ADDDF - adidas's Strong Brand Will Likely Aid A Successful Recovery

2023-06-26 14:22:07 ET

Summary

- adidas's stock is currently in a bottoming process, but it could take several years to fully recover its old highs.

- A strong historical brand and operational improvements increase the odds of an eventual recovery, but it will likely be very volatile.

- Investors would be wise to adopt a medium-term, three- to five-year time horizon if investing in adidas at today's price.

- In this article, I estimate the likely returns and probabilities if one buys the stock today, and I share my investment strategy for adidas.

Introduction

On September 19th, 2022 I published an adidas ( ADDYY ) article titled " It's Time To Buy adidas Stock And Wait For A Recovery ". Here is how the stock has performed since that article when compared to the S&P 500 ETF ( SPY ):

So far, along with providing very good absolute returns, adidas has more than tripled the return of the S&P 5000 index. As with all the stocks I suggest are buys in my articles, I purchased the stock myself around the same time I published my article and I currently remain long adidas stock.

Sometimes with investing, I think we make things more complicated than they actually are, and the best investing ideas only have one or two factors that explain the market's mispricing of any given stock. In adidas's case, there are four broad factors I think investors should consider, and I'll cover them in this article. I will phrase these factors as four questions. The first is: Are adidas's earnings decline likely temporary in nature? The second is: How long might earnings take to recover? The third is: What sort of returns is an investor likely to get over that time period if they buy at a certain price? And the fourth is more personal to each investor, and that is: Are those likely returns acceptable to the investor if we assume a 20% likelihood of failure?

If an investor can roughly approximate answers to these questions, then they can estimate what sort of price they would be willing to pay for adidas stock. While these factors are actually a little more complicated in adidas's case right now than they are with most stocks, they don't need to be more complicated than this. In fact, while I think considering additional factors or trying to be too precise with estimates (especially near-term estimates) might appear more sophisticated to the average reader, they wouldn't likely be more effective in terms of results. (I actually haven't paid any attention to this stock in my portfolio since I bought it last year, other than noting the announcement of the CEO change last fall, because I knew it was going to take some time to see what happened.)

With this simple framework in mind, let's see if we can answer these questions.

Are earnings declines temporary in nature?

Let's start by examining adidas's historical earnings patterns.

