ACRFF - Accor: Seeking To Disrupt The Hotel Industry Through Expansion Into Luxury

2024-01-05 07:00:00 ET

Summary

- Accor has experienced a lost decade despite transitioning its business model to an asset-light profile, which for its peers allowed for significant margin improvement.

- The company’s recent growth trajectory has been strong, and appears well-placed for 2024, although the impact of economic developments remains uncertain.

- Accor is seeking to expand its luxury segment substantially, which has the potential to improve unit economics and earning stability. This presents some execution risk with market share capture.

- Accor is fundamentally underperforming its peers, with no clear route to closing the gap. This makes it a fairly unattractive option.

- Accor is slightly undervalued, but not sufficiently so to imply value.

Investment thesis

Our current investment thesis is:

- Accor is an underwhelming investment proposition in our view. The company is a serial underperformer, with limited scope to disrupt the status quo. It experienced a once-in-a-lifetime opportunity to improve its fundamental financial profile with the transition to franchising almost its whole portfolio but almost no gains have been made.

- It is performing well currently and will likely normalize above its decade average, with growth tailwinds, but this is still far behind what its peers have achieved. This does technically give Accor greater room to improve but we do not see any results from this.

- Its transition to luxury does have potential but it's yet to be seen if this can move the need in the medium term, analysts appear to be pricing in <2ppts on an EBITDA basis.

Company description

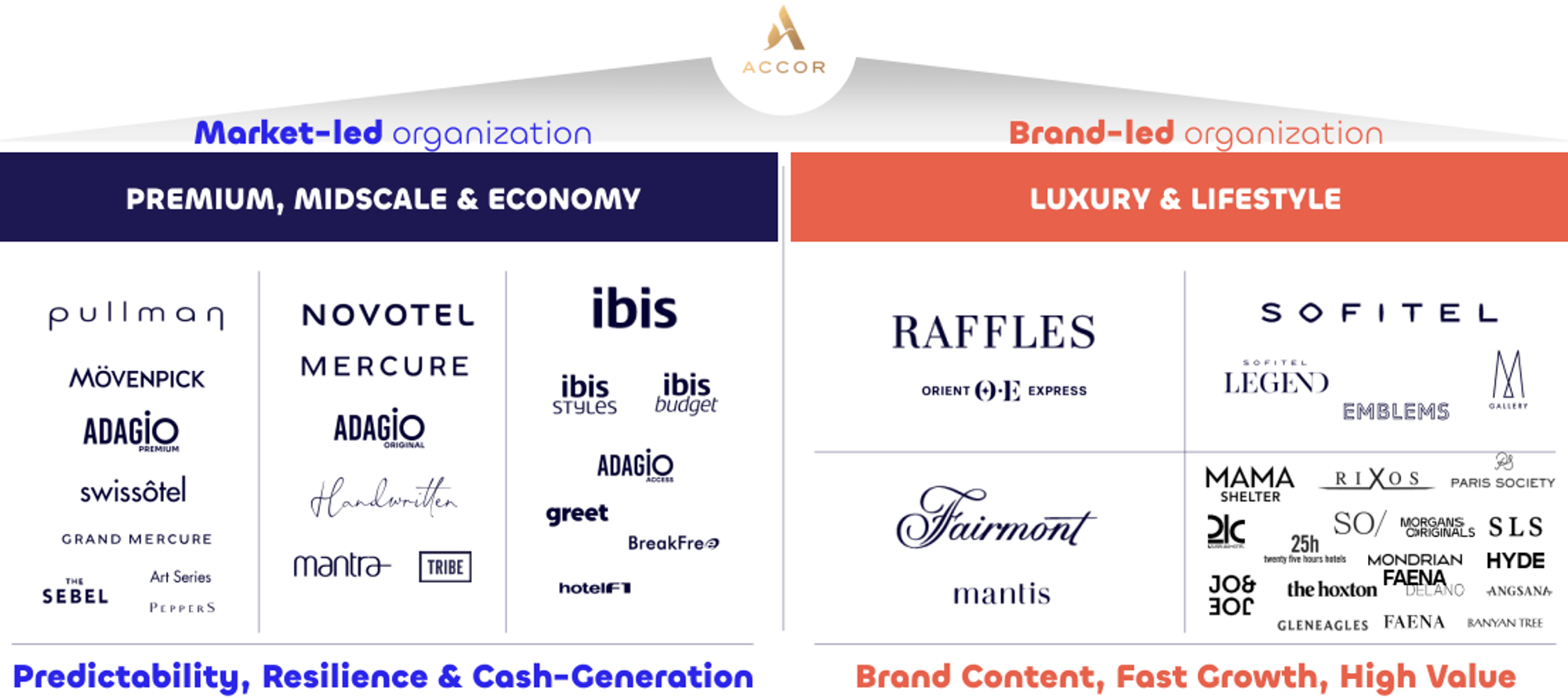

Accor SA ( OTCPK:ACRFF ) ( OTCPK:ACRYY ) is a global hotel chain that operates hotels around the world. The company has three main segments: Management & Franchise, Services to Owners and Hotel Assets, and Others.

