AAON - AAON: Strong Growth Outlook But Lack Margin Of Safety

2024-01-10 00:16:59 ET

Summary

- AAON is a manufacturer specializing in energy-efficient HVAC systems for commercial and industrial applications.

- The company's revenue growth has been strong, driven by the 2023 energy efficiency standards and strong global demand for air conditioning.

- Despite outperforming competitors, the lack of a sufficient margin of safety in the share price warrants a hold rating.

Synopsis

AAON (AAON) is a manufacturer that specializes in air conditioning and heating equipment, known for its energy-efficient and custom HVAC systems for commercial and industrial applications.

AAON’s revenue growth has accelerated in recent years due to the competitive advantage it has created, driven by the 2023 new energy efficiency standards. Although revenue growth was fluctuating, its margins remained robust, which allowed AAON to grow its diluted EPS in 2022. In its most recent 3Q23, revenue continued to show strong growth at double-digit rates. In addition, AAON managed to expand all of its margins year-over-year.

Looking ahead, the strong global demand for air conditioning will drive AAON’s future growth outlook. More significantly, the emerging markets are set to be key drivers of growth as the air conditioning penetration rate in these areas has remained low.

Despite AAON outperforming its competitors in terms of future growth outlook and profitability, the single-digit upside potential means there is a lack of a sufficient margin of safety in its share price. On that note, I am recommending a hold rating for AAON.

Historical Financial Analysis

From 2019 to 2021 , revenue growth was less than 10% due to the impact of COVID, inflation, and supply chain disruption, which negatively impacted AAON’s business. However, in 2022, revenue grew by 66.28% year-over-year due to AAON’s competitive advantage over its competitors. This competitive advantage created was driven by the introduction of new energy efficiency standards in the US, which are slated to start in 2023, and I will discuss it in depth later.

Author's Chart

Despite fluctuating revenues, its margins remained robust throughout the years, and this speaks volumes regarding management’s ability to manage expenses during challenging periods caused by COVID, inflation, and supply chain disruption.

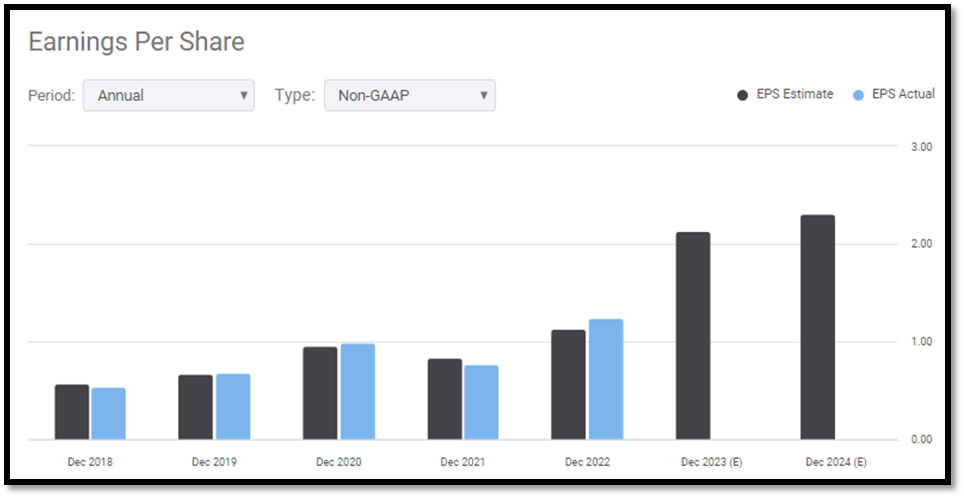

As a result of the strong revenue growth in 2022 coupled with its robust margins, AAON was able to grow its diluted EPS significantly in 2022. Diluted EPS grew ~69% year-over-year to $1.24 in 2022, up from 2021’s $0.73.

Author's Chart Author's Chart

As of 2021, its debt-to-equity ratio [D/E] had increased to ~12%. I believe the increase in debt was mainly driven by its acquisition of BASX . However, it does not raise any concerns for me due to the following reasons. Firstly, ever since 2021, its D/E has remained stable, showing no signs of acceleration. Secondly, its net interest expense as a percentage of revenue in 2022 was ~0.30%. Given its robust operating income margin, its current debt level and interest expense do not pose any sort of solvency risk.

