ZYME - Adding Zymeworks To My Value Watchlist (Initial Buy Rating)

2023-09-11 03:06:49 ET

Summary

- Zymeworks is a biotech company focused on developing therapies for hard-to-treat cancers.

- Its lead product, zanidatamab, has shown promising results in clinical trials and has been partnered with larger pharmaceutical companies.

- The company also has a pipeline of early-stage candidates and a potential for substantial upside through its partnerships and commercialization of zanidatamab.

Today I explain why I've added Zymeworks (ZYME) to my value watchlist. ZYME is a biotech company with a focus on developing therapies for hard-to-treat cancers. It is a value play because it already has a (relatively) proven product that has been partnered with larger pharmaceutical companies.

Zanidatamab

ZYME's lead product is called zanidatamab. It is a bispecific antibody, which means that it targets two separate domains of the human epidermal growth factor receptor 2 (HER2). It has been partnered with Jazz Pharmaceuticals (JAZZ), a company with a $13B enterprise value in most of the world except the Asia Pacific region, where it is partnered with BeiGene (BGNE), a company with a $17.7B enterprise value.

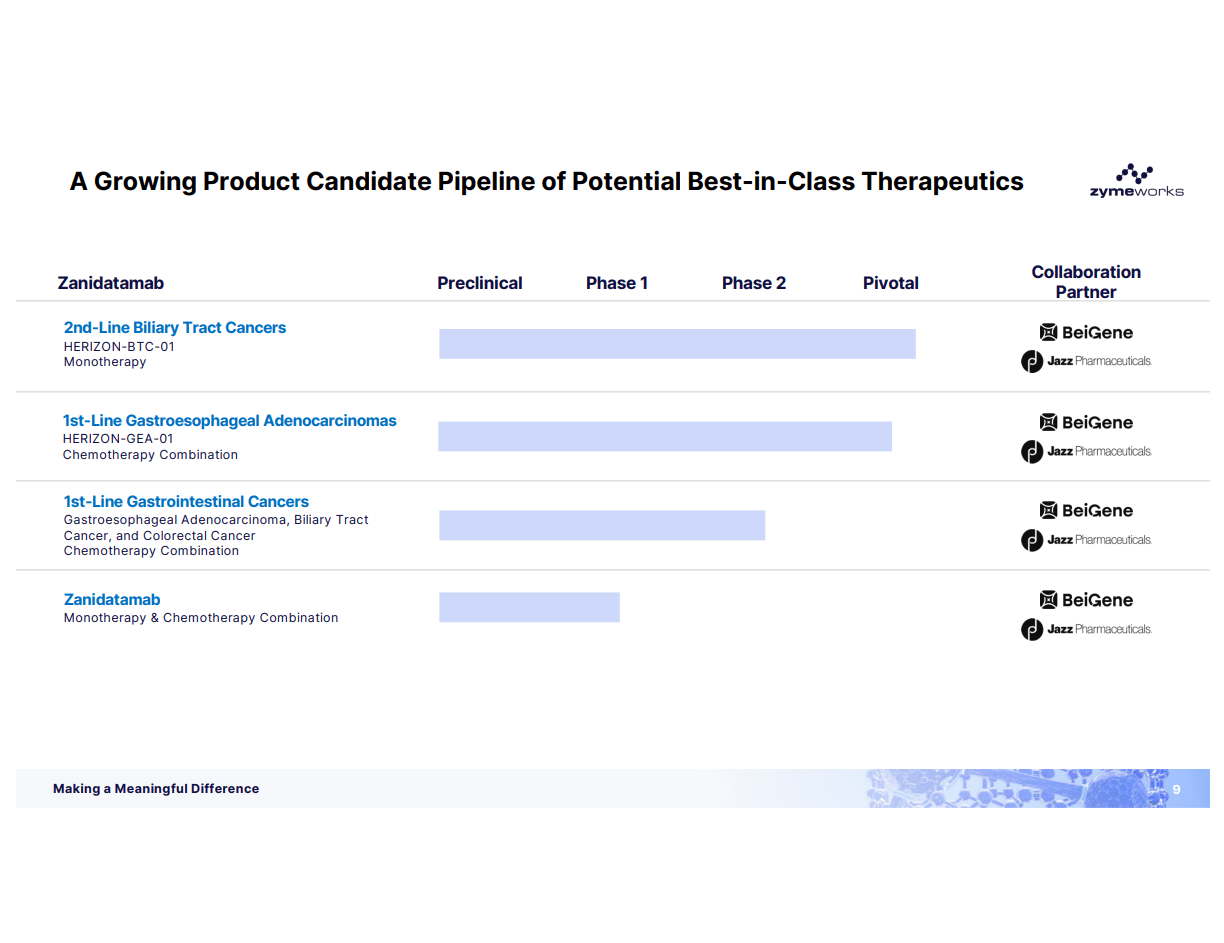

Here are the indications and status of the product as given in the latest investor presentation :

{kind=link}

The partnership opt-in with JAZZ came about after the HERIZON-BTC-01 pivotal trial data came out in December of 2022. The whole data deck is worth looking at, but here are the two most salient slides. First, an explanation of what biliary tract cancers consist of, as well as an estimate of 7,500 cases per year in the US and about 116,000 cases worldwide:

{kind=link}

And the results, with an emphasis on the 12.9 months median duration of response.

{kind=link}

Here's what JAZZ had to say about the data that led to them opting-in to the partnership (with my emphasis):

