ACAZF - Acadian Timber: Pricing The U.S. Housing Weakness (Downgrade To Hold)

2023-06-13 00:27:45 ET

Summary

- Acadian Timber's Q1 2023 EBITDA missed estimates due to contractor challenges and warm weather in Maine, impacting harvest levels and margins.

- FCFs were not sufficient to cover the quarterly dividend payment, and carbon credits monetization was further delayed.

- Our 12-month outlook remains rather mixed on the US housing market. Therefore, we moved our rating to an equal-weight valuation.

In 2023, the Forest Products sector showed signs of promise ( NBSK and average pulp price are stabilizing); however, the sector is notoriously cyclical with rather accentuated moves. Perfect timing is typically elusive and the US housing market's future performance is likely to take a hit .

Acadian Timber Corp. (ACAZF) (ADN:CA) has usually offered a relative defensive appeal along with underlying optionality on carbon value (and a safety dividend yield). Here at the Lab, this has always been a compelling upside (previous analysis called: " Expecting The Carbon Credit ") and could be significant in the medium-term horizon. Despite that, after having analyzed the Q1 update, we decided to lower our estimates. Downside risks are equally important and the US housing market weakness could lead to a decremental return in the next twelve months. In addition, since our initiation of coverage , we almost reached our target price of CAD $18 per share, and including the generous DPS payment, we outperformed the S&P 500 return.

Mare Evidence Lab's past analysis

{kind=link}

Q1 results

Very briefly, Acadian Timber delivered an adj. Q1 2023 EBITDA of $5.6 million and missed Wall Street numbers that were forecasting $6.42 million. Looking at the detail, the largely selected issues included 1) New Brunswick sales with 50k m3 lower volumes, and 2) lower Maine sales volume for an additional 48k m3. Therefore, the company delivered top-line sales of $22.4 million. The main EBITDA contractor was the Maine adj. EBITDA which was estimated at 30% and resulted in a 25% margin.

Acadian Timber Q1 Financials in a Snap

{kind=link}

Here at the Lab, we should also recall that Maine operations were limited by adverse weather conditions that limited contractor capacity. However, as already seen in the past, contractor challenges translated into weaker-than-anticipated harvesting. This might pose an additional risk to Acadian Timber's future.

Acadian Timber - harvesting detail

{kind=link}

Despite the above, lower harvesting activities also mean saving costs in the company's P&L, but despite the price increase, the Maine impacts and lower volumes resulted in an EBITDA miss. Our future outlook remains rather mixed with higher interest rates and inflationary pressure that will hit Acadian Timber's end market. In addition, we also report that the carbon credit project was postponed in Q2 2023.

{kind=link}

Changes to our estimates

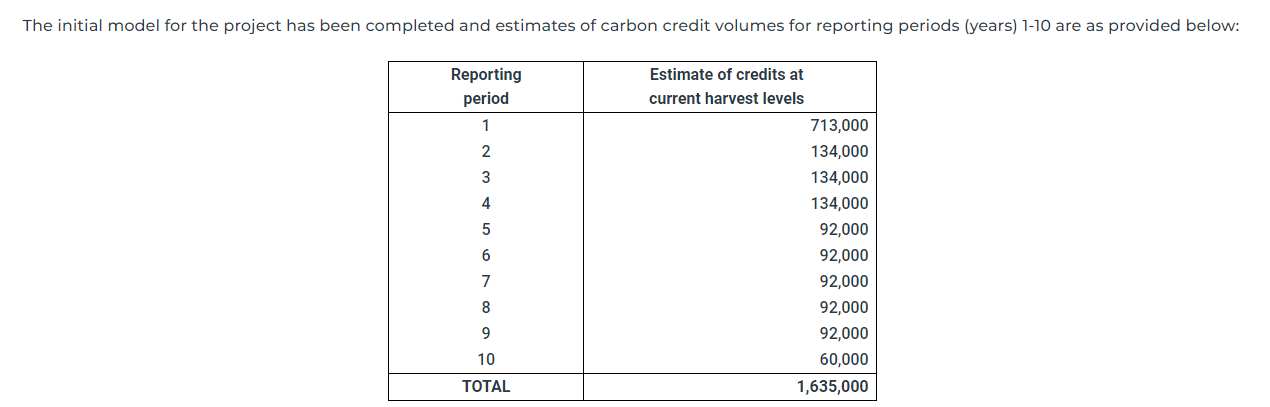

- Compared to our previous estimates, we decided to leave unchanged our initial carbon gross revenue credit estimates at $0.7 million. Carbon credits are now forecasted to be registered in Q2. According to the company's note, the credits will be immediately available-for-sale (Fig 1). Therefore, we are estimating postponing carbon credit sales in Q3;

- Given a negative outlook, we are estimating lower revenue generation for the year. Due to the Q1 results, our top-line sales projection is now at $84.2 million;

- As already mentioned, Acadian Timber interest expenses are in the 2.7% and 3.0% range + the 90-day LIBOR spread. For the above reason, we are forecasting slightly higher interest expenses vs the $3.1 recorded one year ago. Despite that Acadian interest coverage ratio is at 5x;

- The company has sufficient liquidity for the dividend payment; however, in the quarter Free Cash Flows were at $3.7 million and were not able to sustain the current dividend outflow of $4.9 million. As a reminder, Q1 liquidity was at $17.2 million;

- Despite point 4), we are estimating a flat DPS for the following two years;

- After the Q1 results, our 2023 EPS moved to $1.28.

{kind=link}

Fig 1

Valuation and Conclusion

In our view, the Crown timber royalty rates and carbon credits monetization should be still valued as an important upside (and investors should focus more on the longer-term value). However, looking at the twelve-month horizon, we do not place emphasis on quarterly figures and Acadian Valuation looks full. Considering the US real estate market bubble, 2024 implied P/E is at 18x with a 15.8x EV/EBITDA ratio. For this reason, we decided to lower our buy rating to a neutral one with a target price of CAD 17.5 per share. On the risk side, we should also recall that Acadian Timber's stock price suffers from trading liquidity. In the short term, as already witnessed, weaker-than- anticipated harvest might impact the financials. Additional risks include interest rate movements; FX movements, forest infestations, and labor shortages (this was also emphasized in the company's latest interim report).

{kind=link}

For further details see:

Acadian Timber: Pricing The U.S. Housing Weakness (Downgrade To Hold)