{kind=link}

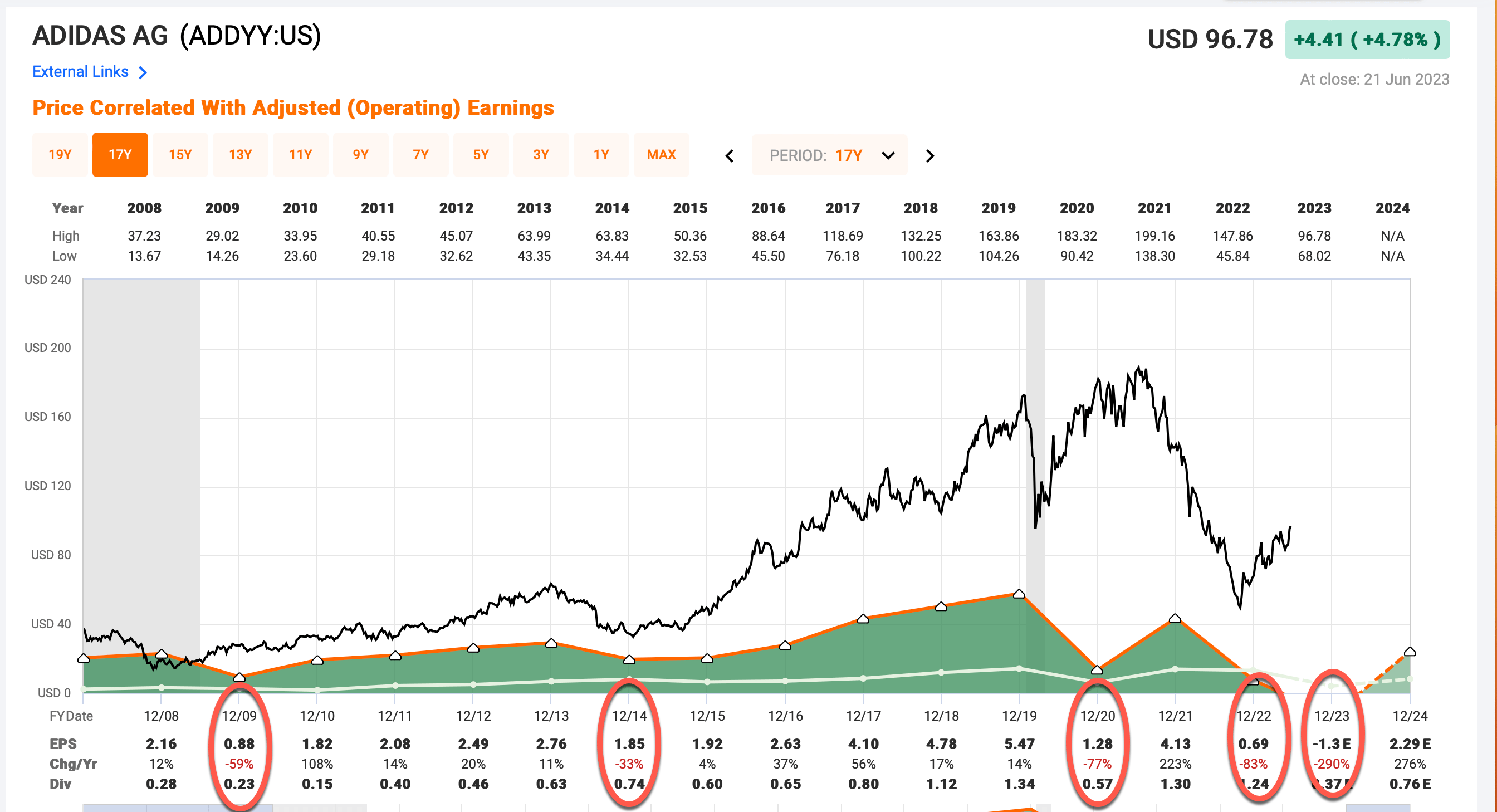

The dark green shaded area in the FAST Graph above represents adidas's historical earnings per share. I have circled in red the years in which earnings growth was negative. The main thing I'm looking for here is historically how deep EPS growth falls during downturns and recessions. If there is a history of earnings falling deeper than -50%, then I categorize the business as "deeply cyclical". In 2009 we see a -59% decline in earnings growth, and also a pretty big decline of -33% in 2014. Because the 2009 decline was deeper than -50% I treat adidas as a deeply cyclical business when I try to determine the price at which I might buy the stock. The most important adjustment that needs to be made for deep cyclicals is to ignore earnings-based valuations. While it is important that a business has a history of producing higher earnings peaks each cycle (which adidas had done until 2020), once this history is established, we must ignore current earnings and earnings estimates because they fluctuate too much to be a useful valuation guide. Quite often, in fact, when P/E ratios look the best with deep cyclical stocks, it is at the beginning of a deep price decline, and when P/Es look worst, it is near the bottom. In the end, as a valuation tool, P/Es are very unreliable for deeply cyclical businesses.

Rejecting earnings-based metrics is the first step toward successfully investing in high-quality cyclical businesses. But we do need to ask whether the earnings declines they are experiencing right now are likely to be temporary or to be long-lasting. I have a strong bias towards using historical patterns as a guide for these questions, and as I pointed out already, even after the GFC in 2009, adidas's earnings recovered in a timely manner and went on to make new highs. Since 2020, adidas has suffered from two or three major challenges. The first was obviously COVID. In 2020 earnings fell -77%. This was no fault of adidas, though, and in 2021 we can see that EPS bounced right back and was on track to fully recover by 2022. So, in my mind, I think adidas's earnings successfully recovered from the GFC and would have recovered from COVID, too. Both of those were macro-factors and didn't really have anything to do with adidas's long-term success as a business.

