ANIOY - Acerinox: The 6% Yield Should Be Safe

2023-03-09 11:30:00 ET

Summary

- Acerinox is a large stainless steel producer, with a specialty alloys division.

- The 2022 results indicate an acquisition completed in March 2020 is paying off.

- Acerinox will see its EBITDA decrease this year, but I still expect strong earnings and free cash flows.

- The company shouldn't have any issues covering the current dividend payments.

Introduction

Acerinox ( ANIOY ) isn't operating in one of the easiest sectors these days. While the economic situation is still pretty uncertain, producing stainless steel also requires substantial amounts of natural gas and nickel and it wasn't a surprise to see the company's financial performance deteriorate during the third quarter but I wasn't too worried as I didn't expect the Q4 results to deteriorate. In this article I will have a look at the company's full-year financial results and what this means for the stock.

{kind=link}

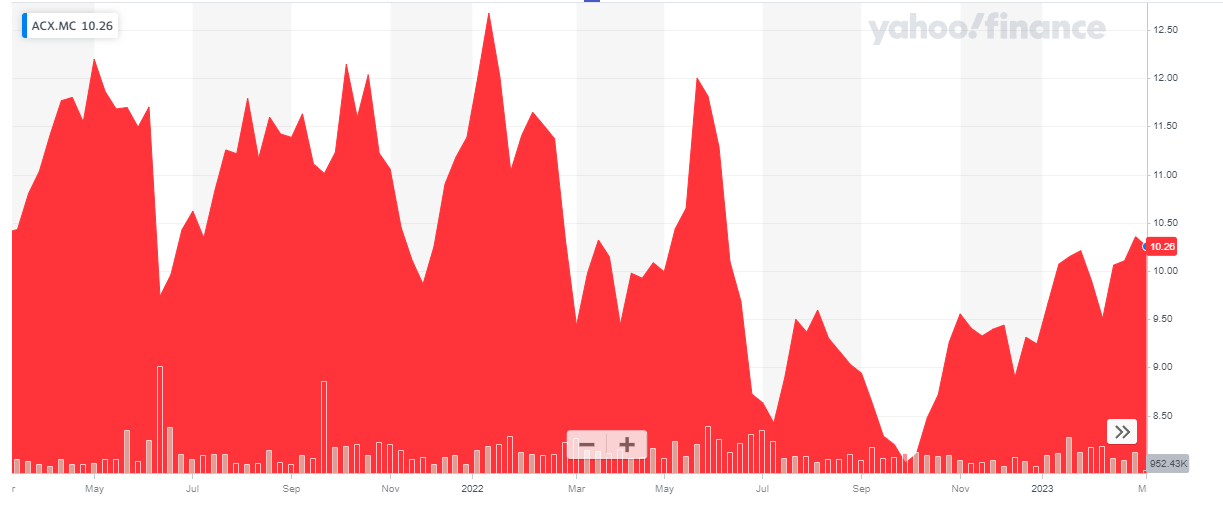

Acerinox has a primary listing on the Madrid Stock Exchange where it's trading with ACX as ticker symbol. The average daily volume of almost 1.2 million shares is clearly superior to the volume on any of the secondary listings so I would strongly recommend using the Madrid Stock Exchange to trade in Acerinox. The current market capitalization is approximately 2.55B EUR as the net share count has decreased to approximately 250M shares (there are just under 260M shares outstanding with just over 10M treasury shares).