{kind=link}

Share price

Accor's share price performance has been incredibly disappointing, significantly falling behind its directly comparable peers and underperforming the wider market. We analyzed the company's business model in 2023 here , with this paper seeking to assess if progress has been made toward improving its fortunes.

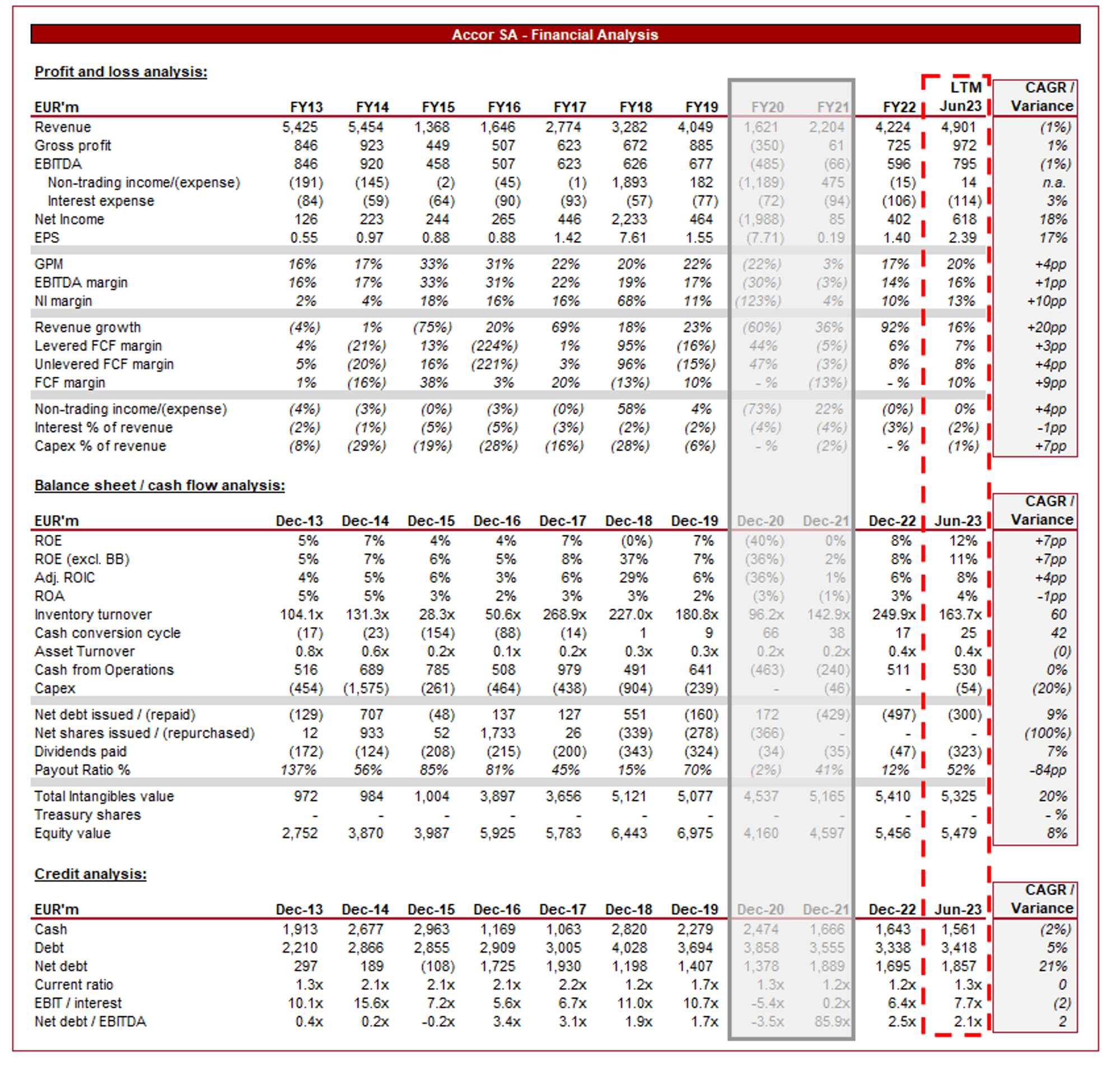

Financial analysis

{kind=link}

Presented above are Accor's financial results.

Revenue & Commercial Factors

Accor's revenue has continued to progress well post-pandemic, with top-line growth of +96%, +109%, +81%, and +39% in its last four half-years. This is primarily a reflection of ramp-up relative to lower comparable periods, as global economies dismiss restrictions and allow travel to return. In conjunction with this, we have seen an unusual expansion of consumer spending, partially funded by healthy wage inflation, with travel demand in particular being robust.

