KBWY - Accelerated Household Formation Could Result In A Protracted Downturn

Summary

- The pandemic caused a surge in household formation, driven in part by remote work and low-interest rates.

- This is likely to result in an extended period of weak growth in the number of households, with a flow-through impact on the rest of the economy.

- The housing sector is an important part of the economy and influences activity in other sectors. Consumer spending is also related to household formation.

Housing is one of the most important sectors of the economy and is often at the heart of the business cycle. The sensitivity of real estate to interest rates and the tendency for activity to be pro-cyclical creates the potential for overly large swings. The last few years have seen strong demand for housing, driven in part by remote work and low-interest rates. This is likely to prove to be unsustainable though, with demand pulled forward rather than increasing. The US housing market now appears set to undergo an extended downturn, with large flow through effects on the rest of the economy. While the housing bubble is already correcting, its impact is still feeding through to the rest of the economy.

Household Formation

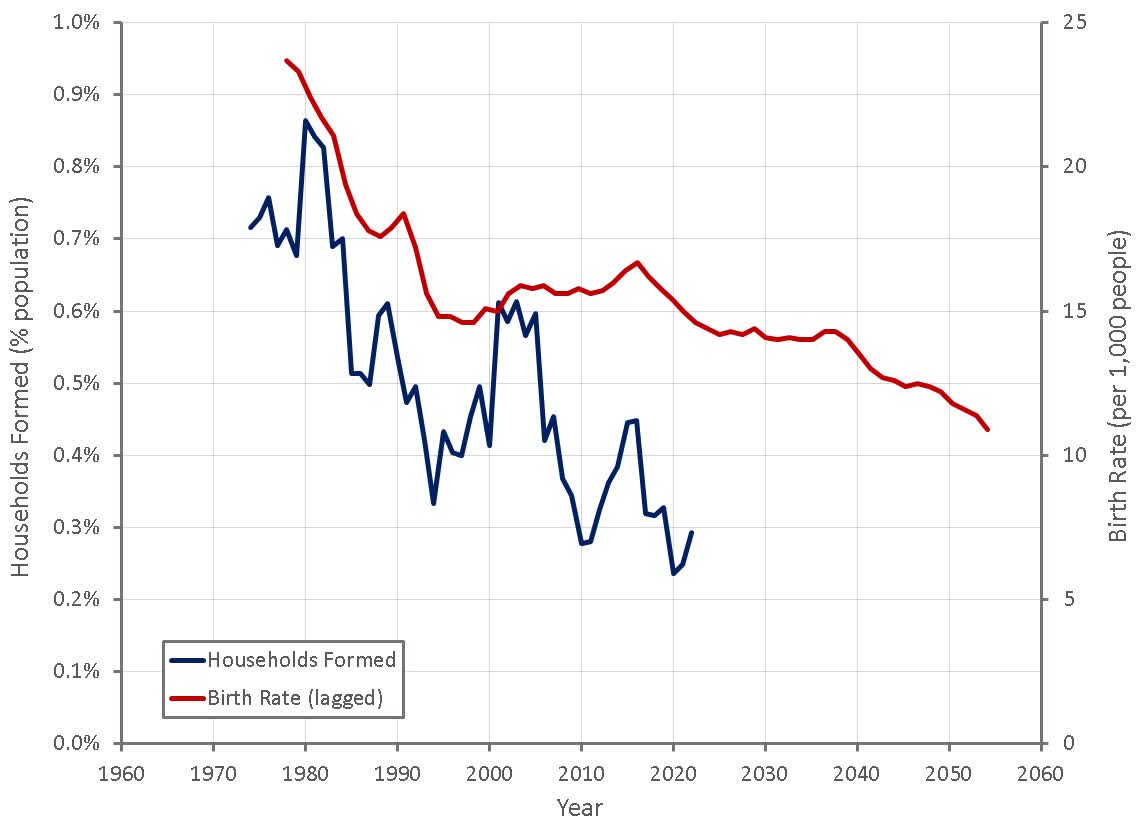

Demand for housing is driven by the size of the population and the average household size, both of which have a tendency to change slowly over time. Birth rates in developed economies have been declining, although many countries have tried to offset this with relatively high immigration rates. The combined impact is somewhat complex as births only add to demand with a large lag, whereas immigration generally contributes to demand immediately.

