ABBV - AbbVie: Get Ready For More Painful Downside

2023-11-30 09:45:00 ET

Summary

- AbbVie's ex-Humira growth products showed solid growth in Q3, boosting management's confidence in their success.

- The company upgraded its guidance, raised its full-year revenue estimates, and adjusted its EPS outlook.

- AbbVie stock has been impacted by industry rotation and macroeconomic headwinds, but its profitability grade supports confidence in a subsequent recovery.

- I argue why the contrarian setup isn't timely, as ABBV isn't priced at a steep discount. Its forward dividend yield is also far from appealing to income investors.

- While the risk/reward is pretty balanced at the current levels, the potential for further painful downside has intensified. Don't try catching the falling knife now.

AbbVie Inc. (ABBV) investors must wonder what it must take for market participants to move past the company's Humira headwinds to focus on its ex-Humira growth products instead. Therefore, I'm pleasantly surprised with the announcement earlier today that AbbVie will acquire Immunogen ( IMGN ) for about $10B in cash. AbbVie will pay a price of $31.26 per share, which saw surge to more than $29 in pre-market trading, reflecting the market's confidence in the deal's closure.

AbbVie's acquisition will see the company gain access to Immunogen's antibody-drug conjugates or ADC portfolio. As a result, it's clear that AbbVie likely saw the need to bolster the growth profile in its current cancer portfolio and pipeline in meeting its medium- and long-term growth outlook. AbbVie has significant firepower in consummating the acquisition (estimated adjusted EBITDA leverage ratio of 1.5x for FY24) and reported a cash and equivalents position of $13.3B in Q3.

However, it came after management alluded in its Q3 conference call that it remains in a " strong position and has confidence in the performance of the ex-Humira growth platform." Still, management kept the opportunity open for business development and M&A activities to acquire "assets that can contribute to incremental pipeline and revenue growth in the later part of the decade and into the 2030s." Therefore, I believe the acquisition of IMGN is intended to be in this direction, bolstering investors' confidence in its long-term game plan.

I presented in my previous update in early September, stressing that it was time to turn cautious on the leading biopharma company. I argued then that while ABBV recovered dramatically from its July 2023 lows, its valuation was no longer as attractive. As a result, I downgraded ABBV from a Buy posture to a Hold, suggesting investors wait patiently for another opportunity to assess a Buy entry.

Since my last update, that caution has panned out, as ABBV underperformed the S&P 500 ( SPX ) ( SPY ). As a result, I believe it's apt for me to update ABBV holders on whether it's timely for them to consider adding to their positions.

Interestingly, AbbVie posted remarkable earnings results in the third quarter or FQ3 in late October 2023, outperforming its internal forecasts. Accordingly, AbbVie posted an adjusted EPS of $2.95. The company also delivered solid growth in its ex-Humira growth portfolio, up 12% YoY. As a result, it bolstered management's confidence in Skyrizi and Rinvoq as part of its immunology platform, as they "achieved over 50% growth, contributing significantly to this platform's success."

Management anticipates that "Skyrizi and Rinvoq are expected to surpass Humira's peak revenues by 2027 collectively." To sweeten the outlook for investors, AbbVie also upgraded its guidance, raising its "full-year revenue guidance by $600 million." In addition, the company also lifted its full-year adjusted EPS to a range of between $11.19 and $11.23, for a midpoint outlook of $11.21. It also bolstered investors' confidence about its momentum for 2024, underscoring an adjusted EPS floor of $11, up from $10.7 previously.

As a result, AbbVie has demonstrated to investors that the company remains committed to overcoming the headwinds from Humira's biosimilar competition, given its robust platform and pipeline.

However, I gleaned that AbbVie and some of its leading pharma peers have suffered in 2023 as healthcare investors likely rotated out and moved into the outperforming pair of Novo Nordisk ( NVO ) and Eli Lilly ( LLY ). Furthermore, while ABBV is an S&P 500 Dividend Aristocrat member, its forward dividend yield of 4.5% isn't considered attractive enough relative to its 10Y average of 4.2%. Moreover, in the current interest rate environment, when the 2Y ( US2Y ) still yields 4.65% despite the recent pullback, it's a tough call to expect income investors to be particularly interested in ABBV's forward yields.

As a result, I gleaned that a combination of company-specific challenges (Humira), industry rotation, and macroeconomic headwinds have likely impacted investors' confidence in ABBV.

However, AbbVie's best-in-class "A+" profitability grade should underpin investors' confidence about ABBV's subsequent recovery as these headwinds begin normalizing. ABBV's "C-" valuation grade corroborates my conviction that dip buyers could lurk and wait for a more attractive opportunity to pounce.

