ADUS - Addus HomeCare: Capital Intensity Economic Profit Under Pressure

2023-04-12 14:55:46 ET

Summary

- Addus HomeCare has been a star performer on the NASDAQ over the past 6 months.

- Investors have rewarded the company's respectable growth percentages and commendable profitability.

- Looking ahead, I foresee a set of challenges related to its capital intensity and tightening returns on capital.

- Net-net, I've pared back my rating to a hold for now, and see a valuation range of $114–$164 depending on certain variables.

Investment Summary

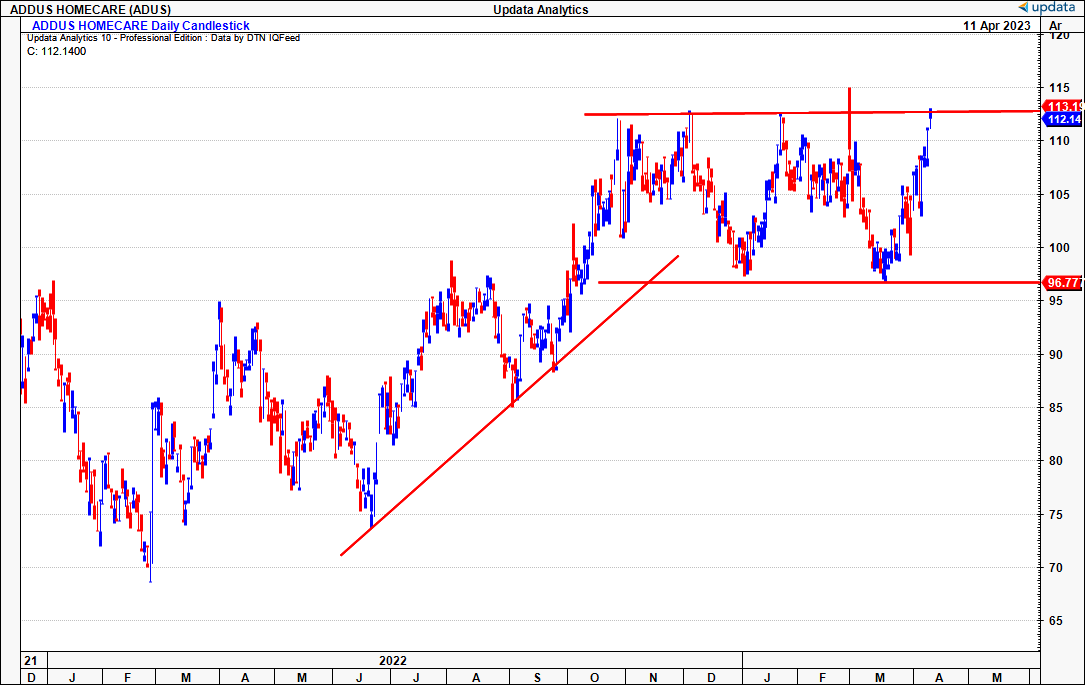

Following a strong 6-month period of growth and capital gains Addus HomeCare Corporation ( ADUS ) has repriced substantially back toward FY'21 highs. Alas, there's now a dichotomy in the ADUS investment debate.

On the one hand, ADUS investors have been treated with a 25% T12M price return, with an equity curve absent of volatility. In fact, since my last two publications on the name, ADUS has been a star performer, reaffirming the buy case in both instances (see previous publications: here , and here ). For example, original findings showed that ADUS " presented with resiliency and defensibility characteristics investors are paying a premium for..." given the shifting macroeconomic sands at the time. This was due to 1) an increasing cost of capital, and therefore hurdle rate; and 2) unwinding of the high-beta growth trade that spanned 5-years to FY'22.