"The compelling top-line clinical data from the pivotal trial in patients with BTC highlight zanidatamab's potential to transform the current standard of care," said Rob Iannone, M.D., M.S.C.E., executive vice president, global head of research and development of Jazz Pharmaceuticals. "This important milestone strengthens our confidence in advancing this therapy for cancer patients with significant unmet need. While our initial focus will be on the ongoing clinical programs in BTC and GEA, these data add to the growing body of evidence that zanidatamab has anti-tumor activity across multiple HER2-expressing cancers ."

And the terms of the transaction were given in that same press release (with my emphasis):

Pursuant to the terms of the agreement, Jazz will make a one-time payment of $325 million to Zymeworks, in the fourth quarter of 2022, to exercise its option to continue with its exclusive license to develop and commercialize zanidatamab in the United States, Europe, Japan and all other territories except for those Asia/Pacific territories that Zymeworks previously licensed to BeiGene, Ltd. Jazz previously made a separate $50 million up-front payment. Zymeworks is also eligible to receive up to $525 million upon the achievement of certain regulatory milestones and up to $862.5 million in potential commercial milestone payments , for total potential payments of up to $1.76 billion. Pending approval of zanidatamab, Zymeworks is eligible to receive tiered royalties between 10% and 20% on Jazz's net sales .

Similarly, the terms of the BGNE deal are given in this slide:

{kind=link}

The drug seems to be advancing towards commercialization, with this update being given on the earnings call :

We continue to support efforts and regulatory interactions by each of Jazz and BeiGene for initial regulatory filings for potential accelerated approval of zanidatamab in second-line BTC. As announced by Jazz yesterday, they have alignment with the U.S. FDA on a confirmatory study in first-line metastatic BTC to support Jazz's U.S. regulatory efforts.

The next big potential catalyst will be to get results from the GEA study (HERIZON-GEA-01) which are expected in 2024. Here's a slide (right hand side) summarizing this trial:

{kind=link}

And here's a summary of the epidemiology of the disease(s):

