ACCO - ACCO Brands Is At A Cyclical Discount

2023-03-21 14:19:42 ET

Summary

- ACCO Brands Corporation's stock is relatively undervalued and presents a lucrative dividend yield worth more than 6%.

- The company's recent woes were a consequence of elevated raw material costs. However, key metrics imply that ACCO's cost base is set to improve.

- The company's latest restructuring is yet to illustrate tangible results. Nevertheless, we think ACCO Brands' corporate strategy will yield success.

- Systemic and idiosyncratic risks persist. Yet, we back ACCO Brands' stock to recover in the coming quarters.

ACCO Brands Corporation ( ACCO ) has shed more than 40% of its market capitalization during the past year. Although ACCO stock has primarily suffered from a broad-based stock market drawdown, other issues played a big part in its below-par performance. For instance, the company suffered from factors such as rising input costs, a sustained competitive landscape, and weakening consumer demand for cyclical goods and services.

However, despite ACCO's poor run of form, we consider its stock undervalued and think its business model is about to reach an inflection point.

Here are a few of our latest findings on ACCO Brands.

Cyclicality Is Playing Ball

Past Results

ACCO's past sales and gross profit margins clearly illustrate the company's cyclical nature. The school and office supply business is extremely competitive, and consumer switching costs are almost negligible. Therefore, ACCO Brands tends to suffer whenever costs rise, and consumer demand tapers.

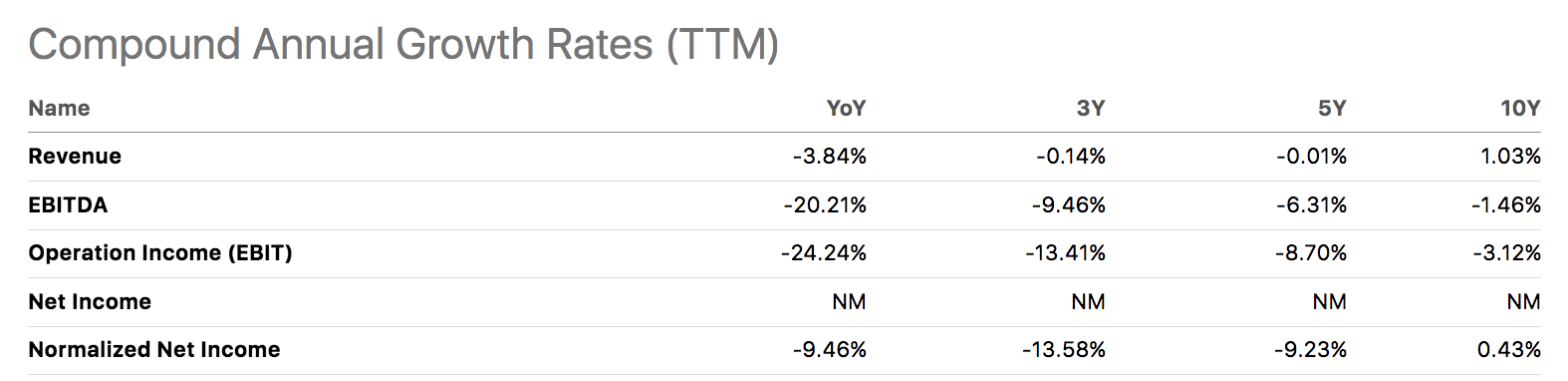

We believe the sharp increase in raw material prices in 2022's coupled with slower cyclical goods demand dampened ACCO's profitability. To support our claim, the company's gross profit and EBITDA margins are currently 9.10% and 20.19% lower than their cyclical averages.

