HIBB - Academy Sports and Outdoors: Long-Term Compounder Supported By Strong Fundamentals

2023-06-27 15:58:12 ET

Summary

- Academy Sports and Outdoors is well-positioned for future growth through store expansion and omnichannel delivery experiences.

- The company plans to open 13-15 new stores in 2023 and 120-140 new stores by 2027, boosting its top-line and bottom-line growth.

- Despite a 25% share price drop since April, ASO's cheap valuation and strong fundamentals make it a compelling buy opportunity.

- The 40-50% upside potential from my conservative DCF estimation could be an indicator that ASO is now undervalued and underappreciated by Mr. Market.

Editor's note: Seeking Alpha is proud to welcome KL Research as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Thesis

The share price of Academy Sports and Outdoors (ASO) has plummeted by 25% from its 52-week high back in April as Wall Street Analyst turned bearish when the company recently published its Q1 earnings and revenue. Q1 Non-GAAP earnings were $1.30, which missed analyst estimates by $0.34. Whereas Q1 revenue was $1.38 billion (down 5.7% YoY), which also missed analyst estimates by $60 million. As a result, the underwhelming performance alongside lowering forward guidance by the management team has led to a spread of contagion fear among investors, causing a massive selloff of the stock.

Despite the huge price correction, ASO remains fundamentally strong. The company is operating in the sporting & recreational industry, with a Total Addressable Market ((TAM)) of $175 billion and growing at a CAGR of 7.9% per year. This will open up huge untapped and addressable markets for ASO to exploit in the future. Alongside its ambitious store growth plan strategy for the next 5 years and its great customer connections focusing on Assortment, Value and Experience, this makes ASO a wonderful business well-positioned to reap its future growth benefits. Given its cheap valuation at the moment and market pessimism, I rate Academy Sports & Outdoors as a "Buy".

Business Overview

{kind=link}

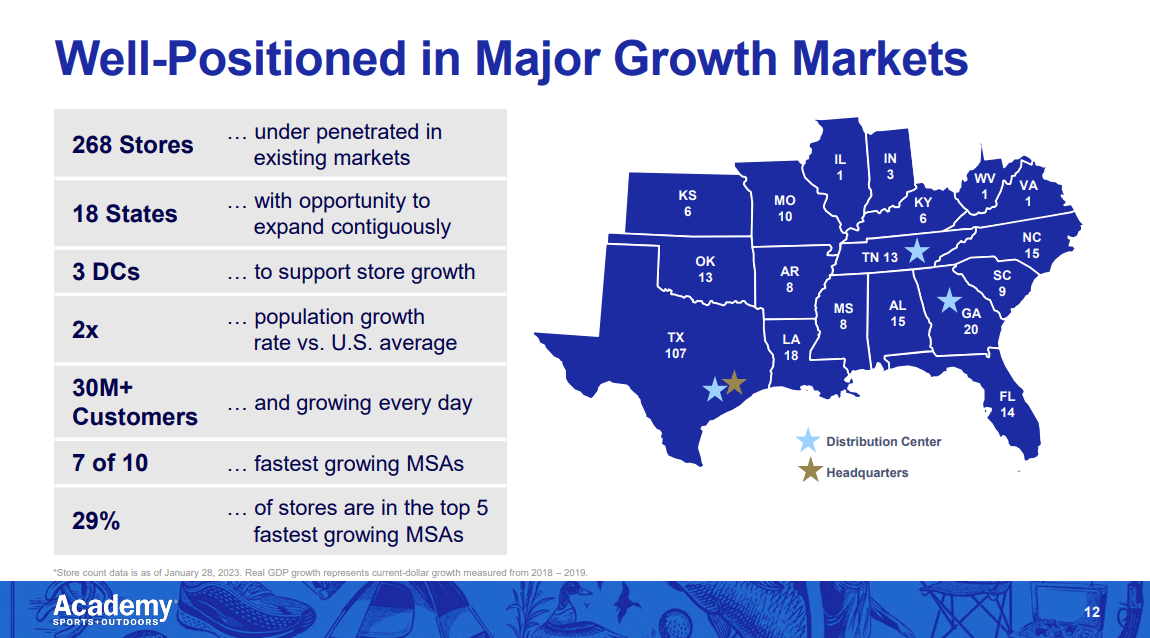

Academy Sports and Outdoors is a US outdoor and sporting goods retailer, operating 268 stores across 18 states. The company first started as a Military Surplus store in 1938 and gradually transformed itself into a retailer in the 1980s-90s. It went IPO in 2020 amidst the pandemic and became a member of the Fortune 500 in 2021. Academy Sports & Outdoors currently offers a diversified number of sporting brands in stores, ranging from leading national brands like Nike and Columbia to Private label brands like Outdoor Gourmet and Magellan Outdoors. The company also differentiates itself from other specialty retailers by providing fun for customers and delivering customer focus experiences through assortments and value.

