SPWH - Academy Sports and Outdoors: Cheap Growing And Poised To Triple

2023-06-20 08:20:48 ET

Summary

- Academy Sports and Outdoors trades at just over 6.0x free cash flow per share.

- The company is a high-quality sporting goods retailer with exposure to favorable macroeconomic tailwinds.

- Management has a proven track record of success and believes they can grow revenue by 50% over the next four years.

- At 10.0x earnings in 2027, ASO has a path to $170 per share, representing a 35% IRR.

Article Thesis

Academy Sports and Outdoors ( ASO ) is a sporting goods retailer with 269 locations across the southeastern United States. Despite operating in markets that have population growth more than twice the national average, generating tremendous amounts of free cash flow, and having a clear path to $10 billion in revenue - which collectively supports at least $10/share of annual free cash flow in four years' time - ASO trades at just 6.2x normalized FCF.

When the consensus narrative of ASO being an average retailer exposed to macroeconomic compression breaks as management continues to execute on their formula of low single-digit same-store-sales growth and >30 annual store openings, ASO will be in the unique position of seeing profits and trading multiples increase at the same time, potentially driving the stock to $170 by the end of 2027, representing a 35% IRR.

Map of ASO locations (ASO Investor Day)

Company Background

From 2013 to 2018, Academy suffered under an enormous debt burden brought on by KKR's leveraged buyout of the company in 2011. In my view, preserving KKR's equity and growing the store base was management's number one priority, and they let the operational side of the business slip for years.

ASO SSS and EBITDA/store (ASO Investor Day, 10-K)

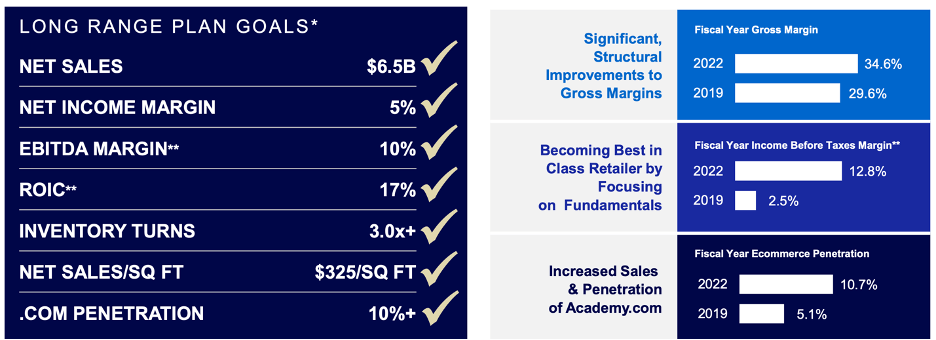

In 2018, seven years after the buyout deal had closed, Ken Hicks was brought in to turn around the company. Hicks quickly attacked the inefficient operations of Academy: increasing same-store-sales, refocusing on the returns ASO was getting on new locations, and reevaluating working capital needs. Five years after Hicks arrived, every single one of the goals he laid out for the company in 2018 had been met, and Academy had been transformed into a best-in-class retailer.

ASO 2018 goals (ASO Investor Day)

{kind=link}

ASO's Performance: Temporary or Permanent?

The ultimate question for Academy is whether their success over the past five years was the result of a mediocre business getting lucky because of extreme, one-off demand related to Covid, or a fundamental shift in the operations of Academy, transforming them into a top-tier retailer. I'm firmly in the latter camp.

Macroeconomic Reasons for Strength

The macro reasons for Academy to outperform in the long-term boils down to two factors: location and the nature of what they sell.

Location

As I mentioned earlier, ASO's biggest markets (Texas, Florida, and Georgia) are the beneficiaries of positive macroeconomic tailwinds. On top of favorable organic population growth, Florida and Texas are the number one and two states Americans are moving to, with Georgia not far behind in fifth place. Forbes attributes this dynamic to low taxes, strong local economies, and beautiful weather (quite the combo!). Additionally, for those immigrating to the United States, Texas and Florida placed second and fourth , respectively, as top destinations, with those two states alone being home to more than 9 million immigrants.

