RANJF - Adecco's Turnaround May Have Begun

2023-09-14 12:05:21 ET

Summary

- Adecco has been lagging behind its peers for a decade.

- Recent results make me reconsider my sell rating because of some improving metrics.

- Though growth has picked up speed once again, there are a few issues investors should consider before jumping into a stock that has raced up 30% since May.

Introduction

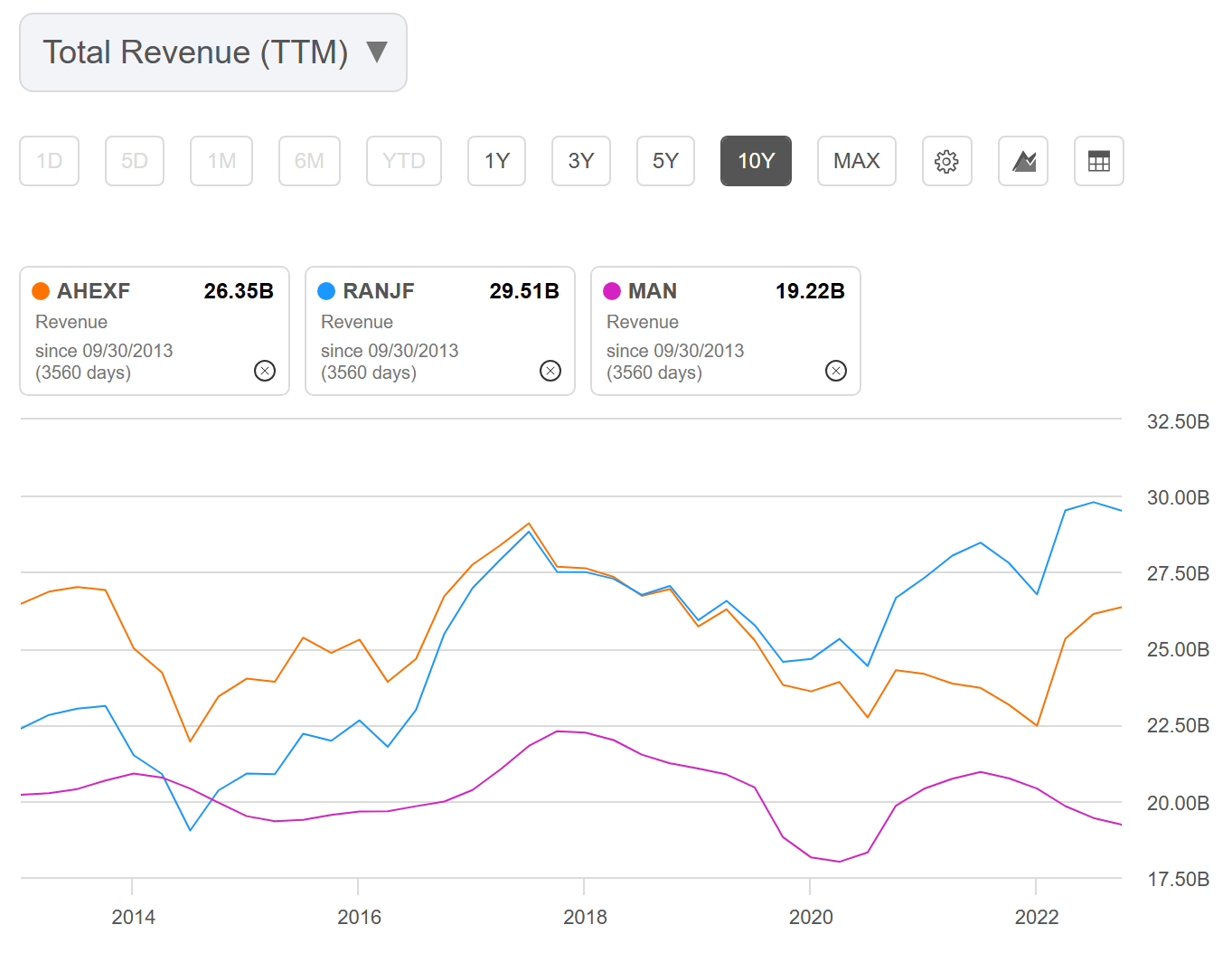

Last month, Adecco ( AHEXF , AHEXY ) reported earnings.

