ASO - Academy Sports and Outdoors: Recent Performance Appears To Be Unsustainable

Summary

- The pandemic created astronomical demand for sporting goods, as consumers used excess stimulus cash to fund outdoor activities.

- Academy saw revenues surge ~18% and ~19% in 2020 and 2021, and net income margins nearly quadrupled from 2019 to 2021.

- While Academy has strong financial metrics on a store basis, I suspect these will decline as consumer demand softens.

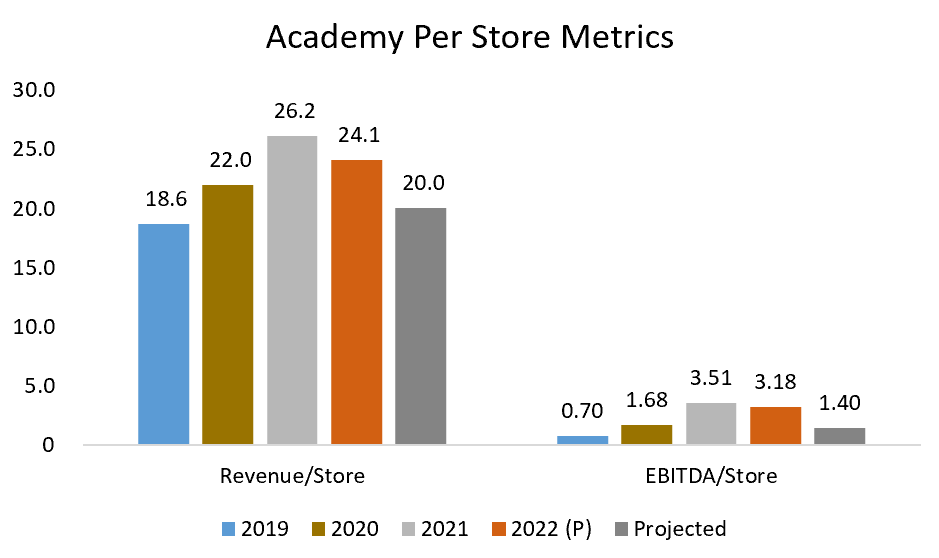

- Management hinted that revenue/store could fall from $26.2 million to $20 million and that EBITDA/store could fall from $3.5 million to $1.4 million.

- Management's plans to aggressively expand are not nearly as attractive when we look at store metrics that reflect future demand.

Executive Summary

I do not believe that an investment in Academy ( ASO ) is a prudent decision, given the current price and incoming headwinds. I believe that recent performance is unsustainable, as most of the recent improvements have been driven by overall industry demand, and not fundamental changes in Academy's business. After all, do we really think it's just a coincidence that Academy saw YoY comparable sales growth of 30% and EBITDA margins jump 900 bps QoQ in Q2 of 2020? Hardly. This in itself isn't a red flag, but there don't appear to be any changes in the business that lead me to believe that margins can stay this way. While we've seen small improvements in digital penetration and private brand sales, these improvements are not nearly enough to sustain quadrupled margins. It appears that management feels the same way, as they hinted at revenue/store and EBITDA/store numbers that are far cry from current metrics. If we combine this with the flurry of insider selling at both Academy and DICK'S ( DKS ), I believe that financials could sour very quickly. In a 3-statement model valuation, I found an implied 5-year price target of $66.95. This equates to an implied IRR of 3.76%... surely below anyone's hurdle rate.

Pandemic Tailwinds

The covid pandemic led to an unprecedented surge in consumer spending , following widespread stimulus by the federal government.