Population growth in ASO's markets (ASO Investor Day, US Census)

What Academy Sells

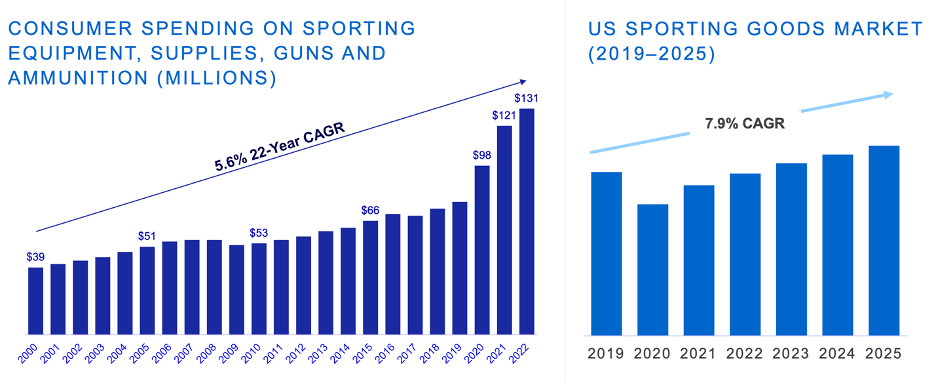

Almost everyone likes having fun outside, and so long as that's the case, Academy should continue to do well. But more than that, a lot of what ASO sells (shoes, ammunition, fishing lines, etc.) must be replaced frequently, creating a recurring-esque quality to Academy's business. This reality is reflected in the long-term growth of the sporting goods industry, which has grown at an average of 5.6% per year for two decades. Going forward, as opposed to the consensus view that folks are going to be pulling back on spending, ASO expects it to accelerate to 7.9% annual growth through 2025.

Sporting goods industry growth (ASO Investor Day, Bureau of Economic Analysis; LT PCE Categories; Morgan Stanley Proprietary Outdoor & Active Living 2022 Survey)

{kind=link}

Company Specific Reasons for Strength

On top of just ASO's general positioning in growing markets, Academy has also given investors reason to believe they can outperform for the long-term. At their April 2023 Investor Day, management laid out their strategic vision for the next four years. Simply put, it comes down to:

- Growing revenue by 50% to $10 billion through 120 - 140 new store openings and 3%+ annual SSS,

- Maintaining a 13.5% EBIT margin and 10% net margin,

- Earning a 30% return on invested capital, with a minimum 20% threshold,

- Generating $3.5 billion of cumulative free cash flow.

Coming from a top-notch management team that has historically executed upon their goals, I'm confident that Academy should be able to reach these targets, and if they come anywhere close, the consensus narrative will be broken. It's improbable that a company growing the top-line 10% per year and EPS in the mid-teens can trade at 6.2x free cash flow. What's more, if there's a hard catalyst for a rerating, say a strong summer and back-to-school season, the stock could soar as the shorts cover (currently >7.0x the average daily volume is sold short).

Additionally, while growing revenue by 50% can sound aggressive, understand that retailers do an excellent job of compounding, as both same-store-sales and the number of stores compound at the same time. Opening ~30 locations per year on its own adds 8%-12% to revenue growth, depending on how the stores perform, while growing SSS north of 3% per year easily pushes ASO ahead of the 10% annual revenue growth they'll need to achieve to reach that $10 billion revenue figure.

What's more, at their current valuation ASO doesn't need to meet these targets for investors to make a lot of money. Just re-rating to where Sportsman's Warehouse ( SPWH ) trades at ~7.0x EV/EBITDA, a low-quality peer with significant exposure to cyclical firearm sales and a management team that has done nothing to combat declining same-store sales, would drive the stock up ~25% to $62 in the short-term.

