AGG - ACP: Solid Foreign Exposure And A Fully-Covered 17% Yield

2023-09-06 07:53:56 ET

Summary

- The abrdn Income Credit Strategies Fund offers a high level of current income with a 17.14% distribution yield.

- The fund's net assets have been declining, but it has not altered its distribution and has released a semi-annual report.

- The fund has been rising in share price over the past three months, indicating improved market perception, but it is no longer trading at a discount on net asset value.

- The fund managed to fully cover its 17%+ distribution in the first half of the year, but it is uncertain whether it can sustain it.

- The fund is currently trading at a much higher valuation than normal, so it might be best to wait for the price to decline.

The abrdn Income Credit Strategies Fund ( ACP ) is a closed-end fund that investors can use to achieve a very high level of current income. The fund's 17.14% distribution yield is evidence of its potential to provide a high level of income. Unfortunately, any time that an asset achieves such a high distribution yield, it is a sign by the market that the distribution is not safe and may have to be cut. In my last article on this fund, I reached the same conclusion as the fund's net assets have been declining for two years now. However, a few months have passed since that time and the fund has not altered its distribution. More importantly, the fund has released its semi-annual report so we will want to see if the strong market that we experienced in the first half of the year allowed it to reverse its declining net asset value problem.

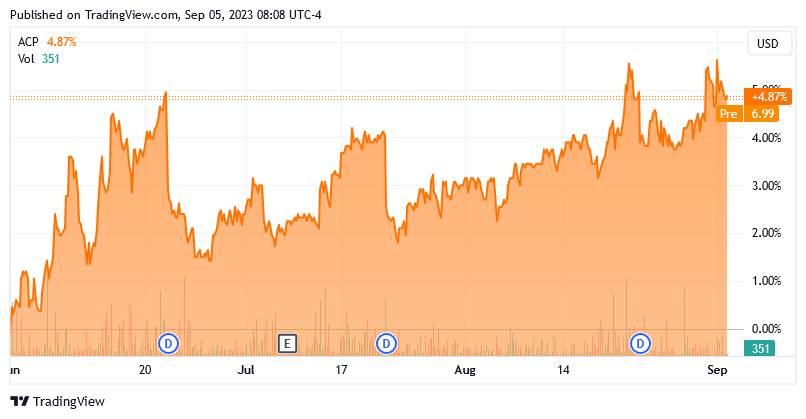

The share price performance does look rather promising, as the abrdn Income Credit Strategies Fund has been rising over the past three months:

{kind=link}

This is a positive sign, as it indicates that the market believes that the fund is in a somewhat better position than it was back in June when we last discussed it. Unfortunately, the fund's shares may have gotten a bit ahead of themselves as they are no longer trading at a discount on the net asset value.

Clearly, a lot has changed here in just a short period of time, so let us revisit this fund and see if purchasing it today makes sense.

About The Fund

According to the fund's webpage , the abrdn Income Credit Strategies Fund has the objective of providing its investors with a very high level of current income. This objective makes a lot of sense considering that the fund's name implies that it will be attempting to achieve its objectives by investing in various debt securities. Indeed, the fund's own website states that this is the general strategy:

The fund seeks to achieve its investment objectives by opportunistically investing primarily in debt and loan instruments of issues that operate in a variety of industries and geographic regions. The fund may invest, without limitation, in credit obligations that are rated below investment grade by a NRSRO such as S&P or Moody's or unrated credit obligations that are deemed by the Advisors to be of comparable quality.

As of the time of writing, 90.78% of the fund's portfolio is invested in bonds. The fund also has a much higher level of cash than we usually expect from a closed-end fund:

CEF Connect

It is curious why the fund would be holding such a high level of cash. One of the characteristics of closed-end funds is that they do not have to continuously redeem shares so they can technically be fully invested. There are two possibilities that I can think of:

- The fund is opting not to reinvest the coupon payments that it receives from the bonds in its portfolio and is instead holding them as cash to use to pay the shareholder distribution.

