ICHGF - Accor: Covid-19 Recovery Priced In

2023-07-03 05:37:37 ET

Summary

- Accor has transitioned its portfolio to a managed and franchised approach but continues to lag behind its peers on an EBITDA-M basis.

- We see growth continuing as China opens and its large pipeline comes online.

- Economic conditions represent near-term headwinds but are not materially slowing the bullish factors.

- Accor is trading at a premium to its historical average, implying its recovery and improvement are priced in.

Investment thesis

Our current investment thesis is:

- Growth is slowly returning, as the impact of Covid-19 subsides. We see improved growth coming from China, as well as the development of its pipeline.

- Economic headwinds and the potential impact of covid-19 on business travel could be an offsetting factor.

- Accor's margins are weak relative to peers, although a noticeable improvement is forecast.

- We believe the company's improved position is priced in, implying no material upside.

Company description

Accor SA ( ACRFF ) is a global hotel chain that operates hotels around the world. The company has three main segments: Management & Franchise, Services to Owners and Hotel Assets, and Others.

Share price

Accor's share price has performed poorly during the last decade, significantly outperforming the market as a whole. This has been driven by poor financial results during the period, compounded by the impact of Covid-19.

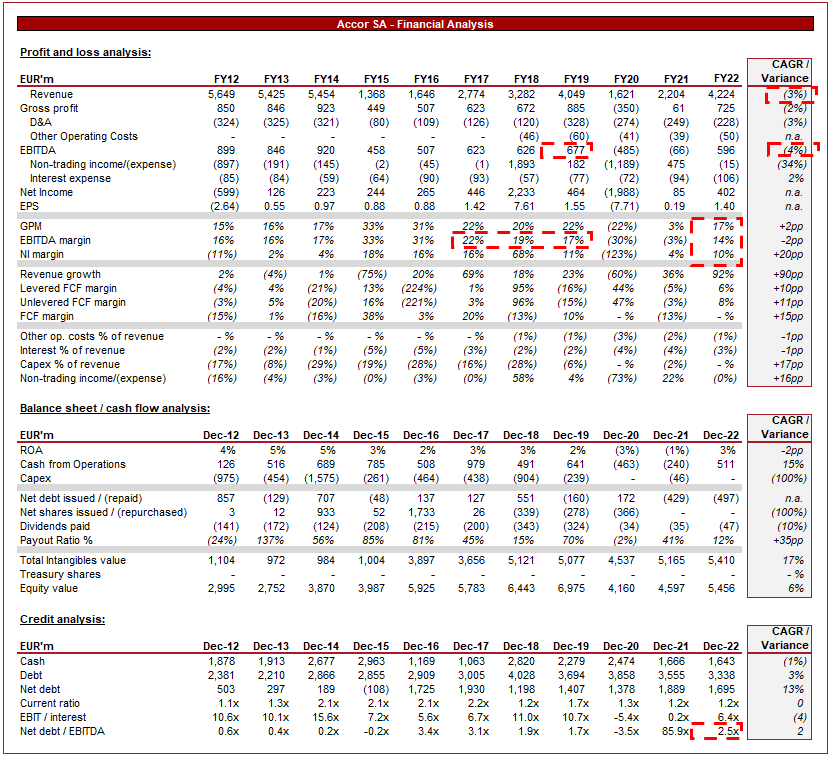

Financial analysis

Accor financials (Tikr Terminal)

{kind=link}

Presented above is Accor's financial performance for the last decade.

Revenue & Commercial Factors

Accor has experienced significant fluctuations in its revenue throughout the historical period above, primarily due to acquisitions and disposals, as well as a \process of franchising. Overarchingly, the business has traded sideways, although slightly depressed due to the lasting impact of Covid-19.

Business Model and Competitive Positioning

Accor currently operates under a hotel management and franchising business model, diversifying its revenue stream. The advantage of franchising is that the business is able to accelerate its growth by exporting its financing costs. It's far quicker for several investors to build hotels than it is for Accor. Further, this strategy reduces risk, as the franchisee bears the direct cost of operations (employees, maintenance, etc) and thus the success or failure of a property.

Due to the attractive economics, we have seen an industry trend of franchising, as businesses seek to de-risk and create greater certainty of earnings. This is illustrated below, with a small number of owned locations.

Hotels by segment (Accor)

This has allowed Accor to reduce the size of its balance sheet substantially.

Hotel ownership (Accor)

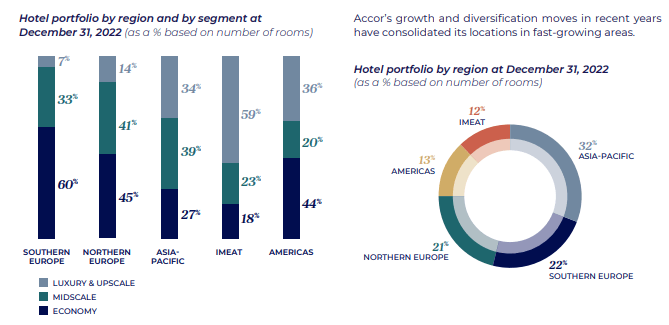

Accor has developed and acquired a range of brands within the industry, managing a wide range of segments, including luxury, premium, midscale, and economy segments. The benefit of this is to increase the company's total addressable market, reaching more consumers and expanding its revenue growth potential. As the following illustrates, Accor's current portfolio is highly diversified, both geographically and by segment.