Zeroing In: Unit Level Economics

While I've written a lot about the high-level picture for Academy Sports and Outdoors, the magic really happens at the store level, where the company earns incredibly high returns on invested capital and exceptional levels of EBITDA. If you're going to invest in ASO, or any retailer for that matter, understanding unit economics is critical.

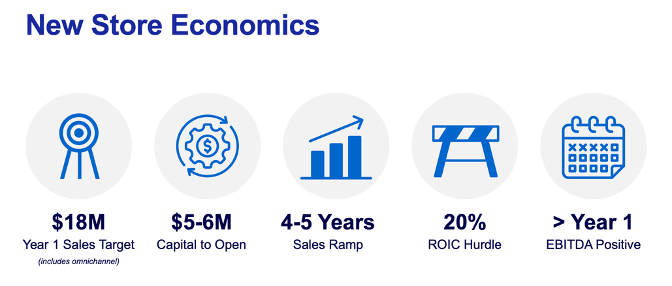

After scoping out a location, likely in a middle-class part of the southeastern United States, Academy will reach an agreement with a landlord to lease a space (the average store footprint is ~70,000 square feet).

To turn the storefront into an Academy Sports and Outdoors location and stock it with inventory, ASO will spend $5 to $6 million. In Year 1, the location will earn $18 million of sales, ramping up to $25 million in Year 4 or 5. Earning that much on a every store is driven by several factors. Firstly, like many retailers, they build out stores next to highways to help drive traffic; secondly, they confine themselves to certain demographic densities, ensuring that the size of the store correlates to the size of the town/suburb/city they're located in; and thirdly, they're so popular that they can get away running stores more than 50% larger than peers without seeing any harm done to sales per square foot.

Now, on that $5 to $6 million investment, Academy will earn $4 million in EBIT once the location reaches normalized earnings power. That's a more than 60% pre-tax return on investment! Even if the store were to perform in the bottom quartile, it would still be raking in $2 million per year, earning a 30%+ ROI.

ASO unit level economics (ASO Investor Day, 10-K)

{kind=link}

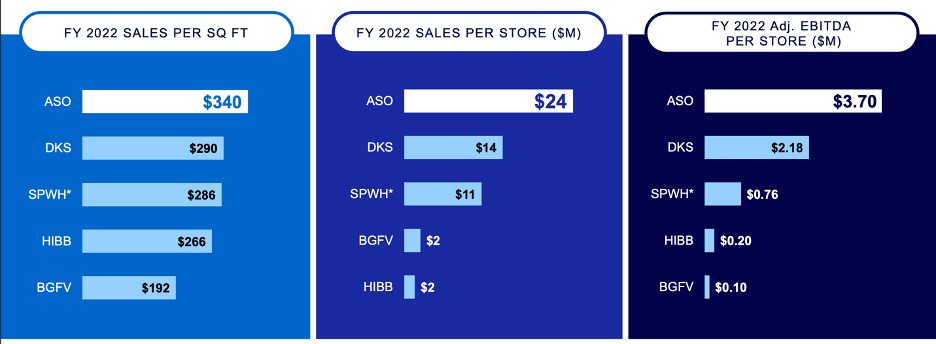

To illustrate how phenomenally well ASO is run, their best competitor, Dick's Sporting Goods ( DKS ), earns an average of $2.2 million in EBITDA per store. That is to say, their most well-run competitor performs in the bottom quartile by ASO's metrics.

And this outperformance isn't just because ASO builds bigger stores. On a sales per square foot basis, ASO still beats Dick's by 17%.

ASO vs. peers on key metrics (ASO Investor Day, ASO 10-K, ASO's peers' 10-Ks)

{kind=link}

Looking back at those earlier targets, ASO's 2027 plan to earn a 30% return on invested capital looks low based on how their stores perform.

Valuation

Given the enormous amount of white space for Academy to expand into, I decided to evaluate the company in three ways: short-term, mid-term bearish, and mid-term bullish. All three reveal that ASO is enormously undervalued.