Also, consider these 3 balancing points:

- Previously, I contended that ADUS' profitability was a standout. It had reasonable returns on capital coupled with strong free cash conversion to the company's shareholders after reinvesting for future growth. This is further exemplified by the 267% YoY growth in free cash to the firm ("FCFF") from FY'21-22, and I've estimated the company has reinvested ~26.8% of post-tax earnings as growth capital for this year. As such, as the firm's equity investors, we've obtained $56.5mm in owner earnings over this timeframe as well, unlocking a CAGR 8.8% in stock price gains since right before the pandemic began. (As a reminder, owner earnings is the free cash flow left over (distributed) for shareholders after the company has reinvested some of its profits back into the business) .

- And yes, managed care organizations are a profitable business and the market has been generous in rewarding ADUS on the same merits.

- So much so, that it now trades at a hefty 39x trailing earnings - above the valuation stated in my previous ADUS publication - and Wall Street has priced it to re-rate lower at 32x forward earnings in FY'23. Further, I've priced it at only very slight premium to market value in my own forward P/E estimates discussed here.

And so it goes, ADUS' key investment facts are under heavy scrutiny as I revisit the investment debate here.

That said, it's best to take first principles. Satisfying the fundamental investment questions comes from analyzing ADUS' current operations and growth strategy.

Alas, I'd segregate two challenge areas for the company:

1. Pressures to current operations:

- The impacts from increasing revenue costs and OpEx over the coming 3-5 years, eroding pre and post-tax margins.

- Concentration risk in generating its top-line revenues.

- Higher capital intensity and maintenance CapEx requirements to maintain existing level of operations.

- Coupled with this, the company's dwindling returns on capital.

2. Challenges to future growth:

- Challenges to the business model with obtaining additional customers through regulatory channels (i.e., Medicare, Medicaid, etc.).

- ADUS' growth strategy that focuses on acquisitions to overcome the above point.

- The ability to generate an economic profit from its capital budgeting and investments for future growth.

Here I'll run through both in the deep dive below to present my re-rating to a hold for now.

Fig. 1 ADUS Price Evolution, FY'21-Date

{kind=link}

Analysis of current operations

Detailed understanding of the business model and way ADUS makes money is imperative to highlight the case. As a reminder, the firm operates by providing healthcare services in 3 segments:

- Personal Care

- Hospice

- Home Health

ADUS' customers (new and retained) fall under performance obligation contracts with the state, local and federal agencies, along with managed care organizations ("MSOs"), commercial insurers, private consumers. Further, the bulk of its customers are dual eligible for Medicare and Medicaid benefits.

A) Revenue recognition

As to the contracts - after the company receives an order, this creates a performance obligation with two skews of revenue. One, for the service provided, two, the service hours per consumer. The company invoices against the service hours, at a rate linking to the type of service. It books revenue against the number of days within each reporting period (key facts on this are discussed later). Payment receipts are generated from the list of agencies and MROs listed earlier, to generate income for the company, and feed profits downstream to investors, in order to create value.

The bolus of revenue is generated from the personal care segment, where it provides personal care services DTC. Hospice revenue is booked from palliative care services (nursing, home care, specialist care, etc.) and ancillary services provided to families (social work, support, etc.). The cost of service delivery is baked into net revenue. In addition, ADUS provides home healthcare services DTC under the mentioned contracts albeit with Medicare and various MCOs.

B) Current performance

In FY'22, the firm clipped top-line revenue growth of 10% of $951mm, growing net operating profit after tax ("NOPAT") 59% YoY to $59.4mm. To hit this mark, it required a $27.8mm increase in net working capital ("NWC") from FY'21, excluding $80mm in cash on hand, and an $8.3mm YoY increase in CapEx - the highest ever for ADUS. This was coupled with a $9.5mm YoY increase in tangible capital under PP&E, mainly from additions to computer software (Figure 2).

