AIR - AAR Corp.: A Good Company But Not The Right Time To Enter

2023-03-29 07:50:12 ET

Summary

- AAR Corp. should continue to benefit from the recovery in airline industry in Q4 FY23 and beyond.

- The recent acquisition of Trax is a step towards AIR’s digitalization strategy.

- AIR stock is fairly valued, hence, I have a hold rating.

Investment Thesis

AAR Corp. ( AIR ) appears to be well-positioned to benefit from the recovering airline industry, with continued healthy demand for its MRO parts. With the industry still not fully recovered to pre-COVID levels, there is an opportunity for AIR to see growth in the upcoming Q4 FY23 and beyond. The recent acquisition of Trax , a leading provider of MRO software for aircraft, is a positive move towards digitalization, which should enable AAR Corp. to better serve its customers. All in all, the company's growth prospects look promising. However, I have a hold rating as the stock is currently trading at a fair valuation.

Financial Performance Review

AAR Corp. recently announced its financial results for the third quarter of FY23, which exceeded market expectations. During the quarter, the company witnessed a significant YoY revenue growth of 15% to $521.1 mn, beating the consensus estimate of $485.56 mn. The primary reason for this increase in revenue was the rise in commercial activities, partially offset by the decline in government sales caused by the completion of certain government projects in the previous fiscal year.

Furthermore, the adjusted EPS grew 19% Y/Y to $0.75, surpassing the market consensus of $0.72. This growth was fueled by an improvement in the adjusted operating margin and a lower share count. Additionally, the adjusted gross margin increased by 80 bps Y/Y to 18.1% due to the exceptional performance in parts supply and MRO activities, along with improved recovery in overhead costs on government contracts. Lastly, the adjusted operating margin also saw an increase of 90 bps Y/Y to 7.6% due to the improvement in gross margin and SG&A expenses as a percentage of sales.

Outlook

The sales of aviation products and services to commercial airline customers are generally affected by many factors, such as

-

The number, type, and average age of aircraft in service,

-

The levels of aircraft utilization (e.g., frequency of schedules, flying hours, and take-off and landing cycles),

-

The number of airline operators,

-

The general economy, and

-

The level of sales of new and used aircraft.

The airline industry has been on a recovery over the past two years, however, it has not yet reached pre-covid levels. AIR's commercial business, which contributes approximately 65% to the total revenue, is benefiting from the continued recovery in commercial flying. The latest data from the International Air Transport Association ((IATA)) for January 2023 indicates a positive trend, with global air traffic reaching 84.2% of January 2019 levels. The growth in Revenue Passenger Kilometers (RPK) is also encouraging, with a 67% increase compared to January 2022, indicating a strong demand for air travel.

AIR's USM activities have been a key driver of growth, especially as the airline industry recovers from the impact of the pandemic. The company's strategic investments in used parts for aftermarket services have paid off, and the increasing demand for MRO services has further fueled the growth of its USM activities. In addition, as the supply chain challenges ease and engine green time (remaining time after the engine has been removed from the aircraft) availability decreases, AIR is well-positioned to capture a larger share of the USM market. The company's focus on innovation and continuous improvement has enabled it to adapt to changing market conditions and provide value to its customers.

AIR's government business, which contributes the remaining 35% of the total revenue, is experiencing tough year-over-year comparisons due to the United States' exit from Afghanistan and the natural completion of certain programs in the previous fiscal year. However, the company has been able to partially offset these headwinds through some short-term projects, such as inventory management and repair services.

In Q4 FY23, I believe revenue should increase in the low teens due to the increasing demand for MRO parts in commercial aerospace and the recent acquisition of Trax, partially offset by the absence of projects in government business. Beyond FY23, I believe the recovery in the airline industry and the resilient aftermarket business should benefit the company's revenues. Additionally, USM activity is picking up the pace, which should act as a tailwind for the company. AIR is also successfully winning new long-term agreements in both commercial and government markets. The company was awarded an exclusive distribution agreement with Collins Aerospace's Goodrich De-Icing & Specialty Heating Systems business. Under this agreement, the company provides airlines, business jet operators, and other aircraft operators, as well as MRO facilities globally, with de-icers and supporting products. The company was also awarded a five-year renewal of its power-by-the-hour component pool and repair support program for FlyDubai's fleet of 33 Boeing 737NG aircraft.

On the government side of the business, in 2022, AIR was awarded a contract from the Air Force to support the United States Air Forces in Europe ("USAFE") F-16 aircraft. This $365 million, 10-year contract provides for F-16 depot work as well as Service Life Extension Program modifications and maintenance. Overall, I believe AIR is well-positioned to capitalize on the recovery in the aviation industry, with a strong portfolio of long-term contracts and successful new business wins.

Trax Acquisition

Recently, AIR acquired Trax Corporation, which is a leading third-party independent provider of aircraft MRO and fleet management software. Trax supports approximately 100 customers and 5000 aircraft, providing critical software for managing an entire spectrum of maintenance activities. This acquisition will accelerate AIR's digital strategy by adding a platform to bring additional software tools and analytical solutions to its customers and creating a unique channel for AIR's products.