Even as economic conditions have switched negatively for consumers, as a cost of living crisis has ensued, this has had a limited impact on the travel industry. The post-pandemic demand for leisure travel, as well as the expansion of wealth as a result of asset valuation expansion, has allowed this industry to soar.

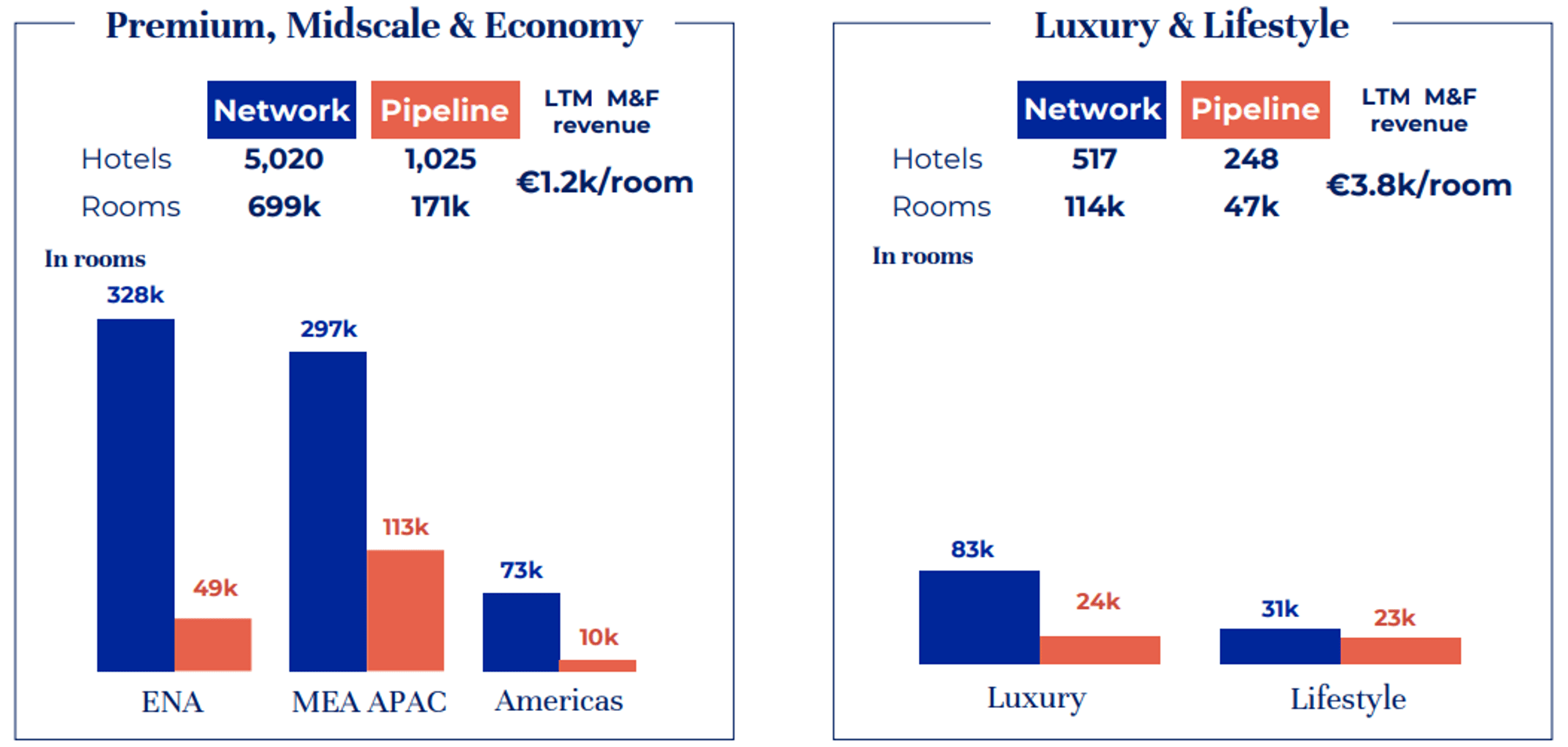

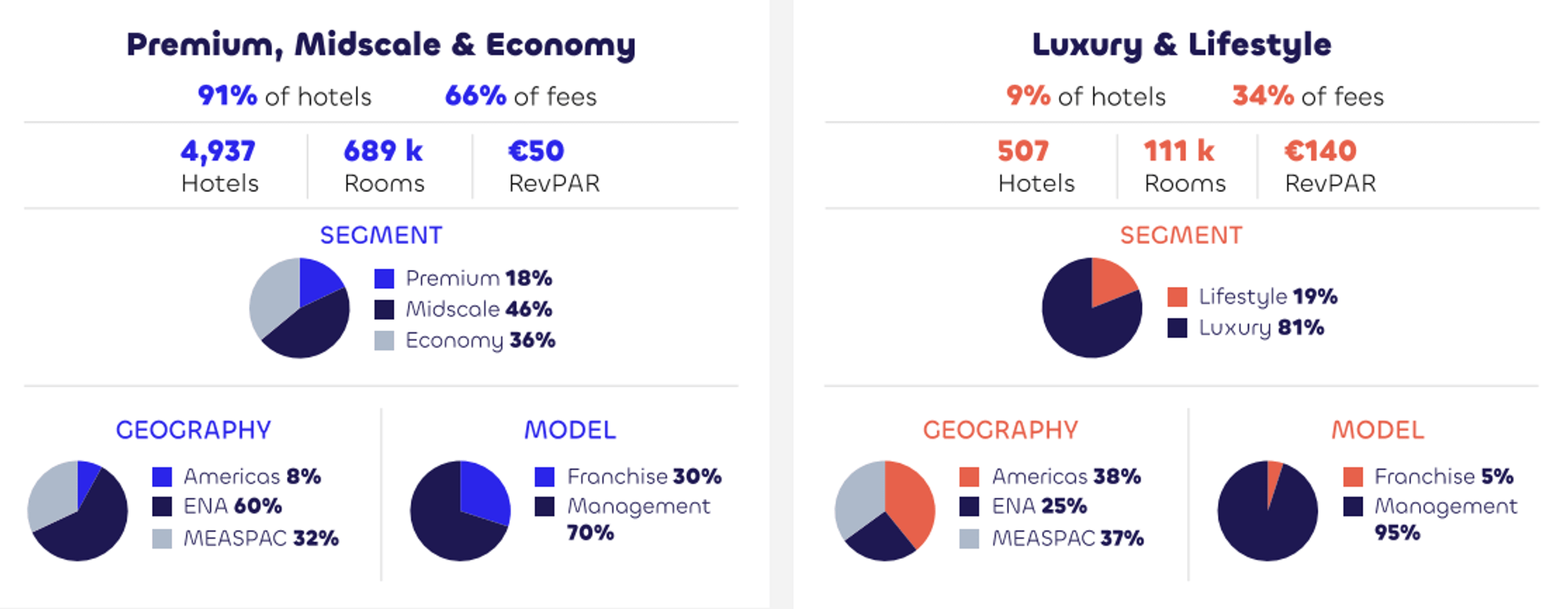

In Q3'23, Accor has maintained its current trajectory. Revenue per available room ("RevPAR") on a system-wide basis was up +15% for its premium, midscale & economy ("PME") segment, while it was up +14% for its luxury & lifestyle ("L&L") segment. This translates to a ~13% like-for-like increase in revenue. Although growth continues to be in the double digits, this is a rapid deceleration relative to the high double digits in prior quarters. This suggests the business has broadly reached equilibrium, with growth now predicated more so on fundamentals and market conditions.

Looking ahead, Accor's pipeline is heavily weighted toward L&L, with ~41% of the current number of rooms in the pipeline. This compares to only ~24% for PME. This is a reflection of a strategic shift toward the luxury segment by many in the industry, given the new-found resilience of the clientele and the greater scope for higher unit economics. We consider this a good decision as it has the potential to significantly improve the company's unit economics. Hyatt (H), a peer weighted heavily in the luxury segment, is currently trading at a ~36% premium to Accor on an NTM EBITDA basis.

{kind=link}

It is worth contextualizing that the company is still primarily weighted toward PME, which is comprised of midscale and economy. One of the primary reasons for Accor's underperformance is its weighting toward these segments alongside ENA, which has underperformed relative to luxury and most other geographies. Although Accor is seeking to differentiate away from these segments, it will likely take several years before a tangible impact is felt.