Fig. 2

Data: ADUS 10-K FY'22, pp. F-19

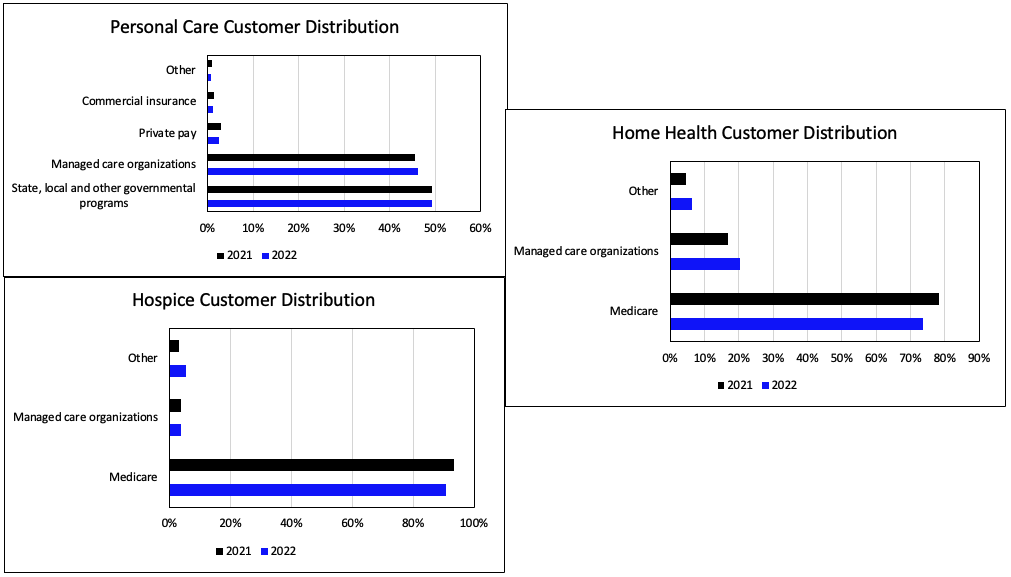

Cash generated from operations was $105mm which the firm helped to deleverage to just 1x EBITDA. Personal care contributed 74.2% of the top-line, with hospice generating 20.5% and home health 5.3%. Further, the distribution of customer revenue is heavily skewed to Medicare in home health and hospice, but is fairly balanced between MCOs and government programs for personal care (Figure 3). Service was provided to a total 66,000 discrete customers (down 1,000 from the year prior) over 202 offices, generating ~$14,410 per customer (up from $12,902 in FY'21) and $4.7mm per office.

On a same-store basis, ADUS saw ~800bps YoY growth, driven solely by the home health segment. It pulled this down to a 9.2% core EBITDA margin and $2.90 in core EPS. Noteworthy, these are ahead of my FY'23 estimates of $2.58/share in earnings and 7% EBITDA margin. I am calling for a 13.6% YoY grown at the top-line to $1.08Bn, requiring another $8.3mm in CapEx and additional $20mm in NWC.

Fig. 3

{kind=link}

C) Pressures to current operations

The macroeconomic milieu is changing rapidly. Consequently, so is my constructiveness on this name. I'd also like to point this out: The majority of ADUS' same-store growth to date has been obtained from reimbursement rate increases across the states. Collectively, the double-digit revenue and NOPAT growth ADUS has enjoyed since FY'18 may be under pressure, in my estimation. Whilst not impossible to overcome, it will be difficult to achieve at the margin.

My case is as follows:

One, the simple fact is that hospice companies live under 2 specific payment umbrellas:

- Inpatient Cap

- Aggregate Cap

The former places a ceiling on the number of patients that can be seen and reimbursed under Medicare stipulations. The aggregate cap, however, limits the Medicare reimbursement a hospice center can receive. It is based on the number of Medicare patients served per period. What that means, is if a hospice exceeds the aggregate cap, it has to repay Medicare the excess in full. The FY'23 cap = $32,486. With ADUS' average revenue per patient at c.$14,410, this could become an issue. It may limit the more profitable patients in payment capacity. It also places an artificial ceiling on patient (customer) profitability at the upper end of treatment cost.

Two, the pitch from management, says that an industry shift away from fee-for-service models to MCOs underpins ADUS' value proposition. States are pushing Medicaid enrollees onto managed care programs ("MCPs") which is beneficial to MCOs. Key benefits touted by pundits include:

- Economic incentives to lower costs (profitability) for customers.