Even though I have been an Adecco bear for the past year, considering it an underperformer compared to the industry leader Randstad ( RANJF , RANJY ), I have to admit this report may mark an inflection point for the Swiss company.

Summary of previous coverage

The HR services industry is highly competitive and fragmented. Don't expect to find double-digit margins here. At the same time, it is very lean, having almost no need for big capex. In addition, it is a good proxy for the overall economy and this is why, together with railroads, I always look at this industry to understand what is really happenings around the globe.

As far as my take on Adecco goes, my main concern was that the company had been stagnating for more than a decade while its Dutch competitor Randstad was able to grow up to the point it became the leading company around the world.

{kind=link}

In particular, despite I was willing to accept flat top-line growth, it was not acceptable to see in what range Adecco's margins were being reported. We ended up with an EBITA margin just above 3% when Randstad was above 4%.

With a weakening economic outlook, I didn't see the imminent future so bright for companies in this industry. Being Adecco the worst performer, I said I wanted to see true signs pointing in the direction of improving how the company was managed.

Turnaround quarter?

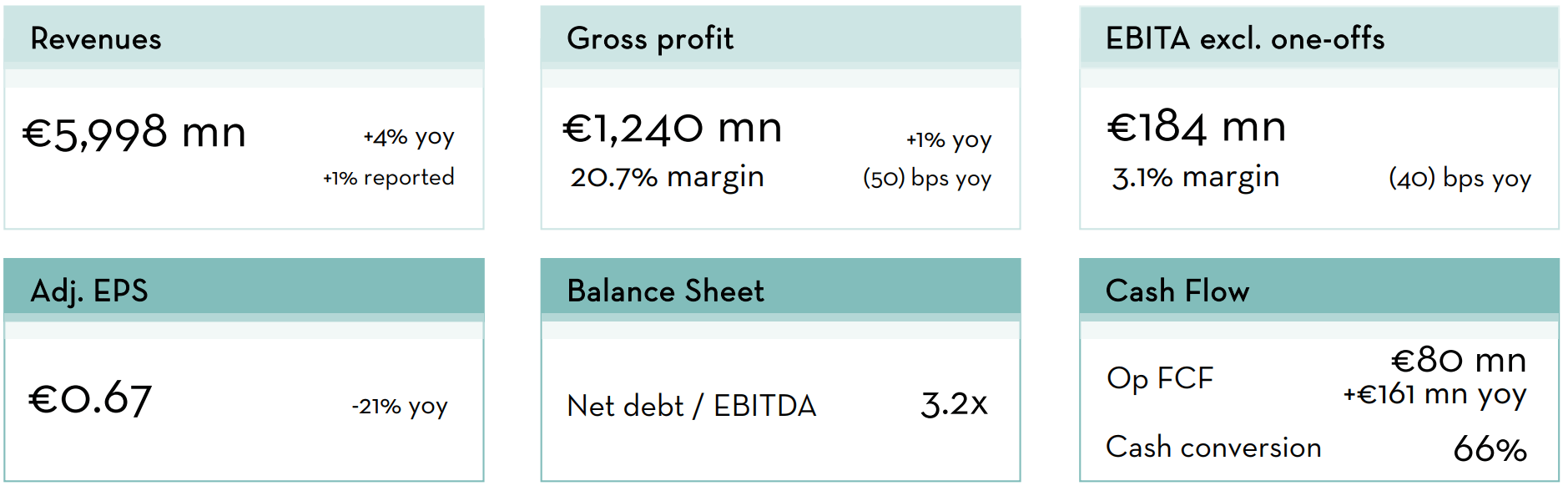

Well, if we look at the main financial highlights, we see a mixed picture.

{kind=link}

Positive metrics:

- Revenues up 4% to €6 billion.

- Gross profit up 1%.

- Operating FCF increased by €161 million YoY.