Store Growth Expansion

{kind=link}

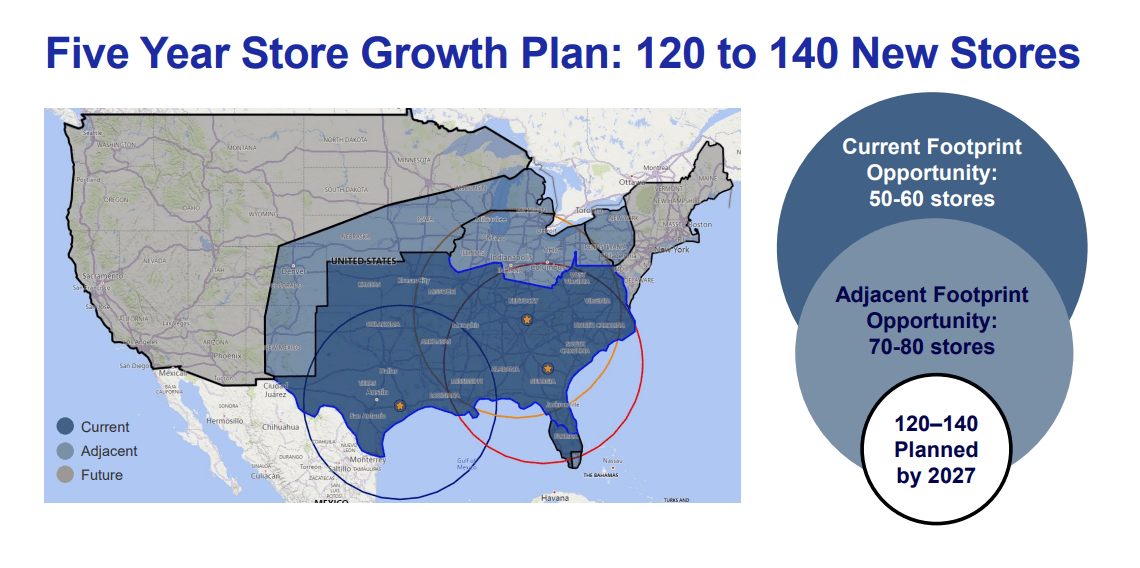

Academy Sports shall see ample growth opportunities through new store expansion. The company opened 9 new stores last year and is also expected to debut 13-15 new stores this year . The Management Team is also committed to opening 120-140 stores by 2027, which will likely improve its geographical penetration and expand its under-served markets, boosting its top-line and bottom-line growth for years to come.

In addition, as most of the stores from Academy Sports are located in the Southern Part of the US, where most of the states are experiencing positive population growth, this will likely bring in more traffic and revenue per store to come.