The lag between waves of new births and household formation is also not constant over time, and there appears to be a general trend for younger generations to form new households later in life. Due to this variable lag, it is difficult to make assessments about housing demand, but it would appear likely that there will be an extended period of low growth in household formations going forward, particularly as COVID likely accelerated household formations significantly.

Figure 1: US Household Formations and Birth Rates (source: Created by author using data from The Federal Reserve)

{kind=link}

Between 2010 and 2016, the number of adults in the US increased on average by 2.3 million per year . Since 2016, population growth has been weak though (approximately 1.5 million in 2021), due in large part to a reduction in immigration. Recent growth in the number of households has been driven more by a reduction in average household size than population growth. Smaller household size could be maintained going forward, but given the impact of COVID, it would also not be surprising to see this trend reverse somewhat.

Household formation was low after the global financial crisis as the number of people living with adult family members who were not their spouse increased by approximately 2% , the equivalent of several million adults. This appears to have been reversed somewhat by COVID, as fewer adults are living with roommates and more are living alone. The extremely strong labor market has also likely contributed to housing demand, as headship rates are generally higher amongst the employed than the non-employed.

The COVID pandemic caused a spike in remote work, with nearly a third of employees still working from home part time or full time as of August 2022. The Federal Reserve Bank of San Francisco recently published an economic letter which showed remote work drove over 60% of the US housing market's home price surge. While many expect work from home to become a permanent fixture, any shift away from remote work could contribute significant downward pressure on home prices and rents.

Part of the reason that remote work has proven relatively sticky, could be due to employee preference and the relatively high bargaining power of employees due to current labor market conditions. An economic slowdown and subsequent slackening of labor markets could rapidly change this situation and reduce the amount of remote work.

There appears to be a preference for laying off remote employees, with 60% of surveyed managers say it's more likely that remote workers will be cut first. The survey was of 3,000 managers across a wide spectrum of sectors, including health care, finance, retail, software, and construction.

There is also the potential for employee perceptions to result in a gradual reduction in remote work over time. For example, 78% of American workers reportedly worry that remote workers would be more at risk of losing their jobs during a recession that led to layoffs than full-time office workers. 68% of workers are concerned that their manager would view full-time office workers as high performers and full-time remote workers as lower performers. Another remote work survey found that only 15% would apply for a job that required full-time office work in 2021. In 2022 that figure was 63%, a dramatic change in only 12 months. In 2022, 44% of surveyed employees said they preferred working from home compared to 68% in 2021.