{kind=link}

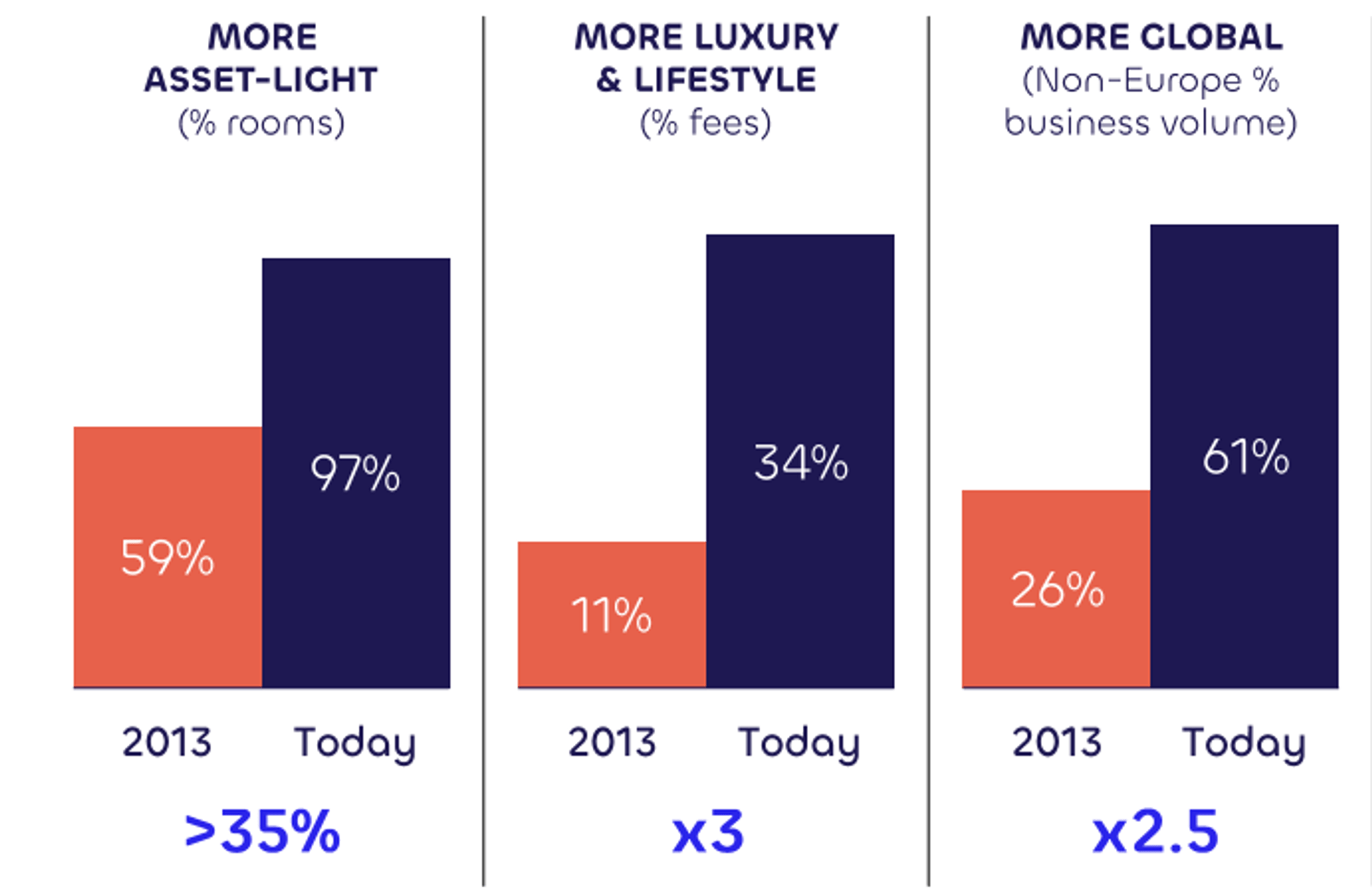

Further, the scope for upside is somewhat limited by the fact Accor has broadly completed its transition to an asset-light model. During the last decade, the majority of hoteliers have aggressively refranchised their properties (and franchised new ones), allowing for margins to aggressively improve and risks to be exported. ~97% of Accor's rooms have been transitioned compared to ~59% in 2013.

{kind=link}

Competitive position

{kind=link}

Accor is a market leader in its primary markets, attributable to its wide breadth of brands and consumer reach within countries. Accor has engaged in strategic acquisitions to expand its portfolio and enter new markets, allowing it to strengthen this position.

Accor's strong brand reputation, built over decades, contributes to customer trust and loyalty. These factors should allow it to maintain its position, particularly as it continues to grow its room numbers to ensure ease of reach.

The company has a robust customer loyalty program, "ALL - Accor Live Limitless," which incentivizes repeat business. Members receive various benefits, including discounts, room upgrades, and exclusive experiences, fostering brand loyalty. This is a similar system operated by its peers, although Accor has done a fantastic job of pushing beyond perks to expand the services offered to improve consumer satisfaction. Spending is ~10% more and importantly, 87% of customers book direct.

{kind=link}

Accor competes with the following peers (also represents alternatives for investors):

- InterContinental Hotels Group ( IHG ): A global player with a focus on brand differentiation and guest loyalty.

- Hilton ( HLT ): Known for its strong international presence and diverse brand offerings. We have previously covered this stock, rating it a hold .

- Marriott International ( MAR ): A major competitor with a diverse portfolio of brands, particularly focused on the higher-end segment. We have previously covered this stock, rating it a buy .

- Hyatt ( H ): Similar profile to Marriott. We have previously covered this stock, rating it a hold .

Accor transition to the higher-end segment will increasingly mean it competes with Marriott/Hyatt's portfolios. We believe the business has the scope to succeed but will be heavily predicated on leveraging its existing customer base through its loyalty systems to market and upsell.

Economic & External Consideration

Current economic conditions have been dominated by inflation and interest rates, with progress finally being made to bringing inflation under control. This said, in a slight turn of irony, the risk of a recession has now reached its peak in the last few years.

