DKS - Academy Sports and Outdoors Q2 Earnings Preview: Investing In Profitable Expansion

2023-08-28 11:31:59 ET

Summary

- Dick's Sporting Goods experienced a significant drop in stock price, potentially impacting Academy Sports and Outdoors.

- Academy Sports and Outdoors' stock also saw a decline, but not as drastic as Dick's Sporting Goods.

- The upcoming Q2 earnings report for Academy Sports and Outdoors will be closely watched to determine the company's performance.

Introduction

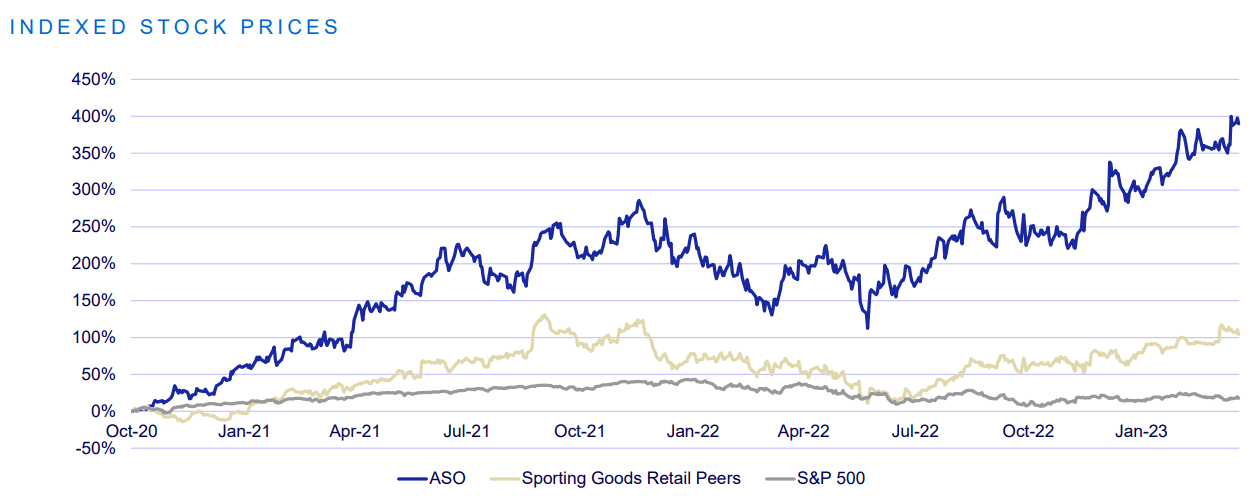

We are set. In a few days, Academy Sports and Outdoors ( ASO ) will report its Q2 earnings. In the meantime, Dick's Sporting Goods ( DKS ) and the stock lost almost 25% of its market cap in just one day, moving from just below $150 to $111 per share. The impact on Academy was strong, though not as big, with the stock trading down around 7% to $52 per share to then fall further in the next trading days. So, are there reasons to be worried about the upcoming report of Academy? In this article, I will share the main data I will be looking at during the report to se e if my bull-case from August 2022 is still intact or not.