Negative metrics:

- EBITA margin of 3.1%, down 40 bps YoY.

- EPS down 21% YoY.

- Net debt/EBITDA ratio of 3.2x vs. 2.7x just a quarter ago.

In particular, if revenues grow, but EPS don't, the explanation is clear: the company's operating efficiency is not able to make each dollar of revenue earned more and more profitable.

Now, during the earnings call, Adecco did break down further what is driving growth and what is lagging behind.

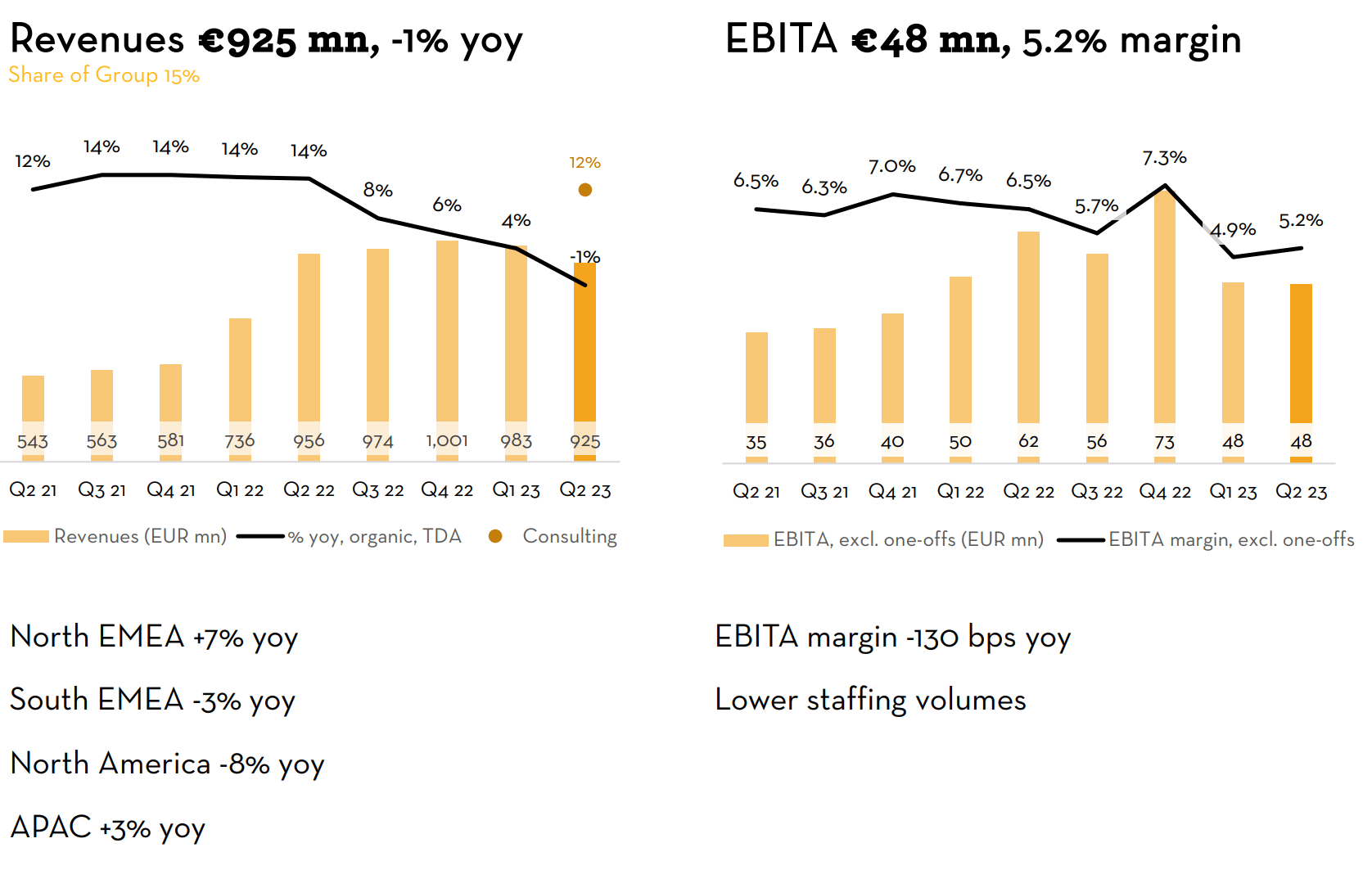

Here we see how Akkodis, whose focus is on engineers and digital experts, is experiencing the bite of tech talent downturn, with decreasing revenues and margins still not above 6.5%.