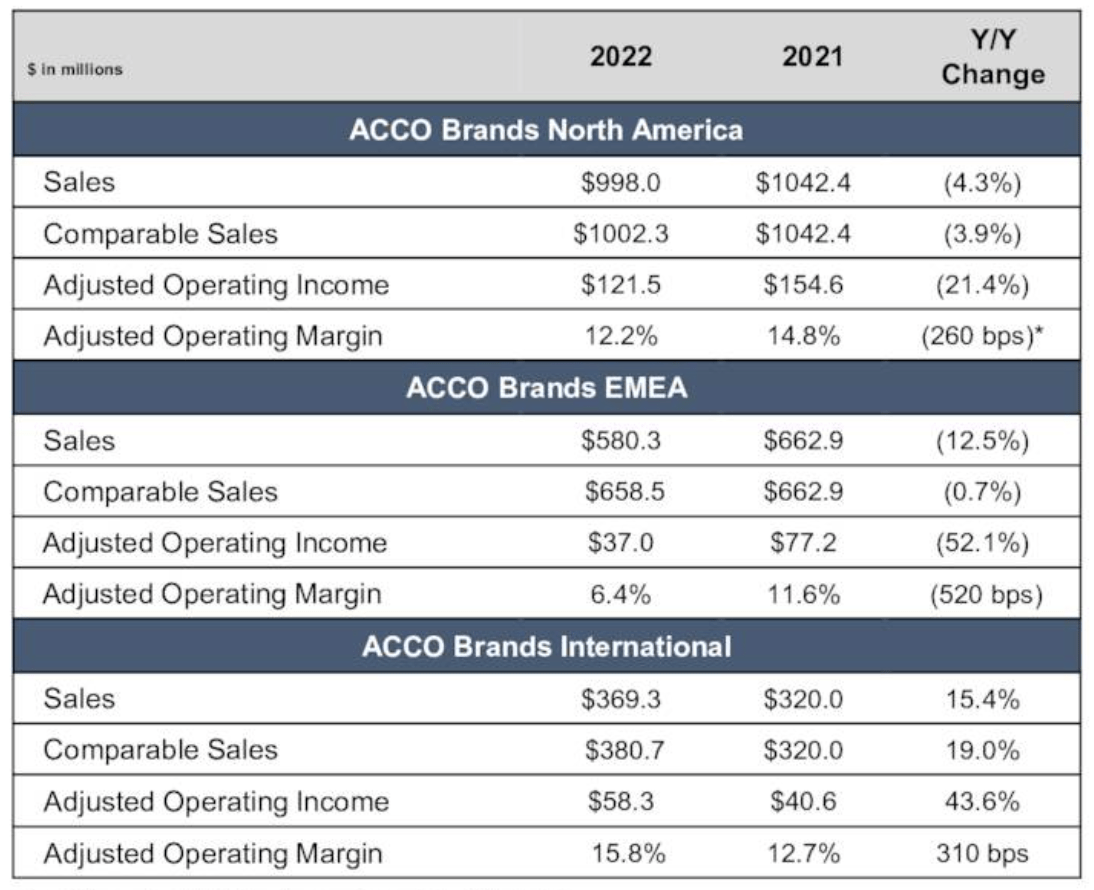

Let us look at a few salient features relating to ACCO Brands' fourth quarter and latest fiscal year.

ACCO experienced a broad-based decline in sales in North America and the EMEA. The firm's softer sales in North America were primarily driven by decreasing retailer confidence, which resulted in downstream outlets carrying leaner inventory. Again, we would like to reiterate cyclicality, and we do not expect this phenomenon to sustain into perpetuity as GDP growth traverses in ebbs and flows.

Furthermore, ACCO's lower sales in the EMEA were partially due to a stoppage of sales in Russia, which we, unfortunately, see as a core/sustainable event. Furthermore, heightened utility bills and food prices in the region resulted in pressure on household balance sheets, which phased out the demand for school stationery and office equipment. Another concern for ACCO was weakening currencies in the EMEA region, which caused a 12% year-over-year segmental translation loss.

{kind=link}

Lastly, ACCO Brands experienced an improved quarter pertaining to its international segment amid a return to in-person education in Latin America. ACCO achieved a 19% comparable sales growth figure accompanied by a 40% surge in operating margins due to the aforementioned reasons and ACCO Brands' regional stronghold via brands such as Tilibra and Foroni.

