AIR - AAR Corp.: Financial Turnaround Is Coming

Summary

- The company's earnings were affected by Covid-19 in FY2021 because of its dependency on a commercial aviation market customer.

- The company has signed a two-year contract with the Norwegian Defence Logistics Organization to offer the Royal Norwegian Air Force P-8A aircraft fleet's commercial common parts.

- The company has also received a contract from the US Air Force to manufacture and sell Next Generation All Aluminum Cargo Pallets.

Investment Thesis

AAR Corporation ( AIR ) provides products and services to commercial aviation and defense markets. The company is experiencing strong growth, helping it to recover from the negative effect of Covid-19. The company has received two new contracts, which can significantly boost financials.

About AAR Corporation

AIR offers products and services to global commercial aviation and defense markets. The company operates its business through two segments: Aviation Services and Expeditionary Services. The company offers aftermarket support and services such as MRO, Engineering services, inventory management, and distribution services to the defense and commercial aviation market through Aviation Services segment. To clients in the commercial aviation industry and government & defense sector, the business offers and rents a comprehensive range of new, overhauled, rebuilt engines and aircraft & their components. The Expeditionary Services segment primarily provides products and services to support the logistics & movement of equipment and personnel by the USA, foreign governments, and non-governmental organizations. The company produces and restores transportation pallets, containers, and shelters which are utilized in military & humanitarian tactical operations. The company generates 95% of the revenue from the Aviation Services segment and 5% of the total sales from Expeditionary Services. The company earns 59.2% of the total revenue from product sales, while 40.8% of the revenue comes from sales of services. The company's earnings were affected by Covid-19 in FY2021 because of its dependency on a commercial aviation market customer.