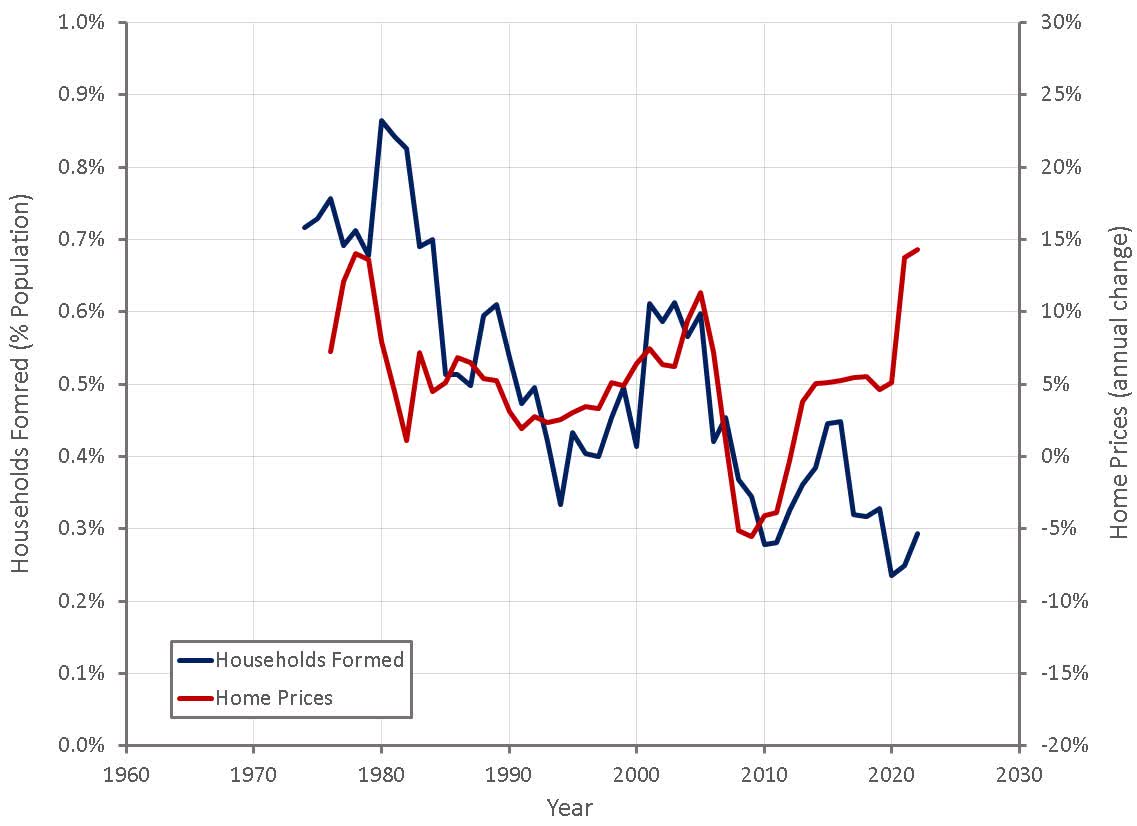

Somewhat counterintuitively, household formations are also likely pro-cyclical, meaning that the number of new households increases when home prices are rising. While this is difficult to assess, as household formations also contribute to rising prices, it appears that housing is viewed as an investment as much as a consumption good and hence rising prices increase demand by creating positive sentiment. This was likely a significant factor over the last few years as many buyers suffered FOMO. It also bodes negatively for demand going forward, as prices appear set to decline significantly, potentially discouraging investors for an extended period of time.

Figure 2: US Household Formations and Home Prices (source: Created by author using data from The Federal Reserve)