A Look at What is In Store

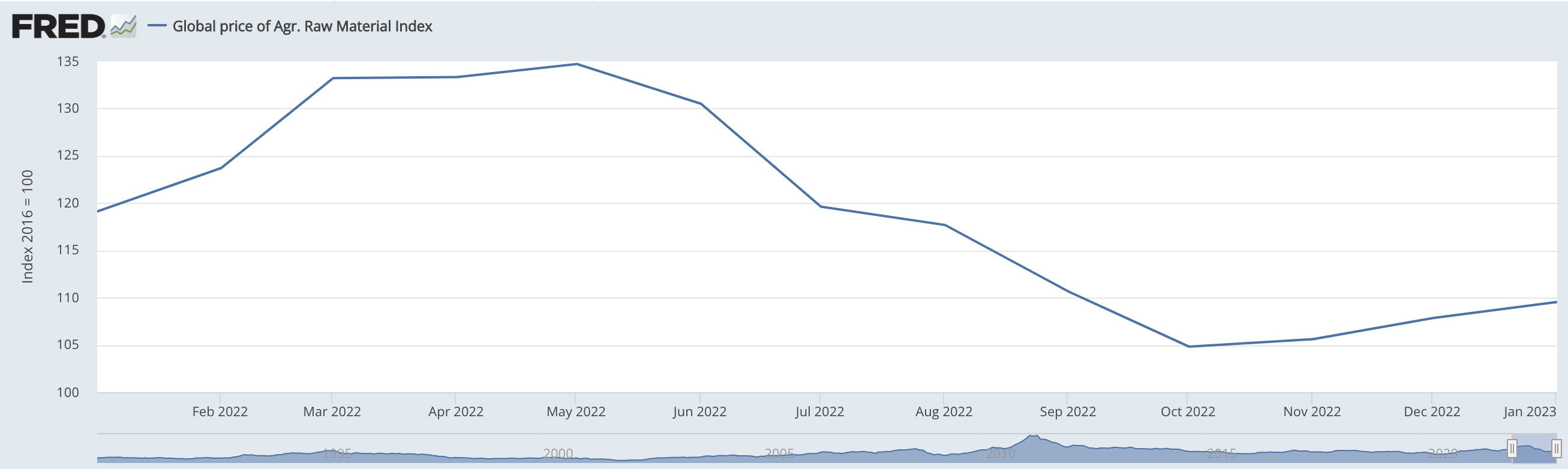

A catalyst for change this year might be the receding raw materials price index. In our view, raw materials still have room to slip as supply catches up with demand and interest rates continue to cap inflation growth. Although GDP growth might soften in the coming quarters, lower input costs will likely play a more significant role for ACCO Brands as the company's expenses seem more elastic than its sales growth.

{kind=link}

Furthermore, the firm cited shipping costs as a significant influencing variable. Congested supply chains seem to have eased as shipping costs are trending downward; this could act as a significant cost-saving tool for ACCO, especially relating to the price of raw materials and its international and EMEA sales.

{kind=link}

Idiosyncratic

ACCO Brands is restructuring its business model to stay with the times as the world transitions into more digitalized office and schooling models. There is no doubting the fact that slowing growth has been a long-time problem for ACCO Brands, which it plans to address by reinvesting in R&D, narrowing down its stock-keeping units, and expanding its footprint in emerging markets.

{kind=link}

Furthermore, the company is actively reconsidering its corporate portfolio. It remains ambiguous whether ACCO will decide to sell inefficient brands while investing in new growth initiatives; however, a restructuring could be priced favorably by the financial markets as it suggests renewed growth is en route.

Specifically, the enterprise seeks to improve its price points by emphasizing its Five Star and Mead brands, which it has identified as essential to achieving maximum value-based sales. Moreover, ACCO is proactively working on automating its supply lines to taper its SG&A costs and consequently increase shareholder value.