- Service incentives to provide more effective service.

- Better management over customer expenditures.

- Streamlined pathways across all allied health professionals and medical practitioners.

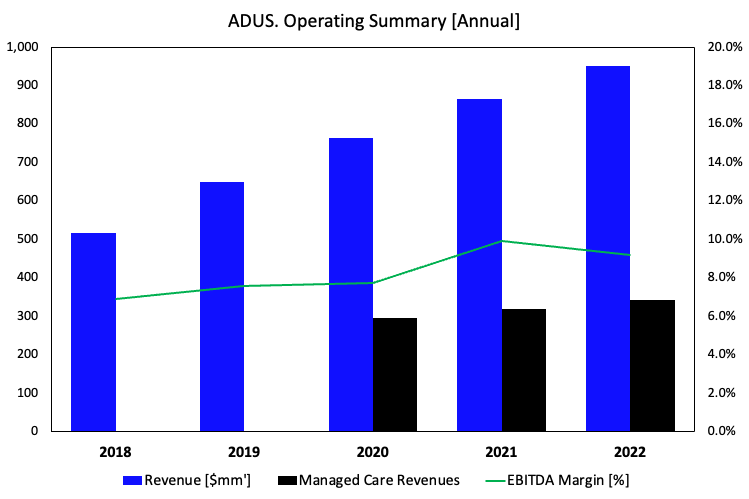

It's not surprising, therefore, to see that ADUS expects more referrals from MCOs into the future. That's good, however, managed care as a function of revenues has been sliding for the company since FY'20. Last year, managed care revenues accounted for 36.0% of turnover, down from 37.2% and 38.6% in 2021 and 2020, respectively. This, despite growing 7% YoY (Figure 4).

Fig. 4

{kind=link}

Three, and more broadly, ADUS's growth contribution hinges entirely on the respective local/state/federal agencies authorizing new customers for the company. Added to that, most of ADUS' personal cares revenue comes from the work it does for state and local governments. So there's a concentration risk in the company's distribution of revenues. Consider that:

- Turnover derived from the company's operations in Illinois, came to ~44% of service revenue in FY'22, up from 38% last year.

- Of this, one customer - the Illinois Department of Ageing, made up ~21% and 18% of net revenue and accounts receivable, respectively.

- More than 51% of turnover in the personal care segment came from Illinois.

- Meanwhile, state, local and other governmental programs made up 49% of revenue last year.

- Revenue, gross profit and operating income is also concentrated in personal care (Figure 5) across all markets.

Four, there are direct margin pressures to operating income growth from this year. A jump in OpEx is actually unavoidable, due to legislated minimum wage increases in Illinois, the firm's main money maker, geographically speaking. Further, Chicago is the only market ADUS didn't receive a corresponding increase in reimbursement rate. Management expect a 120bps YoY decline in gross margin this year, behind my projected 220bps YoY decline to 29.3%. My numbers also project a 12.1% jump in OpEx to $253mm clipping operating income to $63.4mm, NOPAT to $51.5mm. Consequently FY'23 looks to be a challenging year for ADUS below the top-line.

Fig. 5

Data: Author, ADUS 10-K's

Growth contribution looks compressed

In my estimation ADUS needs to hedge its top-line by distributing revenues across a wider customer base. It continues to put its balance sheet to work through strategic acquisitions to achieve this.

Questionable use of capital using acquisitions to grow

Last year, ADUS booked $65mm in annualized acquisition revenue from its JourneyCare and Apple HomeHealth acquisitions, made in FY'22. Together, these cost ADUS $99.3mm in cash, and so the $65mm annualized revenue is a good start. I'd estimate ~$3-5mm in after-tax operating income from this, equating to a ~4-5% return on the investment. But the firm's WACC hurdle was 8.9% last year, meaning the acquisition revenue didn't beat the hurdle rate, and may have been destructive to shareholder value. Furthermore, suppositions from McKinsey & Co. establish that acquisitions are the least effective form of growth to create long-term shareholder value.

