KOPN - A Visit To Kopin's Corporate H.Q. And Conversation With CEO Michael Murray

Summary

- On February 16, 2023, I visited Kopin's Corporate H.Q. and sat down to discuss the company with Michael Murray, Kopin's CEO.

- As part of the visit, I saw the $100 million plus fabrication room, where employees wear spacesuits in a clean room environment to manufacture the company's displays, modules, and sub-assemblies.

- We got in the weeds and discussed a number of upcoming and exciting new programs, and a 2023 (and beyond) full backlog.

- Michael's goal is to cross the rubicon, moving from negative Adj. EBITDA to positive Adj. EBITDA, and he discussed that yellow brick road to Oz.

Almost two weeks ago, I visited Kopin Corporation's ( KOPN ) corporate headquarters in Westborough, MA. This was about a ninety minute drive, each way, from my home and well worth the trip. The CEO, Michael Murray, graciously sat down to discuss Kopin with me for well over an hour, including providing a tour of the company's $100 million plus fabrication facility, where Kopin manufactures most of its product. To picture the fabrication room, think of a really big clean room, perhaps the imagery of the old Intel ( INTC ) commercials , containing people dressed up in what looks like spacesuits, surrounded by lots of fancy and sophisticated equipment. However, instead of producing chips for PCs or data centers, in Westborough, Kopin is producing optical displays, modules, and sub-assemblies.

On our walk to his office, as there are multiple window vantage points, across various stages of the fabrication process, I couldn't help but notice the freshly minted posters hung along the hallways proudly displaying the company's 'On Time, In Full' program as a call to action. This is the company's new and very important mantra. In addition to the posters, there are various colored printouts posted along the walls for both tracking and monitoring of the organization's progress of its 'On Time, In Full' programs. The subtext was embrace the force of the On Time, In Full as increasing the quality (at least 95% quality, with a stretch goal of higher) will take Kopin to the next level and up the value stack. This is Kopin's yellow brick road that now illuminates the pathway towards Oz, as opposed to being lost in the wilderness. This program is precisely how Kopin moves from negative Adj. EBITDA to greener pastures. Following the yellow brick road leads to a new pathway and one where all of the company's immense R&D achievements, Tier 1 customer list/ relationships, a new streamlined cost structure, and robust 2023 (and beyond) defense order book converge, at the end of what surely was a long and wandering path to Oz. Oz is a place where Kopin finally crosses the rubicon into profitability. Let's face it, this is why Kopin's stock can aptly be described as your favorite underdog baseball team, where at the beginning of every season, every team starts the season tied for first place. At the beginning of each season, fans are filled with hope about the promise of the upcoming year - 'This could be the year!' - only to regularly end up with their (or shareholders, in this case) hopes dashed by finishing at or near last place, despite its impressive roster of players (R&D innovations).

Outside of a few pockets of technology stocks/stock market euphoria, where the broader technology market lifted all boats, most recently, think of the December 2020 - February 2021 stretch, back when Cathie Wood ( ARKK ) was the ever so briefly the Queen of Wall Street, Mr. Market has been unwilling to reward Kopin with any type of a valuation, recognize its IP portfolio, or really even give the company the time of day, largely because of its persistent negative Adj. EBITDA losses. Moreover, adding insult to injury, Kopin's valuation multiple (enterprise value to revenue) is further compressed by subconscious fears of running out of cash and then being forced to resort to dilutive secondaries or selling off prized possessions, like its HBT business in 2013.

After spending ninety minutes speaking with Michael Murray, and as an aside, his January 11, 2023, Needham Growth Conference presentation offers a great set of Cliff Notes, as pitchers and catchers already reported to 2023 spring training. This year, though, the Kopin faithful might actually have something to cheer, as this year might actually be our year. Here's to hoping for us long suffering Kopin bulls.