Sales and Earnings Trends

{kind=link}

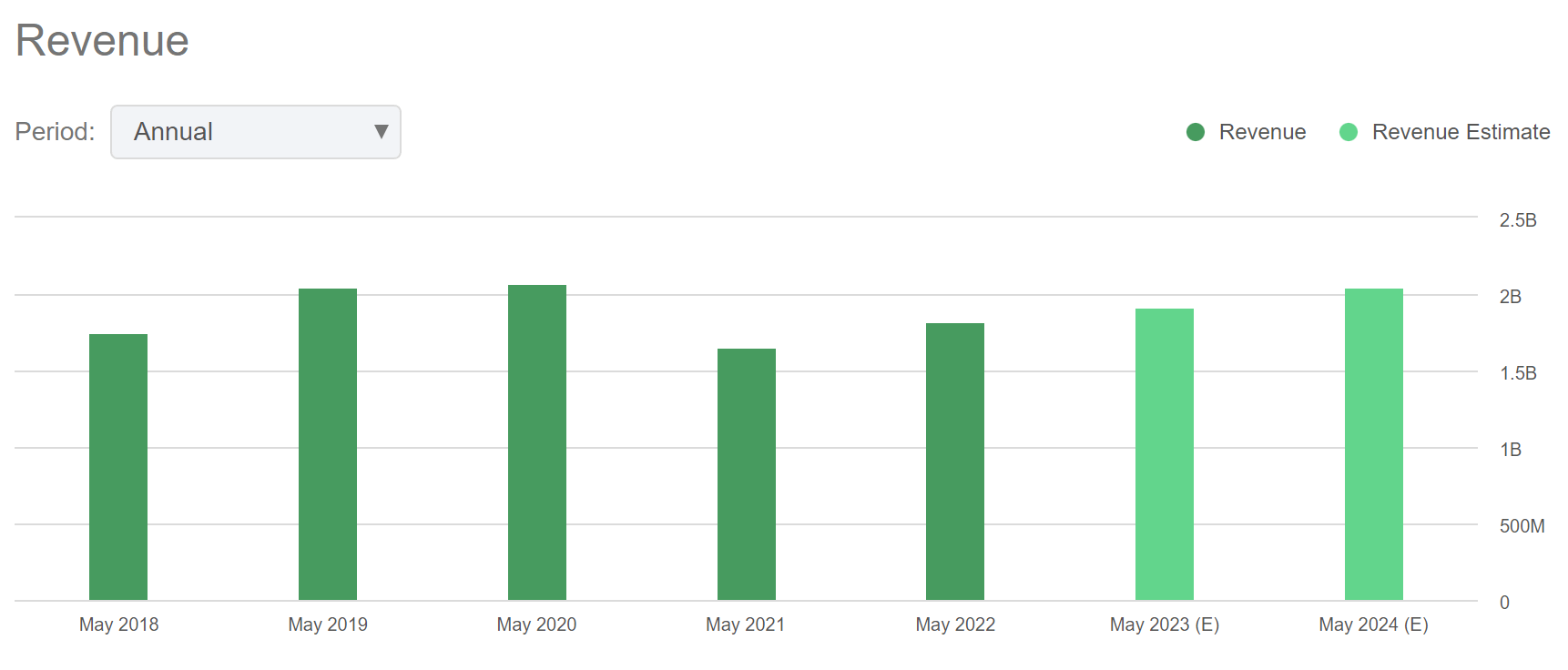

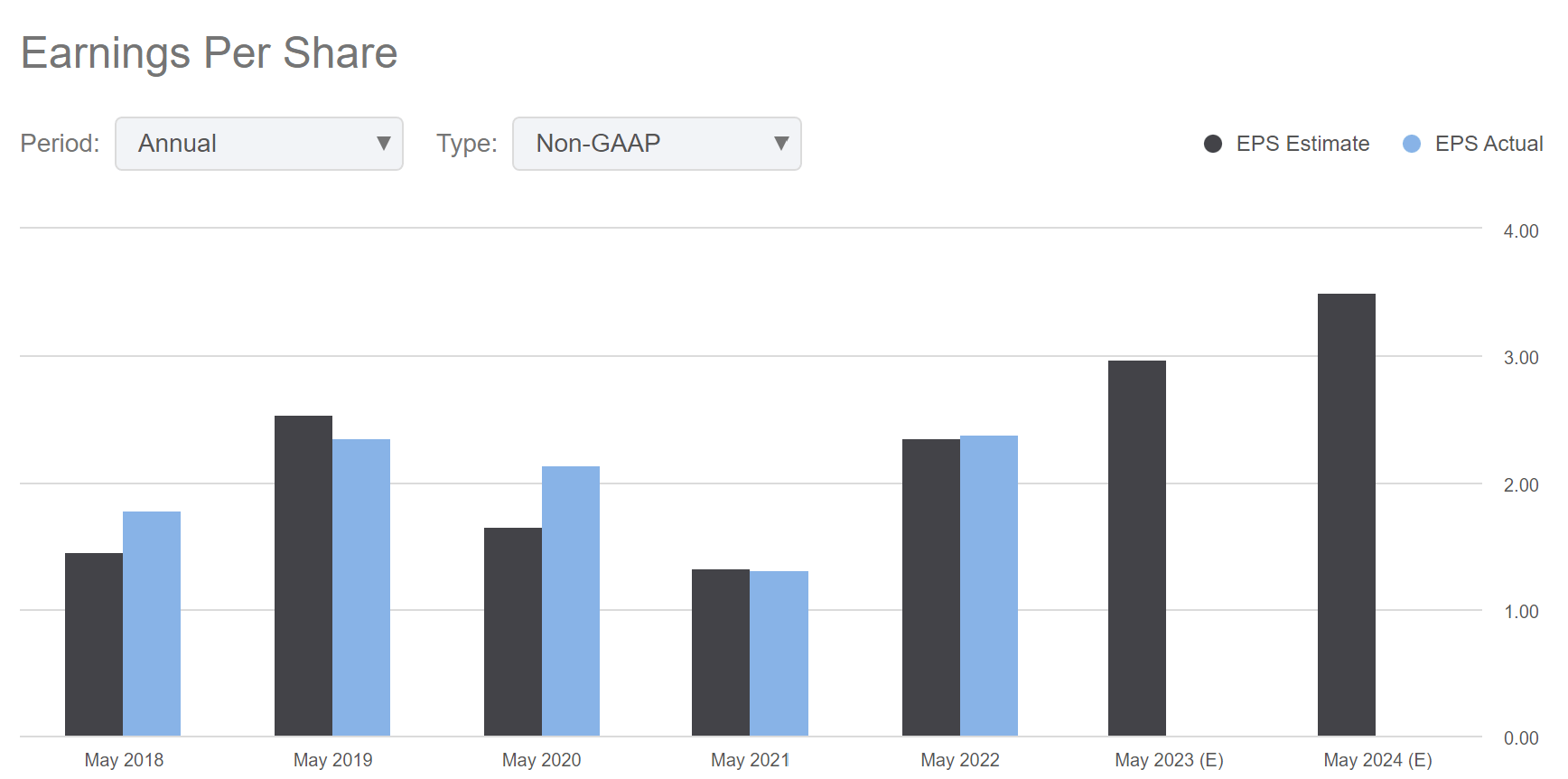

The company's revenue has increased by 10.30% in FY2022 compared to the revenue of FY2021. The 3-year revenue CAGR of the company is -3.92%, influenced by the sudden revenue decrease in FY2021, which I think was due to the adverse effect of Covid-19 on commercial aviation. The company's large chunk of its earnings is dependent on the commercial aviation industry. As we can see in the above chart, the revenue of FY2021 was 20% lower compared to FY2020. We can also observe the same negative effect of Covid-19 on the company's EPS. In FY2021, the company's EPS decreased by 39% compared to the EPS of FY2021.

