NKE - adidas: Buy The Dip

Summary

- adidas shares plunged by as much as 10% following a profit warning for Q3 results, as well as a lowered guidance for the FY 2022.

- adidas estimates that profits in 2022 will be about 60% lower than what has previously been expected.

- The company said that sales in China declined at a "double-digit rate," citing covid-19 restrictions as a major headwind.

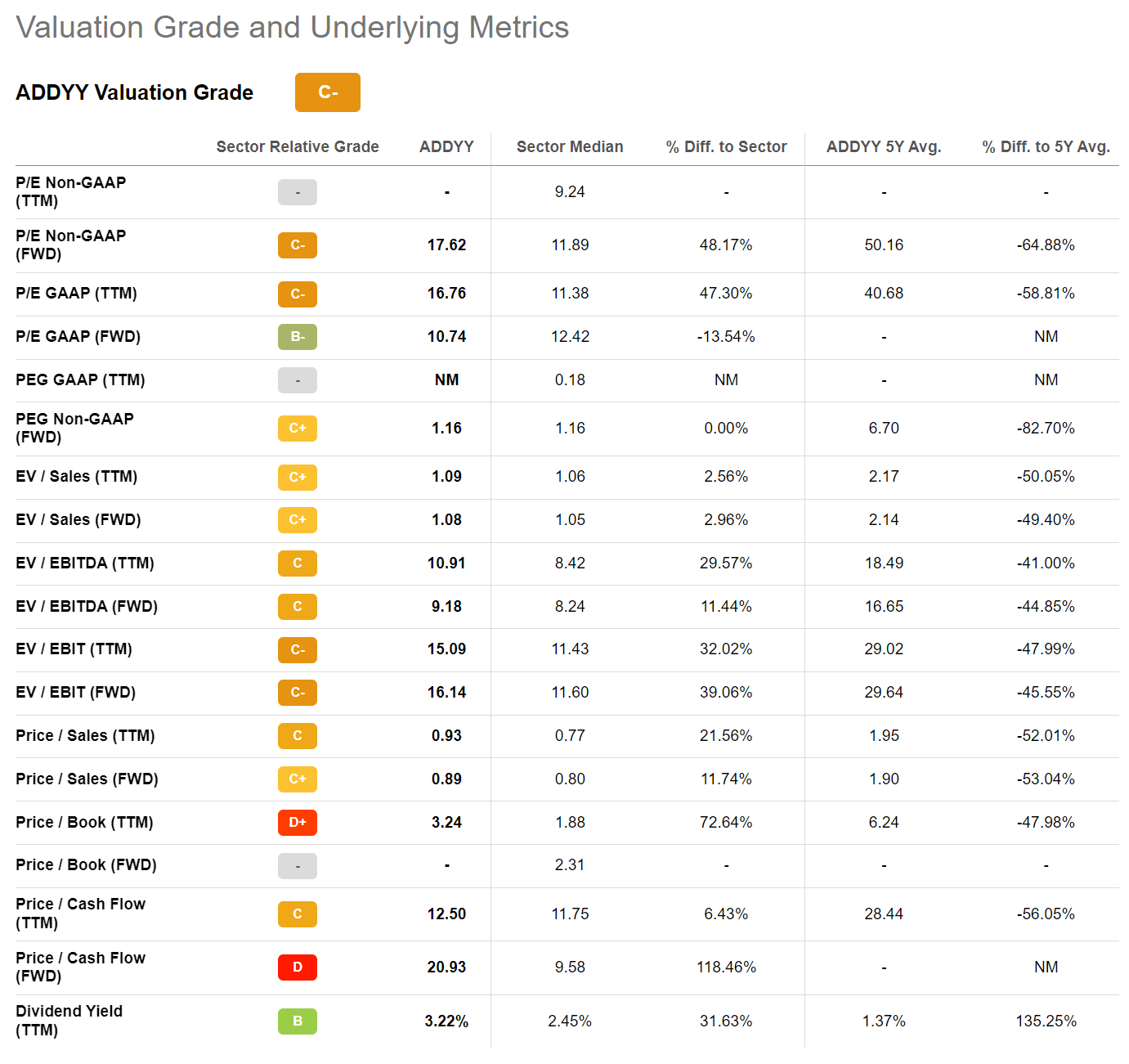

- Following a 60.5% sell-off YTD, adidas shares are trading very attractively - valued at an EV/EBIT of about x15 and an EV/Sales of x1.1.

