ADDDF - adidas: Better Than Expected Performance But Risks Remain

2023-11-28 02:52:39 ET

Summary

- adidas has seen contradictory trends YTD, with muted financial performance but 45% price gains on better than expected performance.

- The company expected a big setback after it let go of rapper Kanye West last year, its partner for Yeezy, coupled with ensuing macroeconomic challenges. But things have not turned out as badly as expected.

- The forward P/E ratio for adidas is currently sky-high but 2023 needs to be seen as an outlier year. If it goes back to normal in 2024, it could potentially be a Buy.

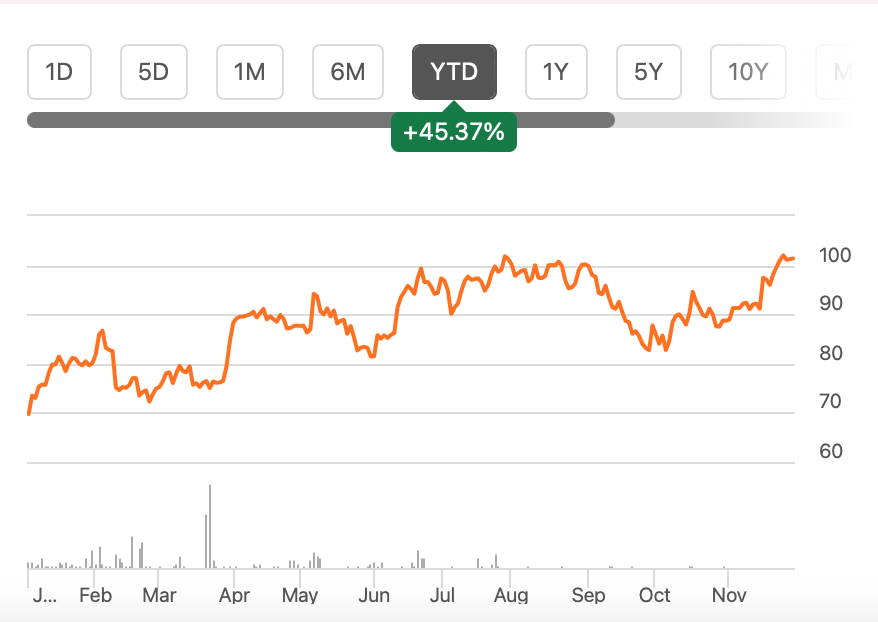

Here’s something puzzling about adidas ( OTCQX:ADDYY ). The popular German sports products company has seen very muted sales and profits so far this year. But its price is on the rising curve, up by no less than 45% year-to-date [YTD].

{kind=link}

Now here’s the real rub. The combination of challenged performance and a price increase has resulted in a non-GAAP forward price-to-earnings (P/E) ratio of no less than 402.75x. This, of course, is far in excess of the 14.8x ratio for the average consumer discretionary stock. But it’s also way higher than the company’s own five-year average of 62.17x.

So what’s still making adidas tick? That is the real question here.