{kind=link}

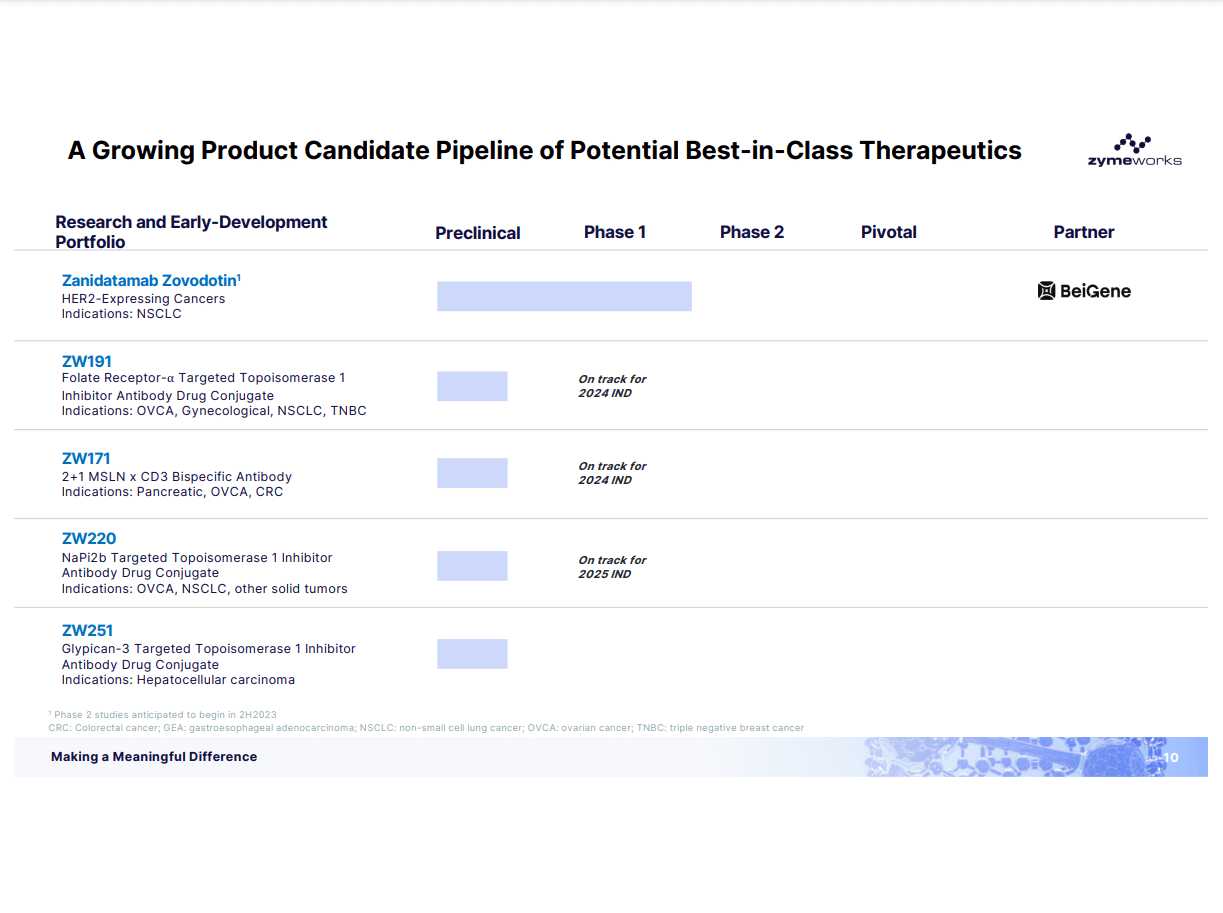

Remainder of Pipeline

ZYME has many early stage candidates and is pushing its "five by five" idea (five new drugs in clinical trials over the next five years).

{kind=link}

Given that they've proven themselves as being able to deliver value, I think all of these have potential, but they're in such early stages that one can't yet ascribe much dollar value to them. However, I do agree with their optimism that they can be more nimble and more global than most companies in executing the development cycle, as discussed on the most recent earnings call (with my emphasis):

What we have done, I think has hopefully put ourselves in a position to run a very efficient translation from preclinical into clinical studies. So, we have a great preferred provider relationship with Wuxi to make all of these molecules, which means I think as we go forward with ZW220, you'll probably see that go faster from translating from selection into clinical studies. So that's one thing we're counting on. And working in one supplier on the CDMO side. I think on the CRO side, we have the same idea to work with a preferred one group as a preferred provider and take advantage of multiple clinical studies coming on track at the same time.

We've definitely positioned ourselves with some clinical and regulatory expertise in boosting in for Asia Pacific and in Dublin for Europe to be able to start these studies with a global thought process in mind from the very beginning. We obviously have a strong, U.S. group as well, but I think you will hopefully see us take advantage of global access to patient populations of interest given the multiple tumor types that exist that we'd like to study in 171 and 191.

And I think by setting that up early, you can go much more efficiently in Phase 1 to find all those patient populations and multiple dose expansion cohorts. And you can go much faster from going from Phase 1 into a Phase 2 process, by already having a global footprint established with KOLs and all the major reasons.