{kind=link}

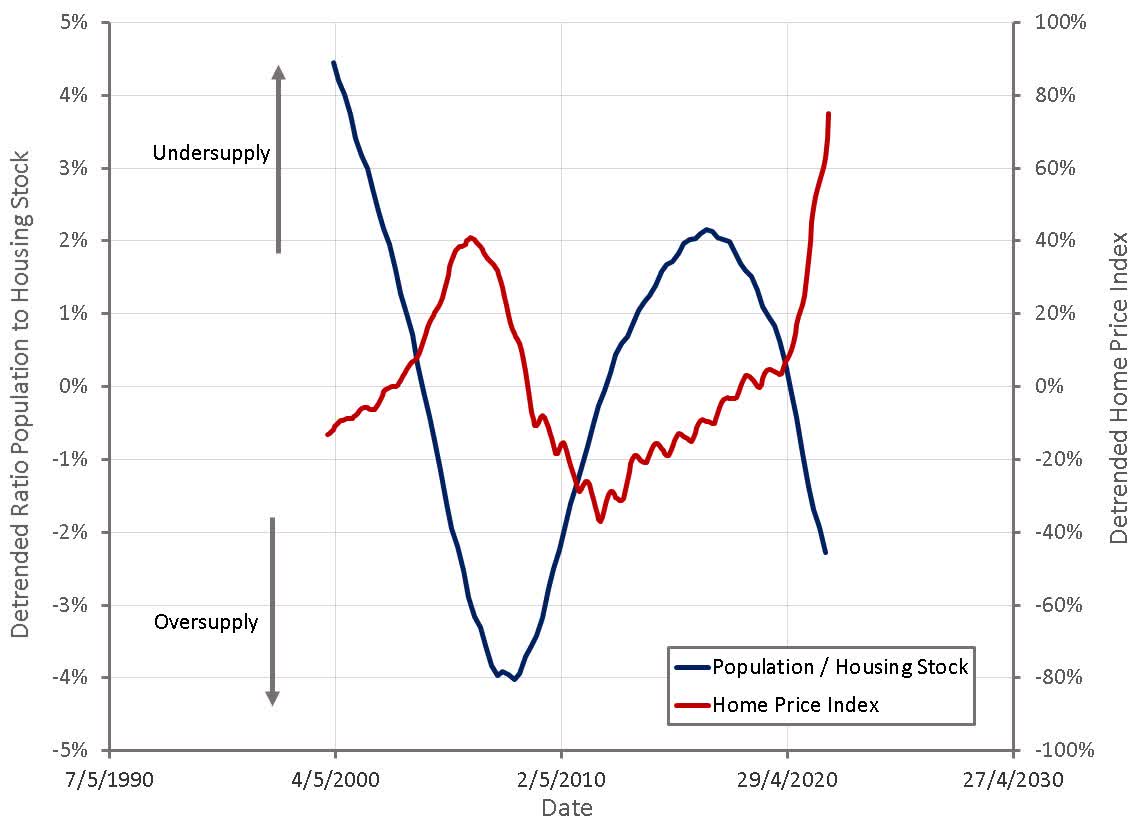

These factors have combined to create the appearance of a tight housing market, which is probably not actually the case. At an aggregate level, the stock of housing appears large relative to the size of the population. This is difficult to assess, as smaller household size may become the norm going forward and the supply of housing must match demand in terms of physical attributes (size, quality, etc.) and geographic location. If the supply of housing is actually relatively high, it would be reasonable to expect an extended period of weak construction activity going forward, with consequences for the rest of the economy.

Figure 3: Housing Stock and Home Prices (source: Created by author using data from The Federal Reserve)