Improved forecasts

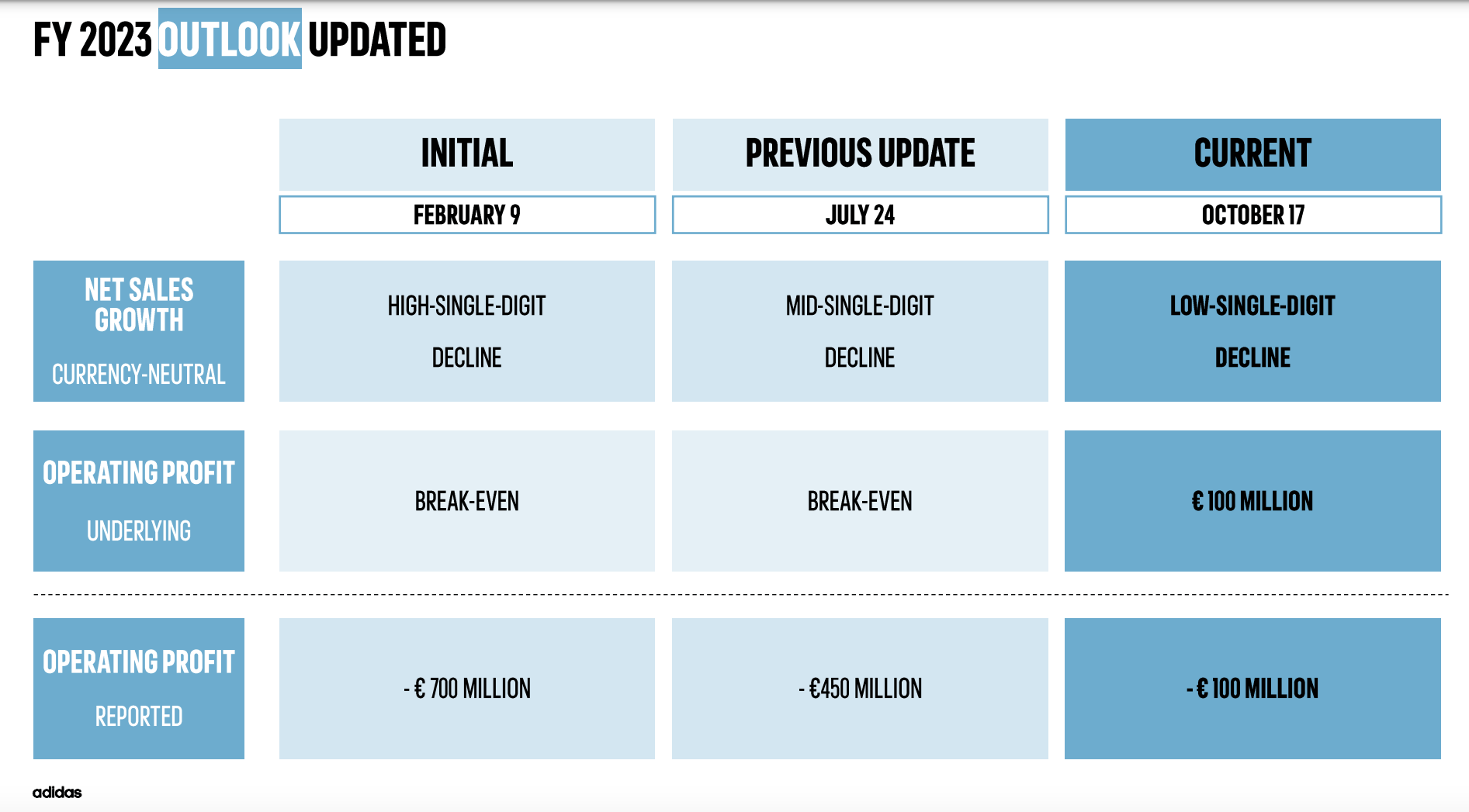

To put it succinctly, and in the company’s own words, “we improved our outlook every quarter”. It made the statement along with its recent third quarter (Q3 2023) results, where it now expects “currency-neutral revenues to be down only low single digits” and a “small operating loss of € 100 million”. This isn’t a positive outlook by any stretch, but it does deserve some context.

The company’s big unexpected problem arrived late last year, when superstar rapper and its partner for the Yeezy brand, Kanye West, was let go for antisemitic remarks. This in turn knocked off EUR 250 million from adidas’s net income in 2022, which was already impacted by a weak China market on COVID-19. The estimated amount was not an insignificant 11.6% of the profits the year before.

{kind=link}

The company was already cautious because of the expected slowdown in Europe and North America and persisting uncertainties about China. The initial outlook for 2023 was further dimmed as a result of the Yeezy impact.

It expected an EUR 1.2 billion revenue loss on Yeezy’s account, which amounts to 5.3% of the company’s net sales in 2022. This in turn translated into expectations of a decline of a “high-single-digit rate” for currency neutral revenues. It also expected a reporting operating loss of EUR 700 million. For reference, it clocked a EUR 669 million operating profit in 2022.

Clearly, it has come a long way since the start of the year, even expecting an underlying operating profit now.