{kind=link}

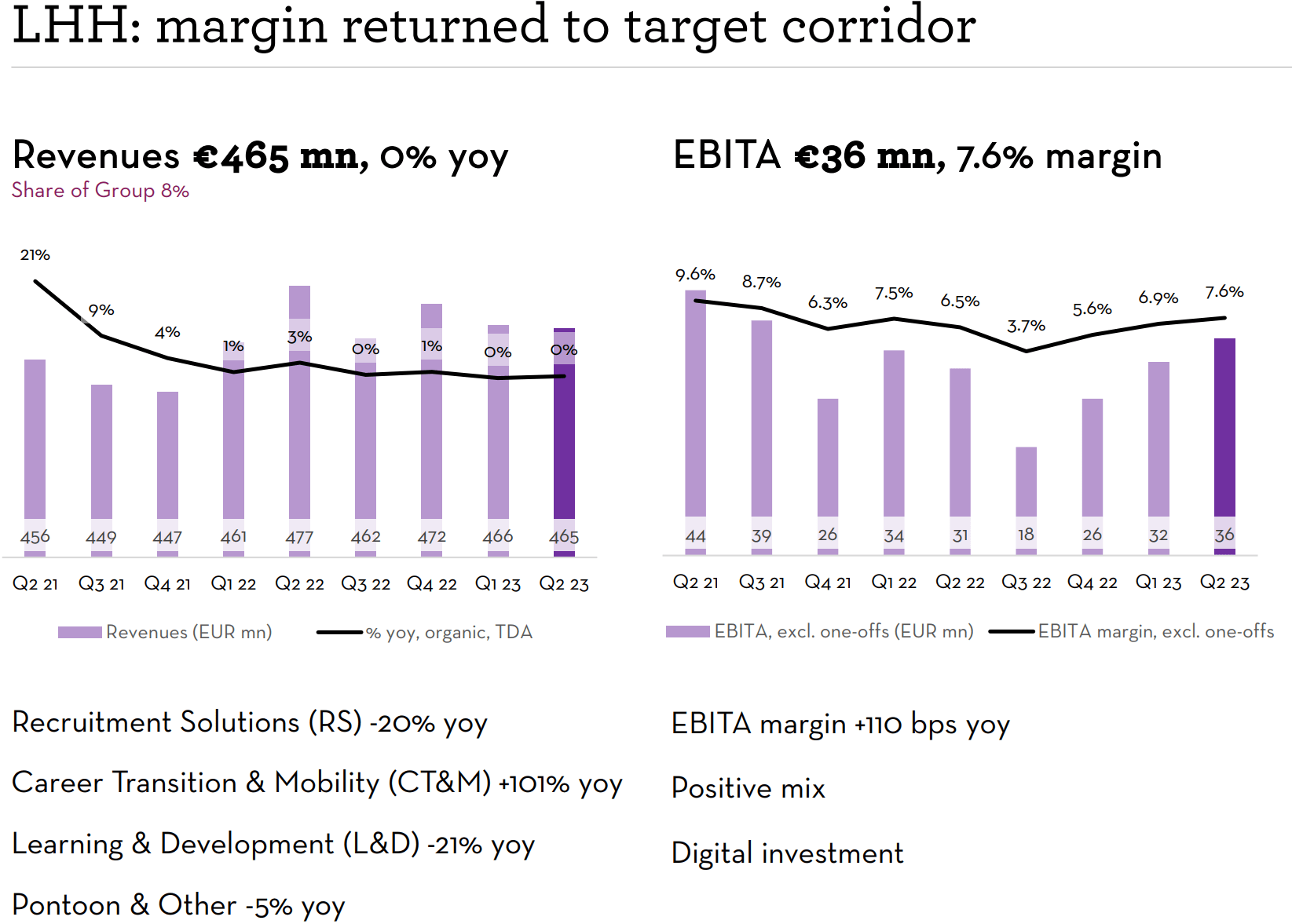

On the other hand, LHH, which provides services to reskill and upskill the workforce, has been able to bring up its margins, though it hasn't seen revenue growth for a while.

