge rally in the low float, illiquid shares of SCLX, with the stock going from $3 to $10+ over 15 trading days.

Sorrento holders were still entitled to their 1/7th share of SCLX- except, instead of 1/7 of a $3 stock, they were now getting 1/7th of a $10 stock. Very quickly, the dividend has become worth more than the Sorrento share themselves.

Now this in itself is by no means an arbitrage. I will remind the reader that the dividend shares cannot be sold until May 11th, and the market is likely saying that despite the earnings beat, the current stock price for SCLX is unsustainable. I tend to agree, but at the same time, the market price is the market price. Also, if you think you can be cute by short selling SCLX commons to hedge your lock-up shares, that probably won't work because the short borrow rate is quite high and the availability to borrow shares in order to short is very constrained.

On/around January 19th, the Sorrento shareholders received their dividend. I say "on/around" because based on discussions and reports from different shareholders and brokers, the distribution of the dividend was done at different dates/times at different brokers. As of January 23rd, some shareholders still haven't gotten their shares and others have had theirs disappear. Overall this will likely take a few days for everything to get settled.

Charles Schwab account we got our Silex shares...:)

I RECEIVED MY SCILEX DIVIDEND IN MY WELLS FARGO BROKERAGE ACCOUNT

JPMORGAN just removed all of my SCLX dividend ???

Source: Reddit.com, /r/SRNE subreddit.

For long Sorrento shareholders, it's going to be an interesting ride for them to see what the ultimate price of SCLX is when the 76M shares become unlocked and free to sell. There also remains a question about the remaining 60M SCLX shares that are being held by Sorrento and what they do with them (sell them, hold them, or distribute them in ANOTHER special dividend?)

To recap, we have a parent company creating a spinoff worth 3x its own value, which is strange in itself. Then we have a special dividend of shares worth 50% of the parent company being paid out, where the special dividend quickly became worth (on paper) 150% of the parent company's value. But that's not where the story ends, the last part is the most interesting one.

Part 3 - The Short Squeeze

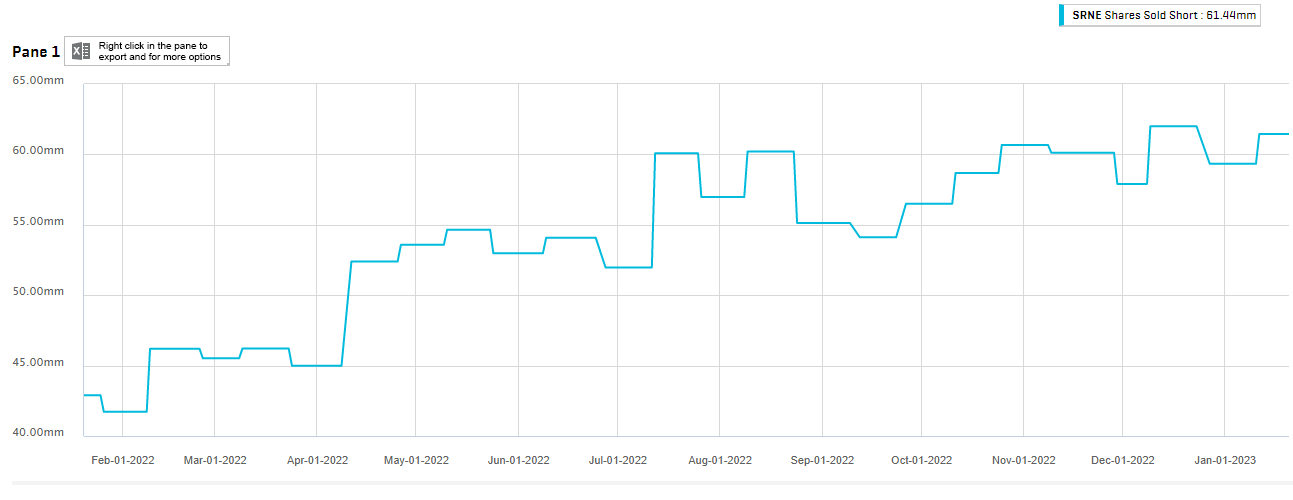

Two weeks prior to the dividend payment, there were approximately 60M shares of SRNE held short. A reminder that FINRA data is 2 weeks delayed, so we currently don't have accurate data for the exact amount of short shares at the time of distribution, this however is a close proxy.

SRNE Short Interest (Capital IQ / FINRA)

{kind=link}

Source: CapitalIQ and FINRA.