Valuation and Dividends

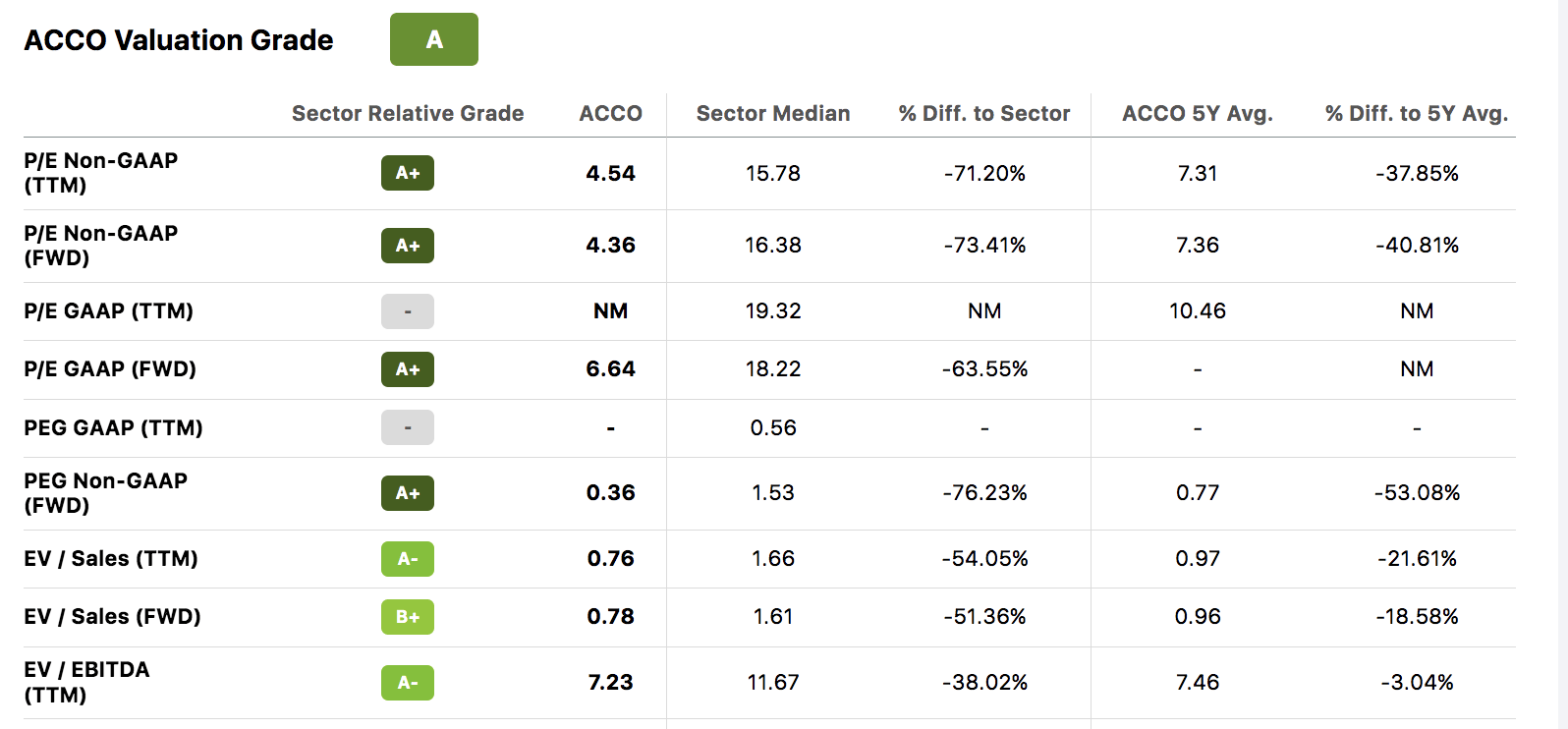

Our theory about ACCO Brands being at a cyclical discount is communicated by its valuation multiples. The company's price-to-earnings ratio is at a normalized discount of 37.85%, while its EV/EBITDA is at a cyclical discount worth 3.04%. Drawing from our fundamental analysis, we think ACCO's EBITDA margins will expand as input costs cool. In addition, existing data conveys that ACCO's post-capital structure multiple (P/E) is underappreciated by financial market participants.