This is likely a reflection of the probability of a "straw breaking the camel's back". Consumers and businesses have suffered with inflation and interest rates for an extended period of time, with the belief being that flat retail sales, slowing wage inflation, and a slowly increasing unemployment rate will combine with the cost of living crisis to finally deliver a recession.

This will inevitably impact the demand for hotel services, although we are not convinced this will be sufficient to cause a decline. This is primarily due to the expectation for rates to decline, likely offsetting the risk of a hard landing. Further, the upward cycle is still in effect, even if growth has now slowed, likely allowing the industry leaders to achieve RevPAR in the region of mid-to-high single-digit growth. PwC appears to concur with this view, suggesting travel will remain robust despite "some caution" .

Balance sheet & Cash Flows

Accor is reasonably financed, with a ND/EBITDA ratio of 2.1x. This provides the business is flexibility to expand through debt, alongside increasing distributions by laddering debt with growth. This is also a reason for its poor share price performance, the company has not managed to provide distributions (and growth of this) in line with its peers.

Outlook

{kind=link}

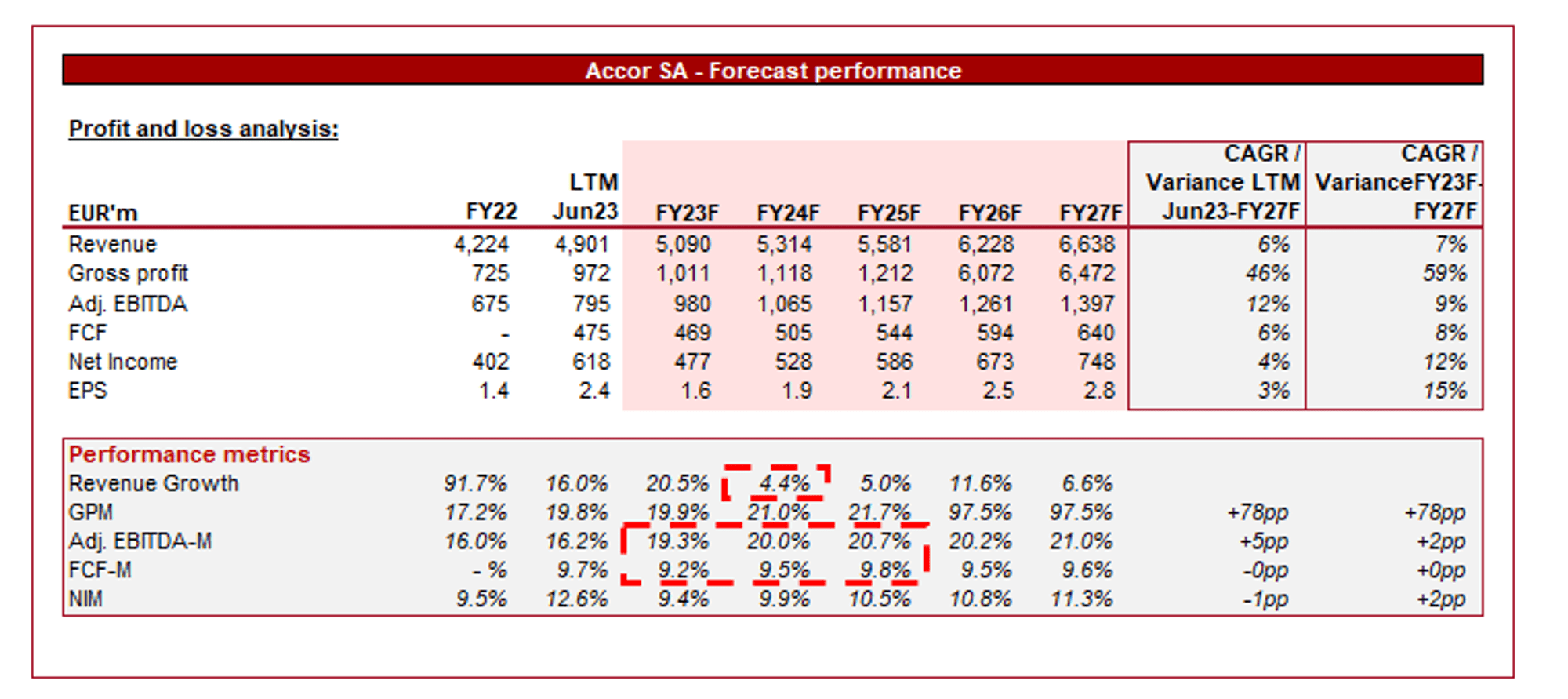

Presented above is Wall Street's consensus view on the coming years.

Analysts are forecasting healthy growth in the coming years, with a CAGR of +6% into FY27F. In conjunction with this, margins are expected to step up to ~20% and normalize at this level, which is slightly higher than its pre-pandemic level. We concur with these estimates.