{kind=link}

This shows how "the market for talent services was mixed in the past few months. This is no secret, as layoffs have been going on for a while. But what I found very interesting during the earnings call were some words outlining how Adecco is thinking of this part of the cycle as truly a downward turn, where countercyclical careers benefit the most:

Performance in countercyclical career transition was excellent. Revenues rose 101% driven by positive momentum globally and across multiple sectors. Supported by more systematic cross-sell between recruitment solutions and career transition, new logo wins were very strong, accounting for nearly 20% of business activity in the quarter. The segment continued gaining market share, particularly among SMEs and achieved record revenue levels. Its pipeline is solid.

A solid pipeline for countercyclical careers means that we will see some tough months, economically speaking.

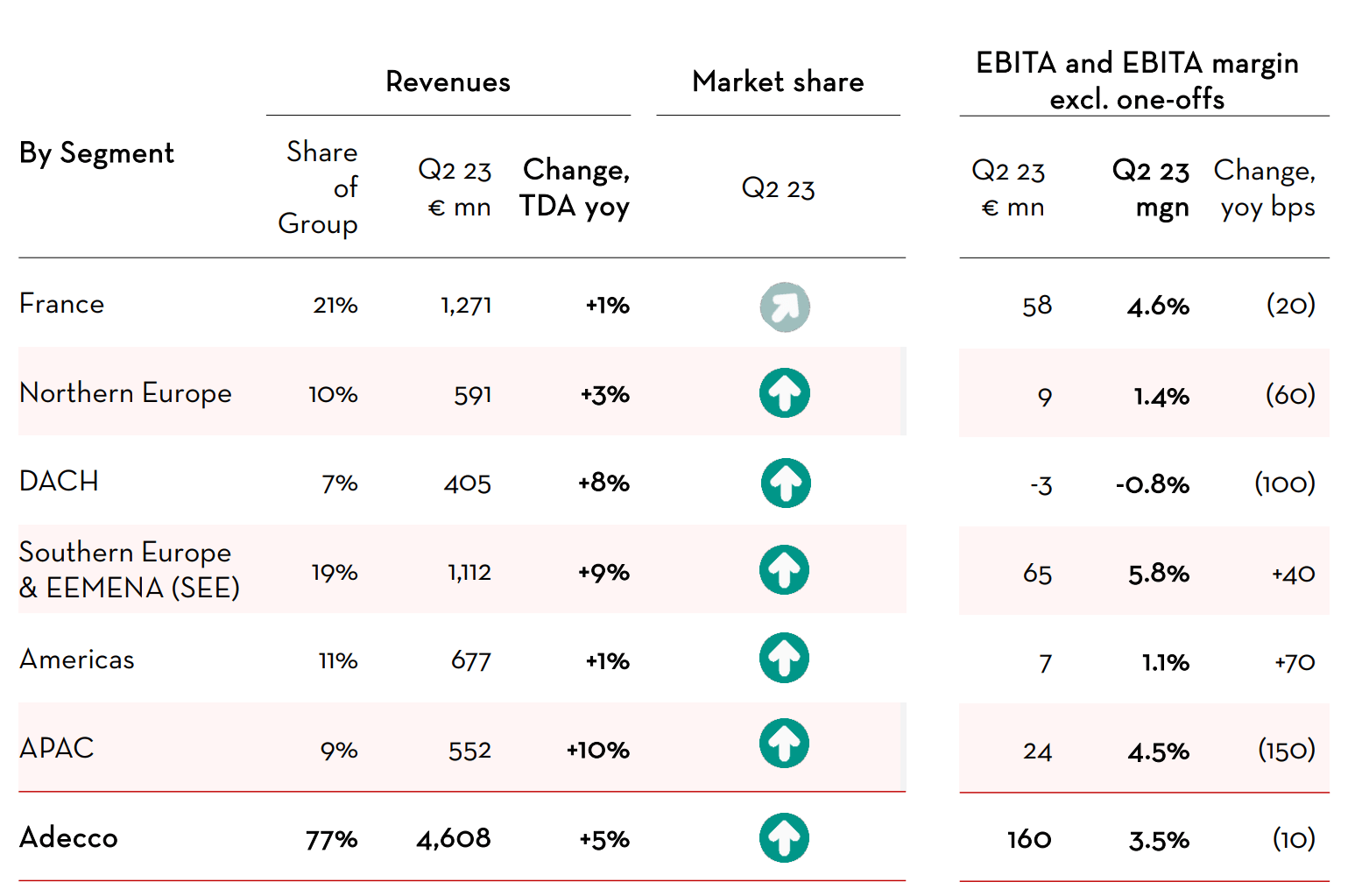

Let's take a look at how Adecco itself performed in its key markets.

{kind=link}

Here some good news appear in a clear way: Adecco gained market share in its key markets. In particular, it performed well where manufacturing (especially automotive) and health care are strong. Logistics, construction, and retail were, on the other hand, soft.

While Adecco performed well in Europe, North America showed a different picture. Here revenues were 8% lower, due to the sharp reduction in staffing activity for tech talent.

Since many are expecting a recession, Adecco reported that "people are a bit less keen in investing for themselves", but that many are just postponing this investment until better visibility on future trends is gained. Therefore, in the next few quarters, we should expect Adecco to achieve results more or less in line with what we have seen in Q2. At the same time, upskilling and reskilling services, which have better margins than simple staffing, should gain new traction by 2024.

Ironically, Adecco itself, a staffing company, had to cut its headcount in North America by 15% to create a more efficient and frugal business.

This leads us to the main issue Adecco is internally facing. While revenues seem to be picking up some speed showing finally decent growth, Adecco has constantly reported poor efficiency in how it manages its internal costs.

