ACU - Acme United: Fairly Valued No Buy Signal Yet

Summary

- Predictable growth makes for simple valuation of Acme United Corporation.

- The unpredictable macroeconomic environment and supply chain issues suppress optimism in revenue growth.

- Acme United Corporation financials are nothing to write home about but are not bad either, and a DCF analysis tells us that the company is valued fairly at the current level.

Investment Thesis

With solid and predictable growth numbers over the years and life returning to normal after the pandemic, I decided to look into Acme United Corporation (ACU) to see if the company might experience better sales now that people are returning to the office and back to schools. With Acme's earnings coming up in the next couple of weeks, I decided to look through the company's financials, get a sense of how the company has performed and how it will perform in the future, and come up with reasonable and somewhat conservative growth assumptions for the next 10 years for my discounted cash flow ("DCF") model. With the things that I discovered, the company right now appears fairly priced, and I would like it to reduce its debt quite considerably before investing., I will give Acme United Corporation a Hold rating for now.

Many may not even be aware of this company. I was looking through some office supplies and stumble upon some products with Westcott's name all over them. I thought of Peter Lynch and his words in the book "One Up On Wall Street" that he found some of his best investments just by looking around everyday life and seeing if a product was from a publicly traded company (I am paraphrasing, of course, as I haven't read that book in a while).

So, I decided to do just that. I went home and started researching Westcott and found out that the owner of the company is Acme United Corporation and found that this company is everywhere. Some of the products they make include scissors, shears, utility knives, first aid kits, and sharpeners, among others. They sell their products to a variety of markets, including office supply, school supply, hardware, and industrial markets, among others.

Armed with this brief knowledge of what Acme United Corporation does, I decided to look into the growth and its financials. Let's get to it.

Revenue Potential

We are still living in the pandemic era. It is still lingering, however, we have learned to live with it and not be shackled by the fear and anxiety of getting it. This is where I believe Acme United Corporation can benefit in the next couple of years a lot more, as most of the companies, schools, and facilities go back to normal. Maybe not fully normal, as a lot of these places have adopted the hybrid work environment, which is certainly much better for Acme than the WFH environment that we saw over a year ago.

When thinking about the next 10 years of Acme United Corporation growth prospects, I looked at the last 10 years of revenue growth and came to around 9.5% average growth per year. This was a good anchor point for my estimates, but to take on a more conservative approach and to have a greater margin of safety to my calculations, I went for a little lower sales growth than the historical. As the saying goes, it is better to be safe than sorry, which can be applied to many aspects of life, not just investing.

Lower Growth Estimates Justification

The macroeconomic situation around the world played a huge role in taking much lower growth estimates for the future. Inflation, although coming down from the peak of 9%, is still very high. Rising interest rates and currency fluctuations coupled with supply chain issues have lowered my optimism, and so I am taking a more cautionary approach to the future until all the macro issues resolve eventually. The European market, although not the biggest, still generates quite a bit of revenue. It has been impacted by and may continue to be impacted by the Ukrainian crisis, coupled with historically low exchange rates for the euro against the dollar, meaning the revenues against the dollar will be affected quite a bit.

Financials

I like to keep my valuation analysis quite simple, and part of the simplicity is to check how healthy the company is on its books. Sometimes, the balance sheet is so good, it may justify an investment right there and then. However, you can always overpay and receive poor returns overall even if the company is very good.