The company

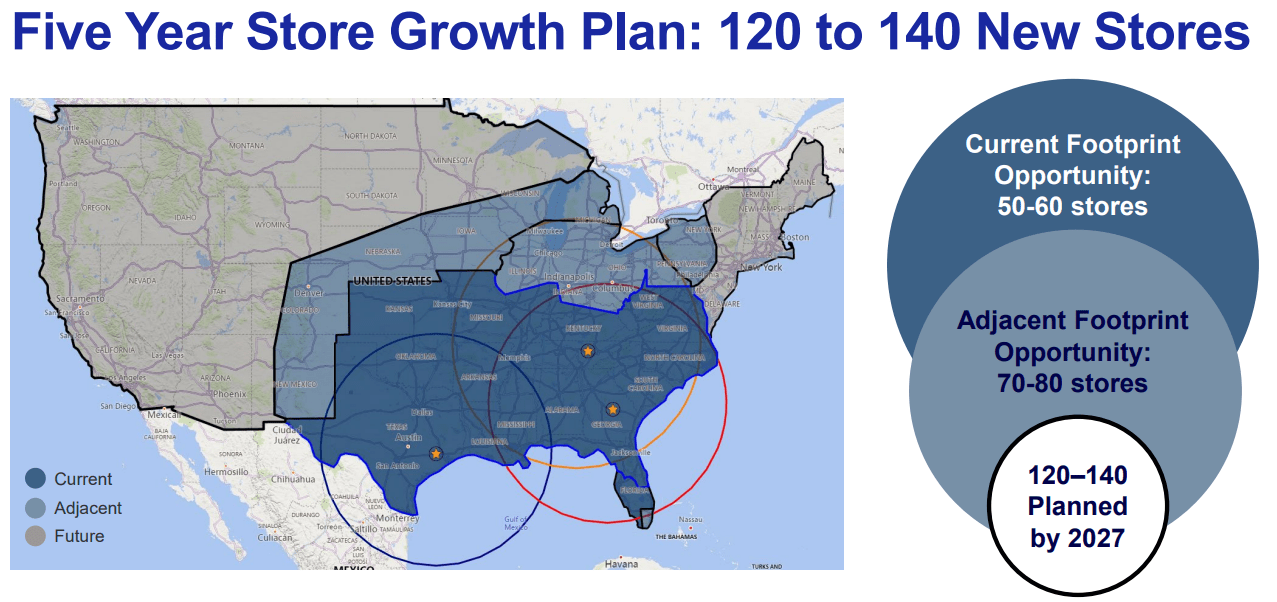

Academy, though it has been around since 1938, is a rather new company to the stock market, having ipoed in October 2020. The company is a sporting goods and outdoor recreation retailer, with a strong geographical footprint in the South. Now, it is planning to grow and expand across the States and currently it has reached 271 stores across 18 states, thanks to the last opening of a new store in Indianapolis. This is the third store opening in 2023 and the company is planning to end this year with a total of 13-15 new stores, thus making us expect around 10 new opening in the last few months of the year. Overall, the goal is to open between 120 to 140 new stores by the end of 2027. This means the company aims at expanding its store base by around 50% in 4 years.

After some years when the business was seeing no growth, with sales and profitability falling precipitously (net sales per store fell from $21 million in 2013 to just above $15 million in 2018), the company saw a big turnround after 2018 which brought its net sales to around $6.4 billion, coupled with a gross margin that moved up from 29.6% in 2019 to 34.6% last year. Net sales per square feet improved, too, and are now at $340, a leading metric among retailers (Dick's is at $290). Sales per store have increased by almost $10 million since the turnaround began and at the end of 2022 the company achieved $24 million per store (Dick's sales per store are at $14 million). No wonder the stock returned 3.5x compared to the S&P500, with a $4 billion increase in market cap since its IPO in 2020.

{kind=link}

Last year, the company also initiated a dividend and paid $25 million to its shareholders. At the same time, it has already repurchased $900 million of shares and it has paid down $1 billion of LT debt.

Summary of previous coverage

Among the main reasons I am long Academy, there are two that I think are worth of being highlighted:

- Compared to its competitors, Academy has a plenty of room to grow in the U.S. because it is still a little more than a strong regional player

- The pandemic was surely a tailwind for its sales, but the company has proven it is able to consolidate its strong results achieved back then.

Working on some projections to understand how the robust expansion in new stores will impact the company's earnings, I went through the available data about store profitability along with new store opening costs. Given that after one year a new store is already EBITDA accretive, I ended up with a 2027 forecast of $9.7 billion in revenue, $1.6 billion of EBITDA (16% margin). This gave the result the company was trading at around a fwd 2027 EV/EBITDA multiple of 3.5 with a stock price of $47. Thus, my fair value came in around $65.

The earthquake shaking retailers

No story comes with no problems. At first, we had inflation, then interest rates rising. However, these may be considered as part of the economic cycle. Over the past year, I went through an issue that can become more entrenched than inflation: high rates of theft . I dealt with it after Target ( TGT ) and Walmart ( WMT ) reported back in December 2022 how shoplifting was becoming an issue. It was at that time that I understood better how Costco ( COST ) is uniquely positioned to face this problem without being damaged as much.

Dick's last earnings release was really clear about it because it reported right from the beginning some serious words from Lauren Hobart, Dick's CEO:

our Q2 profitability was short of our expectations due in large part to the impact of elevated inventory shrink, an increasingly serious issue impacting many retailers.