{kind=link}

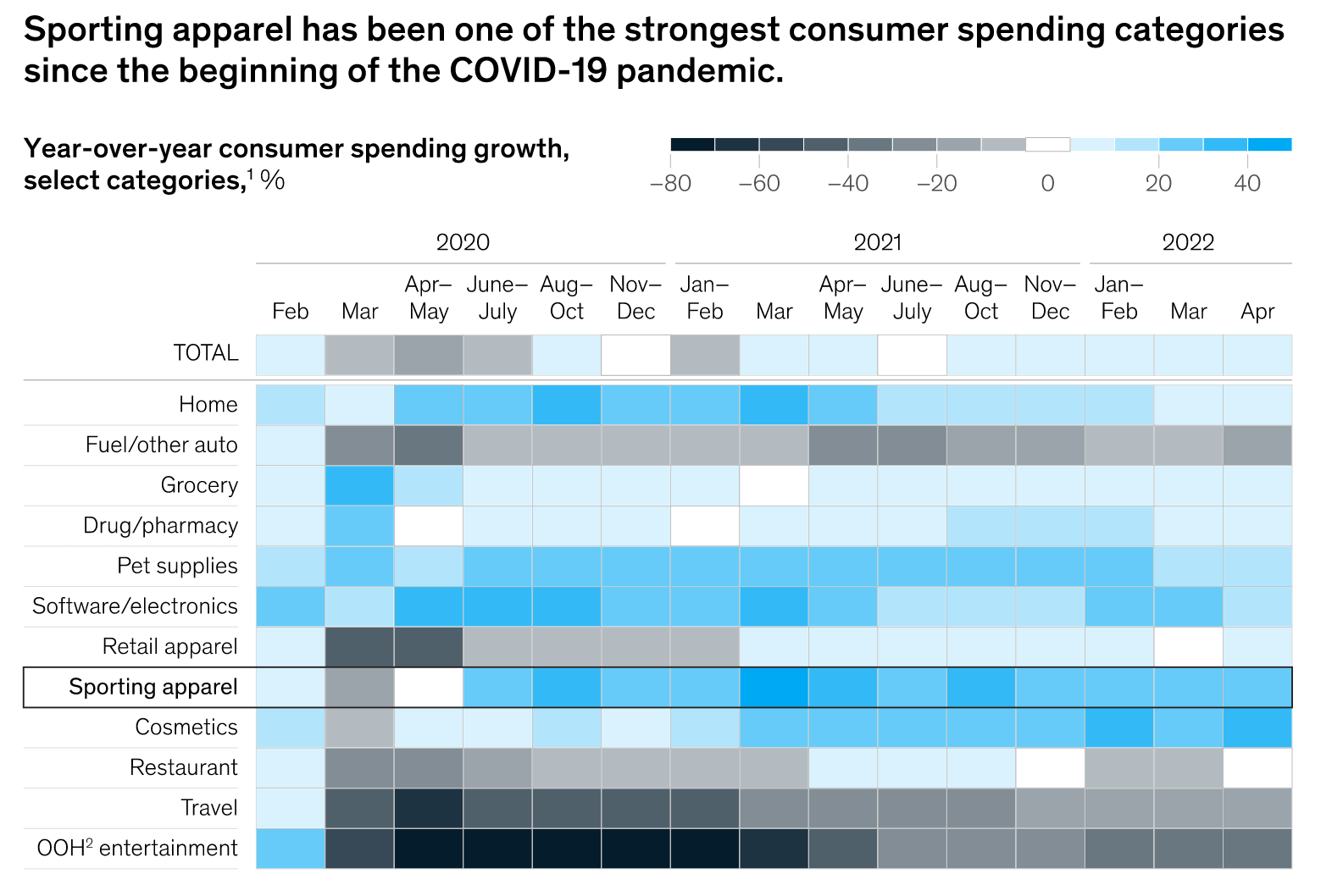

Not only has consumer spending increased at puzzling rates, but consumer spending on sporting goods has increased at an even faster rate. A study by McKenzie showed that athletic apparel was "one of the strongest consumer spending categories since the start of the pandemic" .

