RNSC - AAON: Looking Back Looking Forward - Still Too Dear

- AAON's "story" appeared to be a good one, embraced by investors even before the increase in business due to COVID-19.

- Unfortunately for investors, the reality is not matching the rhetoric, and results achieved immediately following restructuring, and addition of new modern plant, are not being maintained.

- Increases in SG&A costs, likely the "Selling" element, are eroding any gross profit growth.

- The newly acquired BasX might help to shore up declining profits in the existing business, but not enough to provide the overall profit growth levels to justify the current share price.

AAON: Investment Thesis

Back on Dec. 22, 2021 I published article, " AAON: 'Mr. Market' Is Showing Irrational Exuberance ." Since that time the AAON, Inc. ( AAON ) share price has fallen by 31.77%, compared to a fall of 15.88% in the S&P 500 over the same period. But "Mr. Market" continues to show irrational exuberance, with AAON's earnings multiple still at the lofty level of 45.10 at market close on Jun. 24, 2022.

One would think AAON must be experiencing or about to experience explosive earnings growth, if the market is willing to price shares at 45 times earnings per share. In this article, I provide analysis to explore whether AAON has been experiencing high EPS growth, and if not, if it might be about to experience high earnings growth, that would justify its high multiple. The quick answers to those two questions are - No!!! and No!!, and I maintain my Strong Sell rating for this stock.

I will take a backward view first. Past performance is very often the best guide to future performance.

AAON: Looking For Evidence Of Past Explosive Earnings Growth Continuing Into The Future

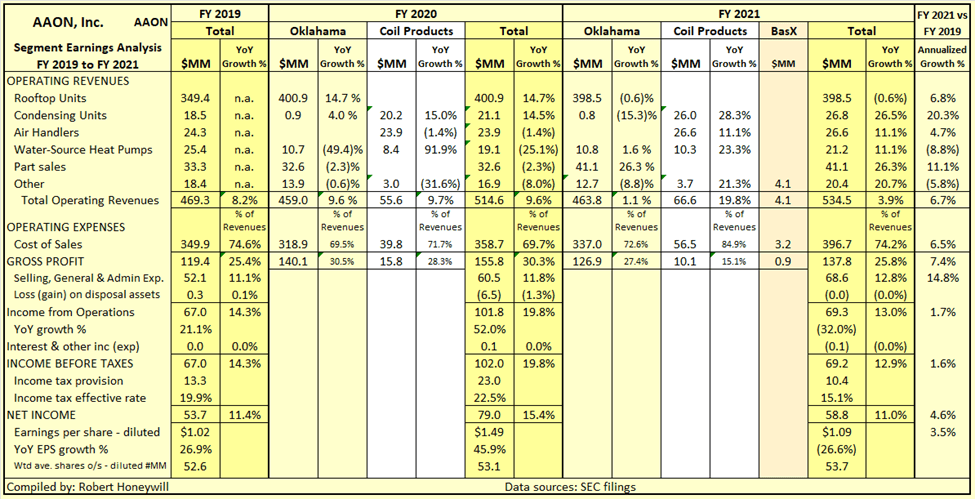

Table 1 below compares revenue, cost and earnings growth going back as far as FY 2017.

Table 1

{kind=link}

Commencing FY 2021, AAON began reporting segments described as "AAON Oklahoma," "AAON Coil Products," and "BasX." There is no reconciliation provided to former segments. New segment analysis is provided only on a fiscal year basis and only back to FY 2019, when a restructuring of operations had been completed. Segment reporting is down to the Gross Profit level only, with no allocation of operating costs below that level.

Comments on Table 1 analysis by segment and total

Oklahoma segment revenue - Aided by increased demand related to COVID-19, Oklahoma segment grew revenues in 2020 by 9.6% over 2019. In 2021, this segment grew revenues by just 1.1% over 2020, and just $4.8 million revenue growth over 2019.

Coil Products segment revenue - Coil Products segment grew revenues in 2020 by 9.7% over 2019. In 2021, this segment grew revenues by 19.8% over 2020.

Total segments revenue excl BasX - Aided by increased demand related to COVID-19, total segments grew revenues in 2020 by 9.6% over 2019. In 2021, Oklahoma segments grew revenues by just 1.1% over 2020, and just $4.8 million revenue growth over 2019. In 2021, total segments (excluding BasX) grew revenues by just 3.1% over 2020, due to the high proportion of low growth Oklahoma in the revenue mix.

Total segments revenue incl. BasX - In 2021, total segments including BasX grew revenues by 3.9% over 2020, due to the high proportion of low growth Oklahoma segment in the revenue mix.

Total segments comparison 2021 versus 2019 - The far right column in Table 1 is provided to eliminate the distortion to trends caused by COVID-19 impact. The percentages shown are for average yearly growth in revenue, costs, profit and EPS over the two years 2019 to 2021.

Revenue - On the revenue front, the high proportion of low growth roof top units sales, results in average yearly revenue growth of 6.3%, despite some smaller categories showing good growth. The inclusion of BasX, without a prior period revenue figure lifts total revenue growth to 6.7%.

Cost of sales and Gross profit - Overall, cost of sales grew at a slightly lower 6.5% per year, resulting in gross profit increasing by a higher 7.4% per year. The higher revenue growth Coil Products segment has a lower gross profit margin, limiting its contribution to earnings growth.

Selling, general and administration expenses impact on Income from operations - Selling, general & admin. expenses grew by a much higher rate (14.8% per year) than Gross profit (7.4% per year), resulting in income from operations showing only an average 1.7% per year growth from 2019 to 2021.

Effective Income tax rate impact on Net income - A low 15.1% effective tax rate in 2021 allowed net income to grow by 4.6% per year.