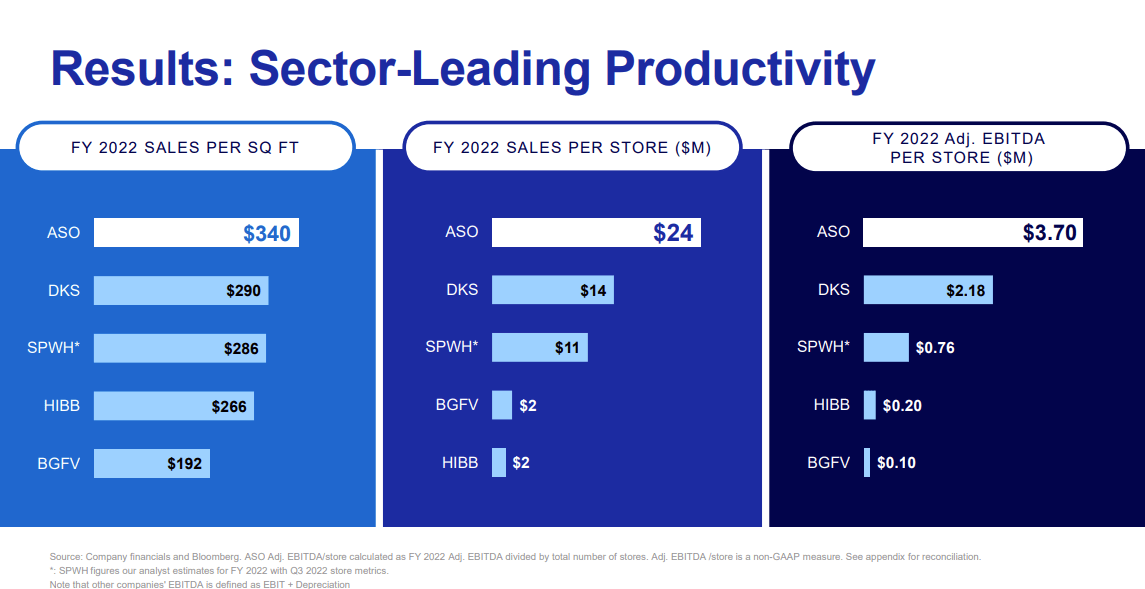

Differentiated Store Productivity among Competitors

ASO has one of the highest store productivity and profitability among its competitors. All stores opened by ASO are profitable, and each ASO store delivers $4 million of EBIT on average, which is double the average amount of EBIT for other sporting goods competitors ($2 million). The new stores also have strong economics, averaging a 20% ROIC per store.

{kind=link}

Academy Sports also has a strong competitive advantage against its competitors when it comes to productivity. The Sales per square foot for ASO is $340/sq ft, which is much higher than its closest competitor DICK'S Sporting Goods ( DKS ) $290/sq ft and Hibbett Sports ( HIBB ) $266/sq ft, which illustrates that ASO is much more profitable and productive than its competitors when utilizing its floor space to channel profits.

Improved E-Commerce and Omnichannel experiences

{kind=link}

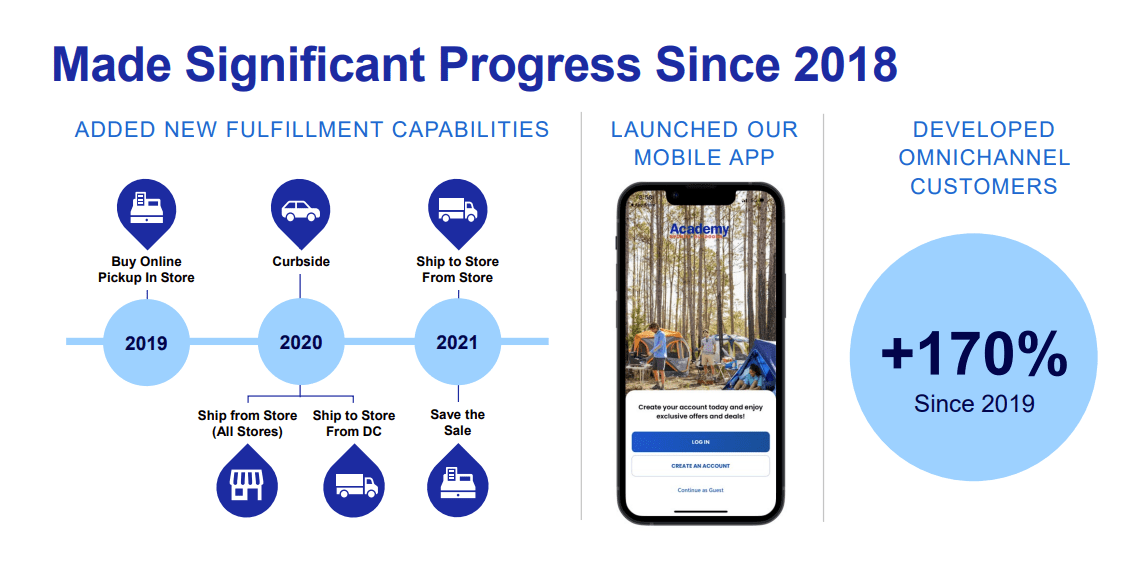

The pandemic has transformed the way we purchase goods and merchandise online. Academy Sports also expanded its footprint into the E-Commerce Space back in 2021 by introducing its mobile apps and improving merchandise checkout experiences. In addition, the company also offers different pickup options for customers to choose from, ranging from Buy Online, Pickup in Store to Curbside Delivery and Home Delivery. As a result, these measures allow the company to scale its operations more efficiently and attract more traffic and customer engagement, which provides more dynamic growth opportunities for the business as well.

