M - A Strong Q4 Should Keep Macy's At Value Levels

2024-01-18 01:10:46 ET

Summary

- Macy's is a high-end retailer aiming to modernize its supply chain.

- The company focuses on delivering value and modernizing its own private brands.

- Macy's faces risks from seasonality, competition from digital shopping, and potential inventory clearance at reduced prices.

High-end retailers are often at a premium, despite the supply chain being difficult to manage. Among the companies trying to modernize their supply lines is Macy’s Inc. (NYSE: M). They will be the subject of today’s analysis.

A company of 722 stores, they are understandably a highly seasonal business, with a lot of their sales coming in November and December. This includes standard Macy’s, a high-end retailer in its own right, the luxury brand Bloomingdale’s, and the skincare product retailer Bluemercury.

Understanding Macy’s

Macy’s is a big retailer that goes after the high-margin business, and in the case of the luxury Bloomingdale’s, the even higher margin business. They say their focus is on delivering a clear value and modernizing their supply chain.

The company has to keep its stores stocked with products that are in high demand despite their high cost. They don’t, after all, want to be stuck with a bunch of inventories that nobody wants, and have to eventually clear it out.

In addition to the name-brand products, Macy’s is working on reimagining their own private brands as offering even better than normal margins. In the summer, they unveiled the first private label of this reimagining, called On 34th, named after the street the corporation headquarters is on.

{kind=link}

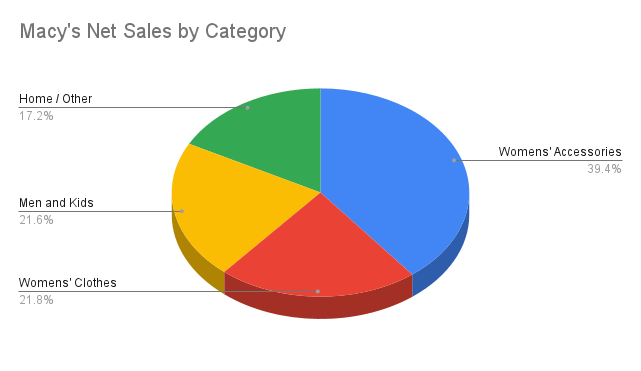

As you can see, the sales are aimed squarely at women. Despite this, bringing in things like in-store Toys R Us products has allowed them to grow the “men and kids” segment. Though it would be nice for the company to grow this more, there is little doubt that women will remain the bread and butter of the bottom line.

By the Numbers

| Cash and Equivalents |

| $364 million |

| Inventories |

| $6.0 billion |

| Total Current Assets |

| $7.0 billion |

| Total Assets |

| $18.1 billion |

| Total Current Liabilities |

| $6.0 billion |

| Long-term Debt |

| $3.0 billion |

| Shareholder Equity |

| $4.1 billion |

| Current Ratio |

| 1.17 |

(source: 10-Q at SEC)

Even in the balance sheet from late October, they have big, big inventories on paper. That is very important with November and December just about to start, and as we will see later, it is an effort that has served them well.

The current ratio of over 1.0 is a nice bonus, suggesting that they are in good financial condition going forward, despite spending a fair bit of their cash on hand on modernization efforts. The long-term debt is also serviceable for a corporation of this size.

Finally, the price/book of 1.20 is not a terrible one and shows that the price of the stock is fairly reasonable, especially for a well-known brand and a company that has been around for nearly 170 years .

Risks

The huge inventory is a current asset, but it is also a potential risk. Efforts are to stock the stores with expensive products their customers want to buy, and if they don’t, they’re likely to have to clear it out at reduced prices, which will naturally kill the profit margin and waste a lot of money and effort.

This is especially problematic because of the huge seasonality of the business, which obligates them to both heavily stock the stores for the Christmas shopping season and try to play prognosticator on what exactly they’ll want to buy.

In-store sales have historically been how this all works, and that too is at risk, as more and more consumers are headed to digital shopping experiences. Macy’s, of course, is trying to replicate this model to keep things moving, but in doing so they are setting themselves up for even more competition, and sometimes with companies that are pricing more aggressively.

A Solid FY2023

| 2020 |

| 2021 |

| 2022 |

| 2023 (9 months) |

| Net Sales |

| $17 billion |

| $24 billion |

| $24 billion |

| $15 billion |

| Op Income |

| ($4.4 billion) |

| $2.3 billion |

| $1.7 billion |

| $453 million |

| Gross Margin |

| 29.2% |

| 38.9% |

| 37.4% |

| 40.3% |

| Diluted EPS |

| ($2.21) |

| $5.31 |

| $4.48 |

| 63¢ |

(source: 10-K and 10-Q from SEC)

The financial results we see show a good profit made in 2021-2022. The 2023 numbers are a nice margin, but not so big a profit, but remember it only spans the first nine months in a company that does most of its sales in months 11 and 12.

FY2022 estimates offered in the 10-K were not very kind and suggested the first nine months were pretty standard for the year. By the Q3 10-Q, however, estimates were a lot more upbeat.

They projected net sales of $22.9 billion to $23.2 billion, the gross margin remaining strong at 38.5%, and best of all, the diluted EPS of $2.88 to $3.13.

This would give us a P/E ratio of 6.30 to 5.80, heavily in the deep discount value range. The final gross margin, if necessarily worse because of holiday sales, is still higher than it was in 2022.

| 2020 |

| 2021 |

| 2022 |

| 2023 (9 months) |

| FCF Operations |

| $648 million |

| $2.7 billion |

| $1.6 billion |

| $158 million |

| FCF Investing |

| ($325 million) |

| ($370 million) |

| ($1.1 billion) |

| ($716 million) |

| FCF Financing |

| $699 million |

| ($2.24 billion) |

| ($1.3 billion) |

| $60 million |

(source: 10-K and 10-Q from SEC)

Though it is hard to predict from the estimates where the FY2023 cash flow will end up, the trend of using up cash for investing and financing seems probable to continue this year.

The company has shown it is capable of generating a fair bit of operating cash flow, and that’s not likely to change. This is a potential for the company when they finish pouring money into their bid to reinvent and modernize themselves.

Conclusion

Many pessimists seek to compare Macy’s to Sears , who of course is no longer around. The big difference between the two, however, is that one is strongly profitable and the other just couldn’t for the life of them bring themselves a positive EPS in their final years.

What we have is a value play with a very old P/E ratio and a modest book value. That says to me the company is fairly priced, if not a bit cheap for what you’re buying.

A private investor group has offered $5.8 billion to buy out Macy’s , showing again that the big money is willing to pay a premium to get their hands on the company. They clearly believe this is a company that they can justify paying that much for, and while the belief is that the real estate value is worth enough to ensure a profit out of that buyout, that’s as true for individual investors as it is for the big money.

In the end, I think it’s easy to justify with the current P/E ratio that Macy’s is a company that is very worth considering to add retail exposure to one’s portfolio. There is money to be made here, and Macy’s has a long history of showing they know how to make it.

For further details see:

A Strong Q4 Should Keep Macy's At Value Levels