{kind=link}

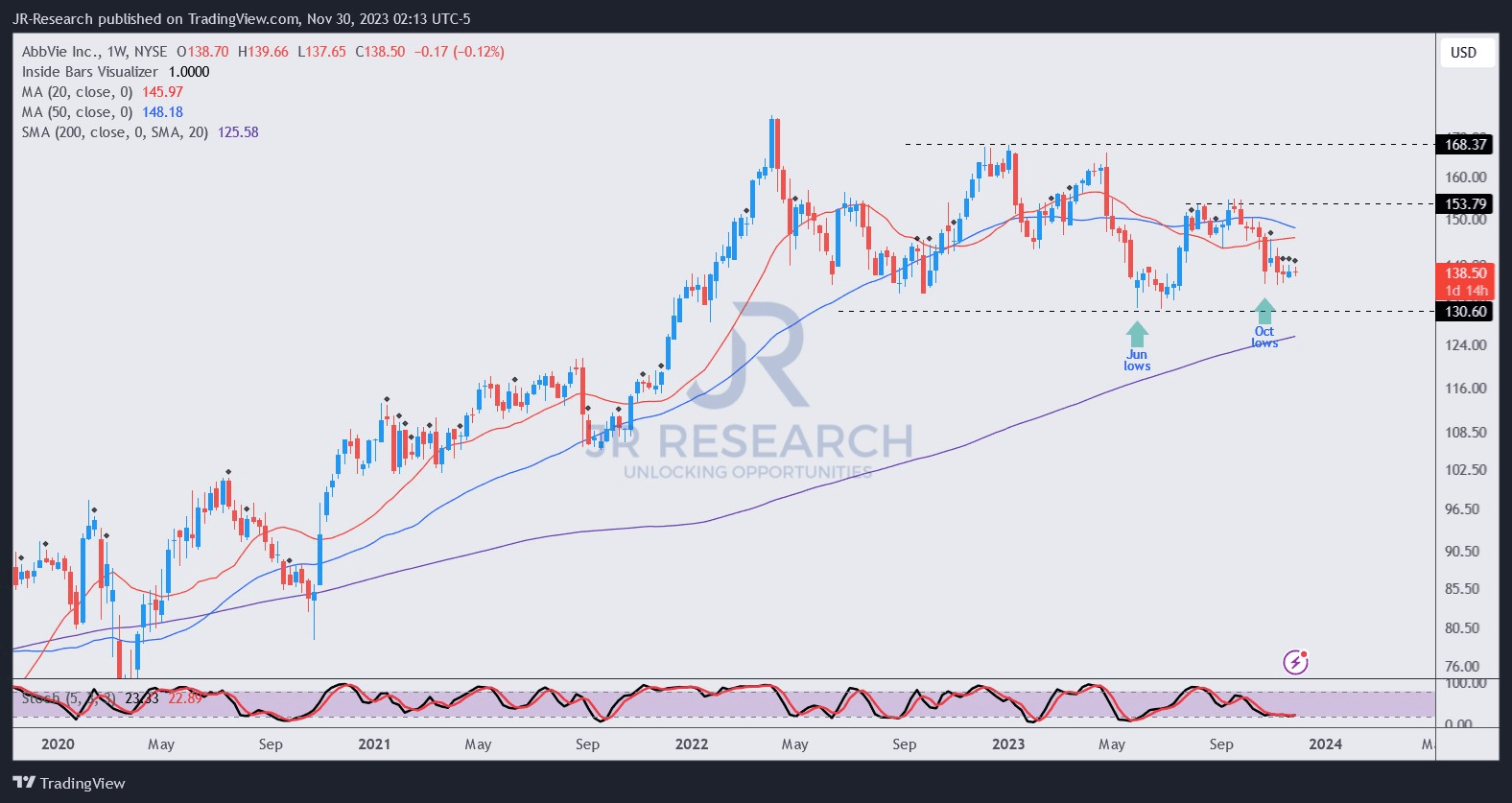

ABBV's price action is mixed. While its June low ($130 level) remains supported, buyers' inability to move above the $154 level before it pulled back is a yellow flag (caution, but no sell signal yet).

As a result, I anticipate potential downside volatility, possibly re-testing ABBV's June low if pharma investors continue rotating out. It's increasingly clear that ABBV has lost its medium-term uptrend. Moreover, the lack of a valuation dislocation could discourage value investors from exploiting the recent pullback.

Therefore, I assessed that ABBV's current buy levels appear to be pretty well-balanced and, thus, not sufficient for me to upgrade my thesis.

Rating: Maintain Hold.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking and note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn't? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

For further details see:

AbbVie: Get Ready For More Painful Downside