In fact, SG&A expenses rose to over 4% of revenues. To address this issue, Adecco announced back in November it was targeting €150 million net G&A savings. During the earnings call, Adecco informed investors about this program and where it is at now:

Following a series of GBU, countries and functional workshops, the group has identified the actions required to deliver savings that will bring G&A expenses as a percentage of revenues to below 3.5%. Of the identify actions, approximately 75% come from implementing a streamlined operating model. We are eliminating overcapacity, duplication and reducing the number of organizational layers. A further 15% comes from optimizing shared functions, for example, by shifting administrative activities to shared services, mutualizing enabling functional resources across GBUs and leveraging near and offshore resources. And around 10% of savings come from consistently taking a highly frugal approach to expenses including travel and entertainment costs, real estate and outside services.

Therefore, Adecco wants to achieve a savings run rate of €60 million by year-end, while it will reach its target of €150 million by mid-2024. This means that Adecco should see SG&A come down by approximately 1.5% this year. These savings should all be seen in the reported operating income where they would make up almost an extra 10%. This will clearly be a crucial point to see if Adecco is going to raise its margins too.

But I clearly see the savings program with a positive note, having repeatedly said Adecco wasn't focused on running its business with a focus on its costs.

In addition, I think the move to keep on hiring salesmen is paying off as revenues are increasing while overhead costs are going down.

One word on the higher leverage: Adecco paid its annual dividend. This makes Q2 usually a more leveraged quarter as per the balance sheet. By the end of the year, the company should be back at a 2.5x ratio. If it won't, then we might have a concern.

Conclusion

Many investors were able to anticipate these results and the stock has had quite a run since May, being up around 30%.