Shareholder dilution impact on earnings per share - Shareholder dilution due to shares issued to staff exceeding share repurchases caused EPS growth to decrease to 3.5%, compared to net income growth of 4.6% average per year.

I see no evidence in those figures of past or emerging growth that would justify a P/E ratio of 45.10.

AAON: Looking For Evidence Of Explosive Earnings Growth In The Future

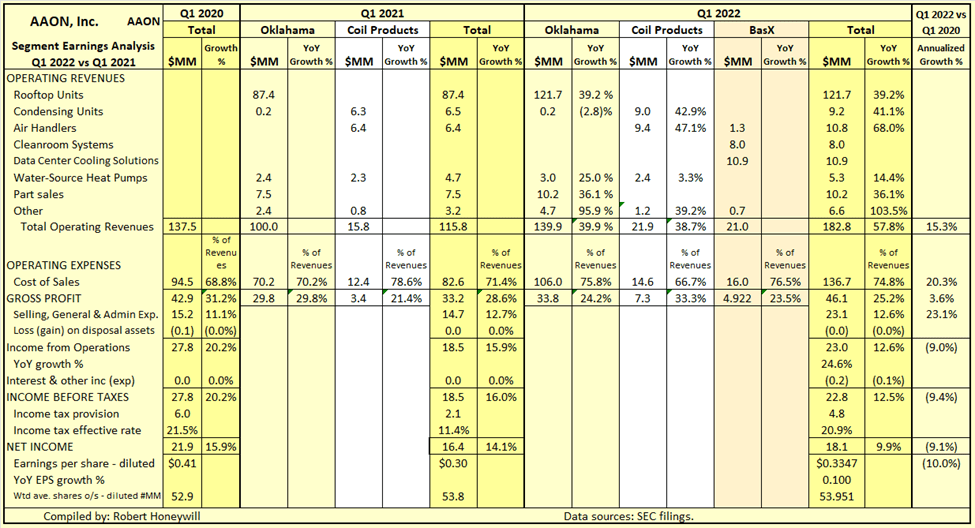

Table 2 below compares revenue, cost and earnings growth for AAON for first quarter 2022, 2021, and 2020.

Table 2

{kind=link}

Making A Fair Comparison

There are some difficulties in making a fair comparison between quarters above. Q1 2022 has the newly acquired BasX segment included, with no proforma amounts provided by AAON for Q1 2021 to allow a valid comparison and judge potential growth rates for BasX. Performance in Q1 2021 was affected adversely by a number of factors which are described in some detail in the Q1 2021 earnings call transcript available through Seeking Alpha Premium. Q1 2020 appears to be a suitable quarter for comparison Q1 2022 against.

Per the following excerpts from Q1 2020 SA Premium earnings call transcript ,

Net sales were up 20.8% to $137.5 million from $113.8 million... due primarily to our increased sheet metal production from the additional Salvagnini machines that were placed into operation... gross profit increased 68.9% to $42.9 million from $25.4 million... gross profit was 31.2% in the quarter just ended compared to 22.3% in 2019. We continue to see overall raw material cost decrease. The company has improved its labor and overhead efficiencies through increased production and absorption of fixed costs. Selling, general, and administrative expenses increased 11.2% to $15.2 million from $13.7 million in 2019....Income from operations increased 142.3% to $27.8 million or 20.2% of sales from $11.5 million or 10.1% of sales in 2019. Our effective tax rate decreased to 21.5% from 23.5%

In case it might be thought it is "cherry picking" to choose Q1 2020 for comparing current performance to, I would say performance like that reflected in Q1 2020 results would be required to justify AAON's current high multiple.

Even with new acquisition BasX included, Q1 2022 results compare unfavorably to Q1 2020

I have done a similar thing with Table 2 as for Table 1 by adding the right hand column showing average yearly growth rates for revenue and costs and expenses.

Revenue growth - Boosted by BasX inclusion, revenue has grown by an average 15.3% per year between Q1 2020 and Q1 2022.

Cost of sales - Also including the BasX impact, Cost of sales has grown by 20.3%, outstripping revenue growth.

Gross profit - As a result of Cost of sales growing faster than revenue, Gross profit grew by 3.6% per year compared to revenue growth of 15.3% per year.

Selling, general and administration expenses impact on Income from operations - Selling, general & admin. expenses grew by a much higher rate (23.1% per year) than Gross profit (3.6% per year), resulting in income from operations showing a decline of 9.0% per year from Q1 2020 to Q1 2022.

Effective Income tax rate impact on Net income - Similar effective tax rates resulted in net income decline of 9.1% per year, similar to the decline of 9.0% for operating profit.

Shareholder dilution impact on earnings per share - Shareholder dilution due to shares issued to staff exceeding share repurchases caused EPS decline of 10.0%, compared to net income decline of 9.1% average per year.

As for the yearly analysis above, I see nothing in the latest quarters reporting that would suggest AAON will successfully grow earnings and EPS at a sufficiently high rate to justify a P/E ratio of 45.0.

Summary and Conclusions

Current and prospective investors in AAON might believe the BasX acquisition will provide the necessary earnings growth to justify the present high multiple reflected in the current share price. Unfortunately, Q1 2022 results, including the BasX earnings, still fall far short of the Q1 2020 results which do not include any BasX earnings. It would appear the best the newly acquired BasX can do for the company is to hide the fact the earnings from the existing business segments are not growing, and in fact might be in decline.

I trust the discussion above enables readers to better understand why I remain very bearish on AAON at current share price. I maintain my strong sell rating on AAON at current share price levels.

For further details see:

AAON: Looking Back, Looking Forward - Still Too Dear