{kind=link}

Housing Multiplier

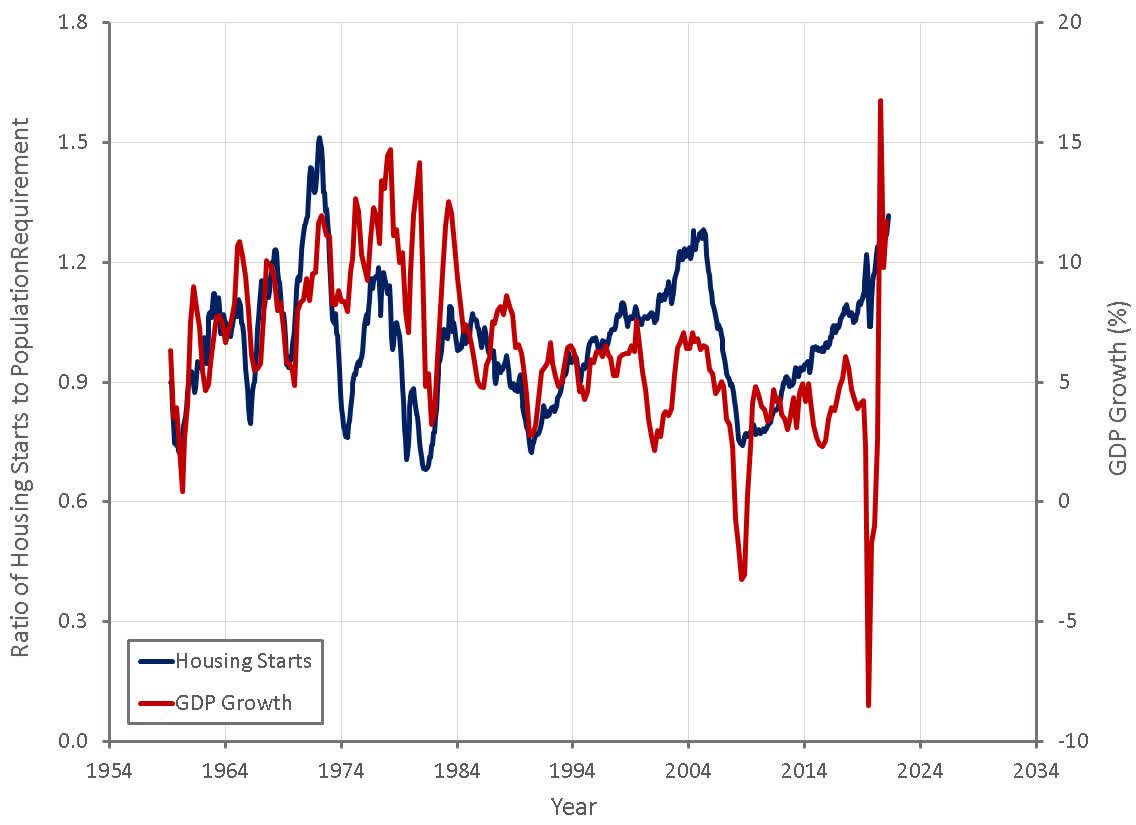

The direct impact of the housing sector on economic output averaged approximately 3% of GDP in the 2000s. While this is important, there is also flow through effects on the rest of the economy the amplify the importance of the housing sector. In the UK, it has been estimated that every pound invested in housing construction results in a total economic impact of approximately 2.09 pounds .

Housing starts and economic output have historically been closely related, and a large decline in housing construction would be expected to result in weak or negative GDP growth.

Figure 4: US Housing Starts Relative to Population Requirement (source: Created by author using data from The Federal Reserve)

{kind=link}

Consumer Spending

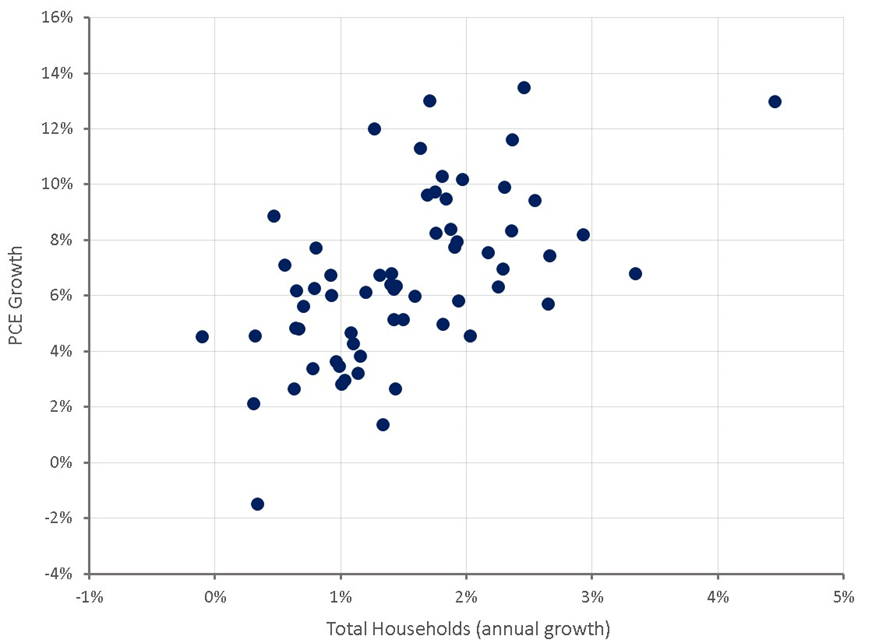

The impact of accelerated household formation on consumer spending also needs to be considered. When a new household is formed, a large amount of spending activity is also likely to occur on items like:

- Furniture

- White goods

- DIY home repairs

- Home exercise equipment

- Pets

If growth in the number of households is weak going forward, demand in these types of categories is also likely to be weak, creating a drag on the economy.

Figure 5: Impact of Household Growth on PCE Growth (source: Created by author using data from The Federal Reserve)

{kind=link}

Conclusion

Demand for housing spiked during the pandemic due to a combination of factors. These factors are likely to unwind in coming years though, creating an extended period of weak housing demand. With a large supply of new housing set to come onto the market, this is likely to result in downward pressure on home prices and rents. While this should help to reduce inflationary pressures in time, it is likely to be negative for the economy as the housing sector is the driver of a large amount of economic activity. With a large amount of demand being pulled forward by the pandemic and low mortgage rates, the Fed may also find it difficult to reinvigorate demand in the event of a recession.

For further details see:

Accelerated Household Formation Could Result In A Protracted Downturn