Author's Chart

Analyzing AAON’s 3Q23 Earnings Results

In 3Q23 , revenue grew 28.6% year-over-year to $312 million, up from the previous period’s ~$242 million. To give you some more context on the strength of AAON’s growth, 3Q23’s growth marks the 7 th straight quarter of record sales for AAON. In terms of organic growth, it was ~11.9% for 3Q23. Management attributed these strong growths to strong backlogs and improvements in its operational efficiencies. In addition, supply chain disruption is still improving, which helped to bolster production rates and ultimately contributed to revenue growth.

In terms of 3Q23 margins, it improved in all areas. AAON’s gross profit margin [GPM] expanded from 10.2% to 37.2%, up from the previous period’s 27%. Its operating income margin [OIM] also expanded from 15.1% to 20.7%. Lastly, its net income margin [NIM] expanded 4% to ~15%. As a result of strong revenue growth and margin expansion, AAON grew its diluted EPS from $0.34 to $0.58 year-over-year, and this represents a growth rate of 70.6%.

Author's Chart

Global demand for Air Conditioning Is Accelerating

Based on the following chart provided by the International Energy Agency [IEA], two-thirds of the world will have air conditioning [AC] installed in their households. The demand for AC in all countries is expected to grow until 2050, with Indonesia, China, and India accounting for 50% of total AC units.

{kind=link}

Currently, most households in emerging economies do not have AC. Based on the following chart from the IEA, it's clear that AC is concentrated in more developed countries, while the penetration rate in less developed countries is less than 25%. Looking ahead, I anticipate that the emerging markets are going to be the key drivers of global AC demand growth, as increasing income levels and urbanization, combined with hotter temperatures due to climate change, are likely to boost AC adoption in these regions.

{kind=link}

AHRI’s 2023 Energy Efficiency Standard

In 2022, AAON’s revenue grew by 66.28%. This strong growth rate is driven by AHRI’s new 2023 energy efficiency standards. New federal minimum energy efficiency standards for residential heat pumps and air conditioners are now in force as part of the Department of Energy's ongoing initiative to lower overall energy consumption in the US. The new energy efficiency standards are set to go into effect on 1 January 2023.

As a response to these new energy efficiency standards, AAON prepared and started to transit in 2022, while its competitors are still being defensive due to the uncertain macroeconomic environment brought about by rising inflation, COVID, and supply chain disruption.

As a result of its strategic initiative to be on the aggressive side rather than sit back and wait for the economy to recover like the rest, this move paid off massively. The move allowed AAON to develop unique engineering capabilities, which allowed it to overcome supply chain issues in 2022. In addition, it has the shortest lead times in the industry, which contributed significantly to revenue growth.

The biggest payoff would be the development of products that are ahead of AHRI's new 2023 energy efficiency standards. As a result of this advantage AAON has, most of its competitors were forced to redesign a significant portion of their equipment and use more expensive components as a result of the new higher energy efficiency standards. This increased manufacturing cost was then offset by price increases, making AAON’s product offerings even more appealing.