A stronger than expected free cash flow result in 2022

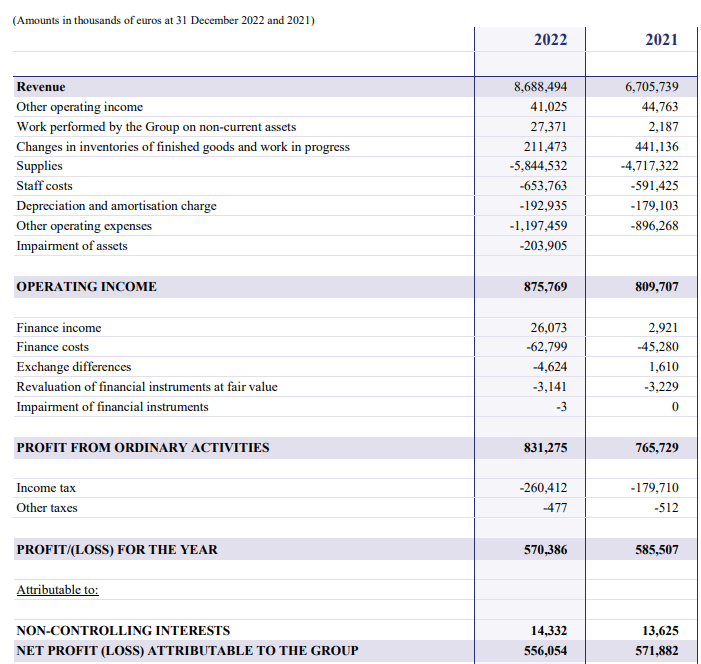

2022 was a good year for Acerinox as the company reported a total revenue of almost 8.7B EUR for the entire financial year. This resulted in an operating income of just over 875M EUR and while this looks disappointing at first sight as it represents an increase of less than 10% versus the 2021 operating income, Acerinox did record an impairment charge of in excess of 200M EUR during 2022 . Excluding that impairment charge, the underlying operating income would have come in at 1.08B EUR, an increase of in excess of 30% versus 2021.

{kind=link}

But despite the impairment charge, Acerinox remained very profitable: the bottom line shows a net income of 570M EUR of which just over 556M EUR is attributable to the Acerinox shareholders. This works out to an EPS of 2.16 EUR per share based on the average share count of approximately 257M shares.

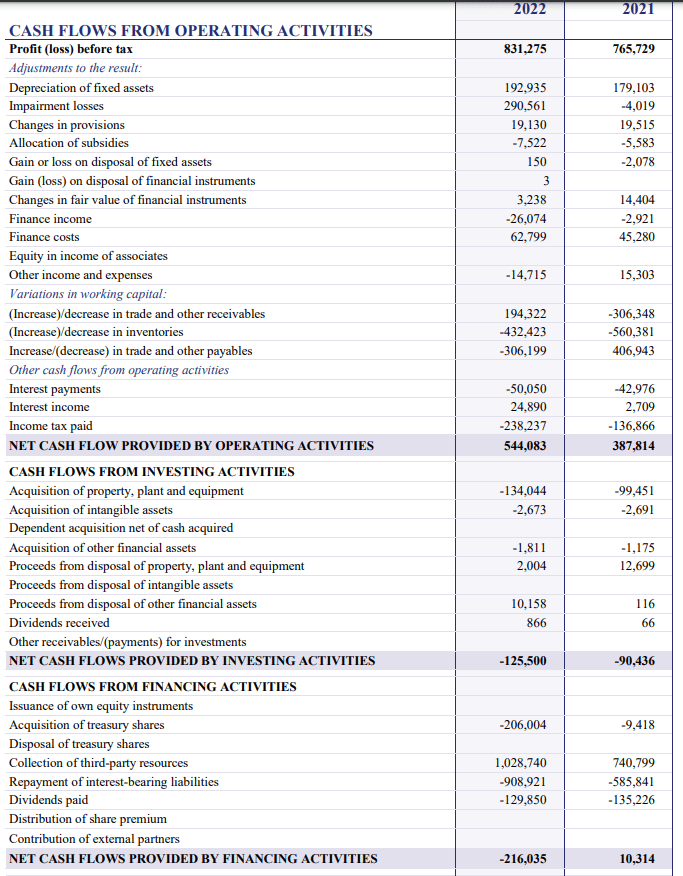

Considering the impairment charge had a rather large impact on the net income result, I prefer to look at Acerinox's cash flow profile. The company posted a net operating cash flow of 544M EUR but this includes just 238M EUR in cash taxes although 260M EUR was owed, based on the income statement, while I'm also deducting the entire 14M EUR in net income attributable to non-controlling interests. But on the other hand, Acerinox did record a net working capital investment of 544M EUR which means the underlying operating cash flow was approximately 1.05B EUR.