Alas, the focus on acquisitions is another reason I have turned more cautious on ADUS. I hoped management would display a more balanced capital budgeting strategy to fund its future growth initiatives from this year. Tied to the points on concentration risk above, it would be a great way to diversify into new revenue streams that aren't capped from a regulatory standpoint. Plus, the more challenging funding environment (higher cost of capital) is a large barrier to entry in most markets, allowing ADUS to deploy capital more efficiently.

Moreover, the acquisitions made in the last 2-3 years haven't pulled through yet. Seen below (Figure 6), nearly all of the firm's key business metrics in the personal care segment slipped from FY'21-22. Whilst revenue/billable hour increased 5.3%, same store revenues fell 37% to $4.6mm. This, coupled with a disposal of 6 locations over the year. An acquisition strategy ideally builds momentum in same-store growth to justify this use of capital, not the case here.

Fig. 6 - Personal Care Key Operating Metrics:

Data: Author, ADUS 10-K's

Fig. 7

{kind=link}

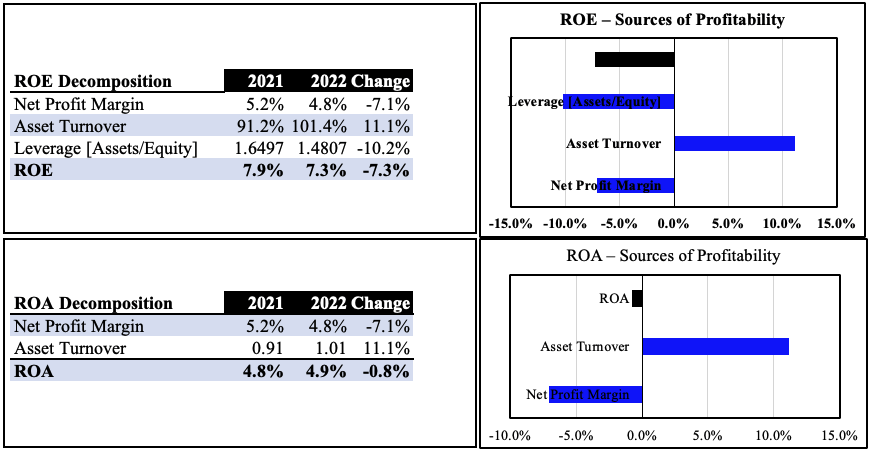

It's unsurprising therefore to see profitability compress YoY:

- For equity investors, the ROE slipped 6bps to 7.3%.

- For the providers of capital, ROA come in flat.

- Both despite a much broader capital base.

Both measures were crimped by margin compression in post-tax earnings, as seen in Figure 7.

How ADUS will unlock value into the future is absolutely paramount to know in detail

Plus, acquisitions are a very expensive way to grow. For ADUS, ~10.4% of revenue and 193% of NOPAT in FY'22 alone. Three points on growth actually:

- All growth comes at a cost to shareholders.

- All growth is not created equally.

- Growth can be destructive to shareholder value.

All growth comes at a cost to shareholders, as frictional costs mean investors typically earn less than their businesses. Those costs being maintenance capital charge on CapEx, NWC and OpEX, plus the amount of profit a firm needs to reinvest to grow.

Most of the time, firm's take some of their profits for the year and reinvest this to fund growth initiatives. Even when raising capital (debt, equity, hybrids), this decreases future earnings somewhat. Key point being, for the most investable companies, it doesn't require a whole lot of capital to grow, or maintain operations. Meaning, the earnings distributable to their owners (shareholders) is higher. And so not all business growth is created equally.

And most importantly, if a firm's growth investments don't outpace the cost of capital, company growth erodes shareholder value. Think of it this way. Profits were taken from shareholders and invested at a negative return. In other words, there is no economic profit, instead, an economic loss.

