ADUS - Addus HomeCare: Ideal For Those Looking To Step Up In The Quality Resiliency Spectrum

Summary

- Addus HomeCare presents with the resiliency and defensibility characteristics investors are paying a premium for in H2 FY22.

- For those investors seeking to stabilize risk-adjusted equity returns, ADUS is a worthwhile consideration with a basket of similar securities.

- Valuations are supportive of this resiliency premium and corporate value stands up well even with necessary adjustments.

- We rate ADUS a buy and value the company at $96–$103.

Investment Summary

Within healthcare there are numerous defensive offerings that offer equity portfolios the chance to shift down in equity beta and stabilize risk-adjusted returns. One such calling is Addus HomeCare Corporation (ADUS) with its resiliency characteristics. Our findings indicate that ADUS offers compelling value - even when making substantial but necessary adjustments to its financial statements to reflect a more accurate snapshot. With Q2 FY22 return on invested capital of 6.4% and the WACC hurdle of 8.3% on an annualized basis, ADUS is the kind of long-term cash compounder we are seeking exposure to, and we advocate its inclusion in portfolios looking to shift up in the quality and resiliency spectrum. Valuations are supportive of a defensive play with additional benefits listed above. This in mind, we rate ADUS a buy on a $96-$103 valuation.

Exhibit 1. ADUS 6-month price action

Shares have caught a bid in H2 FY22 amid a factor rotation back into defensives. In that vein, ADUS looks to offer further upside capture as investors look to shift up in the quality spectrum.

{kind=link}

Q2 earnings - a deeper dive

Diving in further than standard GAAP reporting, we extract some interesting data for ADUS. The company recognized a ~870bps YoY increase in revenue to $237 million. Personal care contributed ~74% to the top whereas hospice sales were 22% of revenue. Geographically, the bolus of ADUS' turnover [accounts receivable included] is obtained from the federal stage and local government payors. Of this, the bulk of revenue is derived from Illinois, attributing nearly 44% to the top-line last quarter, up ~490bps YoY. The largest payor in Illinois is the Illinois Department of Aging. It accounted for 20.7% of revenue in Q2 FY22, down ~200bps YoY. However, accounts receivable from this payor grew at a similar rate in the 12 months to amount to 18.3% of turnover.

Meanwhile, same-store revenue in its home health segment grew 21.6% YoY and was up 36% QoQ. Turnover was $10.5 million in this division, ~4.5% of turnover. This was backed by increased volume of admissions, climbing 25% over the year. Average daily census ("ADC") in its hospice segment also improved with a median length of stay to 23 days from 17 days in Q2 FY21. The company has also booked another $55 million ($3.43/share) in revenue from its JourneyCare acquisition, despite overhang from proposed reimbursement changes from CMS.

Moving down the P&L, operating expenses of $58.7 million were up YoY but included $3.6 million in depreciation and amortization. It brought this down to operating income of $16.9 million and net income of $11.25 million, flat from last year's result. ADUS did convert $56 million of FCF as well and investors realize a 7.7% yield on this, up from $16 million and 3.6% in Q2 FY21 respectively. These are attractive numbers on face value and demonstrate a resilient period of growth for the company.

Adjusted measures to reflect corporate value

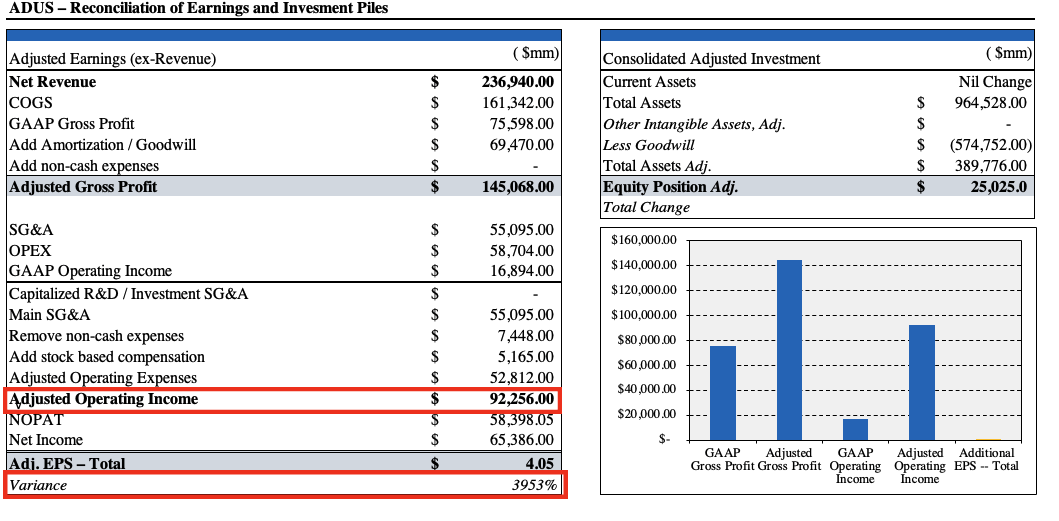

Further examination of ADUS' financials reveals GAAP accounting underserves the company's stated earnings. This has implications on valuation, on the earnings portion of the calculus. Adding back $69.4 million of non-cash charges to COGS restates gross profit to $145 million, up from a printed $75.6 million. Moreover, SG&A costs were recorded at $55 million, and we estimate that 100% of this is likely to be 'maintenance G&A' that is required for operations, and not an investment. We couldn't see evidence of otherwise in the 10-Q.