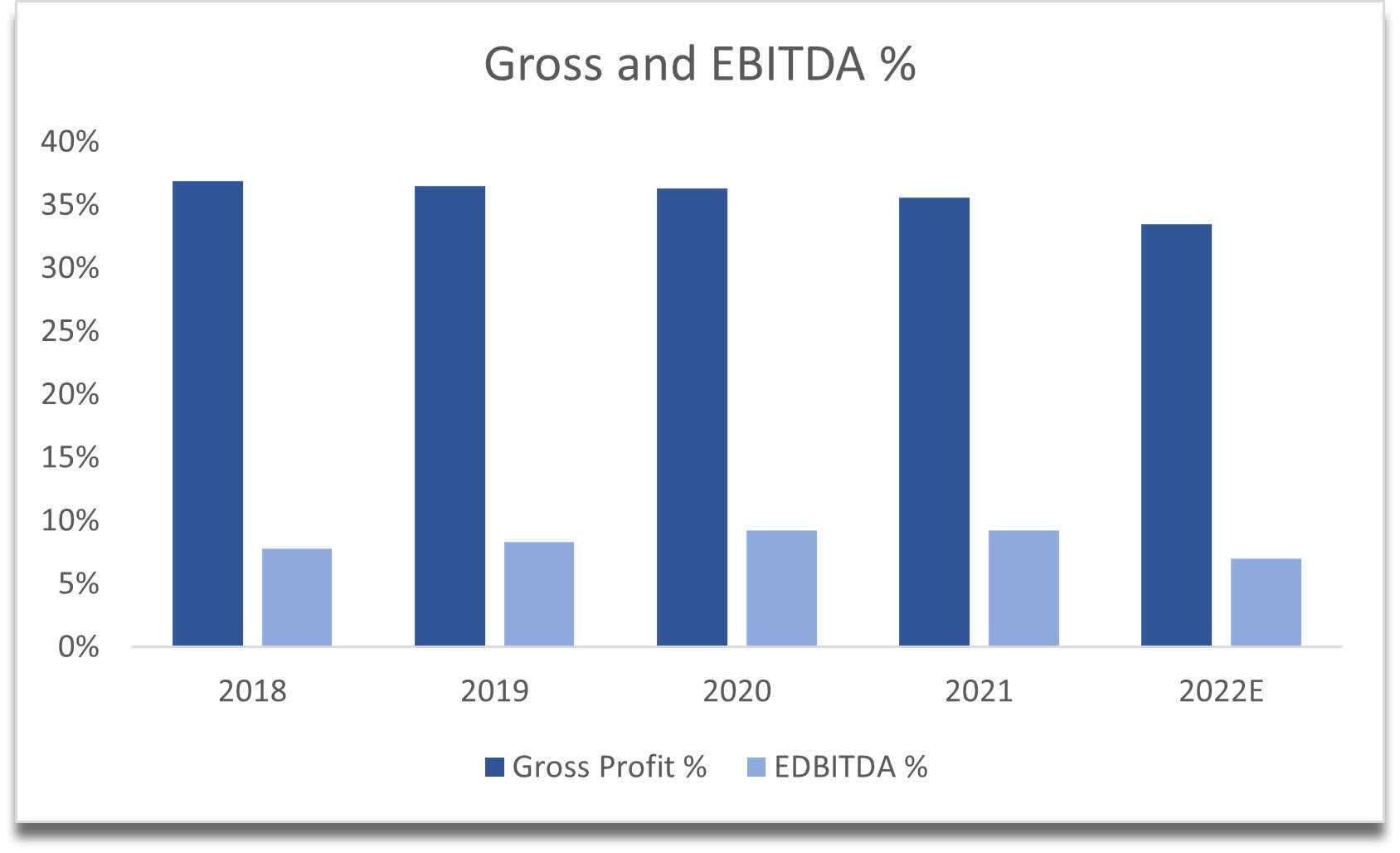

Usually, if I see healthy margins somewhere around 50% on gross and over 10% EBITDA, I would be happy with them. However, if I see that they are lower than my minimum, I'd like to look at how the competitors hold up.

Gross Margins vs comps (Seeking Alpha)

I quickly googled some competitors to Acme United Corporation, and I can see that Acme could do a bit better on the gross margin.

EBITDA margin vs Comps (Seeking Alpha)

Same story on the EBITDA % front. While a higher EBITDA margin is generally preferred, what is considered "good" can vary based on factors such as industry, size, and growth prospects. For a small-cap industrial company like Acme United, an EBITDA margin of 8-9% is not unusual, and it's not necessarily an indicator of poor performance. The above competitors are much bigger in terms of capitalization, so are not perfect competitors, so the differences do not sway my valuation too much.

Gross and EBITDA margins (Own Calculations)