In fact, Dick's reported EPS of $2.82 compared to $3.25 of the same quarter last year. As a consequence, it had to revise downward its 2023 EPS outlook, moderating it a little.

During the earnings call , Miss Hobart had to spend a few more words on what the earnings release reported:

The first was the impact of higher inventory shrink, organized retail crime and theft in general, an increasingly serious issue impacting many retailers. Based on the results from our most recent physical inventory cycle, the impact of theft on our shrink was meaningful to both our Q2 results and our go-forward expectations for the balance of the year. We are doing everything we can to address the problem and keep our stores, teammates, and athletes safe.

Some more color was given by Dicks' CFO Navdeep Gupta, when he explained during the earnings call how a third of the company's merchandise margin decline was related to higher-than-expected shrink (the other two thirds were mainly linked to mark-downs of outdoor inventory before the selling season ends). Overall, the company had to slash its EPS guidance from the original range between $12.90 and $13.80 to the new range of $11.50 to $12.30 (including approximately $0.20 coming from the 53rd week this year). EBIT margin is expected to be approximately 10.2%, compared to the prior expectation of 11.6%.

How to deal with Academy's upcoming Q2 report

All this is necessary to understand what investors will probably find in the upcoming earnings report. I think it is unlikely Academy has not been hit as well by the growing crime rate. If shrink won't be a big issue during the report, I would be surprised and it would mean the company has found a way to protect its stores better than other peers. However, as said, I think it is unlikely.

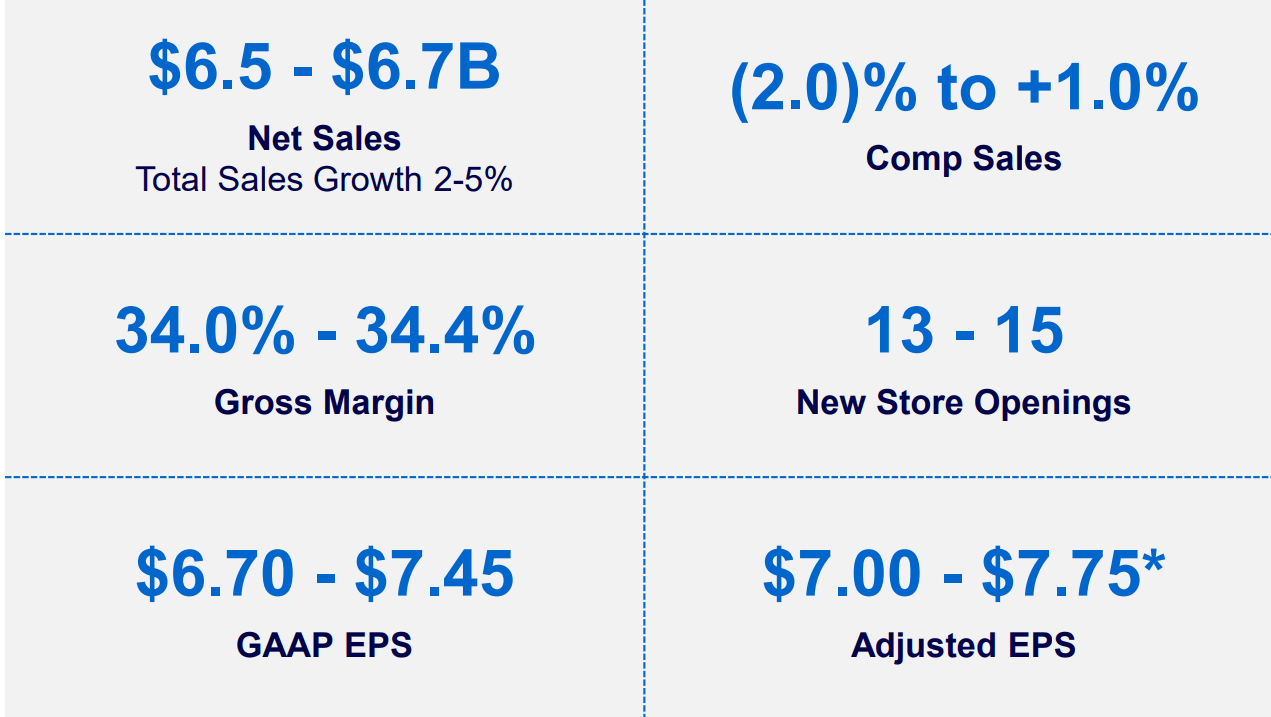

So, what we need to do when looking at the earnings report is to keep in mind this table where Academy shared its previous guidance for this fiscal year.