Michael's Background

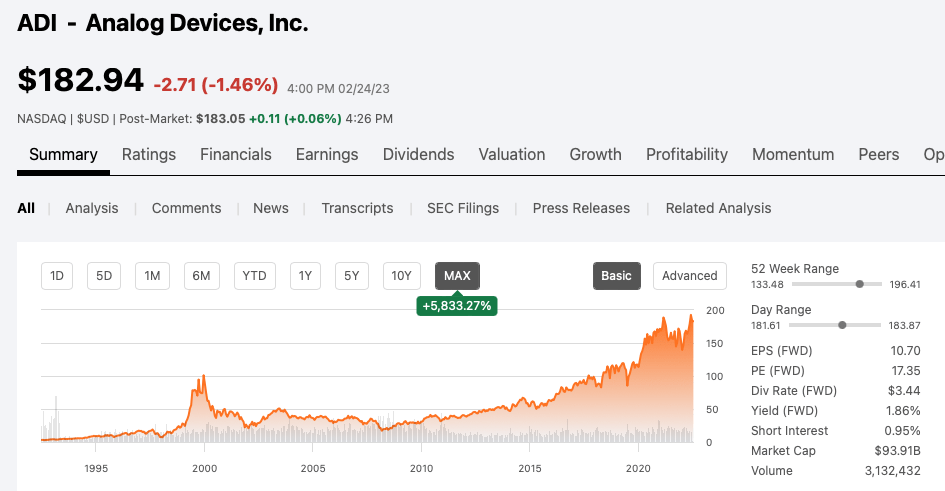

First, let's provide a quick background on Michael. Michael had a really strong career at Analog Devices ( ADI ). If you are truly a Buy and Hold investor, then chances are you're aware of how much wealth ADI has created for its long-term investors. In fact, the stock is up almost 10X, off its 2009 trough lows and up 58X if you bought the IPO.

{kind=link}

At Analog, Michael had real responsibilities, oversight, and gained exposure to some of Analog's best and brightest minds. This was a transformative career experience and one where he was able to share in some of the company's successes. He takes this experience and the playbook with him to Kopin. Post Analog, he joined a few promising start ups, companies with innovative technologies, but these companies simply ran out of runway and capital. Par for the course in early stage companies. Undeterred, he landed on his feet at Ultra Intelligence & Communications. During his thirty month leadership tenure, he ran the Cyber division, one of Ultra's five divisions, and he took a loss making business division with a baseline book of revenue of 78 million pounds to a business with revenues in excess of 175 million pounds. And yes, more importantly, the division crossed the rubicon, from loss making to generating positive Adj. EBITDA. Ultra, the parent company, was later bought by the really sophisticated private equity firm - Advent International - for $2.5 billion.

The Vision

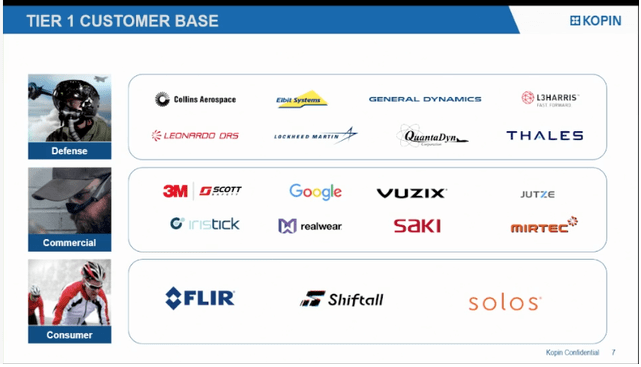

When I sat down with Michael, I wanted to understand his vision. Let me paraphrase how he put it. Kopin, led by Dr. Fan's technological innovation and pioneering spirit, in the optical display markets, is well suited for its next phase of growth, profitable growth. Kopin already owns a treasure trove of patents, has invested well more than $100 million into its fabrication facility, has really strong Tier 1 customers, and has a solid 2023 (and beyond) backlog. However, the key is to put in motion a strategy where Kopin can monetize all these great assets and attributes.

{kind=link}

In the past, the company has persistently lost money as it was unable to convert that great IP into profitability. A new day has come. Besides flying out for in-person meetings with all of Kopin's Tier 1 customers, Michael and team hit the ground running and priority number one was getting the cost structure streamlined.

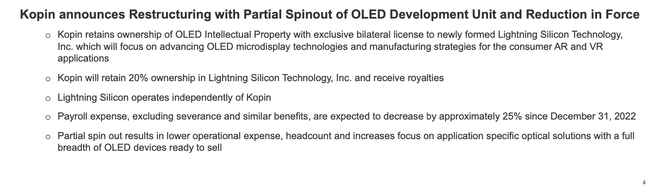

This led to the clever spin-out of the OLED business. Dr. Fan and some other high level and higher salary executives, along with the California research facility as well as other R&D staff members moved off the P/L, at the end January 2023. Post spin-out, Kopin owns 20% of Lightning Silicon. Lightning Silicon is the new joint venture consisting of Lakeside (the semi-conductor foundry, in China), Panasonic, and L-Silicon (the old OLED team and Dr. Fan). This will save Kopin $7 million to $9 million in OPEX on an annualized basis. Importantly, though, Kopin retains all of the existing OLED IP, is eligible to earn royalties on successful commercialization, and will have exclusive access to their 12 inch wafer, when it is (hopefully) produced in 18 to 24 months.