{kind=link}

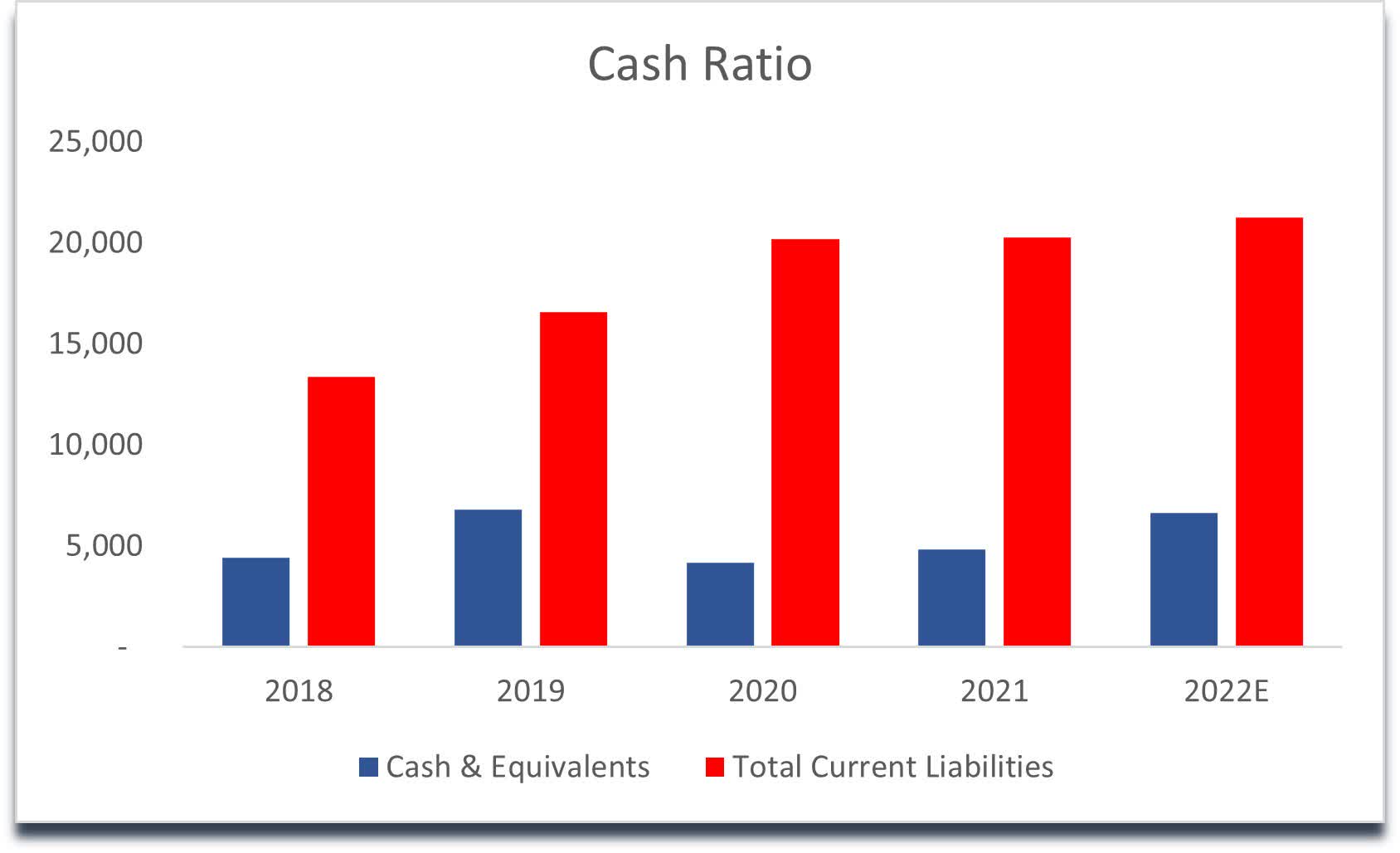

I like companies that can cover their short-term liabilities with cash on hand. Not many are able to, it is quite rare to see, especially from a small-cap company like Acme. The cash ratio gets an X in my view, as it is nowhere near able to cover current liabilities.

Cash on hand vs Current Liabilities (Own Calculations)