{kind=link}

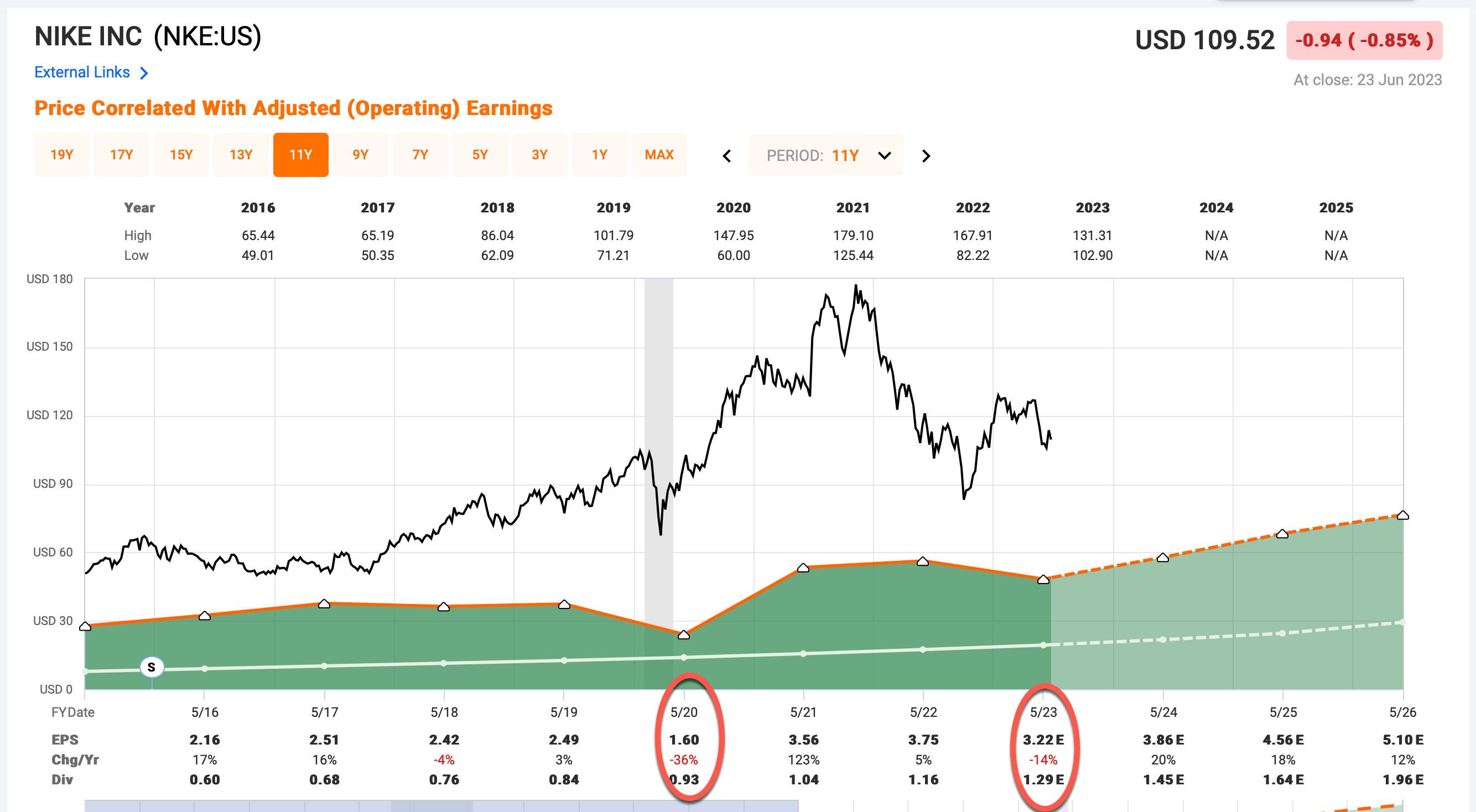

If we look at competitor Nike ( NKE ), we can see that they had a pretty deep -36% earnings decline in 2020, too, which was shallower than adidas's, but some of that also likely had to do with Nike's fiscal year ending in May, instead of December, and then massive amounts of US stimulus being pumped into the economy in early 2021, and the US opening up its economy faster than other parts of the world. Foot Locker ( FL ) shows a similar pattern in 2020 and 2021, which is more evidence there really wasn't anything adidas did wrong. By the end of this year, most of the negative COVID effects in various worldwide markets should be behind us. So I believe COVID is no longer a factor for earnings going forward.

