ACRS - Aclaris Therapeutics: Potential Speculative Play After Zunsemetinib Misses Mark On Hidradenitis Suppurativa

2023-03-09 07:30:00 ET

Summary

- Aclaris Therapeutics reported disappointing marks for zunsemetinib’s “ATI-450” Phase IIa trial for moderate to severe hidradenitis suppurativa. The share price has been nearly chopped in half.

- The trial missed the primary and secondary efficacy endpoints. Aclaris mentioned that the placebo arm outperformed the efficacy observed in other studies.

- Zunsemetinib is the company's flagship asset that has the prospects to hit blockbuster status in rheumatoid arthritis and psoriatic arthritis markets.

- I believe the market took the selling too far and is discounting zunsemetinib’s potential to show some promise in rheumatoid arthritis and psoriatic arthritis. This could be a great opportunistic trade that could be turned into an investment.

- This would be a very speculative trade/investment. Therefore, I am giving ACRS stock a conviction level of 1 out of 5 in my Compounding Healthcare "Bio Boom" Portfolio.

Aclaris Therapeutics ( ACRS ) recently reported disappointing results for zunsemetinib’s “ATI-450” Phase IIa trial for moderate to severe hidradenitis suppurativa. The trial failed to hit primary and secondary efficacy endpoints. The company did point out that the placebo arm outperformed the efficacy seen in other studies, so that had a negative impact on the stats needed to support zunsemetinib. Still, the market saw the headline and slammed ACRS down from around $12 per share to roughly $5 per share. This level of reaction is common in pre-commercial biotech or pharma tickers that experience failure in the clinic. However, for Aclaris, this failure is very significant due to zunsemetinib being their flagship pipeline asset that has the prospects to be a blockbuster drug in rheumatoid arthritis and psoriatic arthritis markets. Investors are probably looking at zunsemetinib’s data in hidradenitis suppurativa, and are doubting that the oral MK2 inhibitor will perform well in rheumatoid arthritis and psoriatic arthritis readouts later this year.

Indeed, zunsemetinib’s data is hidradenitis suppurativa is concerning, and the market’s reaction is justified. On the other hand, the market took selling beyond the value of the hidradenitis suppurativa indication and has arguably already priced in a potential failure in Rheumatoid arthritis and psoriatic arthritis. I believe this could be a great opportunity to establish a speculative position ahead of the rheumatoid arthritis and psoriatic arthritis data in the second half of this year. If zunsemetinib does perform well in just one of those arthritis trials, it is conceivable Aclaris still has a potential blockbuster drug. Thus, potentially returning ACRS to its former glory and allowing me to book a quick profit, and hold the remainder for a would-be long-term investment.

I intend to provide a brief background on Aclaris Therapeutics and will discuss the implications of zunsemetinib’s data is hidradenitis suppurativa. In addition, I will debate over possibly taking advantage of the current sell-off by starting a speculative position ahead of the expected second-half readouts. Then, I will point out some of the downside risks of this play and will provide a conviction rating for ACRS. Finally, I reveal my strategy for managing this type of trade, and how I plan on maximizing the opportunity.

Background on Aclaris Therapeutics

Aclaris Therapeutics is a clinical-stage biopharma that is developing small-molecule drugs to treat immuno-inflammatory diseases. The company has a valuable R&D engine labeled the “KINect technology platform,” which they employ to discover new drug candidates that attempt to regulate the body’s protein kinase system, or “kinome”. The company has been working on small molecule kinase inhibitors that have ATP site cysteines, which distinguishes Aclaris from other kinase inhibitors.

