AIR - AAR Corp.: Solid Q2 FY23 Results And Attractive Valuation

Summary

- AIR posted solid Q2 FY23 results witnessing a consistent revenue and income growth y-o-y.

- The company beat the second quarter revenue and EPS estimates by 1.52% and 1.85% respectively.

- It recently won several new contracts which are expected to drive future growth and help the company maintain its growth trajectory.

- AIR is trading at a significantly cheaper valuation compared to its peers with a forward multiple of 15.5x.

- I assign a Buy rating on AIR after taking into consideration all its growth and risk factors.

Investment Thesis

AAR Corp. ( AIR ), a player in the aerospace and defense industry, was founded in 1951 and is headquartered in Wood Dale, Illinois. The company reported impressive Q2 FY23 results showing improvement on most parameters. I believe the stock is undervalued and can provide significant returns in 2023, so I assign a Buy rating on AIR. In this report, I will also discuss the company's financial development and its future growth potential.

Company Overview

AIR is a global aerospace and defense solution company that provides products and services to government and defense markets worldwide. It operates in two segments: Aviation Services and Expeditionary services. In the aviation services segment, it provides inventory management and distribution services, aftermarket support and services, and engineering services. In this segment, it also sells and leases repaired engine and airframe parts and provide inventory and repair programs, airframe inspection, maintenance, painting, airframe modification, exterior, and interior refurbishment. In the expeditionary services segment, ARR designs and repairs transportation pallets and shelters and provides system integration services for command-and-control systems. It serves local and foreign passenger airlines, regional and commuter airlines, aircraft leasing companies, and domestic and foreign military customers.

Q2 FY23 Result Analysis

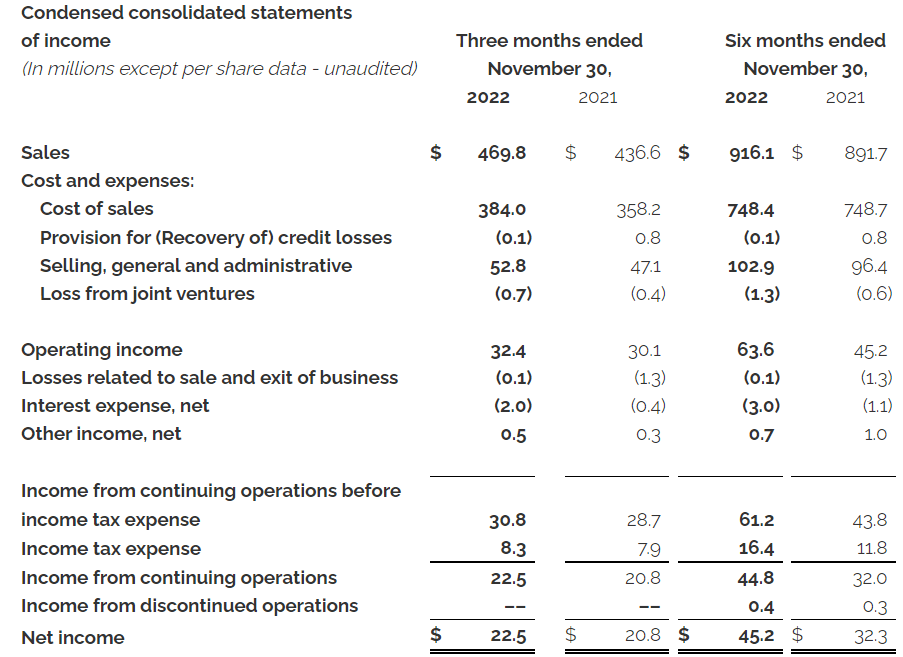

AIR recently posted its Q2 FY23 results that beat the market EPS estimate by 1.85% and the revenue estimate by 1.52%. Net income for Q2 FY23 was $469.8 million, a rise of 7.6% compared to Q2 FY22. I believe the primary reason behind the increase was a rise in sales to commercial customers, which rose by 21% compared to the corresponding quarter of last year. I think the increase in commercial sales was due to the strong demand for their repair and overhaul services. The net income for the quarter was $22.5 million, a rise of 8.1% compared to Q2 FY22. I believe the primary reason behind the rise was an increase in the company's new parts distribution activities. The diluted EPS for Q2 FY23 was $0.64, an increase of 10.3% compared to Q2 FY22.