That is critical - points (1) and (2) above are satisfied via economic profit. As a reminder, the value of any financial asset is the present value of the cash it can generate for us, the investors . With an economic loss, these frictional costs are now being incurred in amounts that cause shareholders to earn far less than previous. If that's the case, the growth is destructive to value.

Keeping these in mind, NWC hurdles for ADUS to overcome include:

- NWC requirements intensifying as operations expand, not to mention with further bolt-on acquisitions. To grow revenue $86mm and NOPAT $3.3mm required an additional $27mm in NWC in FY'22 (excluding cash & equivalents, and including A.R. from all acquisitions).

- Excluding acquisitions, core A.R. actually decreased by ~$17mm on my calculations. Hence, NWC intensity is increasing with acquisitions.

- To this point, accounts receivable has increased drastically and much faster than revenues since Q3 FY'21 to date, on a rolling TTM basis (Figure 8). Cash collection was therefore weak against booked revenues.

Fig. 8

Data: Author, ADUS 10-K's

Management have acknowledged this and focused on cash collections in the back end of FY'22, and DSO was ~1 day less YoY. Nevertheless, given the risks above, if cash receipts from 1 or more payer falls behind - this trend can get out of hand.

At the same time, the capital charge on current operations and growth is increasing. The firm now has ~$700mm in investment required to maintain the current level of operations on OpEx of $226mm. Despite an upshift in NOPAT margin, invested capital turnover has stagnated at ~1x, suggesting a lack of capital efficiency (Figure 10).

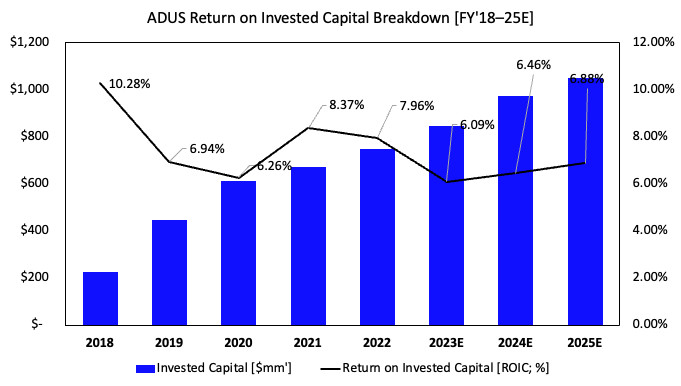

Further, a return on invested capital ("ROIC") of ~8% in FY'22 was below the WACC hurdle of 8.9% (Figure 9). Hence, ADUS generated an economic loss of 0.9% for the year. For these reasons, ADUS' competitive advantage seems to have waned.

Fig. 9 - ADUS Capital Intensity, ROIC

- Over the last 3-years, the company has invested an average of 86% of its post-tax profits each year as capital for future growth.

- This has generated a 15.8% incremental ROIC, growing the company by 13.6% over this time.

- Hence, the 86% cost to shareholders has yielded ~16% in incremental value in 3-years.

{kind=link}

Fig. 10

Data: Author, ADUS 10-K's

Herein lies the headwinds for ADUS in my estimation. It's going to take far more capital to maintain and grow operations looking ahead, at lower rates of investment return.

Capital density and OpEx are both intensifying. Plus, the firm looks to continue on the acquisition trail. This, as the cost of capital remains at multi-year highs. Finally, per management on the FY'22 call: "...we're not going to continue to see $20 million in net working cap improvement even as we grow. That's probably more of a onetime thing".

So I believe the ROIC will continue to stay under pressure. So the vicious cycle is formed: more profits are reinvested each year to finance this, meaning less earnings distributed to shareholders to create value. To specify my models bake in 13.6% YoY growth in revenue and 13% decrease in NOPAT, after:

a). A $100.7mm increase in invested capital, including $19.7mm increase in NWC requirements, not to mention suspected investment in intangibles, goodwill charge from acquisitions.

b). ADUS reinvesting ~26.8% of FY'22 post-tax earnings as growth capital.