{kind=link}

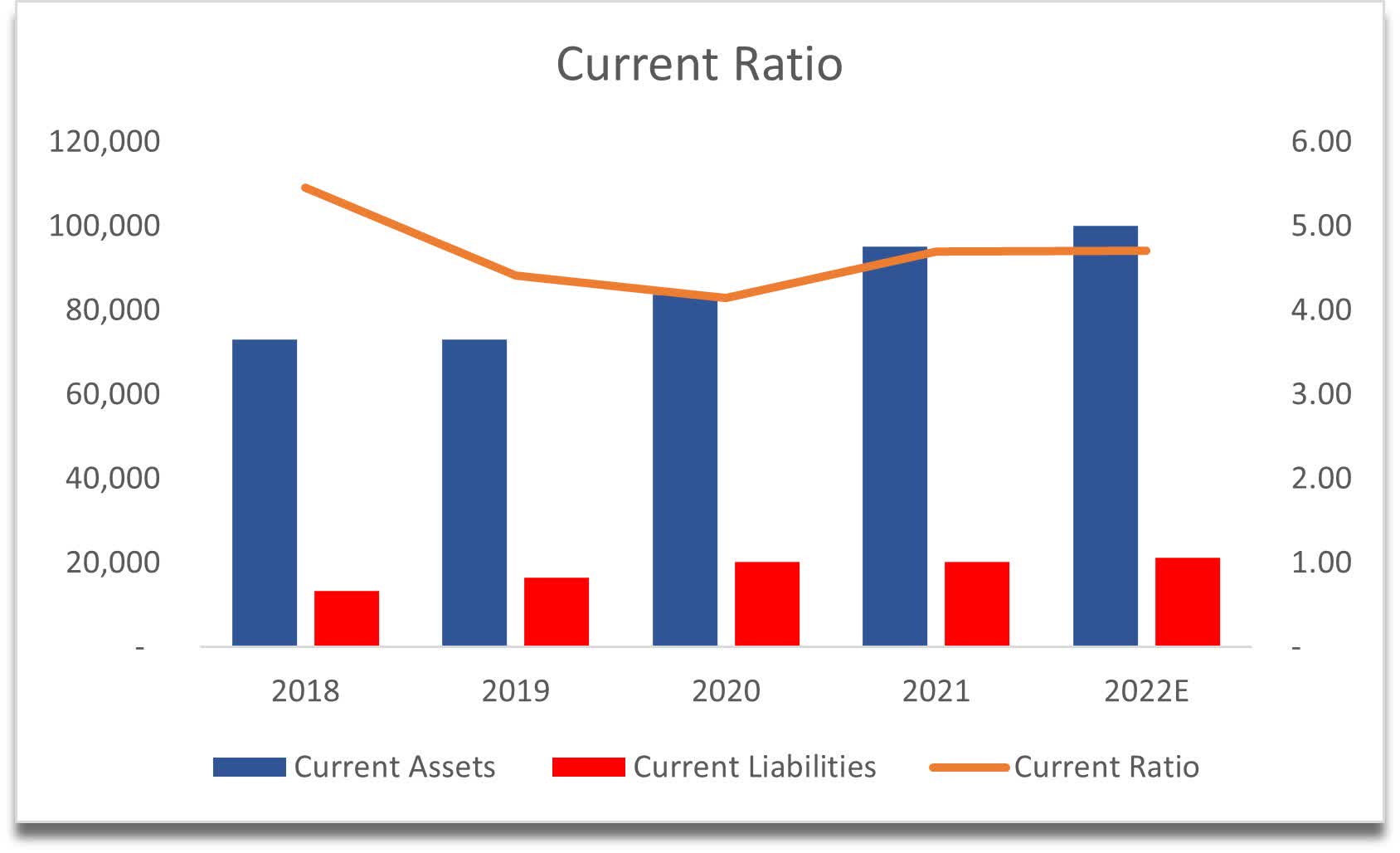

I don't think it is a problem, because of its current ratio. Here the company shines, as current assets easily cover current liabilities and seem to be very stable on that front also.

Current Ratio (Own Calculations)

{kind=link}

I do not like debt on balance sheets . There is such a thing as good debt, and I believe Acme is using the debt in a responsible and very manageable manner here. It is being used to fund growth operations and capital expenditures. The company is repaying its debt steadily, and the low dividend payout ratio helps to put me at ease that they will not default on their debt because of a lack of free cash flow. Also, the company's debt ratio averaged 0.35 over the last 5 years, which is also a good number. 0.5 and below is what I consider to be good.