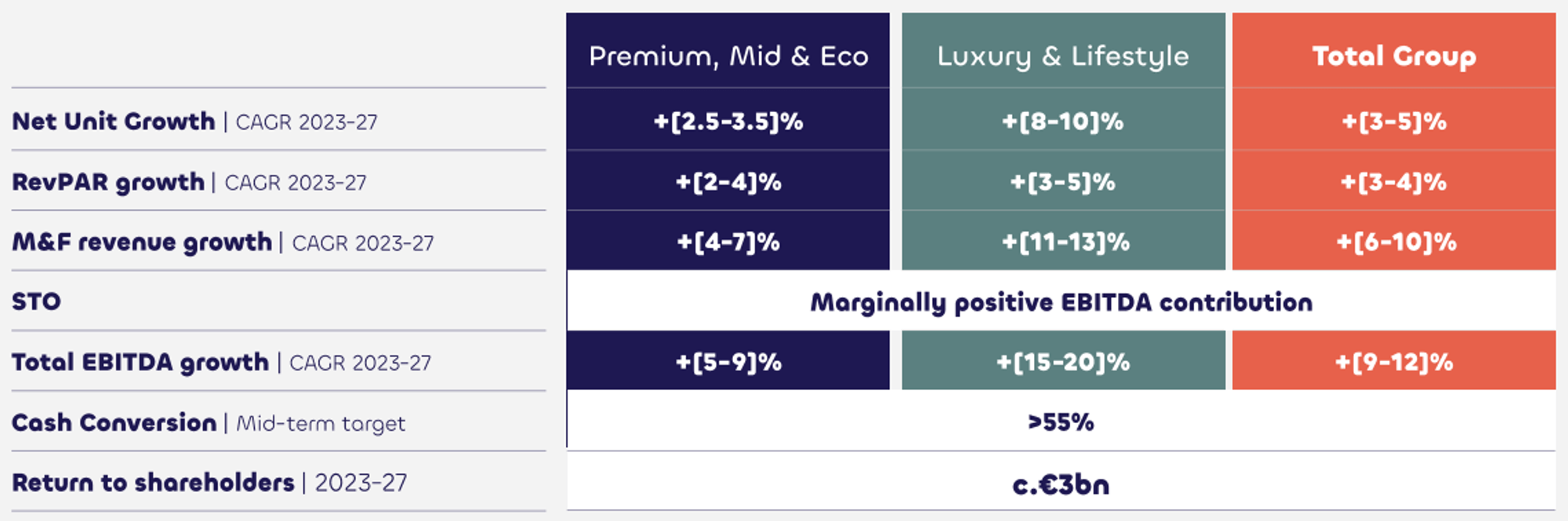

These assumptions align with Management's target guidance, with L&L driving the business' outperformance to historical levels. This does mean execution risk associated with market share capture.

{kind=link}

Into FY27F, analyst forecasts have been slightly altered relative to when we last analyzed Accor. Growth is expected to be slightly higher while margins are slightly lower.