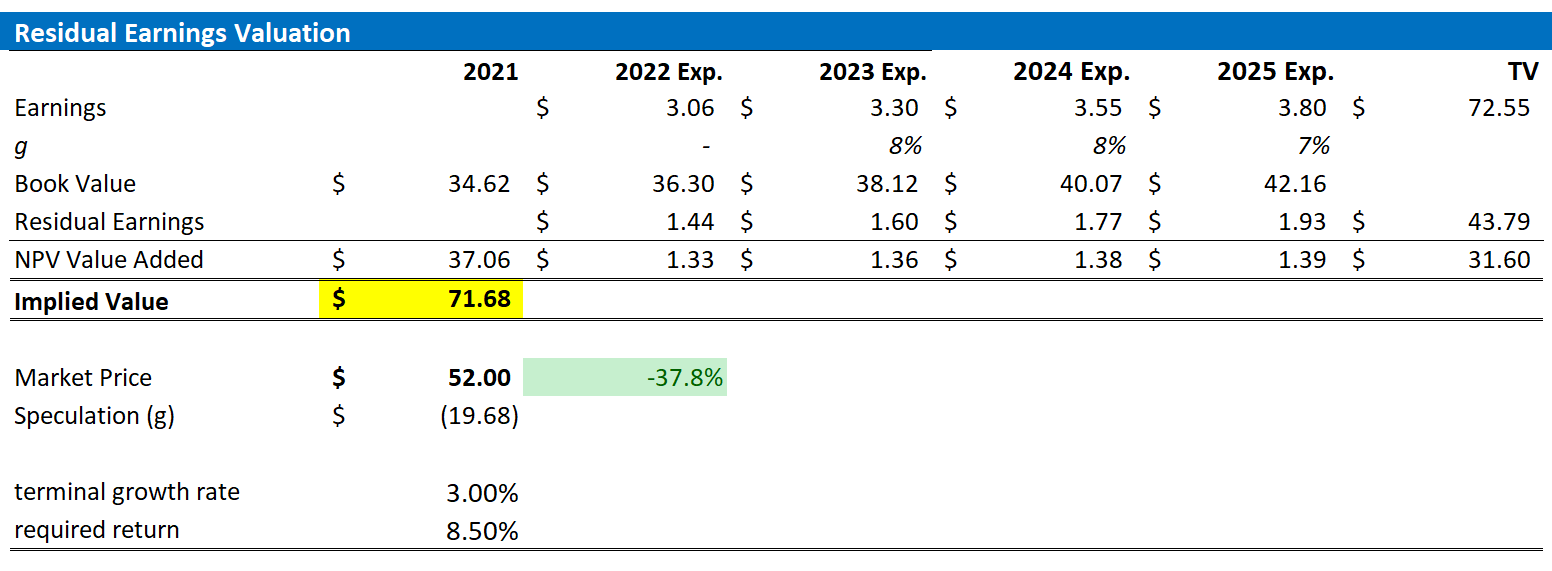

- Long-term investors might like to see through the short-term noise, and I target a valuation for ADDYY of about $71.68/share.

Thesis

adidas ( ADDYY , ADDDF ) shares plunged by as much as 10% following a profit warning for Q3 results, as well as a lowered guidance for the FY 2022. As a consequence of a challenging outlook in China, paired with a slowing demand environment in western economies, adidas estimates that profits in 2022 will be about 60% lower than what has previously been expected.

The adidas profit warning is certainly difficult to stomach. But investors should consider that the company's stock has aggressively derated YTD - being down 60.5%. And the valuation , priced at a x16 EV/EBIT, is surely attractive from a relative perspective as compared to Nike (NKE) and/or Lululemon (LULU).

adidas Profit Warnings

On October 20th, adidas unexpectedly announced worse than estimated Q3 results and lowered guidance for the FY 2022 profitability.

Preliminary Q3 Results

adidas preliminary Q3 results estimate that revenue growth for Q3 slowed down to 4% (year over year reference). The company said that sales in China declined at a "double-digit rate," citing covid-19 restrictions as a major headwind.

Absent any currency fluctuations, adidas revenues would have increased by about 11% year-over-year, to €6.408 billion. With regards to profitability, the sportswear group said that gross margin declined by about 1% versus the same period one year prior, to 49.1%. Respectively, operating profitability declined by about 2.9%, to 8.8% (versus 11.7% in Q3 2021). Moreover, as an additional pressure on profitability, adidas highlighted a total €300 million of one-off expenses, including a major write-down relating to adidas's operations in Russia, as well as " a recently settled legal dispute and higher provisions for customs-related risk."

adidas expects that net income in Q3 will be around €179 million, which would indicate a 60% compression versus the same period in 2021, when adidas generated net income of €479 million.

Weaker Than Expected FY 2022

adidas aggressively marked down its full year guidance for 2022. As compared to "mid- to high-single-digit" previously, management now expects a year over year sales growth in the "mid-single digits," which is lower than inflation in adidas' home country, Germany.

The lower topline guidance is accompanied by a margin compression. Gross margin is estimated to contract to approximately 47.5% (versus previously guided 49.0%), and operating margin is expected to contract to 4% respectively (versus previously guided 7%).

That said, net-income for the FY 2022 is likely to drop to €500 million, which is about €800 million lower than what the company previously estimated.

As the major reasons for a depressed FY outlook, the profit warning states (emphasis added):

The company's new outlook takes into account a further deterioration of traffic trends in Greater China as well as a significant inventory build-up as a result of lower consumer demand in major Western markets since the beginning of September

adidas said that as a consequence of the above mentioned developments, the company is likely to push " higher promotional activity during the remainder of the year ," which obviously implies a low margin product sale.