{kind=link}

Accor's competitive advantage revolves around two key factors. Firstly, Accor owns a portfolio of well-established and recognized brands, providing confidence to those looking to book that they will get their desired level of quality.

Secondly, and in conjunction with the above, Accor has a strong presence in key global markets (Scale), offering a wide range of hotel options. This allows Accor to compete in every key market, increasing the chances of winning volume.

The industry is highly competitive, with many large consolidators such as Accor operating across the value spectrum. For this reason, brand differentiation is critical, which stems from the quality of service provided and price.

Hotel Industry

A key trend impacting the hotel industry is the rise of alternative accommodations, driven by the likes of Airbnb ( ABNB ). This has provided consumers with alternatives to hotels, offering convenience, space, and in some cases, cheaper options. We do not believe this will materially impact the hotel industry, as we have seen the likes of Accor enter the industry, however, it will likely contribute to softening growth relative to the past.

Furthermore, the full impact of Covid-19 remains uncertain. We believe the biggest impact will be on business travel. With the mass adoption of working from home, many realized business travel in some cases was unnecessary. We suspect this will lead to businesses cutting costs by reducing non-critical travel.

Unlike the West, China continued to struggle with Covid-19 into late 2022, as its zero-Covid policy was ineffective. This was dropped in Q4-22, and following a large uptick in cases, the country looks to be returning to a new normal. We believe this will contribute to an uptick in travel from residents of the country, leading to increased near-term demand.

Our view is that there are two key opportunities for Accor to exploit in the coming years. Firstly, we would like to see a the pipeline focused on franchising, further de-risking and improving the company's economics as it develops its capabilities in this strategy. Secondly, expansion of its portfolio remains critical to achieving growth. Organically, Accor has 216k rooms in the pipeline (27% of the total) and 1200 hotels (22% of the total). This opportunity also exists through acquisitions.

Economic & External Consideration

Current economic conditions represent near-term headwinds. With high inflation and elevated rates, we are seeing a deterioration in consumers' discretionary income. As a result of this, consumers are discouraged from tourism, even if they are not materially impacted due to uncertainty about the future.

We suspect this will act as a counterbalance against the improving conditions in China and the overarching recovery from Covid-19.

Margins

Accor's margins are muddied by the various factors impacting the business, as well as its change in portfolio profile. Directionally, the business has underperformed in our view. Margins have not materially improved despite the transition to franchising, likely due to the level of properties it manages. Marriott ( MAR ), for example (slightly extreme given the level of franchising), has seen its EBITDA-M increase from 43.3% in FY12 to 71.7% in LTM Mar23.

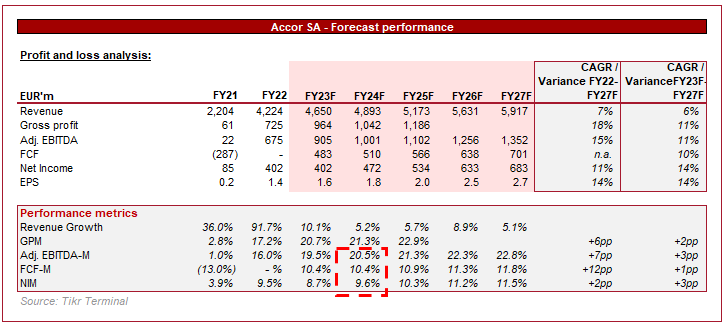

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Accor is forecast to grow well in the coming years, with analysts forecasting a CAGR of 6%. As franchising increased relative to managed and owned, there will be a downward pressure on growth, therefore 6% implies higher organic growth than the absolute amount.

Margins are expected to materially improve, quickly reaching >20%. Given the company was operating at 17-22% prior to Covid-19, we are surprised to see further improvement is not expected.

Industry analysis

Leisure industry (Seeking Alpha)

Presented above is a comparison of Accor's growth and profitability to the average of its industry, as defined by Seeking Alpha ( 31 companies).

The key area of consideration is profitability and Accor currently underperforms. Even with improvement considered, Accor is only expected to reach the average. Our expectation would be for a business of its size to be in excess of this level. As an example, Hilton ( HLT ) currently has an EBITDA-M of 60% and IHG ( IHG ) is at 23.4%. The majority of the businesses below c.20% are non-hotel chains / growing businesses.

Valuation

Valuation (Accor)

Accor is currently trading at 18x LTM EBITDA and 12x NTM EBITDA. This is a premium to its historical average.

Given the margin transition expected in the coming year, we believe readers should focus on the NTM metrics. Based on this, they imply Accor is in a superior position relative to its decade average.

Despite the negative undertone, we do concur with this view. The primary reasons are:

- Even with weaker economic conditions, Accor is not facing another Covid.

- Transitioning to a franchise model is de-risking the business.

- Margins should improve over the coming years.

- The company is at a larger scale.

We struggle to see material upside beyond what is priced in, given the reservations we have about the business, especially when compared to peers.

Final thoughts

Accor owns some of the largest hotel chains globally, with significant scale and expertise in the industry. This operational base is highly attractive and Accor has enhanced this by increasing the % of franchised locations. In 2014, the % of Managed and Franchised locations was 58%, this is now at 97%.

We are slightly concerned by some industry headwinds and the potential impact of economic conditions but overarchingly, stable growth should be possible in the coming years.

Our biggest issue with the business is its relative unattractiveness to peers, as well as its valuation implying its improved position is priced in.

For further details see:

Accor: Covid-19 Recovery Priced In