The rules for short sellers is that they are liable for all distributions that a company pays out while they are borrowing the stock. What this means is that if you were short 1 share of Sorrento on the distribution date, you will now be short 1 share of Sorrento, and short 1/7 of a share of SCLX (restricted shares). Most brokers, will require margin to be posted for the newly created short position, and will likely* mark the entire short position at its fair market value. To illustrate how painful this situation is, review the following:

December 28th - Short seller is short 700 shares of SRNE @ $0.80/share, the total short position has a liability of $560.

January 20th - Short seller is short 700 shares of SRNE @ $1.09/share, AND they're short 100 restricted shares of SCLX worth $11.00/share. Total liability is $1863.

The short seller has lost ($1863-$560=$1303) 232% on their trade on paper (reducing their account equity significantly), and is likely* required to post margin on a value that is 3x larger than their original position. If I wanted a shocking headline, I'd claim that this special dividend potentially created a $100M+ loss, and $200M collateral requirement for short sellers overnight. That's not quite true because each broker handles margin differently.

What's also interesting is that because many of the brokers have not properly allocated the special dividend distributions to people's accounts yet, some shorts are likely not even aware of this timebomb that's about to hit their account. This will likely occur between Jan 23rd and 27th.

So what can someone who is short shares of Sorrento (and also short SCLX) going to do now that they're in this situation? They can cover their Sorrento short via open market purchases, but they cannot buy SCLX restricted shares to cover that position. By their very definition, they're restricted from being transferred. And, SCLX continues to be a low-float deSPAC that has the potential to trade at all kinds of crazy valuations because of the tiny float. It wouldn't be unheard of for SCLX to trade up to $20, $30, $50 (like some SPAC predecessors). While the price of SCLX will likely eventually come crashing down with the May 11th unlock, in the short term this creates a very uncomfortable, inextinguishable liability for someone who was holding a short Sorrento position.

What the short seller can do is purchase a share of SCLX common shares to hedge their position. This ultimately means that if SCLX goes up, the profit from their long SCLX common share will offset their losses on the short SCLX lock-up share, but this also ultimately locks in their loss by effectively "covering" their SCLX short at $11.

What seems to be a better mechanism is to purchase a SCLX warrant, which is struck at $11.50, for around $2.00. This will essentially "knock out" their losses above $11.50, while letting them "make back their losses" if/when the stock finally craters back down to $3.

And finally, here's the squeezy part. The approximate 60M Sorrento shares shorted created roughly 9M shares of SCLX restricted short positions. There's only about 1.5M SCLX shares floating, and another 5-6M warrants (depending on how you count them). In other words, there isn't enough for everyone to hedge/cover, and even if only a fraction of the 9M shares shorted want to hedge/cover, it should cause significant buying pressure on an already very constrained SCLX float.

This is like a short squeeze, but not a short squeeze. A short squeeze results in shorts paying high borrow fees, short shares being recalled, and shorts being required to buy back their shares at higher and higher prices. That specific mechanism can't/won't happen here. The borrow rate on the restricted shares will likely stay minimal, there's no buy-in risk, but significant price risk associated with SCLX still exists. So instead of calling this a short squeeze, I think it can be more aptly called a Short "Pinch". People who are short SCLX restricted shares are going to be very uncomfortable as long as the SCLX share price stays elevated. Trying to hedge out, will cause more pain for all other shorts, which creates a virtuous cycle.

*Author's note: I say likely because risk models, margin requirements, etc. vary from broker to broker. This is a fairly standard, risk averse way a broker would handle the situation. They should be valuing the short restricted share at the fair market value, and the SCLX unrestricted common share is the best (albeit very imperfect) proxy for that. I will also add that many hedge funds operate with massive margin buffers, so if their Sorrento short position has a 1% allocation of their fund, and it suddenly requires 5% margin instead of 1% margin, it's more of a nuisance than an actual problem that will drive any hedging action. They will just close their eyes and wait it out. It's smaller investors, and heavily positioned funds, that should be affected by this situation.

Part 4 - Going forward...

Either by accident, or intentionally, Sorrento has constructed a situation to create a very painful experience for Sorrento short shareholders. It's not obvious in the coming weeks how the endgame evolves, does SCLX keep squeezing based on its low float, or does it drop precipitously? Why would it drop? Well, SCLX management is holding most of the cards here because they have two separate equity distribution programs in place. One with B Riley , and one with Yorkville . Having them means that they can raise cash for the company by issuing equity at any time, presumably when the prices and market liquidity are sufficiently high that they are happy to raise funds. Issuing shares (many of them) will ultimately drop the price of SCLX, to the benefit of the company. This is very similar to how an at-the-money offering is structured.