{kind=link}

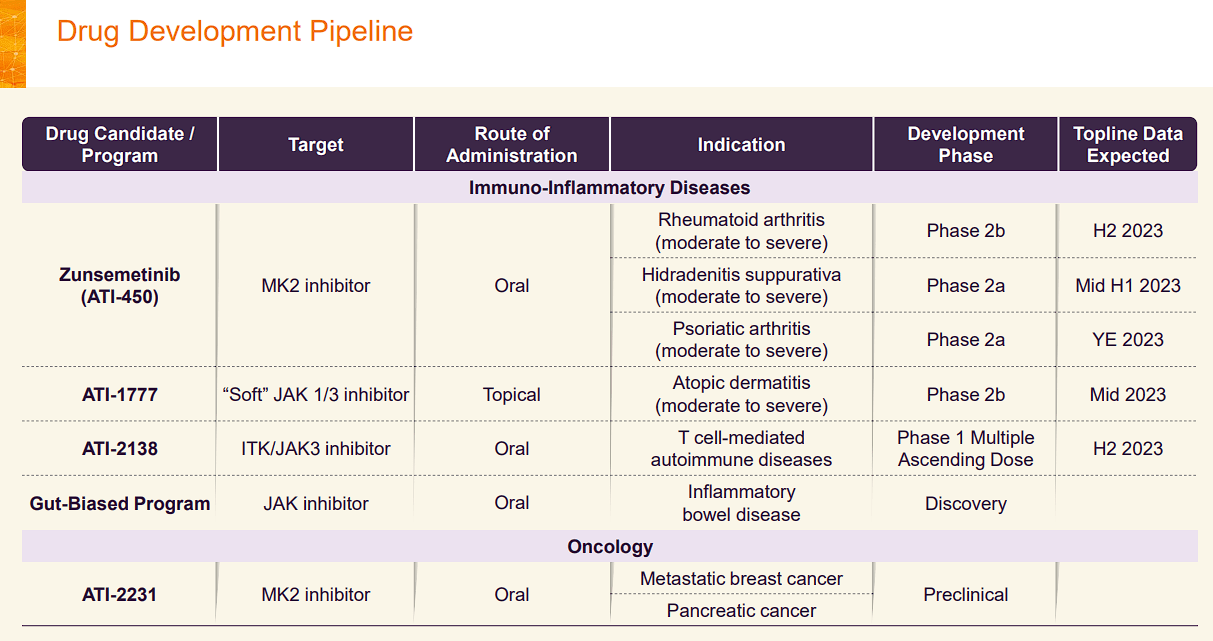

The company’s flagship candidate, zunsemetinib “ATI-450”, is an oral small molecule MK2 inhibitor that has been targeted at immuno-inflammatory diseases such as rheumatoid arthritis, psoriatic arthritis, and hidradenitis suppurativa.

ATI-450-RA-202 is the rheumatoid arthritis program, which is in a Phase IIb dose-ranging trial. Moderate to severe rheumatoid arthritis patients are at 20 mg or 50 mg twice daily of zunsemetinib in combination with methotrexate. This trial is ongoing and the company anticipates topline data in the second half of this year.

The psoriatic arthritis program (ATI-450-PsA-201) is in a Phase IIa trial assessing the safety efficacy, and tolerability of 50 mg twice daily of zunsemetinib for moderate to severe psoriatic arthritis. Aclaris believes they will have topline data including PK and PD numbers from the ATI-450-PsA-201 program by the year-end of 2023.

Aclaris also matched zunsemetinib against hidradenitis suppurativa (ATI-450-HS-201) in a Phase IIa trial where patients took 50 mg twice daily over 12 weeks. Unfortunately, the recent topline data readout revealed that zunsemetinib failed to hit primary and secondary endpoints.

Aclaris also has ATI-1777, a topical “soft” Janus kinase “JAK” 1/3 inhibitor prospect for moderate to severe atopic dermatitis. The ATI-1777-AD-202 program is in a Phase IIb trial that is projected to produce topline data around the middle of this.

ATI-2138 is the company’s oral covalent ITK/JAK3 inhibitor being developed for T cell-mediated autoimmune diseases, and the company is taking aim at ulcerative colitis as the initial target. ATI-2138 is in a Phase I multiple ascending dose trial in healthy volunteers, with a goal of having topline data in the second half of this year. It is important to note that the company has publicized that they are working on supplementary indications for ATI-2138.

In terms of preclinical programs, Aclaris has ATI-2231, which is a long plasma half-life oral MK2 inhibitor for pancreatic cancer and metastatic breast cancer including preventing bone loss in metastatic breast cancer patients. Aclaris anticipates starting clinical development in 2023 with a “ collaboration with an academic third party.”

In addition to the company’s pipeline, Aclaris has their drug discovery and CRO subsidiary, Confluence Discovery Technologies that offers a broad range of services for biotech and pharma customers.