{kind=link}

AIR's Investor Relations

Sales to the government segment however saw a drop of 12% in Q2 FY23, and I believe the main reason behind the fall was the completion of specific government programs like the Afghanistan project. Overall, in my opinion, the company's performance in Q2 FY23 was quite impressive.

Technical Analysis

{kind=link}

Trading View

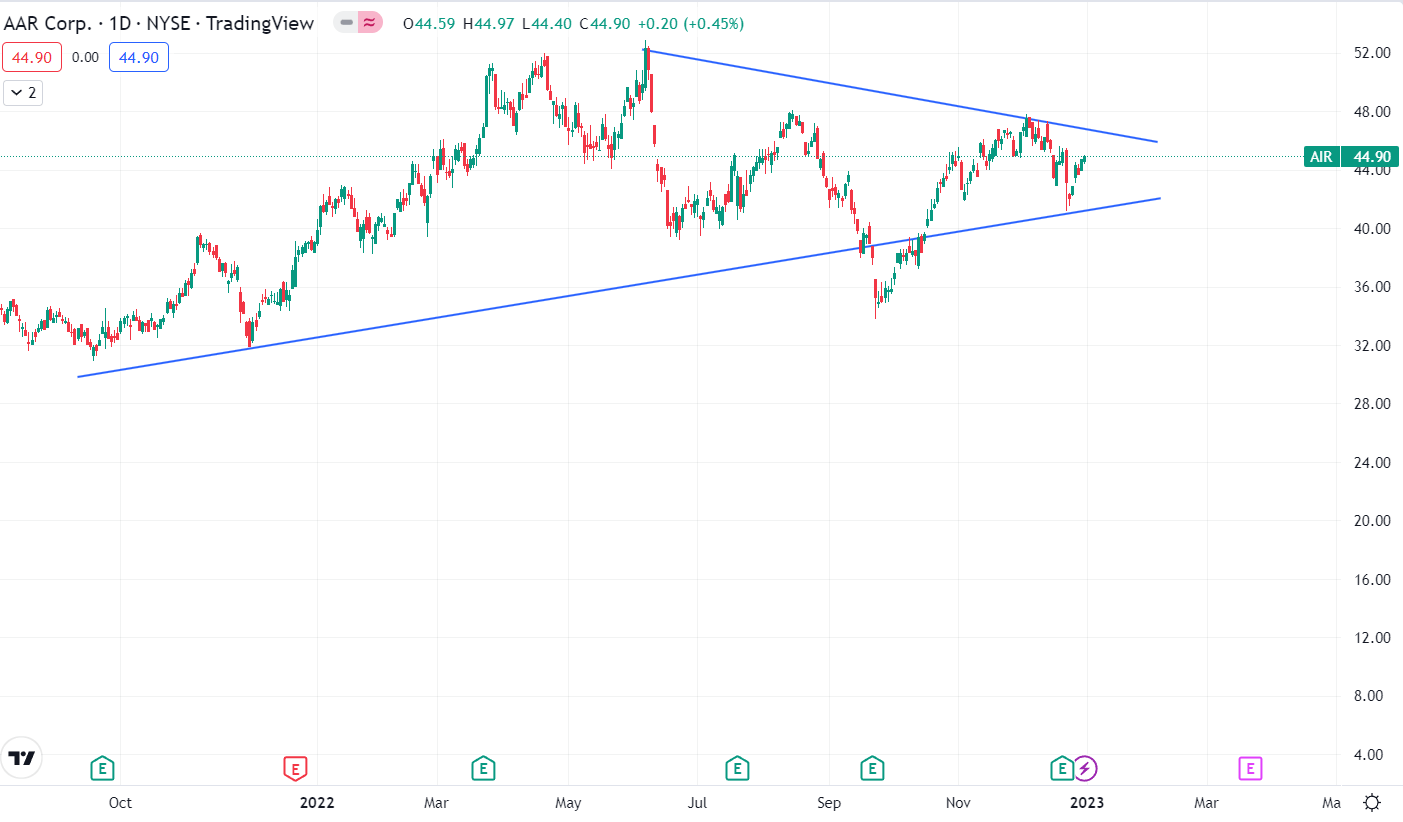

AIR is trading at the level of $44.90. It has risen 17% since January 2022. Now the stock has created a beautiful triangle pattern, and, in my view, if the stock manages to break the upper trend line, then we can see fresh momentum in the stock. There is a major resistance zone at $49, and if the stock manages to break it, then we might see a new all-time high. So, in my view, one should wait for the stock to give closing above $49 in a daily time frame to make new positions. Talking about the downside risk, there is a strong support zone at the level of $40 which reflects a limited downside risk.