{kind=link}

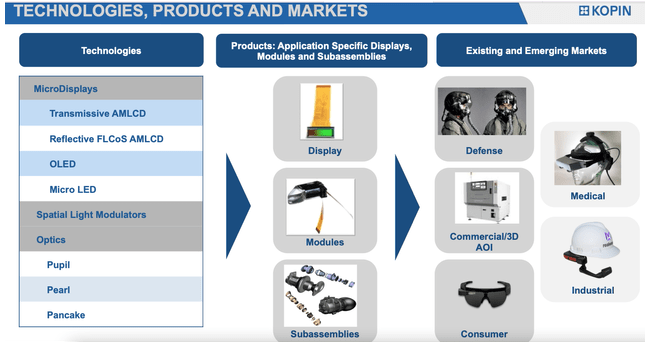

Michael's vision is really about putting in motion the playbook he learned and honed at Analog devices. It is all about moving up in the value chain stack. For example, and he discussed this during the January 11, 2023 Needham Growth Conference, would you rather sell a $1,800 display that might have zero to 25% gross margins or would you rather sell an integrated sub-assembly for $13K to $15K, and with 50% plus gross margins?

One of the biggest advantages that Kopin has, along with these great Tier 1 relationships, is they are technology agnostic. These Tier 1 customers want to buy and will pay for an integrated solution. And Kopin can do this via AMLCD, FLCoS, OLED, or Micro LED. However, it comes down to On Time, In Full. In other words, if Kopin can produce at the quantities and qualities required by its Tier 1 base, Kopin is well positioned to move up the value stack. And moving up the value stack means more value and much more importantly higher gross margins.

{kind=link}

Specifically, as a poignant example of selling an integrated optical assembly vs. just a display, one of Kopin's Tier 1 customers, General Dynamics ( GD ), is in the middle of an Abrams Tank M1A2 SEPv4 retrofit. At the January 11, 2023 Needham Conference, Michael noted that as part of the retrofit program, we are talking about several optical assemblies, per tank. Each integrated optical assembly will be sold for a range between 10K to 20K for each weapon site. And only a few google searches away, globally, we know there are an estimated 10K to 12K Abrams tanks in existence.

Murray couldn’t give me exact figures as they are classified but, based on my understanding of the program and the complexity of the weapon sight assembly, my conservative thinking is let’s assume 2,000 tanks, ultimately, get retrofitted over a three-to-seven-year time horizon.

At a resale of roughly $15,000 x 4 optical assemblies per tank equals roughly ~$60K per tank. And 2,000 tanks x $60K equals $120 million of future revenue. A key milestone for the project is the progression into qualification which is expected this year.

Gross margins on OLED displays are in the 0% to 25% ballpark whereas integrated optical assemblies run from 50% to 60%, sometimes even as high as 70% gross margins. Selling each LCos optical assembly for $13 to $15K each instead of just selling the LCos display, for $1,800 each, is a vastly superior business model and where Kopin is moving.

Upcoming Catalysts

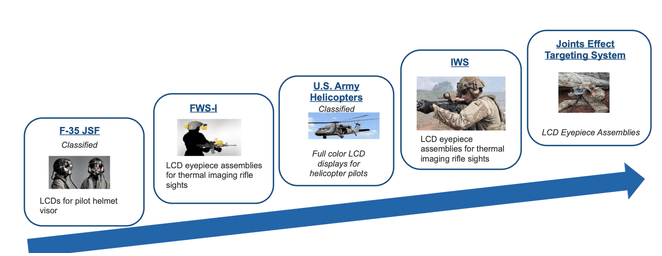

In 2023 through to 2025, FWS-I will be hitting full production. Leonardo DRS received a $579M 'IDIQ' order. In case you aren't familiar with 'IDIQ', this means it is a U.S. Federal government contract and the abbreviation stands for indefinite delivery / indefinite quantity which Kopin provides the display, optics, enclosure, and drive electronics for.

Leonardo DRS Awarded $579 Million Contract for Advanced Thermal Weapon Sights | Leonardo DRS

In addition to the full production of FWS-I, there are various programs in different stages of life cycles, ramping from LRIP (Low-Rate Initial Production) to full run rate production. These programs (see below) are the cornerstones of Kopin's healthy 2023 (and beyond) backlog.