Aclaris' Recent Financial Performance

For 2022, Aclaris reported an $86.9M net loss down from $90.9M in 2021. The company’s 2022 total revenue came in from $29.8M, up from $6.8M in 2021. This revenue growth came from a $24.3M surge in licensing, which comprised $17.6M from the non-exclusive patent license agreement with Eli Lilly ( LLY ) and a $5M upfront payment from the Pediatrix Therapeutics license agreement.

Looking at expenses, Aclaris reported $77.8M in R&D expenses for 2022, up from $43.8M in 2022. This $34.0M spike in expenses was primarily the result of higher zunsemetinib development expenses, as well as the development of ATI-1777, ATI-2138, and ATI-2231. G&A expenses came in at $25.1M up from $23.6M in 2022.

In terms of cash, Aclaris finished 2022 with $229.8M in cash, cash equivalents, and marketable securities, which they believe “will be sufficient to fund its operations through the end of 2025.”

Zunsemetinib ’s Hidradenitis Suppurativa Data

Hidradenitis suppurativa causes inflammations/bumps to form under the skin. Although they are typically small, they tend to form in the armpits and groin, which can make them excruciating. This indication is ridiculously underserved for the time being and was going to be an interesting opportunity for Aclaris to demonstrate zunsemetinib’s ability to treat inflammatory skin conditions. As I mentioned in the introduction, the trial data indicated that zunsemetinib 50mg did not meet its key objective of reducing inflammatory nodule count from baseline compared to placebo at twelve weeks. Furthermore, zunsemetinib did not meet the secondary efficacy endpoints, including the percentage of patients achieving HiSCR-50 (50% reduction in total AN count).

Aclaris did mention the placebo outclassed across all efficacy objectives was higher compared to data from other hidradenitis suppurativa studies. So, it is possible the trial simply was a bad roll of the dice in terms of patients, and not exactly the idea that zunsemetinib failed to be operative against hidradenitis suppurativa. In fact, the company believes there was evidence that zunsemetinib demonstrated its mechanism of action. I will point out, that the safety profile was not exactly benign with a broad array of adverse events and 11 out of 48 zunsemetinib patients leaving due to adverse events, versus 4 placebo patients.

Taking Advantage of the Sell-Off

Clearly, any trial failure can be fatal for a drug’s development and could be a major setback for the company. For Aclaris, zunsemetinib’s failure in hidradenitis suppurativa is a major concern because it damages its thesis as a "pipeline-in-a-product" potential and damages the drug’s prospects against rheumatoid arthritis and psoriatic arthritis. The market did respond to the hidradenitis suppurativa failure news accordingly, and the share price has been essentially cut-in-half.

I am not going to discount the trial failure, but I am not entirely sold that the hidradenitis suppurativa failure is 100% indicative of the drug's performance against rheumatoid arthritis and psoriatic arthritis. Not only is hidradenitis suppurativa’s disease mechanism a bit more complex but the proliferation, persistence, or reduction of nodules can be influenced beyond the inflammation in the dermis. Meanwhile, inflammation from rheumatoid arthritis and psoriatic arthritis are caused by specific cytokines. Indeed, the etiology of both these conditions can be environmental, genetic, stress, trauma, etc., but the result is inflammation. So, zunsemetinib’s mechanism of action should help regulate the inflammatory response, thus, potentially improving the symptoms... regardless of the trigger for the patient.

What Is My Point?

Well, the roughly 50% cut is a bit of an overreaction for trial failure in an indication that has a fraction of the commercial market of rheumatoid arthritis (estimated $70B in 2030) and psoriatic arthritis (estimated $13.7B in 2026). In fact, hidradenitis suppurativa’s market is estimated finally clear $1B in 2029. Again, I will concede the trial failure does not bode well for rheumatoid arthritis and psoriatic arthritis readouts later this year… but, it does not guarantee that zunsemetinib is a complete dud. If there is any indication that zunsemetinib has a shot at either rheumatoid arthritis or psoriatic arthritis, ACRS is going to have a drastic change in outlook. If both data readouts are positive… you are looking at a drug that could be an instant blockbuster. Keep in mind, some of the top-selling drugs for these indications (Cosentyx, Enbrel, and Humira) are injectable biologics. Xeljanz and Otezla are newer oral treatments as well as Olumiant and Rinvoq, but they come with some serious side effects. Keep in mind, some of these drugs are the best-selling drugs in the world… so if zunsemetinib shows any comparison in performance, people are going to quickly jump to it being a possible blockbuster drug and forget about hidradenitis suppurativa trial.

