AHEXF - Adecco: Growth Rate Insufficient At Closer Look Maintain Sell

2023-06-22 00:22:22 ET

Summary

- The HR industry can provide insight into the economic cycle and overall economic direction.

- Adecco Group, a Swiss HR company, has been struggling for the past decade against revenue stagnation and inefficiencies which led to low margins.

- In the meantime, Randstad has become the industry leader through key acquisitions.

- Adecco wants to walk the same strategy, but it has increased its leverage, endangering its dividend.

- Though Adecco reported revenue growth, there are reasons to believe volumes were actually down during Q1.

Introduction

The HR Industry often helps investors understand the economic cycle and what direction the economy as a whole is going. In fact, as soon as the labor market heats up, staffing companies are among the first ones to perceive a surge in workforce demand. On the other side, as soon as the economy slows down, these companies are among the first ones to feel the lack of demand for stable workers which may, at times, lead to a larger use of temporary staffing.

In this article, I would like to go over The Adecco Group ( OTCPK:AHEXF ) after it released last month its Q1 2023 earnings report. We have to see together whether the company deserves a rating upgrade or if we should just stick to the sell rating I gave after it released its annual report back in March.

Summary of previous coverage

When I initiated my coverage on the Adecco Group, I explained how this Swiss HR company offers temporary staffing, permanent recruitment and training services to employers. It operates in Europe and North America and it has three divisions: Adecco, LHH, and Akkodis. At that time, the company's revenues came 61% from Europe and 17% from North America. Among its services, the most important one is flexible placement (temporary staffing).

When I published my first article , my thesis was that Adecco could have been a good investment opportunity since the stock was trading at its (up-to-then) 2022 low. After all, 2022 was a year with a hot labor market and staffing agencies had a lot of hard work to do and to benefit from. Due to favorable macroconditions and an interesting entry point, I first rated Adecco as a possible buy, though not as interesting as other peers such as Randstad. But as the stock didn't really move (since then, the stock has had a total return of just 1% with the stock price actually down by almost 6%), I started digging deeper to understand whether or not there were some hurdles investors were discounting.

In this way, I gained a clearer understanding of what I think was - and still is - one of Adecco's faults. Adecco has been a stagnating company for more than a decade, alongside its peer ManpowerGroup Inc. ( MAN ). This is not an industry problem, because, in the meantime, Randstad has grown to become the industry leader. At the end of 2022, Randstad's revenue was €7 billion, up 12% YoY, with a gross profit margin of 21%, while ManpowerGroup's revenues were $4.8 billion, down 7%, with a gross profit margin of 18.3%. Randstad outperformed both peers , when considering EBITA margin and net income growth, thanks to the performance of two divisions: Inhouse Services (workforce management) and Randstad Professionals (middle and senior leadership positions).

One last point. In my previous articles, I still considered Adecco to be a reliable dividend payer. However, after the Akka acquisition, Adecco reached a net debt/EBITDA ratio of 2.5 compared to the 0 it had the year before. Of course, Adecco has repeatedly stated that it is committed to deleveraging its balance sheet and lowering the net debt/EBITDA ratio. However, this will lead the company to use a larger-than-usual portion of its free cash flow. Therefore, investors should not expect a large dividend boost, while the company undertakes the activity of de-risking its balance sheet. In addition, Adecco has already been using part of its reserves to pay out its dividend, while having part of it not subject to the withholding tax. Still, a dividend paid from a company's reserves is not the best dividend to look for.

Q1 2023 Results

Before we dive into the most recent numbers, let me give a quick reminder. The HR Services industry is quite fragmented, with the leaders holding a 4-5% market share each. It is also an industry with slow growth and low margins. Therefore, we need to set our mind to rather low numbers compared to many other industries where we see growth and margins in the high single digits or in the double digits.

Now, let's take a look at Adecco's results to see how the company started 2023.