This brings us to two remaining issues. One of them is the abrupt breaking of ties with Kanye West and being stuck with a lot of inventory due to that breakup. Again, to me, this is mostly temporary. It wasn't as though adidas did something wrong that would permanently damage their brand. There will always be new athletes and celebrities willing to endorse a brand like adidas, even if it takes some time for them to emerge. It is much more an issue of time than it is the likelihood of permanent brand damage. So it's not if, but when a recovery occurs on this front. And, if anything I think adidas will be more careful when it comes to the partnerships it enters into the future, which likely lowers this sort of risk going forward.

The last issue is one I think is more difficult to gauge, and one I didn't really consider at the time of my purchase of the stock last year, but international relations between the West and Russia and China, along with Chinese economic weakness, is probably the biggest wildcard to the recovery thesis because these economies could 1) still be in decline, and 2) might take a long time to recover.

The issue regarding Chinese sales and margins came up in the most recent earnings call and I thought the answers from management were honest and straightforward.

In China, we need to be careful because the positive thing is the following. We have so in less to the trade that they have sold out. So that means, for the first time, inventories in the trade of adidas product is going down, and there is a demand that the retailers haven't seen for a long, long time. It's the first time I see this in many, many quarters. And that makes all of us, of course, positive. We also had our 2 big retail partners from China here in headquarters, and it's the first time again that they see, I would say, not on the light of the tunnel, but see some normal developments coming.

That gives our team, which you remember has been almost in 2.5 years kind of quarantine or under heavy restriction of course, have a lot of energy, and there's a lot of activities now going on in China that is consumer fronted. We talked about athletes, we talked about culturally-relevant events. We talk about in-store activities. And also in the social media side, starting to build campaign again to generate traffic and conversion. So that's very positive.

The reason why I'm hesitating to say, okay, that would mean that Q2 and Q3 will be up in sales, of course is again, if I say that and it doesn't happen, you get mad at me so I'm careful. But the indication is, of course, that if this continues, that will happen. It's obvious. And I do think you will see an increased top line coming in China. But don't arrest me on quarter-to-quarter because it's impossible to kind of be certain about that.

My personal feeling when it gets to market share is that, of course, all the Chinese brands have exploited the last 2.5 years and in a very smart way. But I do also -- and again, from everything I can see, feel that is being saturated so that the growth that they got almost for free is starting to slow down, and that you will see Western brands, again, starting to take back some market share. And I, of course, hope that we will take most of it back again.

I do not think that China will be 1-to-1 the way it was because competition is, of course, now harder. But I am counting on China being one of our fastest-growing market and also one of our most profitable markets, if not the most profitable. So I am or we are, I think, realistic, optimistic mid-term about China.

I like realistic and straightforward answers like this. They know they have a hole to dig out of, but it's going to take some work and some time to do so. Additionally, throughout the conference call, it was clear to me management is aware they aren't where they want to be. They are bringing in and meeting with all their partners and stakeholders to figure out improvements they can make. This overall approach, because of adidas's strong historical brand, has a high likelihood of success. But they have to play the hand they were dealt, which is currently much weaker than it was going into COVID 3.5 years ago.

Putting all this together, the most reasonable expectations for adidas's future earnings (which is what will ultimately guide the stock price) is almost certainly higher. So, there is a very high probability the current earnings woes are temporary and adidas's stock does recover.

How long might earnings take to recover?

While I think adidas's earnings have a high likelihood to recover, I also think there is a reasonably high probability this recovery will not be fast. They took a hit from COVID, a hit from Yeezy, and a hit from international relations tensions (at least to some degree). We might also see recessions in Europe and the US, and China is already pretty weak and in slow recovery mode. The next year or two could continue to be very challenging. Before I make any estimates, I find it helps to look at history as a guide, at least to give us some sort of framework to build upon. I understand that each down cycle is different, but having a frame of reference never hurts.