Short-term

Free cash flow attributable to shareholders is the ultimate barometer of the money a company is making for shareholders, and so to value the company today I started by estimating normalized earnings power.

Over the past twelve months, ASO generated $900 million of EBITDA. After subtracting the ~$20 million eaten up to meeting working capital needs, $65 million of maintenance capex, and $217 million of interest expense and taxes, we're left with just under $600 million of levered free cash flow.

Dividing that $600 million by the 76.89 million shares outstanding yields a levered FCF/share number of $7.80. At $48 today, ASO is trading at 6.2x free cash flow. By virtually every benchmark, that is an absurdly low valuation.

At 10.0x free cash flow, ASO is worth $78 today . That implies more than 60% upside from the current price.

Mid-term - Bearish

To get a sense of what ASO could be worth in four years in the bear case, I took the mid-point of management's 2027 targets and discounted them by 15%, which is quite aggressive given retail's relative predictability. My assumptions for what ASO could be worth in 2027 are as follows:

- Same-store-sales decline to $20.5 million and only 110 new stores are opened, as opposed to 120 - 140 forecasted.

- A $680 million attribution from omnichannel growth (i.e., digital orders, curbside pickup, etc.) compared to $700 - $900 million forecasted.

- Average EBITDA per store deteriorates to $3.2 million.

In this scenario revenue would be $8.45 billion, while EBITDA would $1.2 billion. Applying the same levered free cash flow calculation (EBITDA - increase in working capital ($60M) - maintenance capex ($115M) - interest & taxes ($375M)) implies that 2027 free cash flow would be $650 million, or $8.45.

At 10.0x earnings, plus accrued cash, ASO is worth $120 per share in 2027, representing a 25% IRR.

Mid-term - Bullish

For the bull case scenario, I took all of management's assumptions at face value to see what ASO is worth if management, who has a record of prior success, pulls it off again.

- Revenue increases to $10 billion as SSS growth averages 3%+ and more than 120 stores are opened.

- EBIT margins stay at 13.5%.

- Depreciation & Amortization stays fixed at 1.7% of revenue.

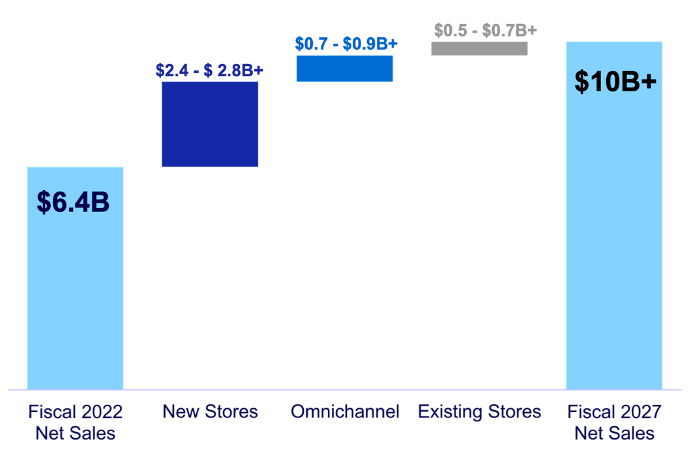

ASO sales bridge (ASO Investor Day)

{kind=link}

In this bull case scenario, EBITDA would rise to $1.52 billion. Again, applying the same normalized levered free cash flow calculation (working capital expense of $100 million, maintenance capex of $175 million, and interest & taxes of $435 million) yields a LFCF number of $810 million, or $10.55 per share.

At 12.5x earnings, admittedly a best-in-class multiple, plus accrued free cash flow, ASO would be worth $175 in 2027, supporting a 35% IRR.

Long-Term Potential

While I'm not one for getting caught up in big promises from management teams eager to impress Wall Street, for long-term investors it is worth looking at ASO's potential over the next decade.