{kind=link}

I believe the demand for the company products is recovering as the company's earnings have improved significantly. The sale from the company's commercial customers in FY2022 has increased by $277.4 million , which is a 34.4% increase compared to FY2021. The EPS of FY2022 has already exceeded pre-pandemic levels with the help of margin expansion due to rising product demand and the optimized portfolio of the company. However, revenue is still below its pre-pandemic levels. According to Seeking Alpha , the revenue growth might be flat and stay below pre-pandemic levels for the next two years. But I think it can exceed the pre-pandemic level sales as the company has recently received two new orders from the government & defense sectors, which can significantly increase its earnings. I think the rising demand of the company can lead to margin expansion as it can help the company to achieve economies of scale. After considering all these factors, I believe the recovering demand and earnings of the company can act as a significant growth factor in the coming years.

New Contracts

Recently, the company has received two new orders from the government & defense market. These new orders can increase earnings significantly, as both orders are long-term and big. The company has signed a two-year contract with the Norwegian Defence Logistics Organisation to offer the Royal Norwegian Air Force P-8A aircraft fleet's commercial common parts. The contract also includes the initial and ongoing provisioning demands for B-737 Next Generation ((NG)) series aircraft. The company will help in spares forecasting & material management and manage the fleet's maintenance, repair, and inspection. I believe the order is significant for the company, as this contract has expanded the company's business into government programs outside of the USA. The company has also received a contract from the USA Air Force to manufacture and sell Next Generation All Aluminum Cargo Pallets. The new aluminum cargo pallet is a replacement for the legacy 463L pallet. The pallets are made to be loaded and unloaded onto a range of commercial and military aircraft. Throughout the transition to the new generation pallet over the following few years, AIR will continue to provide legacy 463L pallets. I believe this deal can boost revenue growth as the total contract value is $173.5 million , which is approximately 10% of the last year's revenue. I think with the rising demand, the investors can expect the revenue to exceed the pre-pandemic levels, and these two contracts might be a significant contributor to revenue growth.

What Is The Main Risk Faced By AIR?

Dependency on Commercial Aviation Industry

The company was significantly impacted by the general economic climate of that sector as a supplier of products & services to the commercial aviation industry. Geopolitical tensions, wars and conflicts, weather-related occurrences, pandemics, disruptions to oil & gas manufacturing and supply scarcity, high fuel prices, and cost inflation circumstances have adversely impacted the commercial aviation sector in the past. Some of the company's clients had occasionally declared bankruptcy protection or shut down due to these and other circumstances. Airlines may decide to limit their local or international capacity as a result of the effects of instability in the world financial markets. Reduced demand for parts maintenance and support operations for the aircraft might result from a decrease in the operating fleet of aircraft, both domestically and internationally. As was recently observed during the past two years during the COVID-19 epidemic, a deteriorating aviation environment may also lead to new airline bankruptcies. In such cases, the company may not be able to collect existing accounts receivable fully. If customers' demand decreases due to the sluggish economy, which includes stringent credit requirements and client bankruptcies, it might adversely affect the company's financial health or operational outcomes.

Valuation

The rising product demand and new contracts can drive the company's growth in the coming years. The company trades at $41 with a trailing P/E ratio of 13.77x. I believe with the new contracts and rising demand for the products, the company can exceed the pre-pandemic level of sales and EPS. After considering these factors, I think the EPS of FY2023 might be $3.30, which gives the forward P/E ratio of 12.42x. The sector median is 15.32x, which is 23.3% higher compared to the forward P/E ratio of the company. The comparison of the forward P/E ratio and sector median is enough to tell us that the company is undervalued. I believe the company has strong growth prospects, but due to rising inflation and geopolitical tensions, it might fail to trade above the sector median P/E ratio of 15.32x. After considering all these factors, I believe the company can trade at a P/E ratio of 15.32x, which gives the target price of $50.60, representing a 23.4% upside from the current share price.

Conclusion

The company is recovering from the adverse impact of Covid-19 with the help of rising demand. I believe the company can exceed the pre-pandemic sales levels with the help of new long-term contracts. The company is undervalued as its forward P/E ratio is significantly lower compared to its sector's median. The company is facing weak momentum due to economic headwinds and geopolitical tension, but I think the risk-reward is still favorable. After considering all these factors, I assign a buy rating for AIR.

For further details see:

AAR Corp.: Financial Turnaround Is Coming