Above is a drawdown chart of adidas's ADR, which includes the great financial crisis and recession in 2008/9. That was a very bad global recession and peak-to-trough, adidas stock fell about -65%. It was that drawdown I used as a guide for my entry point into the stock last year. It wasn't a perfect guide, and adidas stock actually fell another -30% after I bought it, but now the stock looks to at least be starting the bottoming process. If there is a recession within the next 18 months, the stock price might go back down and form a double-bottom, but I doubt it makes new lows from here.

During the 2008 downturn, adidas stock took about three years to recover peak-to-peak, and took about two years to recover off the bottom. The 2014 downturn took about two years peak-to-peak and 1 year off the bottom. When I'm making investments like this my basic rule of thumb is I want to see a +100% return within five years. (Because I bought when adidas was -65% off its highs, I'll be aiming for a +200% return within five years with my investment.) But the stock is currently about -50% off its highs, which means if the stock price recovers within five years, it would still provide adequate returns for many investors.

All that said, the challenges this time around are different than 2008. My base case is that Europe and the US are probably on the edge of going into a recession or extended stagflation if a recession is avoided. So, even though adidas's stock price is down a lot, it's entirely possible a recession gets piled on top of everything they are dealing with. Putting all this together, I think investors considering buying adidas stock today probably need to be prepared to commit to at least a four-year holding period, rain or shine. And volatility is likely to be extreme.

What sort of returns (and volatility) to expect?

When dealing with deeply cyclical businesses (even if there are other factors at play as there are with adidas this time around), I always like to assume that history is a strong predictor of the future. With most elite businesses that have a long history of success, there are reasons why the success has been long-lasting. It's usually not necessary to try to break down each specific reason why this is so (assuming one could). So when I invest in a deeply cyclical business my thinking is that unless the business is coming off a bubble or super-upcycle, then it is reasonable to assume the market will be willing to pay a similar price for the stock at some point in the future when we have an eventual upcycle. As I explained in the last section, adidas stock usually recovers within about three years of the time a downcycle starts. The current situation is a little trickier because we aren't quite in economic recessions yet in the major economies around the world. So, being conservative I assume this time around might take five years for adidas's business to recover and for the market to pay a similar price that it did in the past. I don't usually assume the market will pay more than that price (which, again, makes my expected upside pretty conservative).

What taking this approach allows me to do is look at adidas stock's previous cyclical high price, and assume that within four to five years, we will see the stock price back at those levels. Making these assumptions allow me to estimate my likely total returns. I bought the stock when it was about -65% off its highs, which is roughly a +200% return if the stock price fully recovered within five years. That's just under a 25% CAGR expectation. Now the stock price is about -50% off its highs which translates into a 100% return if the stock price recovers to old highs. If it takes five years, that's about a 15% CAGR, and if it takes four years, it's about a 19% CAGR. These are respectable returns by almost anyone's standards.

The challenges for many investors who are investing in cyclical stocks during downturns are severalfold. First, usually, investors underestimate the downside potential because they haven't examined the history of earnings and stock price, so they buy too soon in the downcycle. This limits the upside return potential while also increasing the drawdown one must suffer through, and even worse, it dramatically increases the chances an investor sells closer to the bottom because earnings come in worse than expected and the stock price craters.

Let me show an example. If a person would have noticed ADDYY was down -20% off its high on 9/30/21 and thought that looked like a pretty good entry point for such a historically strong, well-known business, and bought the stock based on that, the chart below shows their returns over the next 14 months.

At some point during this process, most investors will have questioned their initial thesis and sold the stock at a much lower price than they bought it. And those that didn't sell, but held on, would be looking at many years just to get back to even. I often get a lot of pushback when I share the prices at which I would be willing to buy a deeply cyclical stock (or any stock, really) because they are often pretty low. But I know how nasty these downcycles can be. It just takes one extra unanticipated negative event for the bottom to fall out. Even buying at the very low price I paid, I still had to hold through a -30% drawdown.