As we have seen, Dick's slashed considerably its outlook. Academy, which has been trading down around 13% since its competitor's report, might now fall further if its guidance will be maintained or revised only a bit to the lower end.

{kind=link}

Academy had already been clear with the market that in 2023 its goal was to consolidate its post-pandemic outstanding results.

In terms of gross margins, if we see a number above 33% we can consider Academy well on track. If we will see GAAP EPS guidance still around $7 we can be comfortable with the path the company is going. If we will see a number much below $6.50 then I believe a sell-off might take place.

However, let me point out that, as far as shrink is a big issue, the main driver of performance when looking at retailers is comparable sales. In other words, we need to make sure a company is able to grow every store's profits. So, what would really be concerning would be to see a big drop in comparable sales, which this year's guidance sees more or less flat YoY.

How I am positioning myself

I expect this earnings release to be a little tough. In any case, I think we might be before a good opportunity. Volatility in this case may indeed open up a fantastic opportunity to pick up some shares of a company whose bull-case is strong.

In fact, while Dick's is already quite present around the whole country, Academy's has plenty of room to expand. As we can see from the map below, it is still working on strengthening its existing markets, while growing rapidly in adjacent states. More than half of the country has yet to see an Academy store opening.

{kind=link}

Now, of course, the company could perform badly and make a disaster out of these new openings. However, since 2018 it has proven over and over again that it has found a way to increase its footprint at profit.

In addition, I think the fact Academy is still on its way to grow its store base is something that gives it an advantage over a competitor such as Dick's. In fact, if shrink becomes a problem that doesn't go away quickly, the company might have the opportunity to redesign and build a new store concept to better protect its merchandise. For Dick's this is much more expensive, since it already has 800 stores around the country.