{kind=link}

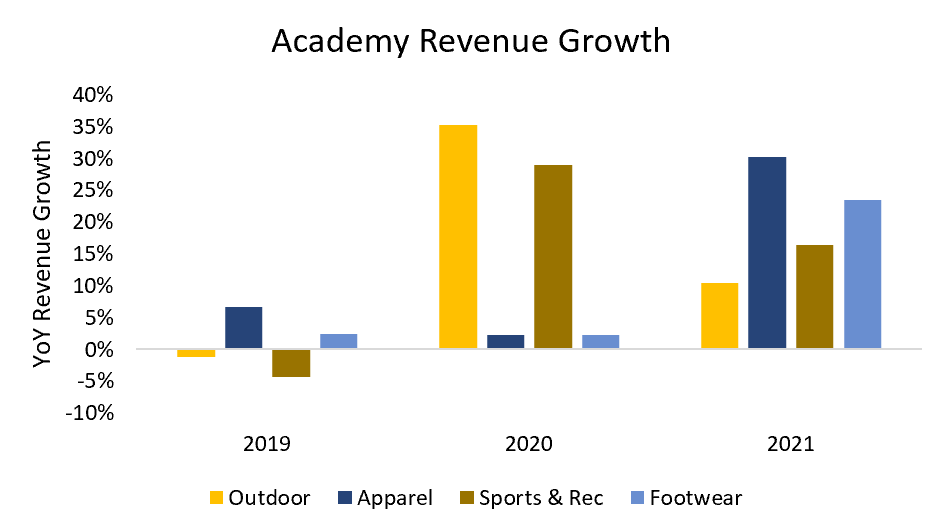

While sporting apparel (and footwear) makes up only half of Academy's revenue, it seems a safe bet that their "Outdoor" and "Sports & Rec" segments saw similar demand surges. This bet is proved to be correct when we look at Academy's revenue growth by segment over the past 2 years.

{kind=link}

All segments saw extraordinary growth in 2020 and/or 2021, however, Academy did not open a single new store during this period. This means that all of the growth was driven by an increase in demand in current markets. Did Academy attract more demand through a differentiated inventory or a unique marketing strategy? I don't think so. You can see that DICK'S had very similar results.

{kind=link}

We see similar results when we look at competitors like Hibbett ( HIBB ) and Big 5 Sporting Goods ( BGFV ). We can take a similar approach to margins as we did with revenue growth. If Academy has really fundamentally changed and improved its business, then we would expect Academy to have increased margins more so than DICK'S.

Author

You can see that EBITDA margins tripled in the second quarter (QoQ), the quarter immediately following the covid pandemic.

{kind=link}

The results are eerily similar. Clearly, Academy is benefitting from increased industry demand, and not increased demand due to their own merits. Before we start looking into the future, I want to look at some aspects of the Academy business that have changed, and how those fundamental changes will/have affected margins.

E-Commerce Penetration

E-commerce was another trend that followed in the wake of the covid pandemic, but it's also one that is somewhat sustainable. While e-commerce penetration has decreased since the peak of the pandemic, it seems that it will be a constant reality for retailers in the future. Academy has invested $230 million since 2011 in its curbside pickup and "buy online pick up in store" capabilities. It seems to have worked.

Author

Omnichannel customers have been shown to spend more money than single-channel customers, and have a 30% higher lifetime value . Additionally, it's been shown that "businesses that adopt omnichannel strategies see 91% higher YoY retention rates". However, s tudies by Mckinsey show something that may surprise you ,

"Online sales are remarkably less profitable than a store sale. You have to invest in [the] capability to have better margin structures."

-Sajal Kohli

Regardless, we'll give Academy the benefit of the doubt, and say that its investments in e-commerce have the ability to increase long-term margins by 1-2 percentage points.

Private Label Sales

Academy has also done a great job in selling its own portfolio of 19 private-label brands. As a Texan, I thought that Magellan, Brava, and BCG (Academy-owned brands) were popular national brands because I saw them everywhere I went.

{kind=link}

Private-label brands made up 20% of total sales for Academy in 2021. In comparison, DICK'S private-label brands made up 14% of total sales in 2021. These products generate higher margins, as national brands generally cost more for retailers to sell. While I could not find this data from Academy, DICK'S says that their private-label brands generate 600 - 800 bps larger margins than national brands . For that reason, I believe that private-label brands could be responsible for long-term margin improvements of 1-2 percentage points.

It Doesn't Appear Sustainable

To summarize what we talked about so far:

- The pandemic drove rapid revenue growth and margin expansion across the entire sporting goods industry, not just Academy. This implies that most of the improvements are not fundamental improvements of the business, but simply due to temporary unprecedented demand.

- Academy has invested heavily in omnichannel capabilities and in its private-label brands. These could be responsible for 1-4 percentage points of margin improvement over the last 2 years, but not the full ~5-10%.