I think investors who are considering buying today, need to be aware that there is a decent chance, say 50%, that during a recession the stock price could revisit its lows. The low for the ADR ADDYY was $45.84. The current price is $96.25. That's a little more than -50% drawdown for investors who are considering buying today. While the upside potential for the stock is pretty good, an investor has to be willing to accept they'll have a non-trivial chance to have their investment cut in half at some point over the next 12-18 months.

Are these risk/return probabilities acceptable to you?

I first started using this strategy in 2015 and sharing it publicly in 2016, so I've been at it for over seven years now and bought and sold dozens of stocks using this approach (For details of the approach, read my previous adidas article linked at the beginning of this one, I didn't want to repeat all that here.). Since the very beginning, a pretty clear pattern of about 1 in 5 investments suffering major losses when using this strategy has held fairly steady (though, I've improved on that a little in recent years). One investment eventually went totally bankrupt. There is real risk when aiming for such high returns. But if you get, say, 3 doubles, and 1 mediocre return, you can afford the occasional big loser and still come away with above-average returns. (Obviously, I don't know which one out of five is going to be the big loser when I buy the stocks.)

Here is how I think this all shakes out given the stock's current price. I'd say there is a 50/50 chance of a significant drawdown in the stock price of around -50% if there is a recession. There is a 20% chance adidas stock does not recover in a timely manner. There is another 20% chance the stock performs mediocre over the medium term. And there is a 60% chance the stock price fully recovers within about four years and returns a +100% total return.

Because I monitor hundreds of stocks and have an unconcentrated portfolio, I tend to take 1% or 2% weighted positions in deep cyclical stocks like these. I started with a 1% weighting in ADDYY, but if we get a double dip, there is a good possibility I would double my position if I thought the decline was due to an economic recession and not just a company-specific issue. I wouldn't suggest taking more than a 2% initial weighting with this strategy, though. The success is largely a game of numbers and as I have shown, these stocks can be very volatile. Taking smaller weightings allows me to buy the stocks at the prices I want and then basically forget about them. It's not uncommon for them to continue falling -50% or -60% and still go on to produce +100% returns a couple of years later.

What is essential to all of this is taking a medium-term (3-5 years) approach. Just as a lot of investors underestimate the downside potential of stocks like these, they can also sell too early in the recovery. If a person bought at a decent price and suffered a -40% or -50% decline, many will be tempted to sell when the stock "gets back to even". I strongly suggest targeting an eventual price that is similar to previous highs instead. If you buy at a good price, and can get somewhere between a +100% and +200% return, then it should be much easier to hold for the medium term instead of aiming for short-term gains.

Conclusion

As I noted in the introduction, sometimes simple strategies are harder to implement than more intricate, precise, or detailed strategies. There are going to be plenty of analysts who try to predict earnings quarter to quarter and who create compelling stories about very specific business issues in an attempt to predict the stock price. But when stock prices get low enough (or high enough) we don't really have to do that anymore. What we really need to do is to zoom out, look at the broad picture, and then extend our time horizon out a few years. If we do that and see the probabilities of a very big return are high enough, we can gain enough clarity to place a bet and wait.

If I was going to lodge one criticism of my approach with adidas stock, it's that part of the current downturn will require an operational turnaround and not just a cyclical recovery. That's a fair critique. But as I noted, I think management is currently doing its best to address the operational side. It's unlikely even people with full inside information know exactly how that turnaround will progress over the next 3 or 4 years. I think the brand is still strong overall and that should provide a tailwind. And, the truth is, if this risk wasn't there, then the stock price wouldn't be trading as cheap as it is. When I bought at -65% off its highs, part of buying as low as I did was to try to account for this risk.

At the current price, my official rating is going to be a Hold, but one of the reasons I shared the breakdown of probabilities and how I think about returns is that for some investors, taking a 1% position here, and then reserving another 1% weighted position if the stock price does come back down near the previous low, probably would make the stock a "Buy" for them. So, as long as the risks are known and understood. And as long as the weightings, time frame, and strategy are generally followed, adidas stock is a pretty good bet still today for medium-term investors.

For further details see:

adidas's Strong Brand Will Likely Aid A Successful Recovery