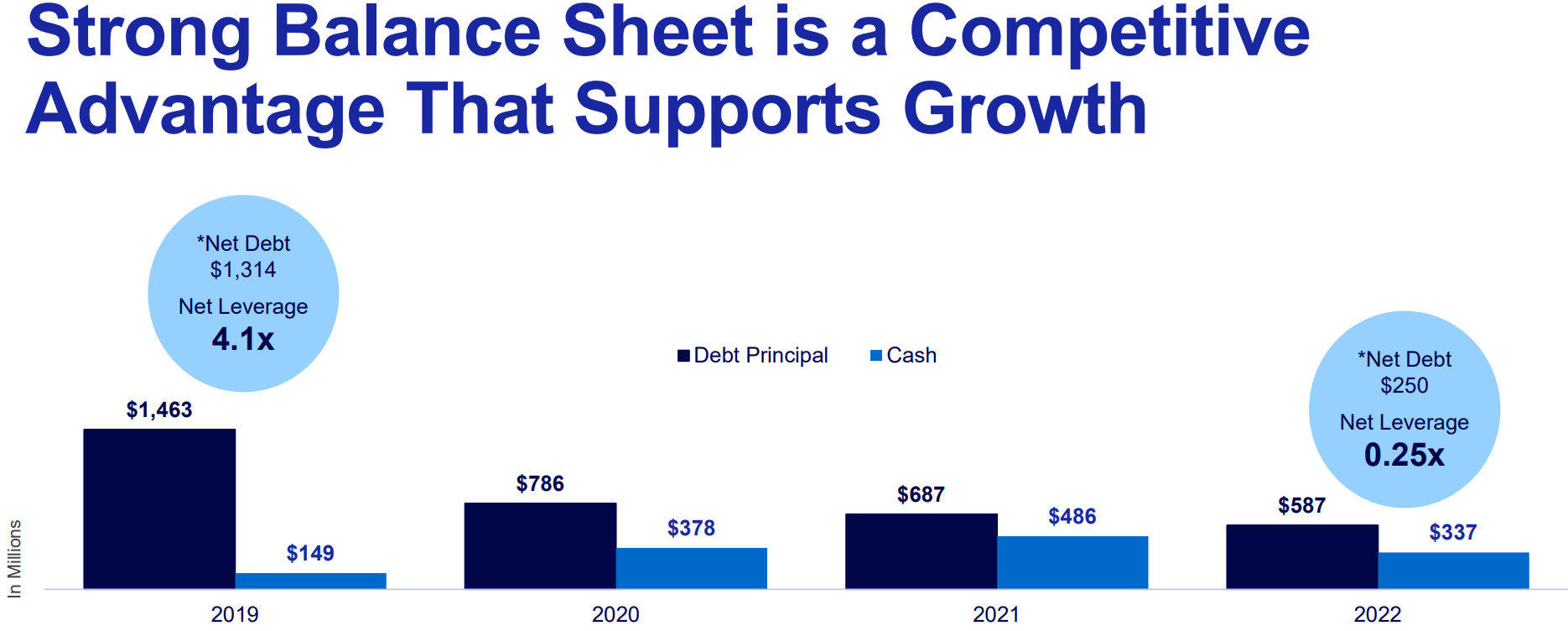

Academy has also been laser focused on improving its balance sheet, bringing dramatically down its net leverage in just 4 years, from 4.1x in 2019 to 0.25x at the end of last year

{kind=link}

This enables the company to face any financial hardship without concern.

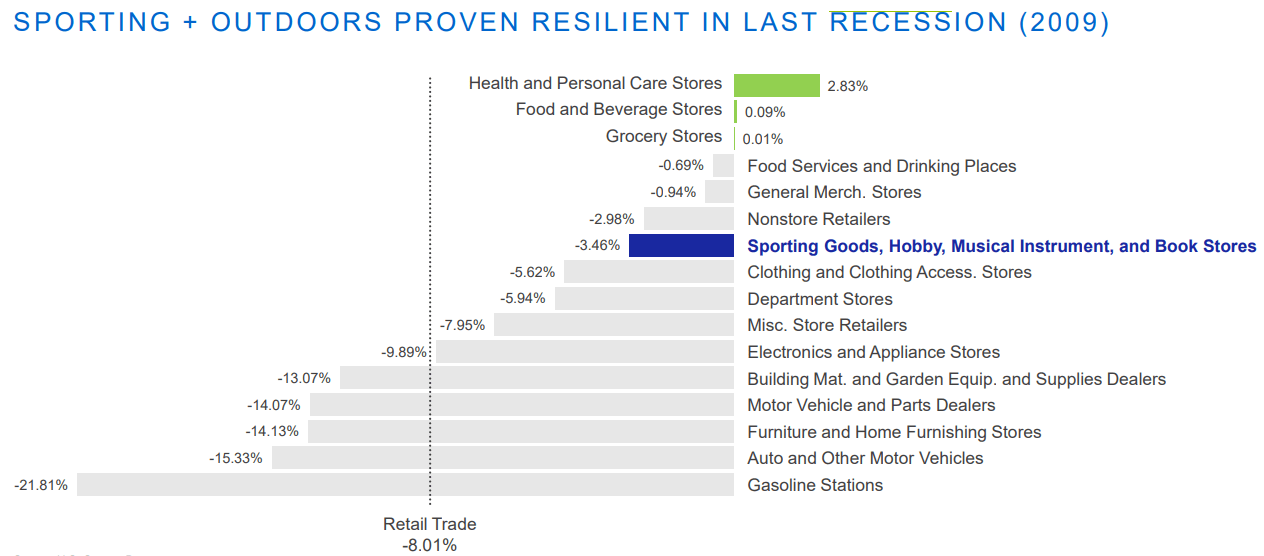

In conclusion, unless we see a real disaster that harms the company's core business, I believe the bull-thesis on Academy is still intact. Actually, I am preparing to buy some more shares in case of a further drop. Sport and outdoor merchandise sees strong demand and it is one of the most resilient sectors among consumer goods.

{kind=link}

With the company now trading at a fwd EV/EBITDA of 6 and a fwd PE of 7.3 we are before a stock whose discount to its main competitor (Dick's PE is 9.3 and EV/EBITDA is at 7) is not so justified given the different growth prospects the two companies have. In my past article, I shared a table showing how I expect the company's earnings to evolve in the next five years, considering its new openings and the EBITDA they will add. As some may see, I am guiding more conservatively than the company itself. Still, I see the company's fair price around $65 and I see no reason to downgrade it over the long-term.

For further details see:

Academy Sports and Outdoors Q2 Earnings Preview: Investing In Profitable Expansion