The number of online omnichannel shoppers grew by 170% since 2019, which drives Net Sales up by 198% during this period, which illustrates that ASO has made significant progress and still has much room for growth when it comes to online retail experiences.

Elevated Customer Experiences and Value Creation

Academy Sports has been ameliorating its customer experiences lately to attract customer loyalty and create value for customers. For instance, the company has redesigned checkout experiences and retrofitted its merchandise store presentation so that it makes appealing to customers. These measures, though seem insignificant at first glance, do help the company to improve its overall customer satisfaction rate, which will likely prompt customers to revisit ASO for future checkouts.

Academy Sports & Outdoors

Financial Analysis

{kind=link}

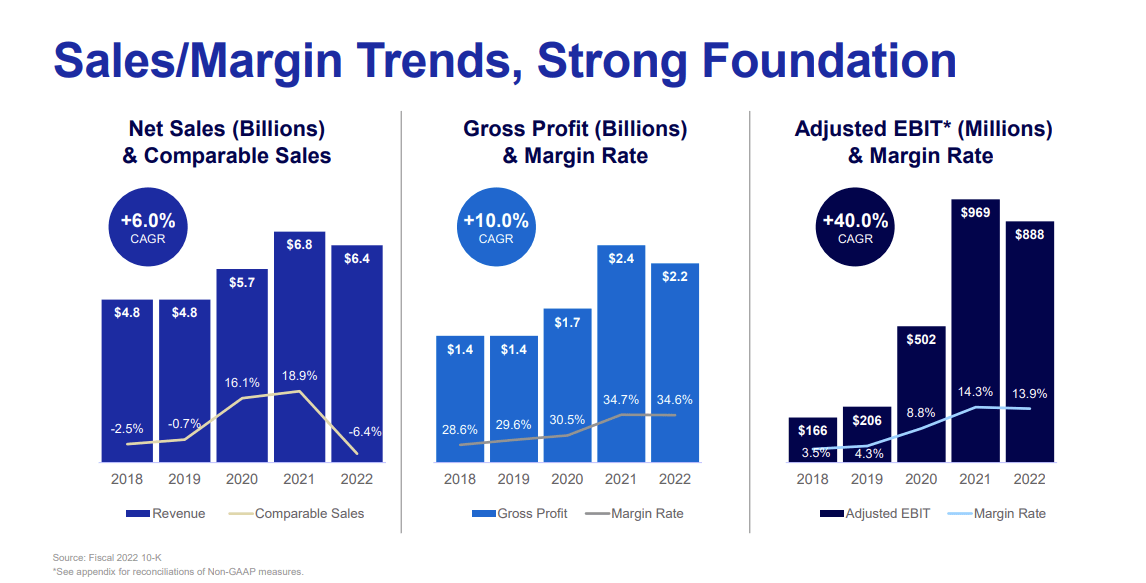

Academy Sports has seen a significant improvement in its financials starting from its turnaround plan back in 2018. Revenue was up from $4.8 billion in FY2018 to $6.4 billion in FY2022, growing at a CAGR of 6.0% despite a slight pullback in 2022. Gross profit margin has also slightly improved from 28.6% to around 34.6% from FY2018 to FY2022, whereas operating margins climbed from 3.5% to 13.9% from FY2018 to FY2022. This illustrates that ASO has leveraged its economies of scale and cost efficiencies over the past 5 years.

The company has also rewarded shareholders through debt reduction, share buyback programs and dividend payouts. For example, net debt for the firm has shrunk from $1.3 billion in FY2018 to just $250 million in FY2022.

ASO has also laid out its vision to achieve $10 billion in net sales by 2027 in its forward guidance. Through this, $2.4-2.8 billion of incremental revenue will come from new store expansion, $0.7-0.9 billion will come from omnichannel online sales, and the remaining $0.5-0.7 billion will come from improvement in existing store checkouts.