I can imagine two potential endgames that could be orchestrated here:

- Continue to let the low-float SCLX common equity trade higher and "melt upwards", causing pain to the short sellers, and then eventually sell shares via the equity facility at elevated prices, probably slowly to collect as much money as possible.

- Sorrento can run a second dividend for the remaining tranche of SCLX shares for Sorrento holders. This will compound the margin (and loss) problem for Sorrento short sellers- and potentially force them to reverse their short positions into a long position. (Why a long position? because then the Sorrento short seller will collect restricted shares from the distribution which will ultimately extinguish their short position from the first distribution) This would be a very clever setup where SRNE was used to squeeze SCLX which was then used to squeeze SRNE.

Conclusion and Disclaimer

Having examined markets for many years, I've yet to run into a situation quite as unique as this one. That's the primary purpose of writing this article, to document something very interesting and try to shed some light for those involved (and confused) about what's happening.

Some readers may conclude that this article is suggesting a short squeeze is imminent and they should get involved. I cannot stress enough how I do not believe this is the case, and I strongly caution those people to reconsider their actions. Situations like these are exceptionally complicated, risky, and random. SCLX ultimately has a hammer that they can use to "rug pull" the stock and dilute it to oblivion. Short sellers have capital that they can use to stay short for prolonged periods of time, they do not have to cover any shares, and the restricted share nature of this makes things significantly easier to navigate. I genuinely have no idea which way this is headed.

But I do have a bet on, and that bet is that the stock is probably going to be extremely volatile in the coming weeks.

As always, I welcome your questions, feedback and suggestions in the comments below.

Author's Misc Notes

Some shorthand notes that didn't fit with the flow of the article.

- Sorrento purchased 1.4M Warrants of SCLX in early December. This transaction stands out to me as odd because it's rare for companies to purchase warrants of other public companies. For modelling purposes I'm removing these from the warrant float which reduces it from 6.9M to 5.5M.

- It's unusual for companies to have two active equity facilities at the same time. This gives them optionality to use either facility, or both facilities. Using both would mean they can dump shares onto the open market faster.

- Long restricted positions of SCLX are probably marked at $0.00 for some/most brokers. They are almost certainly not marginable.

- The company issued 250k shares to B. Riley and Yorkville when they signed agreements with them. These are likely part of the float.

- The company issued 403K shares to the sponsor in exchange for debt forgiveness, these should be part of the float too.

- The company also has a clause that allows the sponsor to sell up to 1.5M shares in order to keep the float high enough to meet listing requirements. They specifically say it can only be used if it's necessary. I don't believe this clause has triggered at this point.

- The dividend spinoff was done extremely quickly, and in a very haphazard way. Both investors and short-sellers really had a hard time figuring out what day would be used to determine the dividend payout. My read on it is it was based on the payment date, not the record date. But I'm honestly not sure. There was no official ex-date as mentioned in this Nasdaq memo . If you think it was "obviously the record date", you should read up on "due bills", I've run into multiple scenarios where the record date is not the correct date.

- I've been on the "other" side of this trade before, where I was short a fraudulent company called SCEI. They issued a Contingent Value Right , and I ended up being short it. I had to post $2 of margin for years since I couldn't "buy it back" since it wasn't tradable.

On Margin

A key to this trade (Part 3, the "Short Pinch") relies on the short SCLX restricted shares to require margin to be posted, and to cause NAV marks as the value of the security goes up. If these are all marked at $0.00, with no/little margin requirement, then there's absolutely no pressure to squeeze SCLX.

Reading the FINRA document about margin rules , there's no specific call out to how a "short position in a restricted security where the common stock trades freely" should be margined. I think examples of this actually happening in the regular markets are extremely rare. However two general pieces of guidance appear to apply:

Other securities shall be valued conservatively in view of current market prices and the amount that might be realized upon liquidation. Substantial additional margin must be required in all cases where the securities carried in "long" or "short" positions are subject to unusually rapid or violent changes in value, or do not have an active market on a national securities exchange, or where the amount carried is such that the position(s) cannot be liquidated promptly.

And this:

When an account has a "short" position in a "when issued" security and there are held in the account securities upon which the "when issued" security may be issued, such "short" position shall be marked to the market and the balance in the account shall for the purpose of this Rule be adjusted for any unrealized loss in such "short" position.

I haven't been able to independently confirm how the short positions are being margined for this situation, and I do believe being "early" and "right" about how this will work is an important part of the trade.

For further details see:

A SPAC, Spinoff, And Short Squeeze Walk Into A Bar