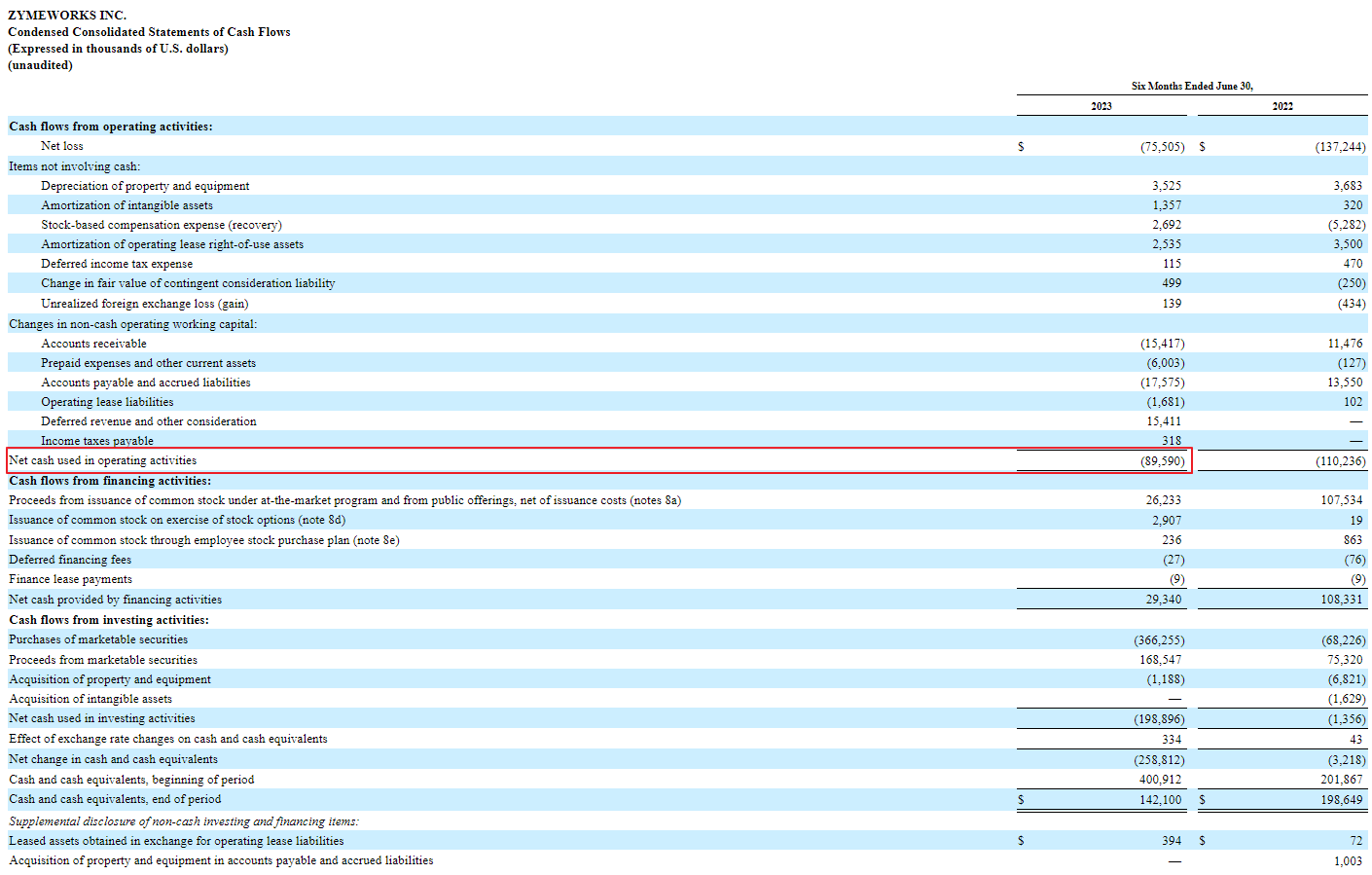

Cash on Hand

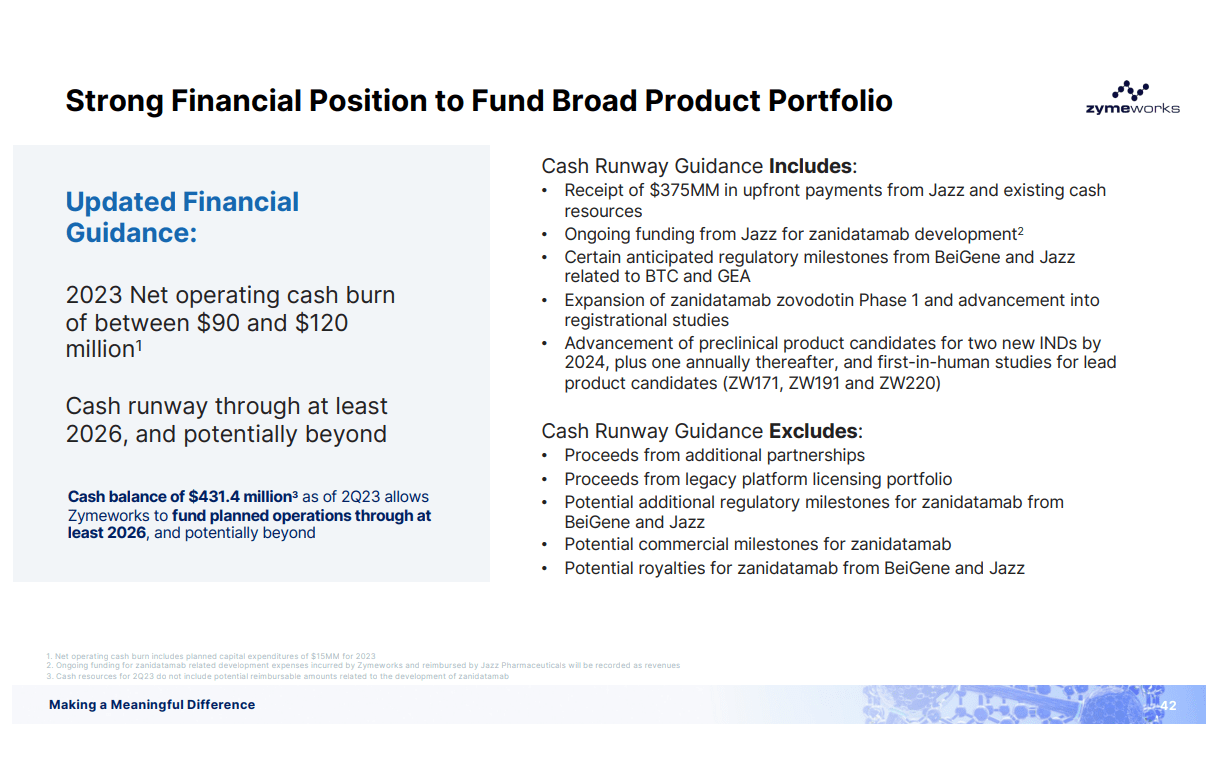

ZYME has $340M of cash and short term investments on hand and burns about $45M per quarter, meaning it has at least a year and a three quarters of cash available, not including any future proceeds from the JAZZ and BGNE deals (see valuation section below for discussion/projection of those).

{kind=link}

Despite having what appears to be sufficient cash on hand, my one reason for putting ZYME on my watchlist rather than taking a full position, is that it still is raising cash via its ATM. Everything else says it shouldn't be, so this gives me pause. From earnings call:

As of August 9, 2023, we had approximately 67.79 million shares of common stock outstanding. During the second quarter, we issued 3.35 million shares of common stock pursuant to our at-the-market facility for net proceeds of $26.2 million.

Valuation

With the stock trading at $7.12, here is a screenshot of Seeking Alpha's super helpful valuation summary:

Seeking Alpha

Now obviously, for ZYME all of its income is going to be lumpy because until (or IF) it receives regular royalties from commercialized products, revenue will consist of milestone payments if and when zanidatamab progresses through further development stages.

We've already seen how large these payments could be if everything goes well, but I'd also like to highlight what isn't yet reflected in the guidance (and valuation?). In particular, no commercial milestones or royalties are yet reflected in ZYME's guidance of having sufficient cash to operate through 2026, nor are any future partnerships on the remainder of the portfolio considered. Again, were it not for the fact that the company is still hitting its ATM, I'd have a strong buy rating on the company based on its valuation and its potential upside.