Valuation

ASO Revenue and EBIT Forecast (KL Research)

{kind=link}

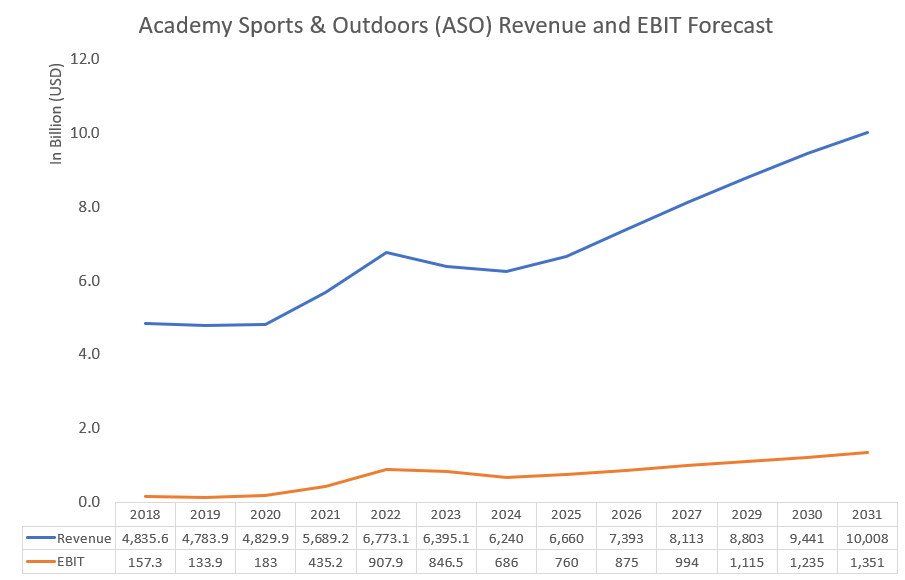

Analysts are forecasting a drop in revenue for ASO of 5% in 2024 to $6.24 billion due to macroeconomic headwinds. However, I expect ASO to recover its luster in 2025 and re-accelerate to achieve double-digit growth from 2026-2027 onwards, as the economy and discretionary expenditures gradually recover. Management teams are expecting ASO to achieve $10 billion in net sales by 2027, but I tend to stay on the conservative side and I personally expect ASO to reach $10 billion in net sales only in 2031.

As for operating margins, I predict ASO's EBIT margins to be around 12-14% over the next 8 years, which is in line with the company's forward guidance. After subtracting the ~$200-350 million of capital expenditures for future store growth expansion annually, and around $200 million for changes in NWC, we're left with $350-450 million of annual unlevered free cash flow for the business annually.

ASO Financial Model Assumptions (KL Research)