{kind=link}

Adecco Q1 2023 Results Presentation

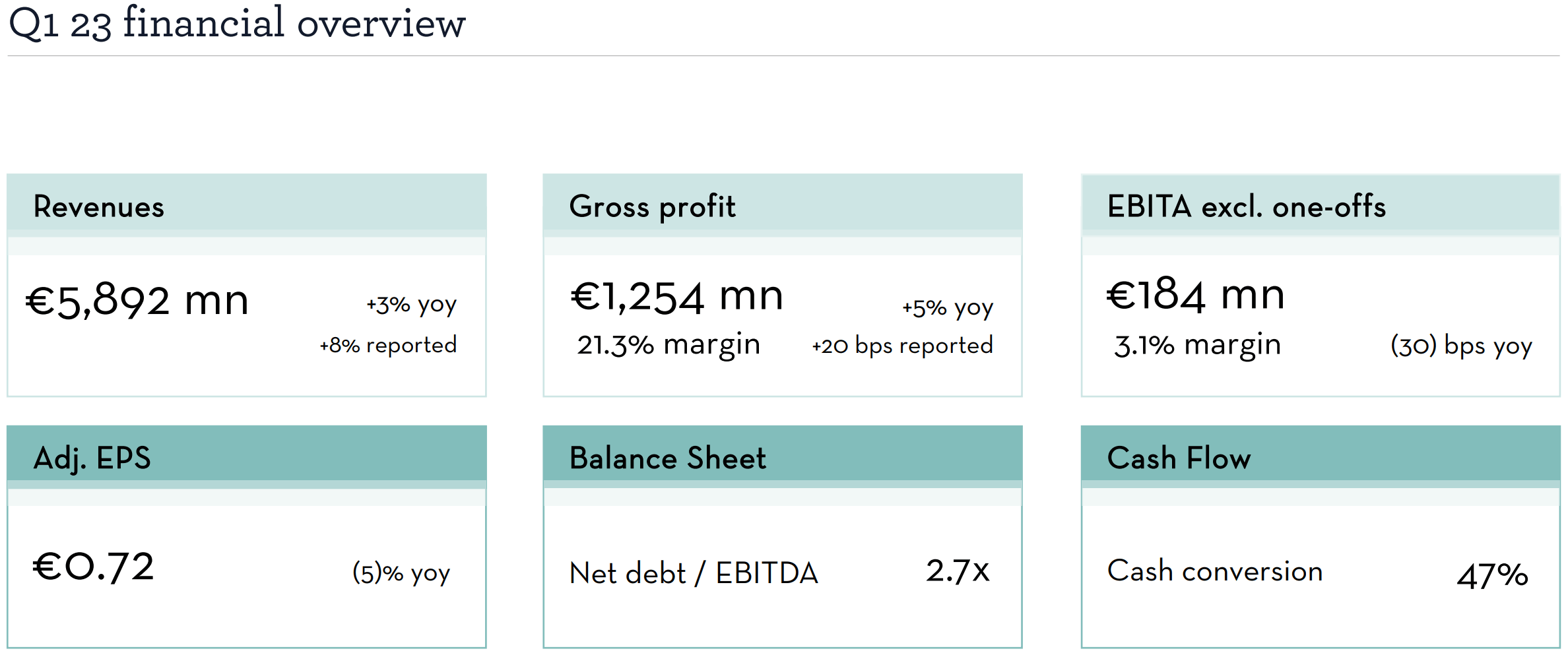

The Swiss company reported a 3% growth YoY with a gross profit that reached a record-high of 21% which is higher than Manpower's (18%) and equal to Randstad's. However, as we move towards the bottom line, Adecco still seems not as efficient as its peers (we know the company is engaged in a big turnaround effort to become more profitable and more able to start growing once again). In fact, Manpower's EBITA margin is 3.3% vs. Adecco's 3.1%. Randstad once again leads with a 4% EBITA margin.

But if we compare the three companies' profitability, we see that Adecco loses ground when we look at the net income margin (1.42% vs. 1.85% for Manpower and 3.18% for Randstad) and, more importantly, when we consider the return on equity. Here, Adecco has a return just barely above 8%. Manpower has a ROE of 14.21% and Randstad a much higher (and more interesting) 20.19%.

If we look at the return on total capital, the picture doesn't change. Adecco is lagging behind with a 5% vs. Manpower's 10% and Randstand's 13%.

During the last earnings call , Adecco's management repeatedly argued how the company's turnaround has started thanks to headcount reduction (yes, even staffing agencies have to reduce their workforce) and big contract wins. However, I could not help but notice a few facts investors should be aware of.

First of all, Adecco's gross profit comes for around 50% from flexible placement and only 25% comes from less cyclical or countercyclical services.