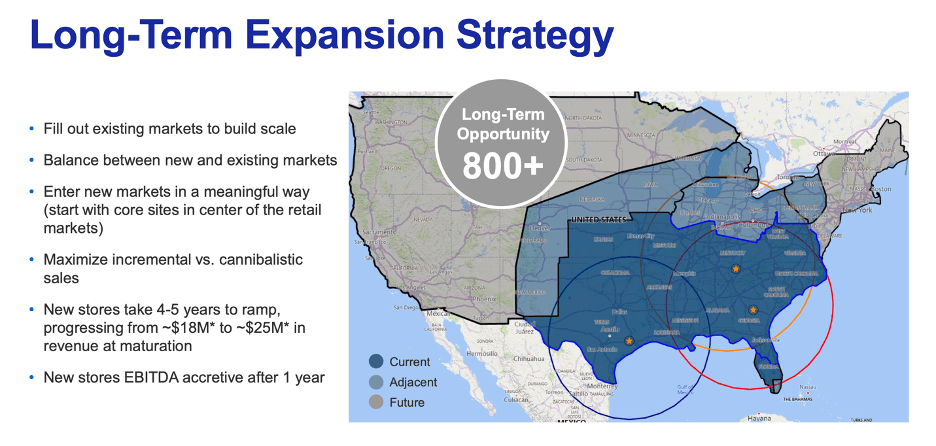

Per the April 2023 investor day, Academy views their long-term opportunity at 800+ locations. Considering Dick's Sporting Goods has 790 locations, such a number is not impossible, but certainly aggressive.

ASO long-term growth opportunity (ASO Investor Day)

{kind=link}

Assuming ASO opens 30 locations per year, from the current base of 269 it will take 18 years to get to 800 locations. If same-store-sales growth grow at a 3% clip over that same period to $41 million, we'd be looking at $32.8 billion of revenue and ~$4.9 billion of EBITDA. At 10.0x EV/EBITDA, which is a ballpark number because it's impossible to know what kinds of multiples will be reasonable in 18 years, ASO would be worth at least $49 billion, giving no credence to cash generated along the way.

While the vast majority of investors don't have that kind of time frame when they invest, Academy's projections give a sense of the kind of compounding at play hidden within the simple retail formula for growth (same-store-sales growth + percentage change in new stores = revenue growth).

Risks to the Thesis and Why the Opportunity Exists

Growing, high-quality companies trading at single digit multiples of free cash flow tend to not be all that common (if they were the sell-side would be in some deep trouble). Additionally, the shorts have over $550 million of exposure to ASO and are banking on a decline, so it's worth reflecting on where I could be wrong.

Risk #1: Recession on the Horizon

The recession expected in 2023 is one of the most predicted in years. From Bloomberg, to CNBC, to Seeking Alpha, there has been a lot of talk about an imminent recession, and, unfortunately for Academy, retailers tend to struggle during economic downturns. ASO lowering guidance in Q1 also hurt investors' confidence in the durability of Academy's revenue and profitability gains.

However, I view the lowered guidance as a temporary headwind for the stock and believe that as the economy strengthens heading into 2024, ASO should be able to once again demonstrate their ability to grow.

Risk #2: Normalized Earnings Power Is Lower than Expected

Normalized earnings power is also a key headwind for ASO stock. Prior to the pandemic, Academy was earning EBITDA margins less than half of where they are today. Should ASO have to lower prices for some reason or have expenses go up in a meaningful way, EPS could be materially hurt.

The problem with the above narrative is that it conflates increased pricing power with a more efficient cost base, giving no credence to the efficiencies Ken Hicks was able to squeeze out of a business previously more concerned with the rate of store openings than store level profitability.

Takeaway

Whether Academy trades at $125 or $180 in four years' time is inconsequential, as the IRR is market crushing either way. The main thing to understand is that right now, a best-in-class retailer that earns incredible returns on every location they build out is trading at just 6.2x normalized levered free cash flow.

As the saying goes, "It is better to be roughly right than precisely wrong." I'm quite confident I'm roughly right on ASO.

For further details see:

Academy Sports and Outdoors: Cheap, Growing, And Poised To Triple