Trax's eMRO product, a web-based enterprise MRO software solution, manages aircraft maintenance and fleet management, including inventory planning and purchasing, maintenance scheduling, engineering, work order processing, mobile task cards, electronic log books, and personnel management. The system is used by thousands of buyers and planners at airlines worldwide, making it an excellent addition to AIR's portfolio.

Trax generated $25 million in revenue in 2022, with approximately 35% EBITDA margins. AIR acquired Trax for $120 million cash upfront, with an additional $20 million earnout based on its revenue performance in 2023 and 2024. While the purchase multiple of 14x LTM EBITDA may seem expensive, the revenue synergies generated by this acquisition should be accretive to AIR in the long run.

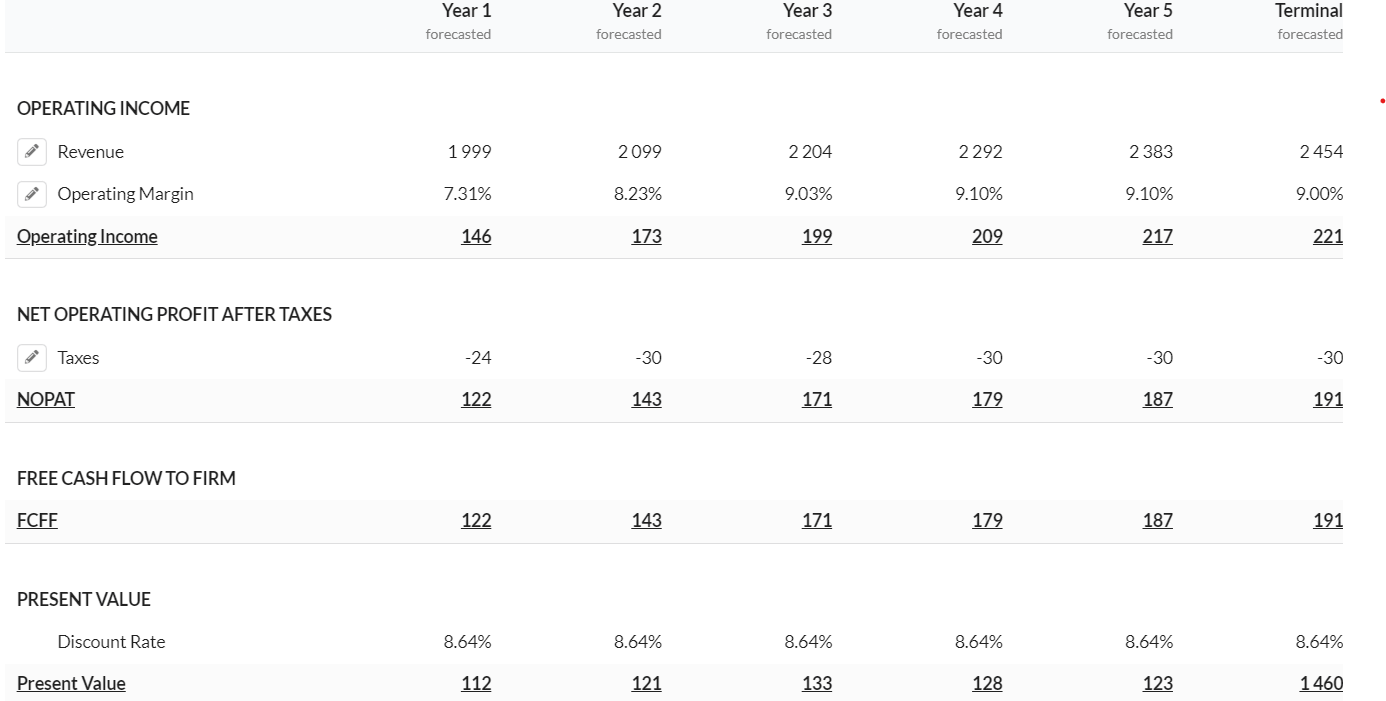

Valuation

DCF valuation (Created by DzD Analysis using Alpha Spread)

{kind=link}

In my DCF calculations, I am assuming revenue growth to be in the high single digits in FY24, given the healthy demand in MRO activities and the acquisition of Trax. Beyond FY24, I have assumed growth to be in the mid single digits, with a terminal growth rate in the low single digits as the recovery to pre-pandemic levels gets completed. I have assumed the operating margins will improve in FY24 and beyond. I used a discount rate of 8.64% by using the cost of equity of 9.37%, which is below the industry level, and arrived at a fair value of $54.94 for AIR.

Conclusion

In my opinion, the current valuation of the stock seems reasonable, and I would recommend a hold rating despite the solid growth prospects. The aviation industry is gradually recovering, and air traffic is not yet at pre-pandemic levels. This situation has created a healthy demand for MRO activities in the commercial sector, which should support the company's revenues.

Moreover, the company has long-term contracts with both commercial and government customers, which is a positive indicator for its future revenue streams. The recent acquisition of Trax is another positive development, as it will help the company add new customers and serve its existing ones more efficiently. Overall, I am optimistic about the company's growth prospects, but I would recommend waiting for a better entry point before considering a buy position.

For further details see:

AAR Corp.: A Good Company But Not The Right Time To Enter