Essentially, I believe ACRS is offering an amazing risk-reward profile here due to its ability to zunsemetinib having two potential opportunities to redeem later this year and possibly reinstate the "pipeline-in-a-product” tag. In addition, the company has several other pipeline and preclinical prospects that should provide a floor and bolster the valuation in the long term. So, while others are focusing on a disappointing result in a small trial in a minuscule indication, I am looking at the ticker’s current valuation verse its immense commercial potential.

At the moment, ACRS is trading around $6-$7 per share with a market cap under $500M. As I mentioned above, if zunsemetinib is approved for either rheumatoid arthritis or psoriatic arthritis, it could hit $1B in sales in a few years of being on the market. Pulling in $1B in annual sales at a $500M valuation would be a forward price-to-sales of 0.5x, which would be absurd considering the industry’s average is around 4x-5x. If this was to occur, ACRS could be valued at $4B-$5B, or $60-$75 per share.

{kind=link}

Admittedly, this is an incredibly pie-in-the-sky number considering the company will most likely have to dilute between now and the end of the decade. However, even if the company increased the number of shares by 3x, you are still looking at $20-$25 per share.

If you ask me, any of those targets sounds great considering the current share price… even if I have to wait a few years for it to hit.

What Could We See In The Near Term?

The Street expects Aclaris to potentially hit $1B in sales towards the end of the decade. Using a 10% discount for time and a 25% discount for risk against the prospective sales of $1B in 2030 and the 4x price-to-sales, I get roughly $17.50 per share. I believe this is a reasonable near-term target if one of the expected data readouts is positive. If both are positive, we could see ACRS retest its April 2021 high of around $30 per share.

Again, these targets might seem to be unmanageable considering where the stock is trading at right now, but some Street analysts believe zunsemetinib’s peak sales opportunity is $5B . If that is true, my $60-$75 targets would be considered laughably low.

Downside Risks

Indeed, ACRS still has considerable upside potential at these prices. However, the ticker is still incredibly speculative at this point. Obviously, there is the risk of regulatory failure and the company having to scrap zunsemetinib. Even if zunsemetinib was able to demonstrate it is effective in rheumatoid arthritis and psoriatic arthritis, there is still a concern over elevated CPK levels, which could be a deal-breaker for regulators. Another concern is Bristol-Myers Squibb’s ( BMY ) oral mk2 inhibitor CC-96677 , which is not far behind zunsemetinib in development. Obviously, Bristol-Myers Squibb has the knowledge, resources, and pedigree to rapidly develop and get their candidate to the market. So, it is possible that Aclaris could be outclassed by the competition at all levels leading to lackluster results.

It is possible these risks will be present for a prolonged period of time, thus, preventing ACRS from trading at a premium valuation for the foreseeable future. As a result, I am giving ACRS a conviction rating of 1 out of 5.

My Strategy For ACRS

My plan for ACRS is very simple… wait for an attractive valuation and book profits early and often in order to move the position to a “house money” status. Using the Street’s revenue 2028 estimate of $450M along with a discount for time and one error, I get a value of $6 per share, which I will use as my “Buy Threshold,” which is basically the highest price I'll pay for ACRS at this moment. For my Sell Targets, I am looking at several sell targets above $12 per share. Taking profits at these levels will allow me to quickly de-risk my position by moving it to “house money” status to remain as a long-term investment.

On the other hand, if the upcoming data reveals that zunsemetinib is a dud, I will attempt to play the volatility by averaging down and scalping my way to a neutral position.

If all goes well in either rheumatoid arthritis or psoriatic arthritis, I will put ACRS in my Compounding Healthcare "Bio Boom" speculative portfolio for at least five years in anticipation that the Aclaris will get zunsemetinib across the finish line, and the company will be acquired at a premium valuation.

For further details see:

Aclaris Therapeutics: Potential Speculative Play After Zunsemetinib Misses Mark On Hidradenitis Suppurativa