- The fund's managers think that bonds are overpriced right now and is having difficulty finding securities trading at a reasonable price that can be purchased.

Of the two, I suspect that the second one is more likely to be the case. In fact, Bill Gross would likely agree with this sentiment. As I discussed in a recent blog post , Bill Gross stated that the ten-year Treasury should be at 4.50% but it is only at 4.234% as of the time of writing. This implies that the ten-year Treasury is substantially overvalued. As most other things in the bond market trade at a spread to the ten-year Treasury, this implies that most bonds are substantially overvalued right now. As such, it actually makes sense for the fund to keep money in cash rather than purchase overpriced bonds. The fact that money markets are actually paying better yields than Treasuries right now is just a bonus, as it ensures that the fund is not sacrificing near-term returns to hold cash instead of bonds.

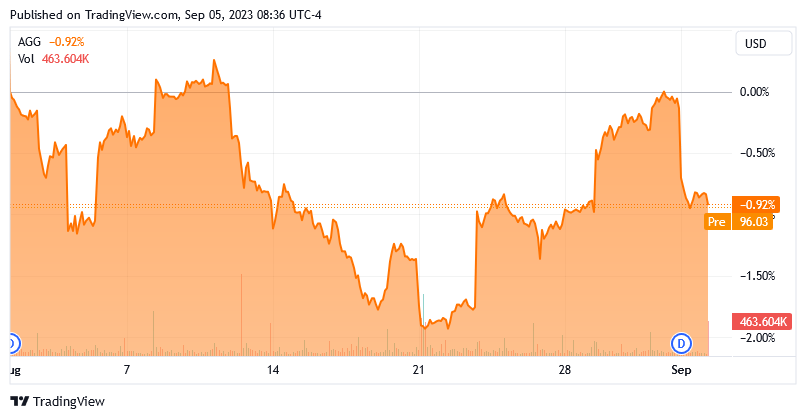

Over much of the past month, the bond market has been weakening. As we can see here, the Bloomberg U.S. Aggregate Bond Index ( AGG ) is down 0.92% over the past month:

{kind=link}

This is due to the market's fading optimism about near-term rate cuts. As I mentioned in numerous previous articles, for most of the first half of 2023, investors were expecting that the Federal Reserve would cut rates sometime either late this year or early next year and then roll into a period of monetary loosening. That seems less and less likely to be a realistic possibility. The progress made on inflation has seemingly reversed as the consumer price index ticked up in the most recent report. Chairman Powell threw further cold water on the market's remaining optimism in his recent Jackson Hole speech. As such, the expectations are now that high rates will be with us for a while and the market is no longer willing to trade bonds as though rate cuts are coming. With that said though, there are still some well-financed institutions that seem to believe that rate cuts will be coming, as indicated by the ten-year Treasury still being higher than it probably should be.

As I mentioned in my previous article on the abrdn Income Credit Strategies Fund, this closed-end fund does not only invest in the American bond market. Indeed, the fact sheet states that only 51.0% of the fund's assets are invested in bonds from American issuers:

Fund Fact Sheet

This is actually a bit less than the 53.1% allocation that the fund had the last time that we discussed it. That could be a sign that the fund's management believes that foreign countries have more attractive bond markets right now. There might be some reason to believe that, as the European economy appears to be struggling more than the American one right now, so it is possible that the European Central Bank will cut rates before the Federal Reserve does. A rate cut would, of course, be positive for the price of bonds denominated in Euros. However, at the moment, officials at the European Central Bank are making hawkish statements in their communications with outside parties so the policy of that central bank is just as uncertain as the Federal Reserve's policy.

At this point, there may be some readers who note that the fact sheet states that the fund has a negative cash position, but CEF Connect's asset allocation shown earlier stated that the fund had a 7.06% cash allocation. The difference can be explained by the fact that the fund is keeping assets in cash equivalents, not cash in a checking account. The fact sheet does not consider cash in money market-type securities as being cash, but CEF Connect classifies such holdings as cash. In short, some of the bonds held by the fund are cash-equivalent securities.