I project ADUS to reinvest ~30.3% of its earnings this year, 162% over the next 3-years. This, as OpEx is projected to increase 12% YoY to $253.6mm and earnings decrease to $2.58 per share. These numbers also point to ROIC of 6.09% in FY'23, then $6.46% in FY'24. Hence, my estimates point to a widening economic loss from FY'23-'24, (Figure 11). As a result, forecasts point to just $7.9mm in FCF to shareholders this year, down from $51.8mm last year, compressing valuation upside and share price performance.

Fig. 11

Note: Hurdle rate assumed at 8.9% into FY'24. Previous to this, calculated from historical data. (Data: Author, ADUS 10-K's)

Valuation

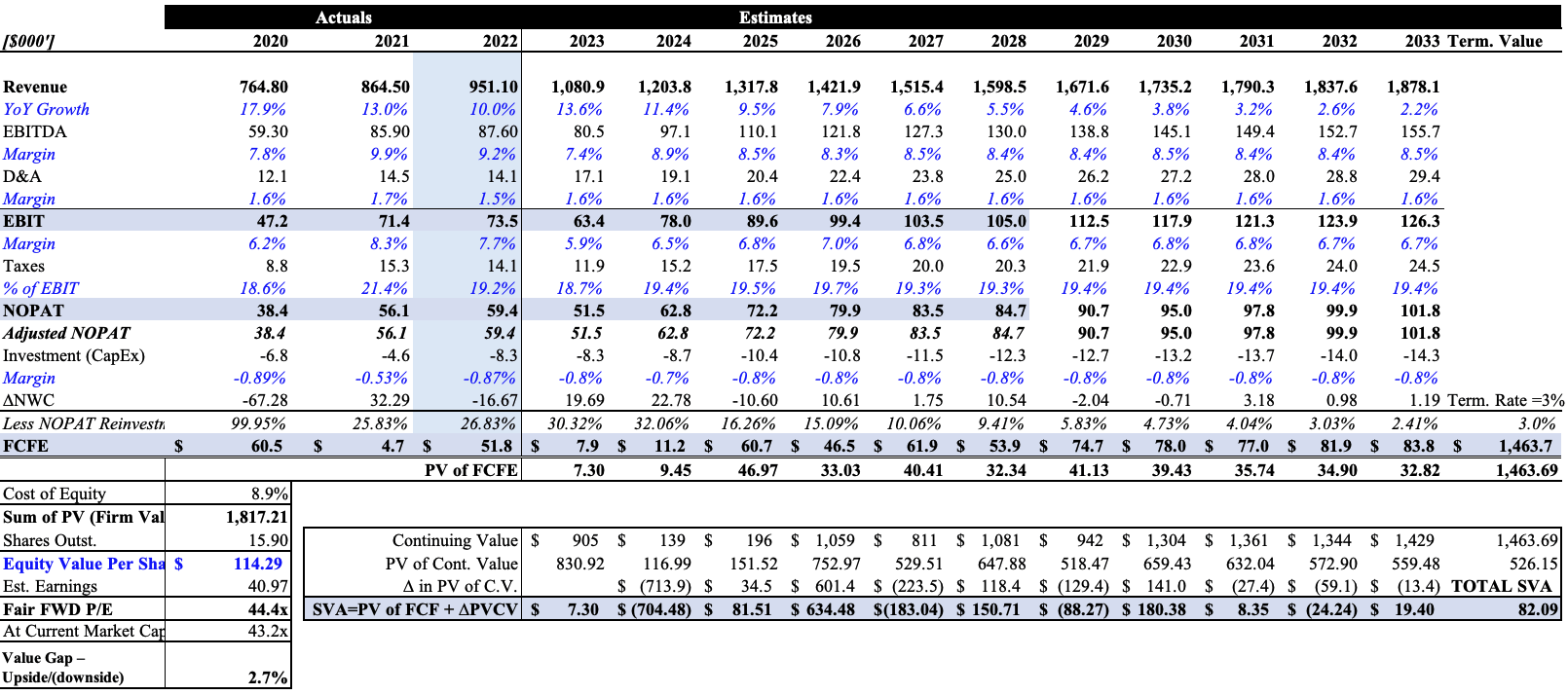

As equity investors, we should be very concerned about dilution to ROIC and economic profit. We don't necessarily want our portion of the profits to be financing a company's growth. We want the company to be doing this itself, recycling the returns it earns from its investments.