Industry analysis

{kind=link}

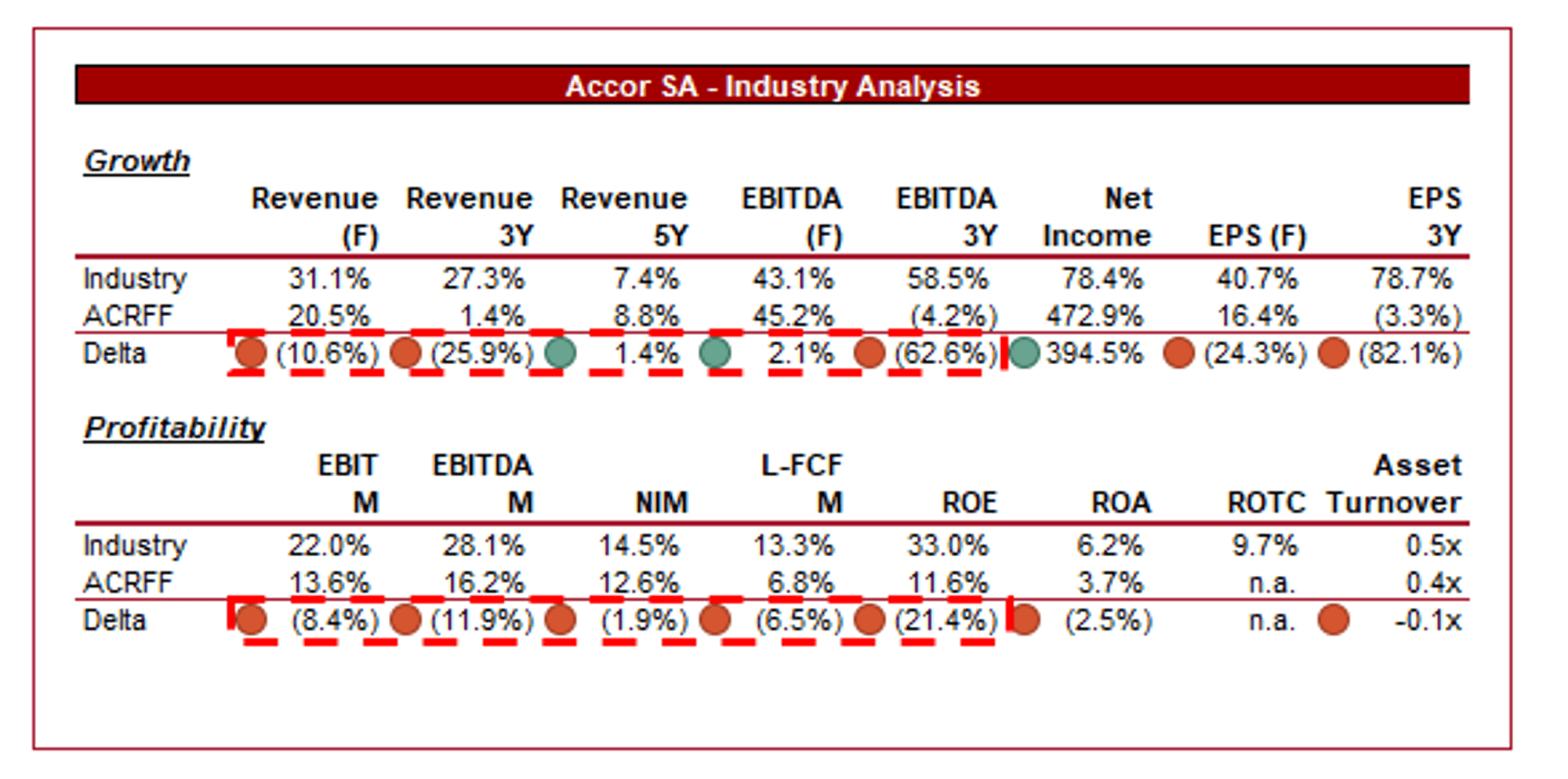

Presented above is a comparison of Accor's growth and profitability to the average of its industry, as defined by Seeking Alpha (30 companies).

Accor is noticeably underperforming its peers, with lower growth and margins, illustrating the reason for its share price weakness.

The depth of weakness, particularly on a margin basis, is a highly disappointing development. This is a reflection of poor execution as part of the company's refranchising efforts, with its peers achieving a far higher margin delta. Hilton's EBITDA-M increased from 26% in FY13 to 58% in LTM23 (+32ppts), Hyatt from 23% to 25% (3ppts - but was already well progressed in franchising), Marriott from 46.5% to 72.3% (+25.8ppts), and Wyndham from 33.4% to 41.2% (+7.8ppts). Accor on the other hand has gained nothing since FY13 and assuming it hits its FY24F target, would only gain ~4ppts.

This delta translates to a lower FCF margin and ROE, limiting long-term future shareholder returns. It's likely that even with its strategic shift, Accor will at best match its peers in YoY growth while remaining fundamentally behind on margins.

Valuation

{kind=link}

Accor is currently trading at 14x LTM EBITDA and 11x NTM EBITDA. This is broadly in line with its historical average.

Parity with its historical average is reasonable in our view, although we do suggest a small premium is justifiable. While the company faces issues with near-term economic conditions and execution risk with margin improvement, we see an upside with its expansion further in Luxury and the scope to increase margins and distributions. This implies a limited share price upside.

Further, Accor is trading at a sizeable discount to its peers, ~30% on an LTM EBITDA basis and ~18% on a NTM P/E basis. This implies an FCF yield discount of ~1ppt. A discount is warranted due to its weaker financial performance, which will limit relative shareholder returns. Yet again, however, we do believe it is slightly undervalued given the cash yield, although with rates where they are, a ~5% yield is not as impressive anymore.

Key risks with our thesis

The key risk to our thesis, for both upside and downside, is how economic conditions develop in the coming year. This will materially impact growth and the company's trajectory into the end of the decade.

Looking long-term, there is execution risk associated with the strategic shift toward L&L.

Final thoughts

Accor is a solid business, owing to its asset base, brands, and consumer reach. However, the company has serially underperformed and its current strategic shift is slightly late, even if we do expect it to generate shareholder value.

Its recent performance has been strong and we do expect a soft landing in 2024, from which point healthy growth can be achieved. We struggle to see how Accor can catch up to its peers and thus represents an underperforming investment at a discount, which is never ideal.

The company does appear slightly undervalued but not sufficiently to be attractive in our view, particularly with various risks and underwhelming potential.

For further details see:

Accor: Seeking To Disrupt The Hotel Industry Through Expansion Into Luxury