ASO - Academy Sports and Outdoors: Rating Downgrade To Neutral As Near-Term Performance Outlook Is Uncertain

2024-01-04 04:11:13 ET

Summary

- Academy Sports and Outdoors' recent performance fell short of expectations, with declining revenues, same-store sales, and gross margins.

- Concerns about the company's growth and margin outlook have led to a downgrade from a buy to a neutral rating.

- The pivot towards promotional strategies, weakened consumer demand, and persistent shrink headwinds have dampened my confidence in ASO's growth and gross margin outlook.

Investment action

I recommended a buy rating for Academy Sports and Outdoors ( ASO ) stock when I wrote about it the last time , as I was positive about the 2H23 sales guidance and margin improvement outlook, which will drive valuation up. Based on my current outlook and analysis of ASO, I am downgrading from a buy to a neutral rating as I am concerned about the growth and gross margin outlook. I wonder if the consumer spending strength has weakened much worse than I expected. If true, near-term growth is going to continue seeing this headwind. Also, management pivoting to a promotional strategy is also going to hurt gross margin, which further compresses earnings growth (on top of the possible weak topline performance).

Review

ASO's recent 3Q23 performance was not up to my expectations. The business reported revenue of $1.398 billion, a 6.4% decline. However, comparable sales was not as great as I expected. Same-store-sales [SSS] saw 8% decline. Gross margin also decreased 44bps y/y to 34.5%. Likewise for adj EBIT margin, it decreased 232bps y/y to 10.2%.

Previously, I was positive on SSS returning and gross margins to benefit from the improving shrink performance and freight cost. However, it appears that the outlook for both is not as great as I thought. For gross margins, the quarter performance was pretty bad, and I wonder if things will improve. Aside from the seasonal clearance (due to bad weather) that should not repeat, I was disappointed that worse than expected shrink – which management mentioned would turn out better in 2H23. Thankfully, in this quarter, the headwinds from shrink were cushioned by freight savings. However, I believe additional savings from freight cost normalization are going to be unlikely. Moreover, I believe supply chain savings are going to be lower in 2024, as most of them should have already been reflected in 2023 (supply chain already drove a 200-bps improvement in 3Q23). If the headwind from shrink persists, the margin is not going to be pretty in 4Q23. Since management has shifted to using strategic promotions to boost sales in a highly promotional environment, my outlook on the near-term margin performance has become more pessimistic. The good news is that it has boosted sales, but the bad news is that gross margin is taking a hit, which is evident from the fact that management has lowered their gross margin guidance for FY23. Mathematically, this implies the 4Q23 gross margin is going to come in way below. If I were to be blunt, it appears that the earnings growth momentum, driven by gross margin and topline growth recovery, has gotten weak. Management now needs to rely on promotions to drive growth.

It is not that the promotion strategy would not work. My concern is that many other retailers were also doing promotions in 4Q23 (pretty typically for 4Q23 given the festive season). As you can imagine, multiple promotions among retailers drive growth but hurt gross margins in the near term. What is positive for ASO is that the weather has gotten better through 4Q23, and it benefited from the extra day of traffic (Christmas fell on a Monday in 2023 vs. 2022), which is a 1-day of comp tailwind. Another concern is that, if 4Q23 did well (due to the promotions), I cannot shake off the weak performance that ASO saw in August’23 despite the strong tailwind from the back-to-school season (August saw a mid-single-digit comp sales decline). The negative side of me tells me that the underling consumer demand strength has been structurally impaired in the near term due to the weak environment. As such, on a like-for-like basis, if the economy doesn’t recover in the near term, comp sales are likely to be weak compared to 4Q22. Importantly, 3Q23 weakness was across various categories, where sports and recreation fell 2.7%; outdoor fell 6.9%; apparel fell 6.9%; and footwear fell 8.2%. This suggests that growth weakness was due to a particular category or customer group, but across the board, supporting my view that the overall consumer strength has weakened.

Overall, I am downgrading my rating from buy to hold as I am not comfortable with the near-term top-line performance outlook. Moreover, gross margin is likely to see compression, which will be a double whammy to earnings growth.

Valuation

{kind=link}

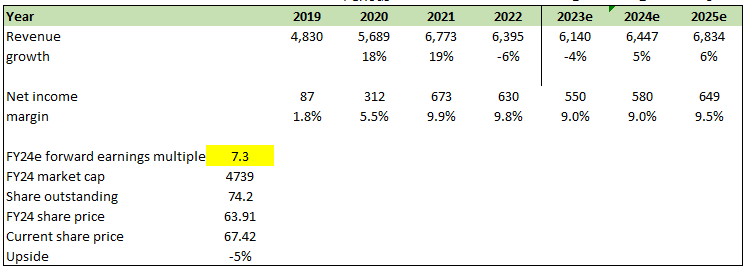

I have revised my growth and margin outlook for ASO downward. Management is now guiding FY23 revenue of $6.14 billion, which is a -4% growth, 300bps delta vs. my previous growth assumption. Hence, I downgraded all my growth assumptions by 300bps in FY24 and FY25 to reflect this change. The bigger change is that I do not expect margin to improve back to 10% within my forecasted period, as I am negative on how ASO’s gross margin is going to proceed from here. The step-up in promotions, reduced benefit from freight cost normalization, and continuous shrink headwind are going to hurt gross margins. With my revised outlook, I am no longer confident that ASO should trade at 9x forward earnings. I assume it would trade at its historical average valuation (historical revenue growth CAGR is 5%).

Risk and final thoughts

I might be overly worried about how weak the consumer strength is, and if that is the case, growth could be much stronger than expected in CY2024, especially if the macro environment improves further from here. Another risk is that the ASO promotional strategy might work flawlessly, driving more recurring purchases and improving brand loyalty. Essentially, gross margin might not see as much compression as I expected. Both of these will cause ASO to outperform my expectations, driving it up to my target price.

I am downgrading ASO from a buy to a neutral rating due to concerns about uncertain near-term performance. Disappointing 3Q23 results, with declining revenues and substantial drops in same-store sales and gross margins, have led me to be concerned about the company's growth and margin outlook. Management pivot towards promotional strategies, weakened consumer demand across categories, and persistent shrink headwinds have dampened my confidence. Consequently, I am no longer confident that ASO can trade at 9x forward earnings.

For further details see:

Academy Sports and Outdoors: Rating Downgrade To Neutral As Near-Term Performance Outlook Is Uncertain