This presents a major problem to valuing the firm. If ADUS can't earn the cost of capital on its new + maintenance capital, the economic loss from FY'22 will continue to widen. As such, any growth it obtains will be destructive to shareholder value. As shown in Figure 11, assuming an 8.9% hurdle rate into FY'24E, my estimates produce a sustained economic loss over this time. This is a major risk in the investment debate.

With ADUS' capital charges projected to increase, cash flows to investors will decrease without a loftier ROIC. A mammoth jump up in revenues and operating margins is also required to offset this. My numbers point to a difficult 3-year period ahead in this domain. The differentials in capital intensity look to generate lumpy earnings and most importantly, lumpy FCF to shareholders, limiting the valuation upside at a presumed 9% cost of capital and 3% long-term growth rate. My numbers also forecast a 4.2% incremental ROIC into FY'25, on a 6.8% NOPAT growth rate. But, given the projected economic losses, I believe ADUS would have to reinvest 167% of its earnings to get there, eating into owner earnings.

Considering these assumptions, my conclusions on ADUS' valuation are as follows:

- The stock is worth $114 today with the discount and growth rates stipulated (suggesting the firm is worth $1.82Bn). This is well off my $138 assigned previously.

- With the growth assumptions shown in Figure 12, ADUS would create another $82 in shareholder value added ("SVA") by FY'33E, a 5.7% CAGR.

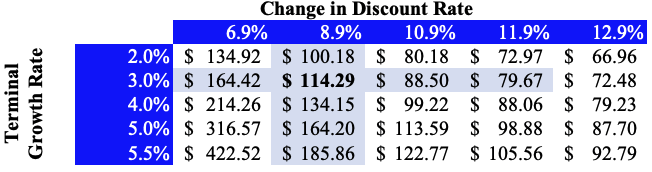

- However, if there's a repricing of the cost of capital, a 7% discount rate could see it valued at $164 (Figure 13). The SVA would be $151, 8.9% CAGR.

- Hence, this supports a neutral vs. bearish view.

With my FY'23 earnings estimates of $41mm, the fair P/E is 44x ($1.82Bn/$41mm), versus the market's view of 42x using my estimates ($1.79Bn/$41mm). ADUS is currently trading at 39x trailing earnings. With my earnings growth and reinvestment estimates, the payback period on this is around 5-6 years, which also isn't terrible, but not fantastic either.

Fig. 12

{kind=link}

Fig. 13

{kind=link}

Conclusion

After this extensive deep dive, the investment debate and re-rating to a hold can be summarized into these key points:

- Capital intensity is increasing for the company, meaning it has to invest more capital to maintain, and grow operations.

- The return it is expected to see on this capital is projected to decline. Plus, the cost of capital continues to be high, leading to economic losses for equity holders.

- More capital required to operate/grow + lower rates of return (below the hurdle) = less cash flow available to the company's owners (i.e., the shareholders).

- Hence, ADUS' growth strategy of bolting-on acquisitions comes at a risk to creating value for shareholders.

- Added to that, there is concentration risk in its top-line revenues that are susceptible to newly-enforced challenges to reimbursement, labor costs.

- This hurts the valuation of the company, and I've pared back my intrinsic value to $114, but see $164 with a lower cost of capital.

- These factors support a neutral view, in my estimation.

In short, I am paring back my valuation on ADUS from a buy to a hold. If the company surprises in Q1, it would be from higher cash conversion, less NWC requirements and tremendous growth in its acquisition revenue. I wouldn't be upset to see this, that's for sure. I'm looking forward to updating investors as the new data arrives.

For further details see:

Addus HomeCare: Capital Intensity, Economic Profit Under Pressure