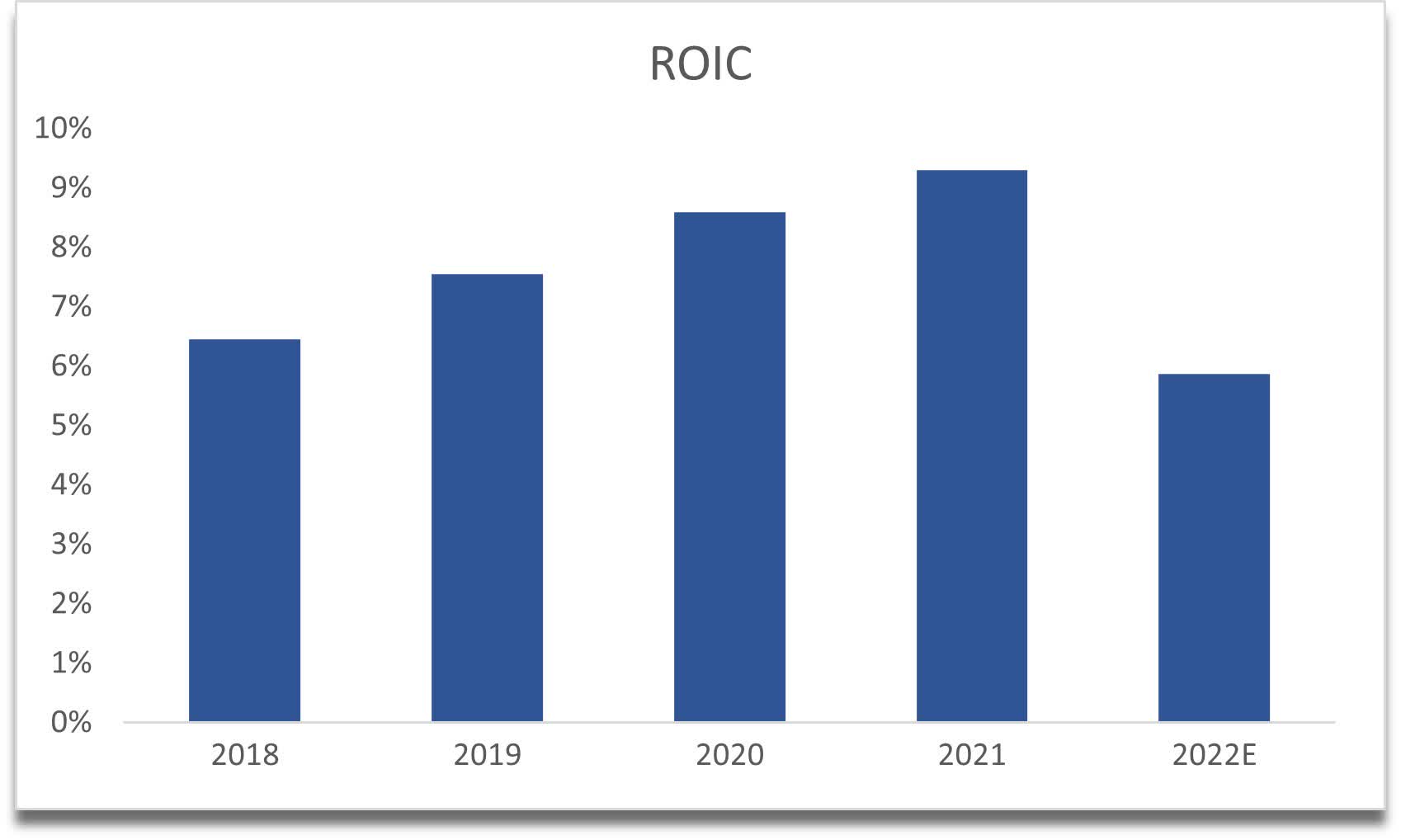

Return on invested capital is, in my opinion, ok. I would prefer something over 10%. I will keep an eye on this metric over the next few quarters and would like to see it trend up.

Return on Invested Capital (Own Calculations)

{kind=link}

The same goes for ROA and ROE. I prefer higher numbers than the company has, but they are about the bare minimum I'd like to see.

ROA and ROE (Own Calculations)

{kind=link}

I'd like to see the upward trend returning on the above metrics in the future, and if they continue to trend downward, I will have to dig in to see why this is happening.

Valuation

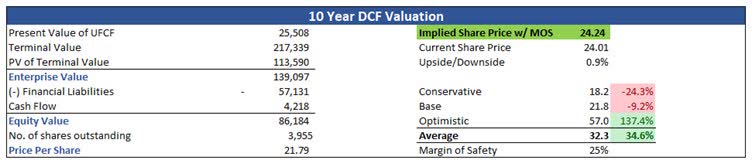

With all of the above taken into account, my job was to come up with some reasonable growth assumptions that will not be too optimistic and not too pessimistic. I like to go for a range in my valuations, and so I set up 3 case scenarios, a conservative case, a base case, and an optimistic case. As I mentioned earlier in the article, historical average revenue growth sits at around 9.5% over the last 10 years. With the macroeconomic environment considered, I have lowered my base case expectations quite a bit and for the next 10 years, I went with a 5.4% average. For more of an optimistic case, I went with a 7.4% average over the next 10 years. These are still lower than the historic ones, but I believe it's justifiable. To finish my price range, the conservative case average growth over 10 years sits at 3.4%.

I also like to put in a good margin of safety to my DCF valuations to be even more certain. In this case, I went with my usual 25% margin of safety.

Now that everything has been inputted into my DCF valuation model, the fair price for the company is $24.24. This indicates that the company is fairly valued according to my calculations.

10-year DCF valuation (Own Calculations)

{kind=link}

Closing Remarks

I am left with two choices here, buy Acme United Corporation or hold off for now until we see improvements in the mentioned metrics and macro economy. I am leaning towards the more conservative choice, which is to keep Acme United Corporation on my watchlist and wait until I see some new developments. The Acme United Corporation FY2022 results will be out shortly, and we will see how much my estimates for the year are different from the actual results. If they are quite different, I will revisit Acme United Corporation in the future and reassess the situation.

For further details see:

Acme United: Fairly Valued, No Buy Signal Yet