Perhaps the most interesting thing about this fund is that it has more exposure to euro-denominated securities than U.S. dollar-denominated ones:

Fund Fact Sheet

This is highly unusual for a bond fund, but it could offer some international diversification to American investors. As I mentioned in a previous article , one of the biggest problems that American investors have with their portfolio is a lack of foreign exposure. This is especially true with foreign currency exposure, as even the foreign stocks that they may hold are American Depositary Receipts. As such, any problem with the U.S. dollar could have a negative impact. The only real way to protect yourself against such an event is to ensure that you have exposure to several different currencies in your portfolio. This fund appears to be doing that so it could help investors accomplish some currency diversification that may prove useful, especially if China and Russia succeed in their attempts to reduce the dominance of the U.S. dollar as the reserve currency.

Leverage

The abrdn Income Credit Strategies Fund is able to employ certain strategies that allow it to boost its effective portfolio yield beyond that of any of the underlying assets. I explained how this works in my last article on the fund:

Basically, the fund borrows money and then uses that borrowed money to purchase high-yielding bonds and other assets. As long as the interest rate that the fund has to pay on the borrowed money is lower than the yield of the purchased securities, it works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund does not employ too much leverage since that would expose us to an excessive level of risk. I normally like a fund's leverage to remain under a third as a percentage of its assets for this reason.

As of the time of writing, the abrdn Income Credit Strategies Fund has levered assets comprising 28.78% of its portfolio. As such, it appears that the fund is satisfying the requirements laid out above. It appears that the balance between the risk and reward here is acceptable.

Distribution Analysis

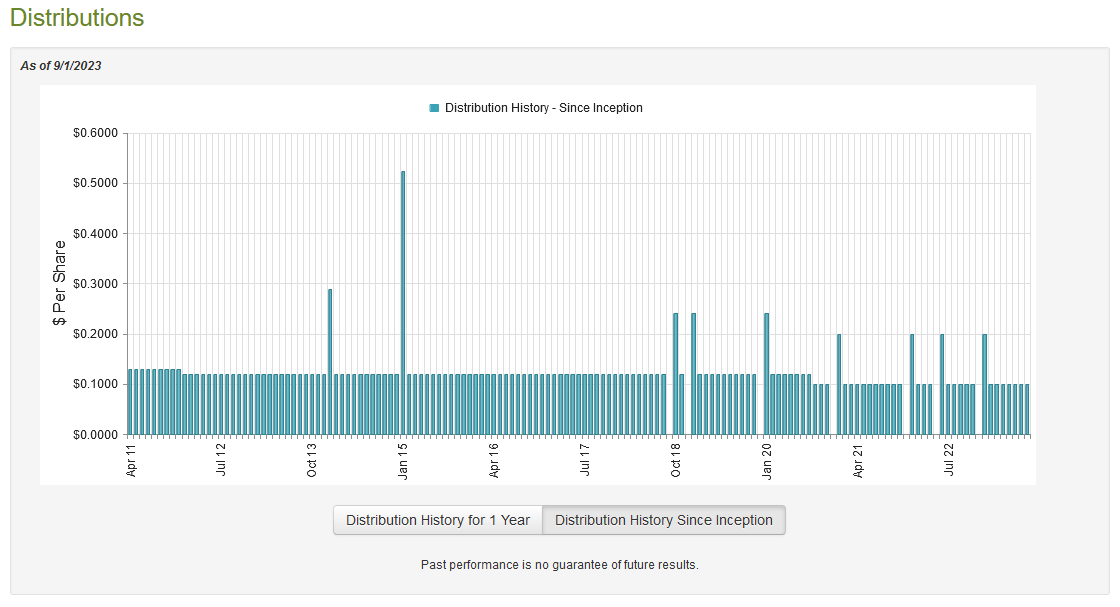

As stated earlier in this article, the primary objective of the abrdn Income Credit Strategies Fund is to provide its investors with a high level of current income. In order to achieve that, the fund invests in a portfolio of income-producing debt securities and then applies a layer of leverage to boost the effective yield of the portfolio. As the securities that the fund purchases have a high yield, we can expect that this process would result in the fund receiving a very high effective yield from its portfolio. It then pays out the majority of its net investment profits to the shareholders. As such, we can expect that this fund will have a very high yield. This is certainly the case as the fund pays a monthly distribution of $0.10 per share ($1.20 per share annually), which gives it a 17.14% yield at the current price. The fund has generally been consistent with respect to its distribution, although it has cut it twice:

{kind=link}

For the most part, this distribution has been far less variable than other fixed-income funds, although the fact that it hasn't been perfectly stable may be a turn-off for some investors. However, the fund has been stable since central banks all over the world started hiking interest rates in the middle of 2022, which is better than many other fixed-income funds have been able to achieve.

As is always the case though, it is important that we ensure that the fund can actually achieve the distribution that it pays out. After all, we do not want to be the victims of a distribution cut that reduces our incomes and almost certainly causes the fund's share price to decline. This may be especially important with respect to this fund today, as the market seems to believe that it will be forced to cut the payout in the near future. This is implied by the very high current yield.

Fortunately, we have a very recent document to consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on April 30, 2023. This is a newer report than we had available to us the last time that we discussed this fund, which is quite nice as it should give us a good idea of how well the fund was able to take advantage of the strong market that existed in most of the early months of this year. It will also give us better information on the fund's ability to sustain its distribution than what we had the last time that we discussed it.

During the six-month period, the abrdn Income Credit Strategies Fund received $57,467 in dividends and $17,875,562 in interest from the assets in its portfolio. This gives the fund a total investment income of $17,933,029 during the period. It paid its expenses out of this amount, which left it with $12,675,681 available for shareholders. Unfortunately, this was not nearly enough to cover the $20,388,000 that the fund actually paid out in distributions during the six-month period. At first glance, this is quite likely to be concerning as we usually like a fixed-income fund to be able to cover its distribution out of net investment income.

However, the fund does have other methods through which it can obtain the money that it needs to cover the distribution. For example, it might have capital gains that can be paid out to the shareholders. Fortunately, the fund had some success during the period. It reported net realized losses of $56,387,886 but this was more than offset by net unrealized gains of $68,391,105 during the period. Overall, the fund's assets increased by $199,674,204 after accounting for all inflows and outflows during the period.

That is obviously a very large increase in net assets considering the other numbers that were mentioned in the above two paragraphs. The majority of the fund's asset increase came from a massive issuance of new shares, which resulted in the fund raising $196,427,470 on the net. However, the fund's assets still increased overall even in the absence of the share issuance. The fund did succeed in covering its distribution during the period, which is a nice change from the disappointing performance in the previous full-year period. The question now is whether or not the fund can continue to generate sufficient investment profits to cover its distributions. That remains to be seen, but the reversal of the bond market over the past month or so is unlikely to help it.

Valuation

As of September 1, 2023 (the most recent date for which data is available as of the time of writing), the abrdn Income Credit Strategies Fund has a net asset value of $6.89 per share. However, the fund's shares currently trade for $7.02 each. That gives the shares a 1.89% premium at the current price. This is a lot more expensive than the 0.29% discount that the fund's shares have had on average over the past month. Thus, it may be a good idea to wait for the price to come down somewhat before purchasing shares, as a better price may become available in the near future.

Conclusion

In conclusion, the abrdn Income Credit Strategies Fund certainly looks a lot better than it did the last time that we discussed it. The fact that the fund managed to cover its distribution during the most recent six-month period is certainly a very nice thing to see, as the fund's very high yield implies a considerable amount of concern on the part of the market. This is one of the few fixed-income funds that has a considerable amount of foreign exposure, which is very nice for American investors who tend to have insufficient exposure to foreign markets. Overall, this fund may be worth considering today, but the current price is rather high and it would probably be best to wait for a decline before buying in.

For further details see:

ACP: Solid Foreign Exposure, And A Fully-Covered 17% Yield