See here:

{kind=link}

See here:

{kind=link}

The Reason For the Secondary

On January 25, 2023, Kopin caught the market a bit off guard. The company announced a $20 million secondary offering. This consisted of selling 14 million shares, at $1 per share, and this came with a sweetener, as there were 6 million, pre-funded $1 warrants (so people can exercise the warrants by paying $1 and they convert into shares) so Kopin’s balance sheet remains clean of warrants. In addition, there was a 3 million share over-allotment options. Prior to this secondary, Kopin has 95.2 million shares. So all-in, we are talking about some expensive new equity, as the post transaction diluted share count moves from 95.2 million shares, to 118.2 million shares, before accounting for any new stock option grants. And Kopin received approximately $23 million before underwriter fees.

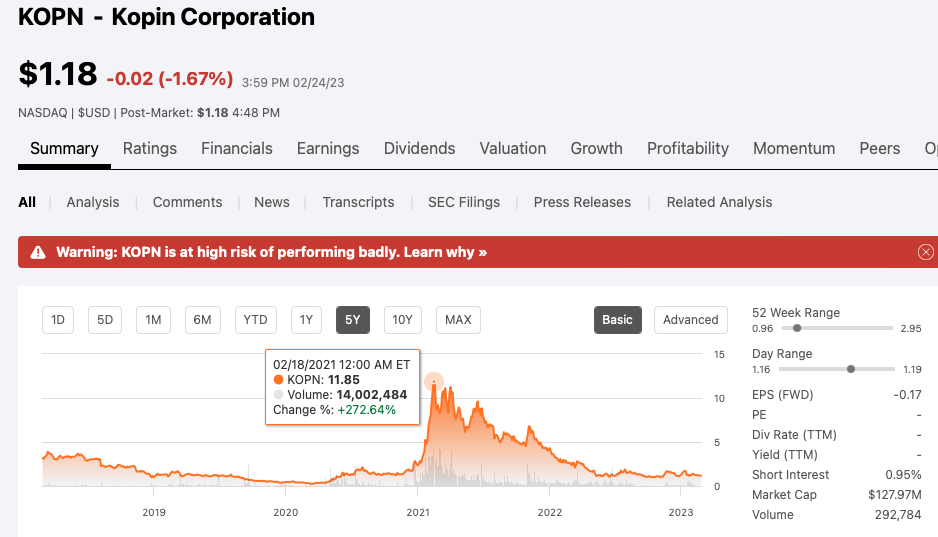

Candidly, and this was well before Michael Murray's time, but it is kind of crazy that Kopin's stock moved from the low $1s during the second half of 2020, and briefly traded north $13s in February 2021, and Kopin's management team didn't do a secondary offering back then. Arguably, they could have easily floated a one million to two million secondary offering, even if it was a priced at a 20% to 25% discount. Alas, this didn't happen, so it isn't worth elaborating on, other than to point out why the Street hasn't awarded Kopin with any type of a valuation. Let face it, if an investor is looking backward, this history of persistent operating losses and sloppy secondary raises at the inopportune times leaves a lot to be desired.

{kind=link}

Therefore, naturally, this was an important topic to discuss.

Michael put it this way.

1) In order to get to On Time, In Full, and get quality high enough to move up the value stack, as Kopin's Tier 1 customers want to give them those type of orders, but only 'if/ when' the quality metrics have been obtained, Kopin needs to spend significant additional capital investment into the Westborough, MA fabrication equipment and cleanroom.

2) In order to be eligible to win new and important government contracts, potential firms have to be a going concern and must have enough balance sheet cushion so as to not be disqualified and unable to bid on new work. Therefore, even though the $15 million of net cash, as of September 25, 2022, might have been enough to squeak by, as they are shooting for Q4 FY 2023 breakeven, they couldn't risk not being able to bid for important new contracts due solely to a weak balance sheet.

3) In order for the index funds to maintain eligibility to own Kopin shares, there is a required amount of balance sheet liquidity. This is a cash flow calculation of current and projected cash burn rates relatively to on hand liquidity. Michael said, look - we won't risk index funds being forced to sell the stock - due to tightness of cash burn rates, as we march towards breakeven. We also believe that the market will become more difficult and costly to raise capital and so far, that thesis is proving to be correct.

