ABCL - AbCellera: Difficult 2023 Suggests Business Model Should Pivot In 2024

2023-12-08 01:30:09 ET

Summary

- AbCellera's stock has decreased by 34% since I gave it a "sell" rating in March.

- The company's high valuation was largely based on its success discovering the COVID antiviral bamlanivimab, which earned >$4bn revenues but has since been withdrawn from the market.

- Royalties on bamlanivimab revenues helped ABCellera earn >$400m in 2021 and 2022 but the company may earn <$50m this year.

- AbCellera's business model of discovering blockbuster drugs for partners is unsustainable, and the company should focus on developing its own drugs.

- Encouragingly, management is moving its own assets into the clinic - this is the only way to win in drug development - you can't make money promising to discover blockbuster drugs in exchange for small milestone payments.

Investment Overview - AbCellera Stock Sinks As Drug Discoverer Fails To Replicate Early Success

I last covered AbCellera for Seeking Alpha back in March, giving its stock a "sell" rating and outlining a few objections I had to the Vancouver, Canada-based drug discoverer's business model. AbCellera shares have decreased in value by 34% since that note.

AbCellera ( ABCL ) began its life as a public company with an Initial Public Offering ("IPO") in December 2020 that raised ~$483m, at $20 per share, and the stock price briefly exceeded >$50 per share in January, however, it has been downhill ever since.

Much of the company's valuation - and the trigger for such a mega-money IPO - was built upon its discovery of the COVID antiviral bamlanivimab. As per the company's 2022 annual report/ 10-K submission :

we discovered bamlanivimab from a single blood sample obtained from a convalescent patient, and with our partners, advanced into clinical testing 90 days after initiation of the program. It was the first monoclonal antibody therapy to reach clinical testing and the first to receive Emergency Use Authorization, or EUA, from the U.S. Food and Drug Administration, or FDA, for the treatment of mild-to-moderate COVID-19 in high-risk patients.

The partner mentioned is Eli Lilly ( LLY ) - now the world's largest Pharma by market cap, and bamlanivimab went on to generate revenues of $2.2bn in 2021, and $2bn in 2022. AbCellera was able to report revenues of $375m in 2021, and $485m in 2022 almost entirely due to bamlanivimab royalties. The company was also able to generate healthy net income in each year of $154m, and $159m respectively.

Unfortunately, bamlanivimab was found to be ineffective against newer strains of COVID and was withdrawn from the market. So far, lightning has failed to strike twice, and in Q1, Q2 and Q3 of 2023, AbCellera has reported revenues of $12.2m, $10.1m, and $6.6m, and net income of $(40.1m), $(30.5m), and $(28.6m).

In this context, it is easy to see why the market has turned against AbCellera, and why the share price has fallen >75% below its IPO price. Nevertheless, AbCellera's market cap valuation remains at $1.4bn - is this still too high for a loss-making company driving <$50m revenues per annum?

Why It Can Be Tricky To Succeed With AbCellera's Business Model

The issue with AbCellera's business model is that it is predicated upon AbCellera helping its partners discover the next bamlanivimab, or Humira, Keytruda, or any "blockbuster" (>$1bn per annum revenue) drug. AbCellera's investor presentations make this look and sound relatively straightforward - invest heavily in technology, and watch as your drug is discovered, developed, aces its clinical studies, and becomes a blockbuster within 20 years.

The reason why Humira, Keytruda, etc. are such valuable drugs is precisely because they are so rare and difficult to develop, however. Naturally, AbCellera's founders are some of the most talented and capable drug development experts around, but even they cannot discover a bamlanivimab every year - once a decade, perhaps, which makes for a very uneven business, "feast or famine" style business model.