Valuation Analysis - Peer Comparison

In this section, I will compare AIR with four companies in its sector: 1) Kratos Defense & Security Solutions ( KTOS ), 2) Rocket Lab USA ( RKLB ), 3) Embraer ( ERJ ), and 4) Virgin Galactic Holdings ( SPCE ), which will give us a fair idea about the company. In the last one year, while all four companies in the peer group failed to give returns to their shareholders, AIR was the only one that gave returns of 16.45%. Returns of its peers in the last one year were as follows: KTOS -46.5%, RKLB -68.6%, ERJ -38.28%, and SPCE -74.84%. This shows the potential of AIR and its ability to perform in a volatile market.

Talking about the valuation part, AIR has a P/E ((TTM)) ratio of 16.94x and KTOS 33.29x. The rest of the companies have a negative P/E ratio, which shows that AIR is undervalued when compared to its peers.

A Price / Sales ratio below 1 is considered suitable for a company; the lower the better. AIR has a Price / Sales ((TTM)) ratio of 0.86x, KTOS has a ratio of 1.51x, RKLB 9.30x, ERJ 0.53x, and SPCE 570.6x. As per my analysis after looking at all the valuation metrics, I think AIR is undervalued compared to its peers.

Now let us talk about the company’s future growth estimates. With the current revenue growth of AIR and its consistent performance in the past, I estimate the FY23 EPS to be in the range of $2.90-$2.93.This gives us a forward P/E multiple of 15.5x at the current share price of $45. This forward P/E multiple of 15.5x is significantly lower compared to the industry standards. This reflects that the company is expected to perform better than its peers and still trade at a lower valuation. I believe that AIR has significant upside potential with respect to its current valuation, which gives investors an opportunity to invest in a growth company with low-risk exposure trading at a cheaper valuation than its peers.

Additional Catalysts

AIR recovered well after the pandemic. Its FY22 revenue was 10.3% higher than the FY21 figure. The estimated revenue for FY23 is $1.92 billion, which is 5.5% higher than the FY22 revenue. I believe with the removal of travel restrictions and increasing travel demand, the company might see a rise in demand for its aftermarket services, which will help it achieve its revenue targets. In r ecent times, AIR has won contracts that will increase its revenues in the future - 1) Expansion of their distribution agreement with Union Industries, which will help them broaden their distribution of select Union ignitor plugs, harnesses, and related spare parts. 2) Contract with flydubai, 3) Subsidiary Airinmar's agreement with Cebu Pacific, 4) Extension of their distribution relationship with Leach International Corp. As per my analysis, these contracts will increase the company's net income and revenues. With growing revenue, AIR will be able to pay off debts which will decrease its interest expense and will positively impact the balance sheet. The optimistic revenue guidance by the management and the recent contracts won show that the company is on the right growth trajectory.

I believe ownership pattern says a lot about a company. I would consider a company where institutions own more than 65% of the stake in a company a safe and suitable investment option. If we look at the shareholding pattern, institutions own 95% of AIR shares, which is a positive sign. In 2021 the company announced a share repurchase program worth $150 million, and in Q2 FY23, purchased shares worth $28.2 million increasing its stake. They are yet to purchase shares worth $57.6 million which shows the management's trust in the company.

Risk

The aviation business sector is very uncertain and volatile. A pandemic or global conflict-like situation can adversely affect the aviation sector. Due to the COVID pandemic, there were travel restrictions worldwide, due to which the company’s balance sheet was negatively impacted. Although countries have lifted travel restrictions after the vaccine, travel remains well below pre-pandemic levels. AIR operates in various countries, and global situations can impact the company’s operations. Restrictions on Russia by Europe and the United States and the Taliban taking over Afghanistan have reduced the company's business operations, affecting its revenue. Increasing tension between the US and China over Taiwan and rising global conflict make the aviation business uncertain.

Final Take

AIR has delivered strong Q2 FY23 results, and the management is optimistic about the company’s revenue growth. Revenue and net income are growing every quarter, and I believe with the recent contracts won by the company and increasing travel worldwide, AIR will continue to do better financially in upcoming quarters. The stock is trading at a lower valuation than peers, and is technically looking strong. As per my analysis, the company is looking strong and can be a good bet for 2023; it can provide significant returns in the short term. I therefore assign a Buy rating on AIR.

For further details see:

AAR Corp.: Solid Q2 FY23 Results And Attractive Valuation