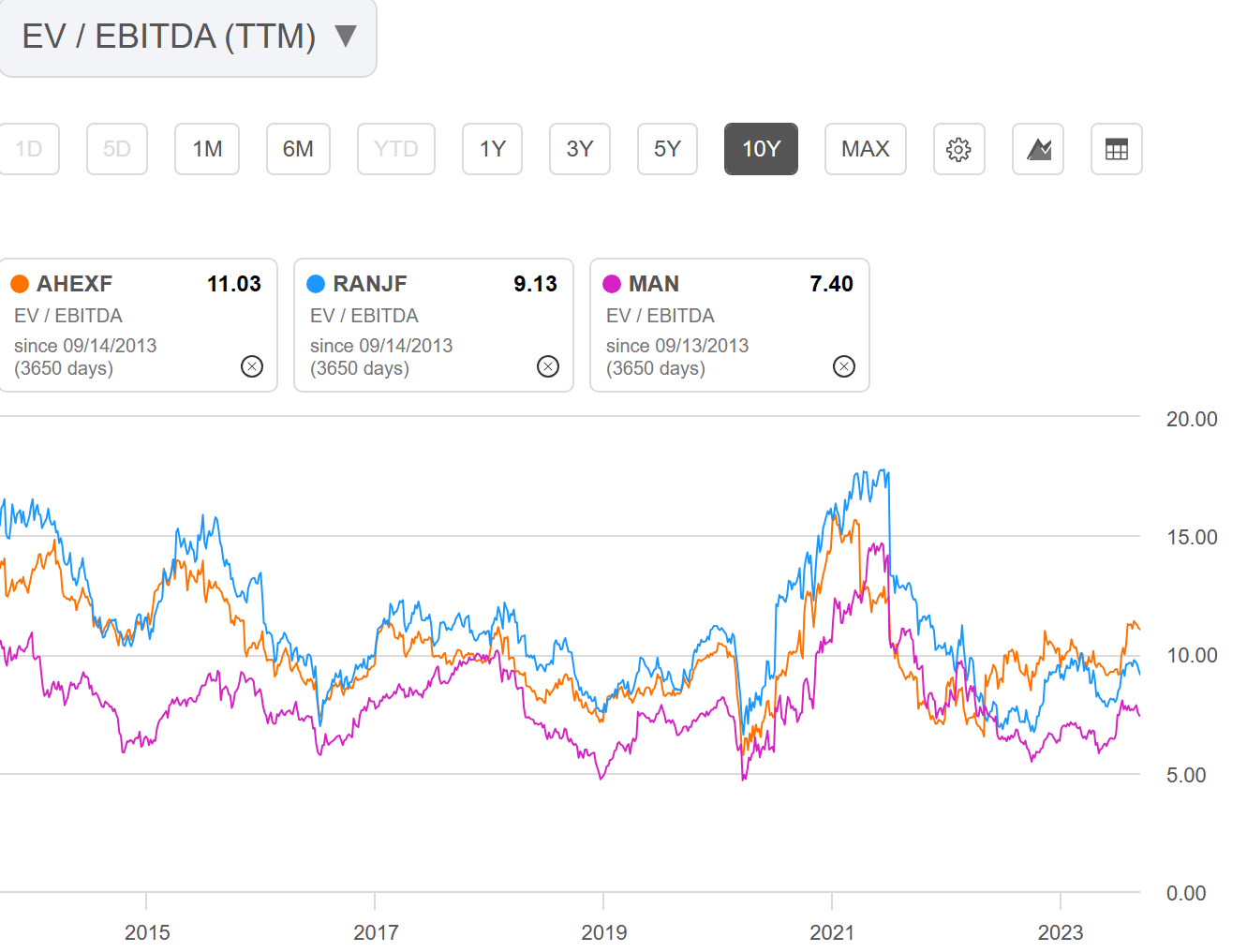

Given the last report, Adecco did give some indications about a trajectory it wants to walk to improve its economics. I thus see less concerning aspects compared to a few months ago. However, the stock seems to have run a bit ahead of itself, being now valued at a greater EV/EBITDA versus its main peers.

{kind=link}

Considering the industry may still see some weak quarters, I don't think this is the right moment to buy the stock. Yet, given the improvement in its fundamentals, I change my rating from sell to hold.

For further details see:

Adecco's Turnaround May Have Begun