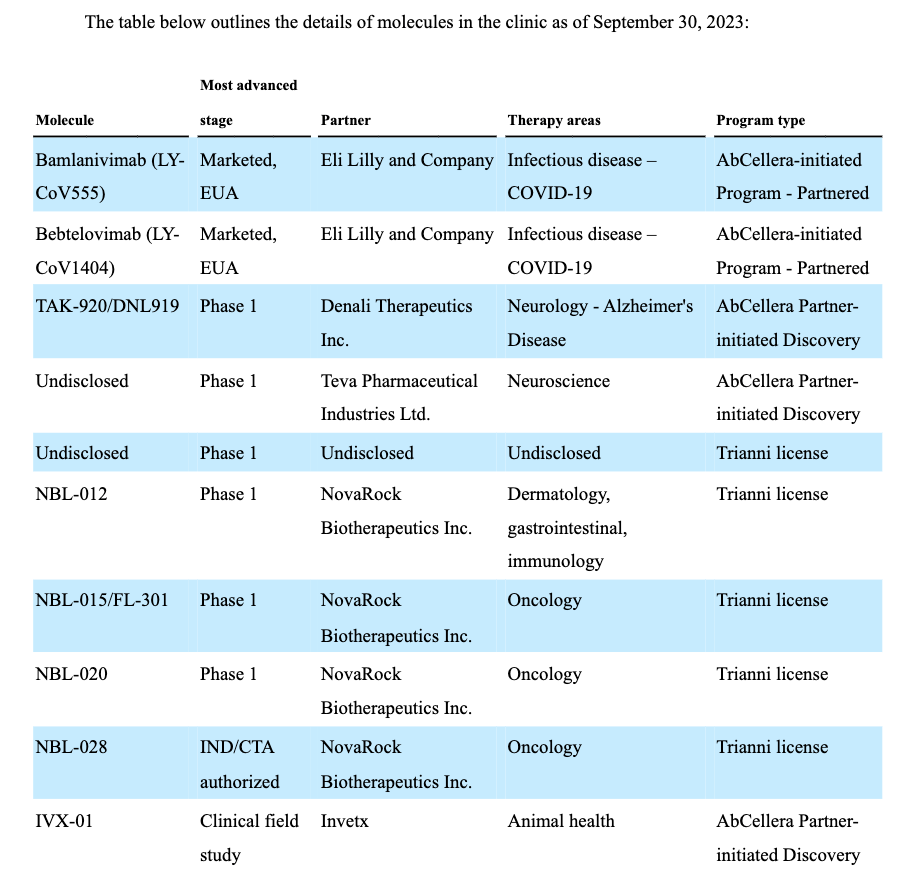

AbCellera - molecule in clinic (Q3 10Q submission)

{kind=link}

As we can see above, besides bamlanivimab and bebtelovimab, the twin COVID antibodies developed with Lilly, AbCellera has 8 molecules currently in the clinic, with 6 at the Phase 1 study stage, and 1 which has secured its investigational new drug ("IND") license, allowing in-human studies to begin.

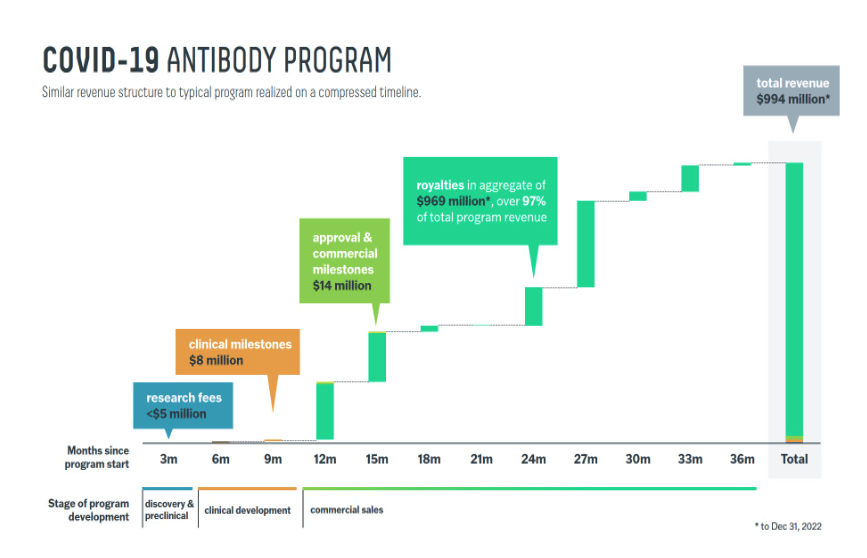

Revenue profile for COVID-19 programs (2022 10K submission)

{kind=link}

Above is a breakdown of AbCellera's earnings from its COVID-19 collaboration with Lilly, and as we can see, clinical milestone payments and even approval milestones offer slim pickings in terms of revenue, the drug under development essentially needs to become a blockbuster if AbCellera is going to realise any revenue that would justify a $1.4bn valuation.

Based on the above, even if all 6 of the clinical programs of the Phase 1 program results in approvals and commercial sales, AbCellera would generate revenues of ~$160m, and it's important to remember that bamlanivimab was developed during the pandemic when clinical development times were accelerated as never before. In the current environment, no matter how fast technology can discover novel antibodies, the clinical study process will take at least 3-5 years.