{kind=link}

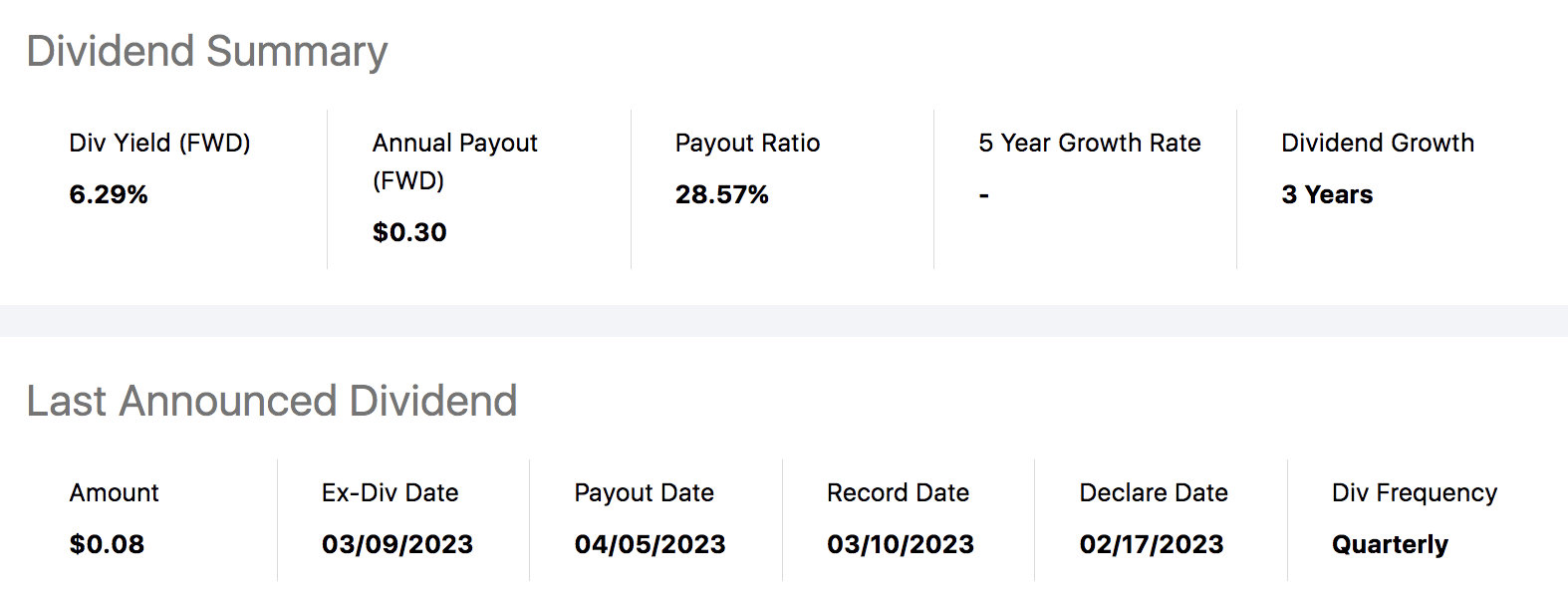

Furthermore, ACCO Brands provides a lucrative dividend profile with a dividend yield and coverage ratio of 6.29% and 3.53 , respectively.

Does the company's recent bottom-line deficit pose a threat? Yes, we think so, as evidence suggests that ACCO implements a constant dividend policy, which links its dividend growth to its business' underlying performance. Nevertheless, investors have an opportunity to lock in a heightened dividend yield on cost considering the stock is 19.06% below its 200-day moving average.

{kind=link}

Noteworthy Risks

As mentioned before, ACCO Brands Corporation is in the midst of a restructuring that will see it streamline its SKUs, automate its supply lines, and rebalance its corporate portfolio. However, tangible results are yet to be witnessed from the restructuring; in essence, the business model's improvement remains "all talk" for now.

Furthermore, ACCO is highly exposed to emerging markets. Drawing from our existing knowledge, emerging markets are struggling with extremely high inflation, posing the risk of slowing consumer spending.

Final Word

Based on our analysis, ACCO Brands Corporation stock presents investors with an opportunity to secure an asset at a severe discount while locking in a lucrative dividend yield on cost.

ACCO Brands Corporation has suffered from severe input cost pressure during the past year. However, the tide has turned amid rapidly declining costs of raw materials. Furthermore, ACCO Brands Corporation is in the middle of a restructuring period, which might see it reignite growth and cut costs by implementing streamlined stock-keeping units, automated supply chains, and adding exposure to emerging markets.

Although this is a risky bet, we assign a strong buy rating to ACCO Brands Corporation stock with an indefinite horizon.

For further details see:

ACCO Brands Is At A Cyclical Discount