{kind=link}

The total capex was just under 137M EUR, resulting in a net free cash flow of in excess of 900M EUR which represents an FCFPS of 3.50 EUR using the weighted average share count.

The second semester was clearly much weaker than the first semester but that's fine as the results still slightly exceeded my expectation. The Q4 EBITDA was lower than I had anticipated but that included a downward revision of inventory values of 98M EUR and excluding that, the 188M EUR in underlying EBITDA actually came in pretty close to the 200M EUR I had anticipated . The inventory revision in Q4 also means the guidance for a 'clearly higher EBITDA' in Q1 is a little bit meaningless considering there likely won't be a (substantial) inventory revision in Q1.

Acerinox will pay a 0.60 EUR dividend in the second quarter, resulting in a dividend yield of almost 6%. That does make the stock pretty attractive, especially when you know Acerinox only needs about 150M EUR per year to cover that dividend. The standard dividend withholding tax rate in Spain is 19%.

The balance sheet is robust and the previous acquisition is now fully integrated

It's always interesting to see how companies handle mergers and acquisitions. Right before the COVID pandemic shut down the world economy, Acerinox had committed to purchasing VDM Metals. Back when the deal was announced, in 2019, the valuation was very attractive: Acerinox was acquiring the company for a total enterprise value of 532M EUR (including 165M EUR in pension liabilities) which represented about 5.5 times the EBITDA before synergy benefits.

Those synergy benefits were initially estimated at 14M EUR and subsequently increased to 17M EUR but apparently Acerinox handsomely exceeded this target and was able to squeeze out about 25M EUR in synergy benefits in 2022 . And thanks to the higher interest rates the retirement liabilities are likely decreasing fast as well (this item is no longer discussed in greater detail in the financial results). The VDM Metals division (now called 'alloys') generated an EBITDA of 125M EUR in FY 2022 which is more than twice the 2021 EBITDA. And based on the original purchase price of 532M EUR, this acquisition is now paying off very well despite closing the deal in March 2020 when the world economy came to a standstill.

This gives me confidence in Acerinox's ability to pursue M&A deals. I'm open to any sort of bolt-on acquisitions and/or diversification ideas the company might have and despite the temporary headwinds, the Acerinox balance sheet can now certainly handle another decent-sized acquisition.

As of the end of December, the company had 1.55B EUR in cash on its balance sheet while the short-term debt was approximately 593M EUR with an additional 1.4B EUR in long-term debt. This means the total net debt is just around 440M EUR. That's the lowest level in 20 years despite completing the VDM acquisition and surviving a touch 2020 and H1 2021 before the situation got better. The total EBITDA came in at just under 1.3B EUR, and although it will be difficult to replicate that in 2023, it's clear the balance sheet could handle another sizable acquisition.

Investment thesis

2022 was the best year in the company's history but we definitely shouldn't base any investment decisions on that excellent result. I expect this year's EBITDA to fall back to around 700M EUR, but that still makes Acerinox pretty attractively priced at less than 4.5 times the EBITDA (using the current net debt into account). And using the same 700M EUR EBITDA number, I expect the EBIT to be around 500M EUR, and a net income of approximately 350M EUR (this will depend on whether or not Acerinox will be able to make some money on its 1.55B EUR cash pile now interest rates are increasing). That's about 1.40 EUR per share which means the stock is trading at about 7.5 times earnings, even taking a 40% EBITDA drop into account for this year.

This doesn't mean Acerinox is a 'must buy'. But I am confident the strong balance sheet will help the company to navigate through these more challenging times. Visibility for 2023 is still limited and additional volatility should be expected, but the dividend should be safe.

For further details see:

Acerinox: The 6% Yield Should Be Safe