Better than expected sales

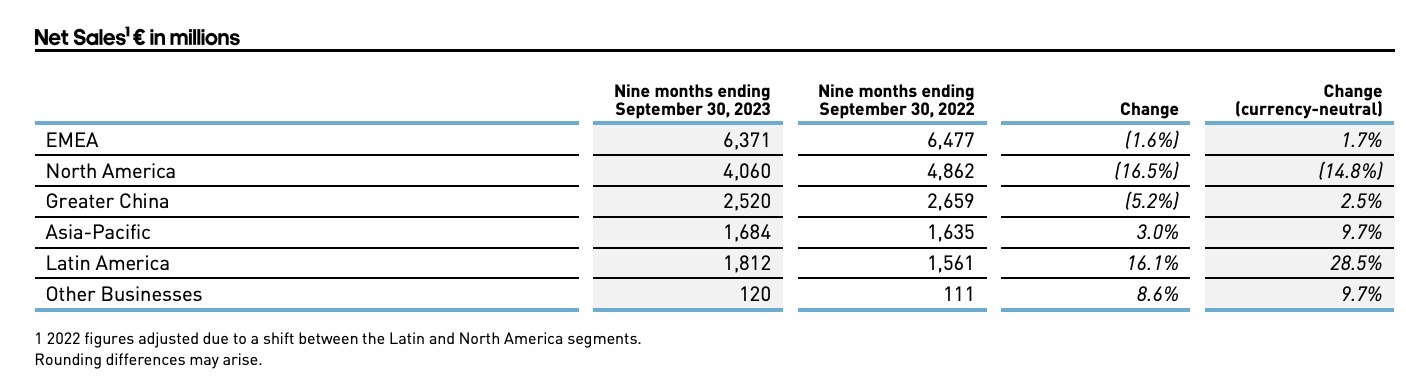

Underpinning the company’s improved outlook, of course, is its better than expected performance so far this year. For the first nine months of 2023 (9M 2023), currency neutral revenues have remained unchanged from the prior year and in the third quarter (Q3 2023) it actually saw 1% year-on-year (YoY) growth.

adidas did run out of luck as far as exchange rate movements go, though, resulting in a 4% decline in net sales during the year. This is also reflected in a revenue contraction across geographies.

At the same time, it's notable that it was able to sustain currency neutral revenues despite the fact that its performance in North America has been severely affected (see table below). Double-digit growth in Latin America and healthy growth in Asia Pacific, however, were positives on a currency neutral basis. Despite initial concerns about the macroeconomic situation in Europe in 2023, growth in the EMEA region continued to be positive as well, albeit significantly below the full-year 2023 growth of 8.8%.

{kind=link}

Source: adidas

Limited profit impact

But perhaps the most heartening aspect is the EUR 646 million of operating profits adidas has managed to clock, despite dire warnings in its initial outlook. The number is less than half the EUR 1.4 billion seen for 9M 2022, but it is very close to the EUR 669 million seen for the full year 2022, as adidas fell into a significant EUR 724 million loss in Q4 2022.

The company’s operating margin at 3.9% for 9M 2023 is actually improved from the 3% levels seen in 2022. The net income margin, however, lags behind at 2.1% compared to 2.8% in 2022. But this is essentially on account of gains from discontinued operations last year, which don’t come into play this year.

The explanation for the forward P/E

For the full year, though the company still expects to post an operating loss, on account of seasonality in Q4. This presumably would translate into a net loss for the full year as well. However, it does expect an underlying operating profit of EUR 100 million, which converts to USD 109 million.

Assuming the ratio of net profit attributable to shareholders to operating profit remains constant at 91.5% in 2023, the same as in 2022, the underlying net profit would amount to just under USD 100 million. This in turn results in a forward non-GAAP P/E of 361.4x. It’s nowhere close to as high as the average of analysts’ estimates, but it’s definitely closer to it than to the average for the consumer discretionary sector.

The key point here really is that the forward P/E for 2023 doesn’t count as it has been an outlier year for adidas. It’s only next year that the forward P/E will reflect the true valuation of the stock or its ADRs. For 2024, the forward P/E is at 24.1x, which isn't low either, incidentally. But it does compare favourably with its peer NIKE ( NKE ), which has a forward P/E for the year ending May 2024 at 29x.

What next?

I would, however, let the adidas story play out for another quarter for now. The reason is that it’s not just Yeezy that has impacted its numbers, it’s also the weakening macroeconomic fundamentals in key markets like North America and Europe. I find trends in North America particularly concerning, considering that it’s not just adidas but a host of other consumer discretionary companies that have reported recent weakness in the market.

The US economy might be in better shape with inflation softer and the let-up in interest rate hikes can be a relief for consumers, but there can still be a lagged impact on the health of the economy from these recent challenges. And if adidas's and other companies' latest numbers are anything to go by, we shouldn’t take growth in the US for granted. The same holds for Europe.

I’m going with a Hold on adidas for now. If its outlook for 2024 is positive, it would be Buy, assuming its price stays where it’s at right now. But that remains to be seen.

For further details see:

adidas: Better Than Expected Performance, But Risks Remain