{kind=link}

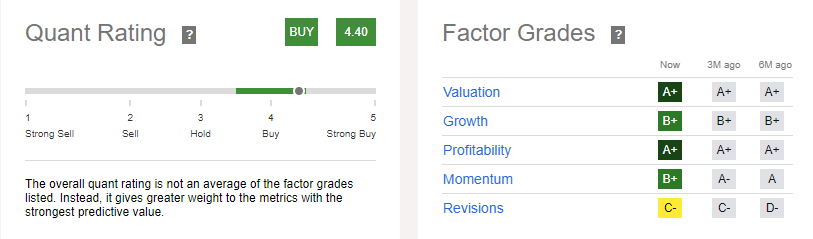

Quant Ratings

Seeking Alpha currently rates the stock a buy, with factor grades as follows:

{kind=link}

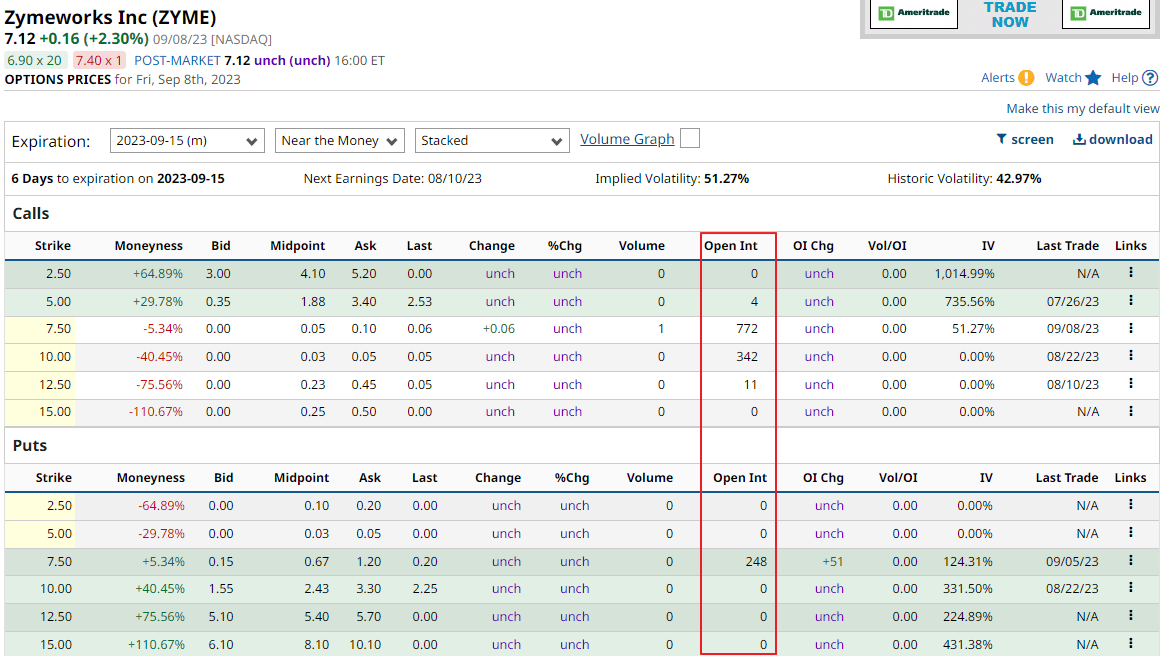

Options

ZYME trades options, but they are only moderately liquid.

{kind=link}

Risks

The biggest risk with ZYME, is that despite having strong partnerships and data, the company is really dependent on a single molecule, zanidatamab. Should new safety concerns emerge or future trials having disappointing efficacy data, the company would take a big hit (since the remaining pipeline is very far from commercialization). Anyone taking a position in the stock should size accordingly.

Summary

ZYME has proven itself, most importantly, by presenting strong enough data to compel large pharmaceutical companies to opt-in to partnerships with ZYME. As discussed above, the valuation metrics are enticing at today's share price. Moreover, there is substantial upside to those partnerships and valuation numbers should zanidatamab eventually be commercialized (particularly if it happens in the larger indication of GEA).

I rate the stock a "buy" and have taken a small starter position, but am waiting to understand why the company is tapping its ATM given all of the other seemingly bullish information about the company.

For further details see:

Adding Zymeworks To My Value Watchlist (Initial Buy Rating)