Valuation Is Attractive

While I understand the negativity surrounding the profit warning, I argue that every investment thesis must be considered in relation to valuation. And following a 60.5% sell-off YTD, adidas shares are trading very attractively.

adidas is currently valued at a EV/EBIT of about x15 and a EV/Sales of x1.1. This compares very favorably to Nike, which is valued at x3 EV/Sales x22 EV/EBIT, and to Lululemon, which is trading at x4.8 and x25 respectively.

So, an investor might consider that adidas' U.S. peers are roughly valued at a 35% premium. This, in my opinion, is not justified - especially since Nike also has recently issued a profit warning .

{kind=link}

Residual Earnings Model

To derive a more precise estimate of a company's fair implied valuation, I am a great fan of applying the residual earnings model, which anchors on the idea that a valuation should equal a business' discounted future earnings after capital charge. As per the CFA Institute :

Conceptually, residual income is net income less a charge (deduction) for common shareholders' opportunity cost in generating net income. It is the residual or remaining income after considering the costs of all of a company's capital.

With regard to my adidas stock valuation model, I make the following assumptions:

- To forecast EPS, I anchor on the consensus analyst forecast as available on the Bloomberg Terminal 'till 2025. In my opinion, any estimate beyond 2025 is too speculative to include in a valuation framework. But for 2-3 years, analyst consensus is usually quite precise.

- To estimate the capital charge, I anchor on adidas' cost of equity at 8.5%.

- For the terminal growth rate after 2025, I apply 3%, which (about one percentage point higher than estimated nominal global GDP growth).

Given these assumptions, I calculate a base-case target price for adidas of about $71.68/share.

{kind=link}

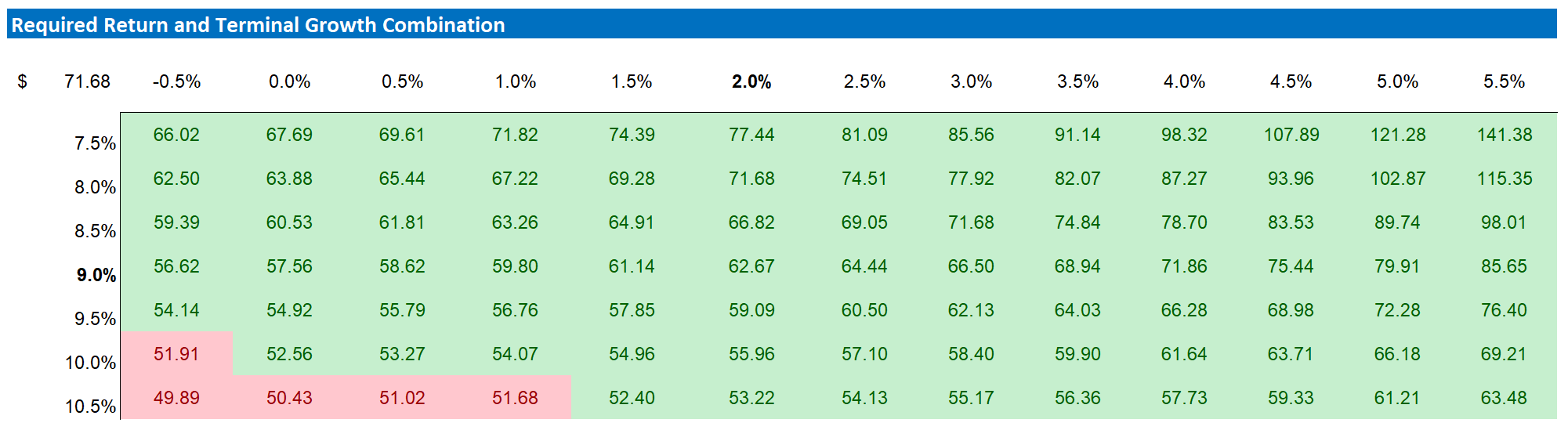

Notably, my base case target price does not calculate a lot of upside. But investors should also consider the risk reward profile. To test various assumptions of adidas' cost of equity and terminal growth rate, I have constructed a sensitivity table.

Note that the matrix looks very favorable from a risk/reward perspective. With bearish assumptions, the downside case is somewhere around $50/share, while with bullish assumptions, the upside case could be as much as $141/share.

{kind=link}

Risks

adidas' business operations are clearly positively levered to the health of the global economy, and especially to China. Accordingly, any further slowdown in consumer confidence - which is not yet priced in - could materially affect the company's profitability. Moreover, adidas is based in Europe, but operates globally. Thus, investors should consider that FX fluctuations might contribute to a respective fluctuation in financial performance. Finally, investors should also note that much of adidas' share price volatility is driven by investor sentiment towards risk assets (stocks) in general. Thus, investors should expect price volatility even though adidas' business outlook remains unchanged.

Conclusion

The profit warning clearly indicates short-term challenges for adidas. But personally, I cannot identify any headwinds that might pressure the sportswear group's business outlook long term. Thus, long term focused investors might consider the "dip" as a buying opportunity - the valuation certainly looks attractive, in my opinion. According to my model - which I anchor on a residual earnings valuation - adidas stock should trade at approximately $76.68/share. Buy.

For further details see:

adidas: Buy The Dip