AGRO - Adecoagro Hit Hard By A Weakening Outlook For Ethanol And Sugar Production

Summary

- Brazilian ethanol prices have been falling on sluggish demand and government efforts to bring inflation to heel, undermining margins for producers like Adecoagro.

- Current prices favor shifting production from ethanol to sugar, but I don't believe the sugar market can absorb the more than 4M potential incremental tons that could hit the market.

- Adecoagro's crop business isn't large enough to offset the hit to SEE profits, and weather, higher input costs, and lower commodity prices remain threats here.

- Management has shown a lot of flexibility in the past when it comes to managing commodity market challenges, and further expanding ethanol exports to the EU could mitigate some of the pressure.

- There is definitely headline risk where ethanol and sugar prices are concerned, and Adecoagro hasn't been a good long-term buy-and-hold name, but the valuation looks too low now.

Brazil’s Adecoagro ( AGRO ) is a good case-in-point that a commodity company can do everything right (or at least do many things right) and still see larger commodity and economic trends, and investor worries about those trends, undo that hard work. Adecoagro, for its part, as long been a low-cost producer of sugar and ethanol (or SEE) in Brazil, as well as a low-cost producer of grain and other agricultural products in Argentina, but it has meant basically nothing for long-term investors, as annualized returns over the last three, five, and 10 years is basically flat to negative.

I was bullish on the prospects for Adecoagro to leverage attractive energy, sugar, and crop prices into solid cash flow that would be returned to shareholders in the wake of completing a major multiyear investment program. While the company has indeed instituted a dividend and buyback, the shares are still down about 15% since that last update – outperforming Cosan ( CSAN ) and Sao Martinho , but still down (and worse than the performance of other ag names like Cresud ( CRESY ) and SLC Agricola ( OTCPK:SLCJY )).

The trouble with assessing Adecoagro today is that whenever you find yourself asking “how could it get worse?” with a commodity company, the market has an uncanny way of showing you just exactly how it could get worse. I do think that Adecoagro’s valuation is low, but with real concerns about ethanol and sugar prices over the next 12-18 months, as well as crop yields and profitability, this is a tough place to go bargain-hunting.

SEE Gets Sawed

Adecoagro, as well as other Brazilian SEE producers is looking at some difficult choices in the year to come with respect to sugar and ethanol production, as both markets are having their own problems. It does help some that Adecoagro has among the lowest production costs in Brazil and high flexibility to shift between ethanol and sugar, but there’s only so far these advantages can go.

Ethanol prices have been weakening in Brazil since the spring, hurt in part by oversupply and government efforts aimed at reducing the cost of fuel for citizens. Brazilian hydrous ethanol prices started 2022 at $0.59/liter, rose to over $0.80/liter in April, and then headed steadily lower through the rest of the year, ending the year at around $0.55/liter. While producers had hoped to get some respite with the reimposition of gasoline taxes, President Silva announced last week that he would extend the tax break for at least another 60 days and concerns remain that the government may seek to curb fuel price volatility by imposing price caps.

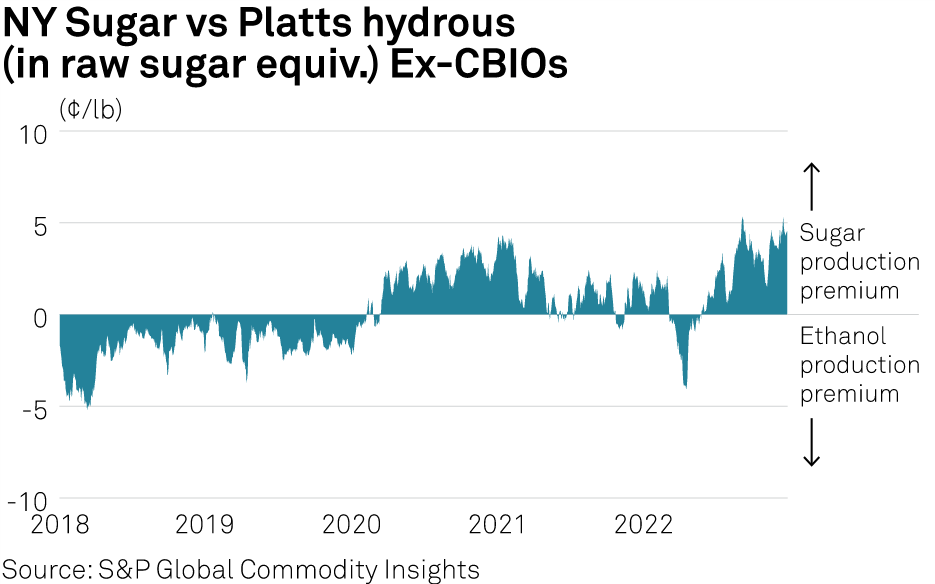

With weaker ethanol prices (below the cost of production for at least some SEE participants), producing sugar now looks like the better bet, and indeed the premium for sugar production has hit a multiyear high.