Additionally, we need to factor in the risk that one, two, or five, or even all of the clinical assets do not make it out of the clinic, due to failing studies on safety or efficacy. Statistically, it is probably most likely that they all fail, which again, makes AbCellera's business model problematic in my view.

On a more positive note, AbCellera had 182 programs under contract as of Q3, with partners including Pharma giants such as Regeneron ( REGN ), GSK ( GSK ), Moderna ( MRNA ), Gilead Sciences ( GILD ), Merck ( MRK ), and Novartis ( NVS ). The issue is that these do not seem to be proactive partnerships i.e. the companies have not agreed to work on a particular development program plan with AbCellera.

It is in fact hard to put a finger on why a large Pharma would turn to AbCellera when its own in-house drug development capabilities are also state of the art. AbCellera might argue that its powerful discovery engines are churning out promising drug candidates, but while using technology to accelerate the process of drug discovery is a valid idea, the hit rate is far too low for it to be considered a viable business model.

Looking Ahead - What To Expect From AbCellera Going Forward

The question is whether AbCellera can pick itself back up off of the canvas in 2024, and I would argue that the best way to do that may be to focus on its in-house programs.

For example, AbCellera says that in Q3 it:

reached a cumulative total of 182 programs under contract (up from 164 on September 30, 2022) that are either completed, in progress, or under contract with 42 different partners as of September 30, 2023 (up from 38 on September 30, 2022).

These 182 programs added up to $6.6m of revenues in Q3 or ~$36k per program. For a privately owned small business these would be good numbers, but for a $1.4bn valuation listed company that earned $485m in 2022, boasts a cash position of $886m, and has close to 500 employees, the numbers aren't big enough.

Essentially, I see two ways that AbCellera can put itself back on a path to growth. The first is to invest heavily in sales people who can go out and push the company's platform to as many pharmaceuticals and drug development companies as possible, and bring in some revenue, although the way that AbCellera currently structures its deals, it only really benefits if a drug candidate is successful, and even then, only if the drug candidate drives blockbuster revenues. If I were management, I would consider changing this structure, and charge companies higher fees from the outset for use of its technology.

The second, more favourable strategy I would pursue would be switching to developing its own drugs - as I wrote in my last note:

If you're capable of discovering drugs for numerous partners, why not simply select one yourself and develop it - surely that's a far more lucrative exit strategy?

The market has a much greater tolerance for drug developers who lose money while studying their assets in the lab and conducting clinical studies than it does for a company that views itself as a business that can achieve revenues and profitability by charging its clients for services rendered but still loses money.

Encouragingly, AbCellera appears to be doing exactly this. On the Q3 earnings call , company President and CEO told analysts:

The highlight this quarter is that we are advancing assets from two AbCellera-led programs into IND-enabling studies. The first asset, ABCL575 targets Ox40 ligand and is being developed as a potential best-in-class therapy for the treatment of atopic dermatitis and other indications in autoimmunity and inflammation.

We discovered ABCL575 during our collaboration with EQRx as part of the co-development program that was initiated in 2021. We took ownership of this program in September after EQRx was acquired by Revolution Medicines. ABCL575 has been designed with potency, PK and developability to enable less frequent dosing, which provides a potential for differentiation.

At present, we believe ABCL575 has the potential to be one of the first assets to follow amlitelimab, which is being developed by Sanofi and which recently had a positive Phase II readout providing evidence for the potential of this new class.

Ultimately, AbCellera achieved its initial incredible success by helping to discover and develop bamlanivimab - had it developed the drug itself rather than with partner Lilly, it could have earned >$4bn in 2021 and 2022, as opposed to <$1bn. The business model the company has been pursuing of discovering and developing client's drugs and only accepting payment should they become stand-out commercial successes seems wholly unsustainable and will lead to further share price devaluation, in my view.

AbCellera, which announced last week that it would let go ~10% of its staff and focus more on developing therapeutic antibodies, finally seems to be realising that as a drug developer/biotech, you can burn through hundreds of millions of shareholders' cash and still be rewarded with triple-digit percentage overnight share price gains on clinical data alone, without any requirement for actually generating revenues.

In short, in a drug discovery industry that makes very little practical sense from a financial perspective, it is infinitely better to be the biotech than the biotech's partner.

I still expect AbCellera stock to lose some value in 2024 as it gets to grips with a changing business model, but with >$850m cash to spend, the company can afford to take the initiative with some of its own programs, and may eventually reap much larger rewards by doing so.

For further details see:

AbCellera: Difficult 2023 Suggests Business Model Should Pivot In 2024