Adjusting for non-cash operating expenses and adding in stock based compensation of $5.165 million restates ADUS' operating income at $92.25 million, ahead of GAAP reported c.$17 million. This has profound impacts to earnings as well, as, following this reconciliation process, EPS lifts to $4.05 and therefore presents with compelling value.

Moreover, as seen in Exhibit 3, ADUS boasts more than $574 million in goodwill on the balance sheet, comprising more than 50% of total assets. Depending on how one values goodwill, treatment of it in ADUS' case has immense impact on factors of valuation. Stating it in the calculation of corporate value would see ADUS' equity value at $599.7 million. However, removing the goodwill impairment [it isn't amortized like other assets], shareholder equity slips to $25 million. The question then arises on how much, if at all, of an issue this difference will be.

Exhibit 2. Adjusting for goodwill has substantial differential in valuation outcomes

The question then turns to exactly what are we buying here?

{kind=link}

Exhibit 3 covers the company's accounting for its assets and liabilities acquired, with the bolus comprised of goodwill. Again, goodwill is a non-cash asset that must be tested for impairment periodically, and therefore we question what future economic value from $70.77 million of undefinable value might be provided in these instances. We choose to omit goodwill from our valuation.

Exhibit 3. In ADUS' acquired assets and liabilities, goodwill makes the bolus of 'value', ahead of identifiable intangibles that can be amortized

Data: ADUS 10-Q Q2 FY22

Valuation

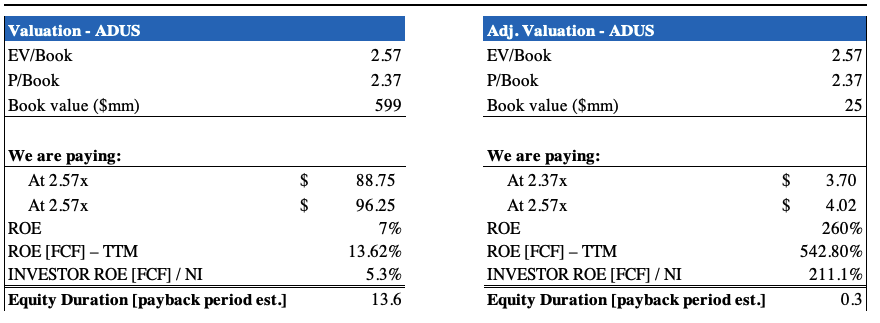

Shares are priced at roughly 2.5x enterprise value ("EV") to the stated Q2 FY22 book value of $599 million. At this multiple, we'd be paying an implied price of $96.25, a premium that will need justifying from the earnings pile of ADUS' valuation. In terms of the investment pile, our post-adjustment output provides a paradoxical viewpoint - we'd be paying a large discount, but for a mere $25 million in value on the balance sheet. The question is if one is prepared to pay 25x T12M earnings for that.

Alas, as seen in Exhibit 4, there could be compelling value on offer post-adjustment. If we accept these adjustments, then the adjusted FCF return on equity is a staggering 542% for ADUS, and an equally impressive 211% for us as investors if we pay 2.5x this book value. The implied payback period from FCF is less than 1 year at this level.

Exhibit 4. Substantial differences in valuation depending on how goodwill is treated on the balance sheet

Data & Image: HB Insights Estimates

{kind=link}

With respect to the earnings pile of valuation, outputs vary from a price objective of $89.55-$103.85 depending on forward estimates. We've priced FY23 EPS estimates in a range of $2.93-$3.63 for ADUS. As seen in the Exhibits below, this produces the valuation range stated above. The arithmetic mean of these two values is $96.52, suggesting the stock could be fairly priced at this level based on the above analysis as well.

Exhibit 5. Valuation - earnings pile

Data: HB Insights US Equity Fund Data: HB Insights US Equity Fund

What we see here is the differential between the two EPS forecasts. Each suggests that we are paying a fair and reasonable price at ~2.5x EV/book value.

In effect, we are paying an implied $88.75-$96.25 to receive $89-$103 in value (7-15% upside from the current market price). With that in mind, valuations are supportive for further upside, even backing goodwill out of the picture as a cleaner measure of tangible/intangible value.

In that vein, we rate ADUS a buy and value the stock at $96-$103. We believe the company's resiliency premium will continue to shine through and offer investors a stabilizer of risk-adjusted returns in equity portfolios on the tactical allocation side.

For further details see:

Addus HomeCare: Ideal For Those Looking To Step Up In The Quality, Resiliency Spectrum