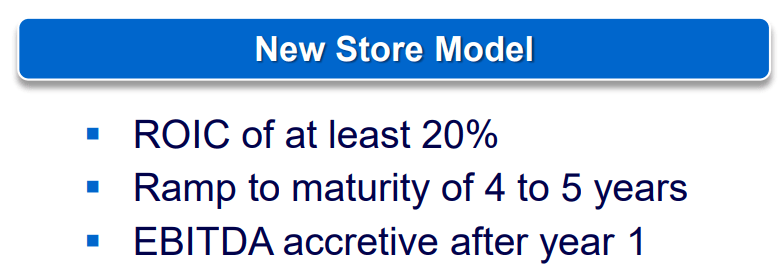

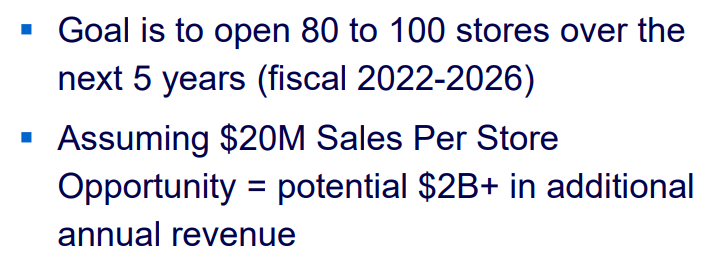

So where do I see the business going from here? Well, it seems that management has hinted at that exact question. Management is planning on opening 80-100 stores in the next 5 years , and they gave us their expectations for these stores. In their investor presentation , they guided at:

- $20 million in sales per store

- EBITDA accretive after 1 year

- Ramp to maturity of 4-5 years

- ROIC of at least 20%

- Average store CapEx of $5.5 million

Academy Investor Presentation Academy Investor Presentation

{kind=link}

{kind=link}

We can actually determine a lot from these numbers. Let's first assume that Academy opens 80 stores in the next 5 years, distributed equally throughout that time period (4 new stores each quarter). We then assume $20 million in sales per store, which is easy enough. After 4-5 years, management expects an ROIC of at least 20% on an initial investment of $5.5 million. To be generous, we'll assume a 25% return, resulting in EBITDA/store of $1.4 million. This doesn't mean much unless we look at historical revenue and EBITDA/store metrics.

{kind=link}

These projections (aided by management), are a drastic fall from covid levels. However, they're still above the 2019 levels, which implies that some margin improvements will stay, presumably driven by e-commerce and private-label brands.

Insider Selling

While you may have trouble believing these projected metrics, I believe recent insider selling backs up my thesis. Not only have insiders been selling at Academy, but insiders have also been selling at DICK'S. I usually don't pay too much attention to insider selling, but the trading has been so lopsided for both companies. Here is Academy's data:

Academy Insider Trading Last 6 Months (Dataroma)

And DICK'S data:

Dick's Insider Trading Last 6 Months (Dataroma)

While I wouldn't use this as a sell signal by itself, coupled with my previous points, this is a huge red flag. Management not only gave us drastically lower EBITDA/store and revenue/store data for future stores, but they're also selling their shares in large amounts. If nothing else, I think this provides some validation to the threat of declining growth and margins.

Valuation

I created a 3-statement model with the following assumptions:

- Academy opens 80 stores in the next 5 years

- Revenue/store drops to 20.7 in 2023, and gradually improves to 21.2 in 2027 (above management's $20 million per store assumption)

- EBITDA/store drops to 1.63 in 2023 and gradually improves to 2.09 in 2027 (above management's implied EBITDA/store of ~$1.4)

- Free cash flow is used to repurchase ~$2 billion worth of shares throughout the 5-year forecast period

- EV/EBITDA at the end of the forecast period stays at 5x.

Author

An IRR of 3.76% is far from attractive. With that being said, I do fundamentally like Academy as a business, and I would buy it at the right price after we see how much demand softens.

Final Recommendation

As I said above, I actually like Academy as a business. They have a lot of metrics that are superior to DICK'S and they have a much larger growth runway. I have owned Academy stock throughout the pandemic, but I believe the headwinds are becoming too strong to justify holding. Consumer demand has already started to soften and, in my view, will continue to soften throughout 2023. Long-term management assumptions for new stores are far below today's metrics, implying a sharp drop in fundamentals. This thesis is backed up by heavy insider selling in both Academy and DICK'S. I recommend selling Academy shares (and DICK'S for that matter) and waiting to see what happens to the share price in the coming year or two. However, I DO NOT recommend actively short selling, as I don't believe the risk/reward is appealing.

For further details see:

Academy Sports and Outdoors: Recent Performance Appears To Be Unsustainable