{kind=link}

Unfortunately, the sugar market looks to be in a somewhat precarious balance. Sugar prices (the #11 contract) are still pretty healthy at $0.196/lb (compared to a range of around $0.147/lb to $0.21/lb over the past two years), but between sugarcane acreage expansion and shifting away from ethanol production, the global sugar market could see a surplus of more than 4M tons, and that’s before considering the impact of good growing seasons in areas like Thailand. While the Indian government’s decision to limit exports (likely to between 8Mt and 10Mt) does help, I do see a risk of weaker sugar prices over the next 12-18 months as Brazilian producers shift production.

Adecoagro has only limited options – the company, like other SEE producers in Brazil, looks to be squeezed between weaker ethanol prices and precarious sugar prices. Management has been actively hedging near-term sugar production at attractive prices, but those hedges will roll off eventually. One positive is the export market – the company has been active in exporting ethanol to markets like the EU (about 20% of recent production), and prices there are about 15% higher than in Brazil.

Crops Can’t Really Cushion The Blow

Adecoagro’s farming business isn’t really capable of offsetting weaker earnings from the SEE business. The company’s farming operations in Argentina are fairly efficient as global standards go, but the business accounts for only about 20% of total EBITDA in a given year and that’s really not enough to offset weaker realized prices for sugar and/or ethanol.

Moreover, it may be premature to assume a great year for the crop business. The company has seen a hit to yields from adverse weather in recent years (they’re not the only ones, it’s a region-wide problem), and there’s still a risk of further droughts this year. On top of that, production costs are higher (the cost of fertilizer, labor, and other inputs), further pressuring margins, and while grain prices have held up, the current outlook in the futures market is for soy prices to head about 5% lower and corn prices to head about 10% lower.

The Outlook

Maybe it goes without saying that there are a host of difficult-to-forecast drivers that play into Adecoagro’s outlook. Weather is notoriously unpredictable, and while a better-than-expected growing season would be good for grains, it would likely also increase sugarcane yields and add more supply pressure to the ethanol and sugar markets. Likewise, there are numerous other drivers of ethanol prices in Brazil, including Brent crude prices, the U.S. dollar – Brazilian real exchange rate, economic growth in Brazil, and the tax and energy policies of the Brazilian government.

The best I can really say here is that I think Adecoagro is better-positioned than most – the company has low-cost SEE assets (as well as efficient, low-cost farming assets) and unusually high flexibility. Moreover, management has shown itself to be pretty skillful in managing harvesting, crushing, and ethanol/sugar production to maximize earnings. Those skills could well be put to the test over the next year or two.

I expect Adecoagro to finish 2022 with 9% revenue growth, with low single-digit annualized growth for a few years thereafter and long-term growth likely in the low-to-mid single-digits. The biggest risk here is that prices weaken even further, particularly sugar prices, but that is likewise a potential source of upside (upside seems more likely to me in ethanol than sugar). I expect EBITDA margins to fall from 39% in FY’21 to around 34% for FY’22 and then below 30% for a couple of years before recovering back into the mid-to-high 30%’s.

I do still expect the company to generate positive free cash flows, and that cash flow should fund further returns of capital to shareholders. I wouldn’t be shocked if management looked to be opportunistic and acquire SEE assets from stressed producers. I expect the market would hate that in the short term, but management has shown in the past that it is willing to ignore short-term sentiment in the pursuit of its long-term growth strategy.

Valuation is where things get a little complicated. My revenue estimates are below published Street estimates (about 5% to 10% depending upon the year) for the next four years, and my EBITDA and FCF estimates are likewise below the Street, but I still get a double-digit fair value on discounted cash flow. Using EV/EBITDA, a 5x multiple (on the low end of the company’s normal historical range) on my trough FY’23 estimate gets me a fair value of almost $10, and I’d note that usually commodity companies trade at higher-than-normal multiples on trough earnings.

The Bottom Line

I suppose one obvious conclusion is that the Street is pricing in an even more dire outlook for 2023-2024 than what I think are low estimates in my own model. I can’t rule that out, particularly as sugar prices could weaken significantly if several incremental tons of Brazilian sugar hit the market.

On the other hand, trading at below book value, I do find these shares interesting. This has been a tough place for buy-and-hold investors to make money, but I am fond of considering commodity names at cyclical lows and Adecoagro certainly seems to be under serious pressure today despite a bearish outlook that would still see relatively healthy margins and cash flow generation.

For further details see:

Adecoagro Hit Hard By A Weakening Outlook For Ethanol And Sugar Production