{kind=link}

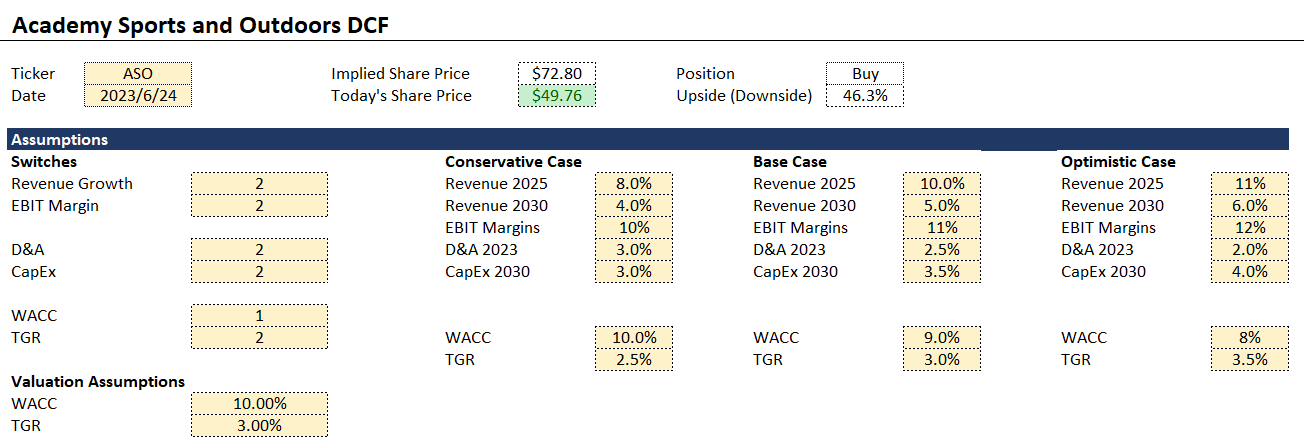

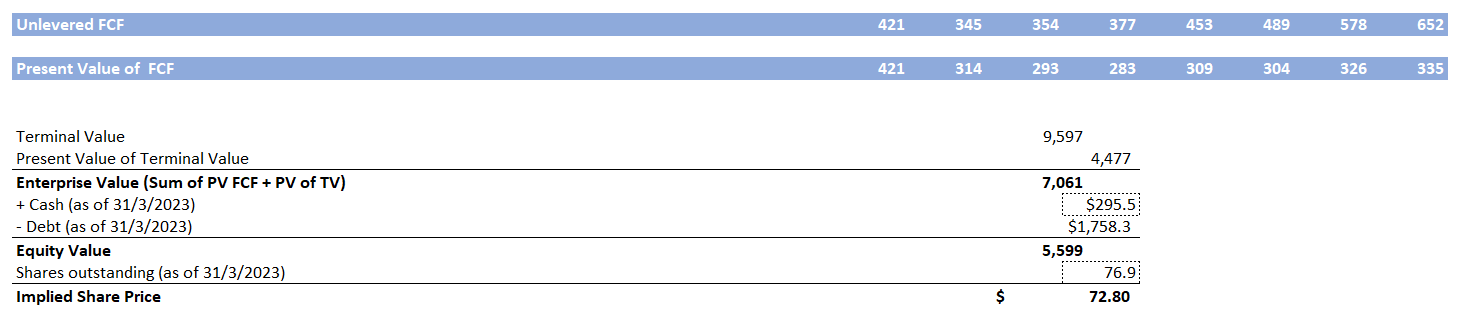

By using a discount rate of 10% and a perpetual growth rate of 3%, I have arrived at an enterprise value for Academy Sports of around $7 billion. By adding back the $295.5 million amount of cash while subtracting its total debt of $1.7 billion, and dividing it by the total amount of outstanding shares of 76.9 million shares, I have arrived at a fair value of around ~$70-80 per share, implying a 40-50% upside!

ASO Intrinsic Value Calculation (KL Research)

{kind=link}

With a 25% Margin of Safety, I rate ASO as a great "buy" when it is trading at a price below $55 , which offers a great buffer for the risk and uncertainties involved in the business.

To provide another perspective, by using comparable company analysis, ASO is now trading at a compelling valuation relative to its peers. The company is now trading at a P/E GAAP ((TTM)) of just 6.92x, well below its competitors like Dick's Sporting Goods of 11.54x. The P/B and P/CF multiple of ASO are now at 2.21x and 7.33x respectively, which is equally well below DKS' multiples of 4.31x and 12.48x respectively, and this could be an indicator that Academy Sports is undervalued relative to its competitors .

Potential Risks

Despite the compelling growth prospect as well as the stock's cheap valuation, there are still some underlying risks behind the business that are worth considering before you make an investment.

Economic Recession Headwinds

First of all, the long-expected economic recession this year might impair the company's top-line and bottom-line growth. As the economy slows and unemployment rises, this may hamper people's incentives to purchase discretionary items like sporting and outdoor equipment, which might place some headwinds for business sales going forward this year. In fact, ASO has already revised downwards its forward guidance for revenue and EPS this year, sending massive shockwaves among investors and Wall Street.

However, I believe such a phenomenon shall be temporary. When the economy recovers next year, I expect ASO to pick up double-digit growth again after 2024. Hence, short-term economic headwinds shall not impair ASO's long-term economic strength and strong fundamentals.