This means that Adecco is not immune from the market cycle. Actually, staffing agencies work very well both in tight labor market conditions and when the economy slows down a bit. In the latter situation, in fact, many companies still need workers but are unwilling to hire them directly. Therefore, staffing agencies come into play. The picture becomes difference if a recession becomes severe.

In Europe, Adecco reported that sectors such as automotive, health care, IT and manufacturing are performing well and have an overall growing demand for employees. At the same time, logistics and construction are currently softer industries. This is no surprise, since these are among the first sectors to be hit by a restrictive monetary policy. On the other hand, automotive and manufacturing are sectors with such a huge backlog covering most of 2023 and, in some cases, part of 2024, too.

There are some differences among the regions, with northern Europe seeing already a lower manufacturing activity, as well as Benelux.

But Adecco's Achilles' heels is North America. Here revenues decreased 8% YoY and management had to reduce headcount by almost 10% at the end of the quarter.

Wage and fee inflation

Now, overall, I see a company whose growth seems to be picking up again a little. However, a 3% growth in this industry is something we need to look at carefully. As some analysts pointed out during the earnings call, given wage and fee inflation which have a direct impact on revenue growth, we can actually grasp how Adecco's volumes were surely down YoY. This is because, as Adecco's management admitted when questioned, wage and fee inflation is running low- to mid-single digits. This means it should be around 5%, which is more than the 3% organic growth reported. This implies that volumes were down with a negative impact of at least 2 percentage points on the overall revenue growth.

Let me explain this with an example. Companies such as Adecco work mostly in the following way. When they are able to place a worker in a company, they earn a fee which is usually a percentage of the annual salary the company agrees to pay to the new employee. So, if we are in an environment where wages are going up, Adecco's fees will go up as well. This growth, however, is not really an organic growth since it is linked to a labor market dynamic Adecco has little control over. For clarity's sake, let's make up a helpful example.

Let's imagine that Adecco was usually able to place a worker with a $50,000 annual salary earning a 5% fee on this, which is $2,500.

Now, that same position can't be filled unless a company is willing to pay $55,000 to the employee. Without doing anything, Adecco automatically sees its revenue from this fee grow by 10%, to $2,750.

This means that if Adecco is able to keep its volumes stable, it should report a revenue growth of around 10%, at pace with wage inflation. Anything below 10% would mean that Adecco is signing less contracts and, therefore, it is seeing lower volume. On the contrary, if Adecco were to report a revenue growth above 10%, it would mean that, on top of wage inflation, Adecco's growth should be linked to volume growth.

Now I think is clearer why a 3% growth is not satisfying when wage inflation is around 5%.

Risk: LT debt and dividend support

Adecco's balance sheet, as we already said above, is more levered than its peers due to its recent attempt to start growing through M&As. At the end of the quarter, the debt-to-EBITDA ratio was at 2.7x.

This leverage stems from the acquisition of AKKA. Now, even though we are close to the 3x threshold, I don't think Adecco is in danger. In fact, the group's interest costs are sustainable with 78% of net debt fixed at rather low rates.

However, with the company committed to lowering its debt, much of its cash from operations will be directed to this. The consequence is that one of Adecco's appeals - the 6% dividend - may not be as supported as before, with the possibility of seeing a dividend cut in 2024. During Q2, Adecco will pay around €400 million to its shareholders and this will also increase the net-debt-to-EBITDA ratio.

This may cause some volatility in a stock where institutional investors own around 50% of the company. Since Adecco is not yet generating a strong enough growth to create substantial capital appreciation, the dividend becomes part of the investing thesis for many institutions aiming at owning "safe" stocks yielding more than bonds.

If the dividend is cut, we may see some institutions exit or trim the position and this usually leads the other institutional investors to do the same.

Conclusion

Considering Adecco's is trading at a PE of 14, above Manpower's 11 and Randstad's 10 and that the price/FCF ratio is 13 for Adecco, while Manpower trades at an 8 and Randstad at a 7.8, I think the company is still not a bargain. In fact, the company still needs to prove it will be able to turnaround its operations with better efficiency and renewed growth. Until then, I see no reason to pay a premium for this stock. Therefore, I keep my sell rating until further signs of an improved situation.

For further details see:

Adecco: Growth Rate Insufficient At Closer Look, Maintain Sell