Although certainly not optimal, having to dilute the equity by 24%, ultimately though, having the extra cash on hand took precedence, as this enables Kopin to be better positioned to play the long game and hopefully reward long term shareholders via some important new contract wins. Speaking of new contact wins, this is a good segue to IVAS.

IVAS Is The Holy Grail

Integrated Audio-Visual System ((IVAS)) HoloLens is a up to a $22 billion, ten year program, for the U.S. Military to develop the state of the art night googles for soldiers. Microsoft has won the initial contract, but it has been slow going, as early trials have been plagued by reports of nausea and headaches. Congress has asked Microsoft to go back to the drawing board and devise a version 1.2 to alleviate these issues.

When I spoke with Michael, he said, currently, there is $580 million of R&D dollar available for the IVAS program. These dollars will be broken into different sub buckets, with a Prime, and various Small Business contracts. Given Kopin's extensive optical display arsenal, and IP, the company should, at least theoretically, be well suited to partake in this program. The specific timing, R&D dollars, and terms are very much an open question, but arguably, this could one of the biggest catalysts in Kopin's history given the amount of R&D dollars involved combined with Kopin's optical display IP and capabilities.

I would argue that Mr. Market is placing very little to no upside on the sheer possibility of IVAS, using its stock price as a barometer. Mr. Market seems to be unaware or even completing the possibility of Kopin participating in IVAS, in any form. Candidly, I'm not sure how to even attempt to quantify this, but this is clearly a big potential catalyst here and Mr. Market is asleep at the wheel on this front.

Other Nuances

- I asked about the automotive market and to be eligible to participate in that arena, a company has to be P.A.P.P. certified. Lo and behold, Kopin is presently working to obtaining this specification, as part of its optical assembly program for General Dynamics, and the Abrams tanks retrofit.

- I asked about Kopin's existing capacity. Michael said this isn't an issue. The focus is 'On Time, In Full' and achieving and maintaining a very high-quality standard, as this is the linchpin to moving up in the value stack. The Tier 1 customer base needs the comfort level and assurances that Kopin can deliver the sufficient levels of both quality and quantity.

- Another nuance is Michael has reorganized the business development go to market strategy. And this includes bolstering the strength of the program management group, including a few key hires from Raytheon ( RTX ). These seasoned veterans are tasked with running their own P/Ls and owning outcomes.

- Another fun fact. In early February 2023, industrial headset maker RealWear announced plans to go public like a SPAC . Kopin owns an undisclosed percentage of RealWear's equity and earns a royalty stream on sales of its headsets, as they utilize Kopin's IP. This is another catalyst presently not exactly priced into its current stock price.

Putting It All Together

Despite the dilutive but necessary $23 million secondary offering, bringing with it 24% equity dilution, the Kopin board and Dr. Fan appear to have hired the right CEO to manage the team into the next and pivotal phase of its growth / lifecycle. Michael Murray is laser focused on getting this business to inflect, and with him, he bring his playbook and blueprints honed from his Analog Devices and Ultra Intelligence and Communications days. The idea is to leverage Kopin's extensive IP, Tier 1 customer base, and move quality up with its On Time, In Full program, such that the business can move up in the value stack. The profit pools, a fun B School phrase, are derived via integrated optical assemblies as opposed to selling low gross margin displays. The company is technology agnostic and laser focused on delivering a bespoke solution to solve the specific application and customer needs.

As outlined, on January 11, 2023, at the end of the forty-minute Needham Growth Conference, during the Q&A session, Kopin has a stated goal of breakeven profitability, during the Q4 FY 2023 quarter. Moreover, the company's goal is crossing the rubicon of profitability during Q1 FY 2024. And the conservative math is based on flat revenue, to FY 2022, and driven by the $7 million to $9 million of OPEX savings from the OLED spin-out, combined with improving gross margins. The improvement in gross margins is a function of achieving higher quality metrics, redirecting the company's bandwidth, and working capital dollars, and fabrication capacity into programs where there are attractive gross margin dollars. Also an added tailwind, with important defense programs moving into full run rate production, this also helps gross margins. Moreover, the sheer possibility of landing some type of participation in IVAS is arguably as compelling and as exciting as the possibility of AR, VR, and the Metaverse which is still a few years away from prime time. Simply put, if Michael Murray and company can put on the field a team that gets to profitability, then this equity dramatically re-rates. That said, a twelve-month investment horizon is required here.

For further details see:

A Visit To Kopin's Corporate H.Q. And Conversation With CEO, Michael Murray