ASO - Academy Sports and Outdoors: Business Fundamentals And Outlook Turning For The Better

2023-04-21 08:02:42 ET

Summary

- Management reaffirmed their FY23 guidance. However, there may be inter-quarter volatility due to the challenging macro environment and persistent inflation rates.

- ASO anticipates opening 13 to 15 new locations in 2023 and a total of 120 to 140 new locations by 2027.

- Management anticipates a gross margin of 34 to 34.5% between 2023 and 2027, with a long-term goal of an EBIT margin of 13.5%.

Description

My original recommendation was a hold as I believed the stock was fairly valued back then. My thesis was that Academy Sports and Outdoors ( ASO ) offers a wide range of sporting and outdoor recreation products to consumers. A number of favorable trends, the majority of which resulted from the COVID-29 pandemic, are contributing significantly to the growth of ASO. ASO Analyst Day reinforced my optimistic outlook on the company. The ASO Analyst Day signaled the company's intention to shift to a strategy of store growth requiring deeper investments that will also improve FCF profile at maturity. While there are opportunities to increase sales and profits by analyzing customer data and tailoring marketing campaigns, I believe that opening new stores will be the primary growth driver in the future. I feel it's important to stress that ASO still has a lot of room to catch up to most best-in-class retailers in crucial areas like omni-channel experience and its supply chain to support the forthcoming growth. Although this indicates that ASO is falling behind, it also suggests that there is considerable room for growth and that mature earnings/FCF could be significantly higher than at present. After considering the company's new growth strategy and possible business profile at the analyst day, I have changed my recommendation from a hold to a buy.

Guidance reaffirmed

Management reaffirmation of FY23 guidance should de-risk overall consensus FY23 numbers. Net sales are expected to be between $6.5 and $6.7 billion, with SSS growth of -2% to 1%, a gross margin of 34% to 34.4%, and adjusted EPS of $7.00 to $7.75. While I agree with management's decision to reiterate full-year guidance, I am concerned about the inter-quarter volatility. Readers should be on guard for any "impact" in 1H23 due to the challenging macro environment and persistent inflation rates. The bull case is that as we move towards 2H23, things should start to turn for the better and ASO start to see sequential improvement in numbers, which could lead to the market gaining more confidence on FY23 numbers.

Store target and potential

Compared to the nine stores predicted for 2022, ASO now anticipates opening 13 to 15 new locations in 2023, with a total of 120 to 140 new locations planned by 2027 as a more long-term goal. This target was increased from the original 80-100 stores expected to open by 2026. Of these, 50-60 would be located within ASO's existing footprint and the remaining 70-80 would be located within the adjacent footprint. This roadmap, in my opinion, is an unmistakable sign of management's eagerness to prioritize expansion and strengthen the company's foothold in the market. This is a necessary step toward offering an omni-channel experience, so I fully support it. While many people think that e-commerce is the best place to start when implementing an omni-channel strategy, I maintain that a physical storefront is essential. It's an advantage that's tough to imitate because it requires a lot of time and money to duplicate 100+ stores in a similar location. Beyond this, management thinks there's room for 800+ locations nationwide in the long run. Since DKS already has 853 stores, I don't think this is an unrealistic goal.

Profitability

Management now anticipates a gross margin of 34 to 34.5% between 2023 and 2027, which I believe is achievable given DKS has a gross margin of 34.6% in FY22. Long-term, management aims for an EBIT margin of 13.5 percent. ASO's previous long-term goal for EBIT margin was at least 10%, which I find interesting. Management stated that in order to reach their goal of a 13.5% EBIT margin by 2027, they expect to gain a 40 basis point advantage from a boost in merchandise margins and a 100 basis point advantage from improvements in their supply chain. Therefore, we'll be focusing on how ASO can enhance its supply chain, which, in my opinion, is a matter of timing and execution. While ramping up the supply chain, I would expect to see pockets of margin headwinds such as investments for ecommerce fulfilment, and digital infrastructure investment.

Valuation

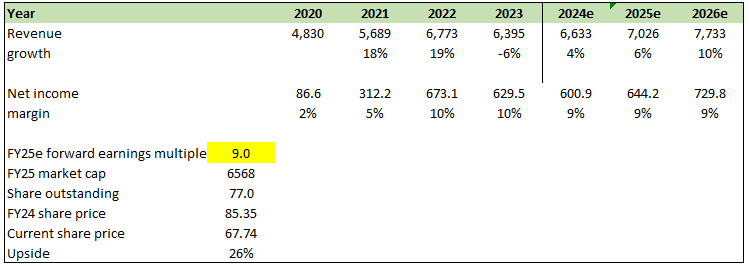

Given the new outlook and business fundamentals, I now believe ASO should trade at a premium to its historical average. Assuming it continues to trade at the current valuation of 9x and using consensus figures, ASO should be worth ~$6.6 billion in market cap in FY25. This equates to $85.35 per share.

{kind=link}

Risks

There are 2 key risks. As a first step, Nike may decide to limit or cease product distributions to ASO if the latter is viewed as a generic retail partner. A loss of customers and market share could have a negative impact on ASO's financial results and stock price if Nike products were no longer available. Second, compared to rivals, ASO's omnichannel capabilities are lacking. Although ASO is making efforts to improve its digital presence and omnichannel capabilities, failure to do so may result in the loss of customers and market share. As mentioned above, ASO's operating expenses is likely to increase while it plays catch up to rivals, which will cause headwinds to bottom line that might spook investors.

Summary

I have changed my recommendation from a hold to a buy. The company's increased store target, management's reaffirmation of FY23 guidance, and potential for growth in earnings and free cash flow make me optimistic about its future prospects. ASO current fundamentals and outlook suggests that it should trade at a premium to its historical average.

For further details see:

Academy Sports and Outdoors: Business Fundamentals And Outlook Turning For The Better