Comparable Valuation Model

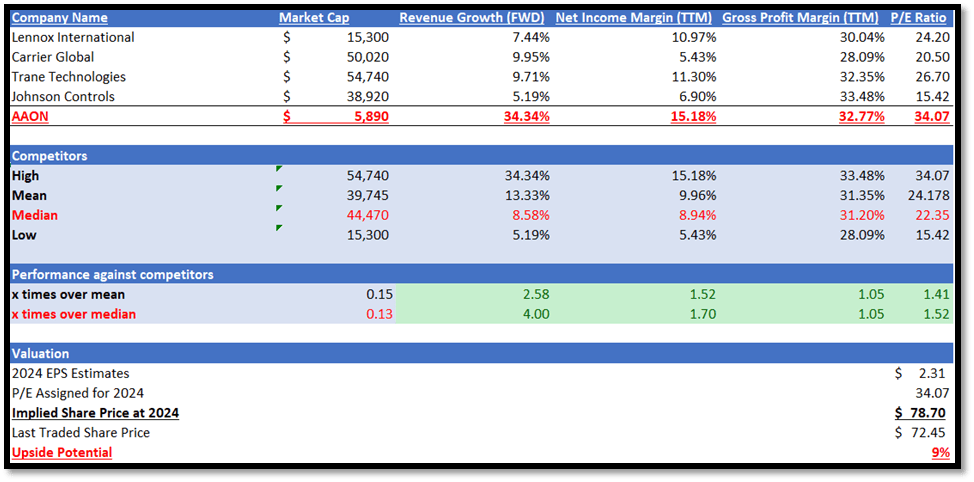

AAON specializes in heating and cooling products and competes with several other companies in the HVAC industry. The companies listed in my model are involved in the development, manufacture, and sale of HVAC systems and components, just like AAON.

In terms of market size, AAON is significantly smaller than its competitors. AAON has a market capitalization of $5.89 billion, while the median is $44.47 billion. This means that AAON is only ~13% of the median size.

Despite AAON’s smaller market size, its forward revenue growth rate dominates its competitors. AAON has a forward revenue growth rate of 34.34%, while the median is only 8.58%, representing a 4x greater growth rate.

Even though AAON’s GPM TTM of 32.77% is sort of in line with the median of 31.20%, AAON’s NIM TTM outperformed the competitor’s median. AAON’s NIM TTM is 15.18% vs. competitors’ median of 8.94%, representing 1.7x over the median.

Currently, AAON's forward P/E ratio of 34.07x trades at a premium to the median of 22.35x. Given its solid forward revenue growth rate and NIM TMM, its higher multiple is justified. In addition, AAON’s current P/E is below its 5-year average forward P/E of 40.96x.

The market revenue estimate for AAON is expected to reach $1.16 billion in 2023 and $1.30 billion in 2024. In addition, 2023 EPS is estimated to be $2.13, while 2024 is $2.31. Given the strength of AAON’s financial performance and the growth catalysts I have discussed above, it supports these estimates.

By using 2024 EPS estimates of $2.31 and applying them to my 2024 target P/E of 34.07x, AAON’s 2024 implied share price is $78.70. This represents an upside potential of ~9%. In my opinion, it lacks a sufficient margin of safety despite all the strength of AAON. Therefore, I am recommending a hold rating for AAON for now.

{kind=link}

{kind=link}

{kind=link}

Risk

One downside risk of holding AAON lies in potentially missing out on the expansive growth opportunity in emerging markets, which I have discussed above. As global demand for air conditioning is accelerating, especially in underpenetrated emerging markets, AAON’s strong market position and portfolio of products that are well ahead of the 2023 energy efficiency standards position it favorably to capitalize on this growth. If the upcoming earnings results manage to beat market expectations, its current P/E multiple might be revised upwards, leading to share price appreciation.

Conclusion

In conclusion, AAON’s past financials have demonstrated accelerating revenue growth, driven by its products’ competitive advantage and easing supply chain disruptions. Despite the fluctuations, its margins remained robust, which ultimately benefited its diluted EPS. In 3Q23, AAON continued to report strong revenue growth. In addition, it managed to expand its margins, driven by improved operational efficiency.

Looking ahead, the global demand for AC is anticipated to continue growing strongly. The growth is expected to persist until 2050, with emerging markets being the key driver due to the current low penetration rate.

AAON was able to significantly grow its 2022 revenue because of the competitive advantage its products possess. The reason AAON was able to achieve this was due to its strategic decision to research and design products that were compliant with AHRI’s new 2023 energy efficiency standards. Due to the macroeconomic uncertainty caused in 2022, most of its competitors decided to remain cautious, while AAON chose to be aggressive, took a leap of faith, and created products that were well in compliance with the new standards.

When I compared AAON with its competitors, it was clear that AAON outperformed them both in terms of growth outlook and profitability. However, with single-digit upside potential, the lack of a sufficient margin of safety leads me to recommend a hold rating for now.

For further details see:

AAON: Strong Growth Outlook But Lack Margin Of Safety