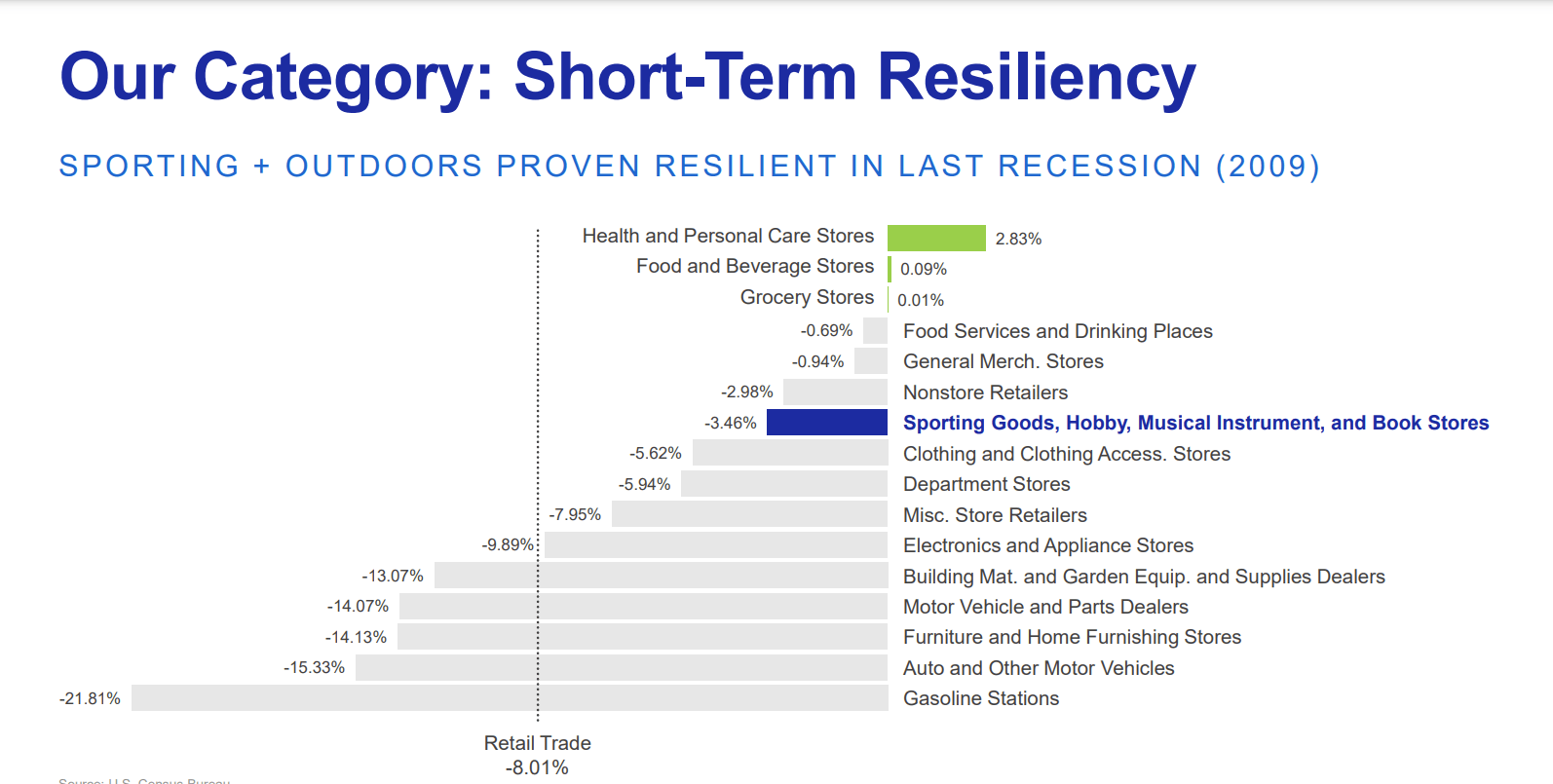

To add on, sporting and outdoor equipment tends to be less elastic due to the sticky nature of personal hobbies, which makes ASO's revenue stream much more resilient compared to other discretionary industries. In fact, the business sales of the whole Sporting Goods Industry only fell by a minor 3.46% back in the Great Recession of 2009, illustrating the fear from Wall Street has been grossly magnified.

{kind=link}

Conclusion

Despite the recent fall in share price, Academy Sports and Outdoors remain well-positioned for future growth, supported by its robust store growth expansion, enhancement in its omnichannel experiences as well as its great customer experience. Its differentiation in-store productivity and sales conversion also make ASO strongly positioned among its competitors over the long run. Given the recent dip in share price and the pessimism of Wall Street, I believe the cheap valuation with a 50% upside potential makes ASO stock a great "Buy" opportunity for investors looking for long-term compounding under a risk-to-reward perspective.

For further details see:

Academy Sports and Outdoors: Long-Term Compounder Supported By Strong Fundamentals