ADMA - ADMA Biologics: Adding Intrinsic Value Based On The Catalysts

2023-06-15 22:10:33 ET

Summary

- ADMA continues its demonstrated sales performance with another tremendous growth in revenue for Q1 last month.

- There are fundamental, sentimental and valuation facts to suggest ADMA is mispriced in my opinion.

- Reiterate buy, seeking a 20% return objective over the coming 6-months.

Investment Summary

A full 6-months have passed since my buy thesis on ADMA Biologics, Inc. ( ADMA ), and the investment thesis has begun to vindicate itself with a 14% return on capital at the time of writing. There were several features adding a bullish reward to the risk/reward symmetry in ADMA's case back in January. To name a few:

- The market has been generous to the company's primary humoral immunodeficiency ("PHI") hypotheses.

- The market for PI diseases is expected to grow at CAGR 7-8% into 2029/'30.

- The company's new 4,400 liter scale production level for BIVIGAM is a meaningful tailwind to revenue in that segment.

- Tremendous revenue ramp projected into FY'24/'25

The critical facts have been updated after the company's latest numbers, where it booked $57mm in quarterly revenue, ahead of The Street's estimates. This analysis will convey these critical facts and illustrate my own informed opinion on the company. I believe there is evidence investors will pay a higher market value for ADMA over the coming 1-3 years. Net-net, the numbers do the talking for ADMA here. The growth numbers that is. I am reiterating the company as a buy, looking to $4.80 as the next target, or 20% upside on the current market price.

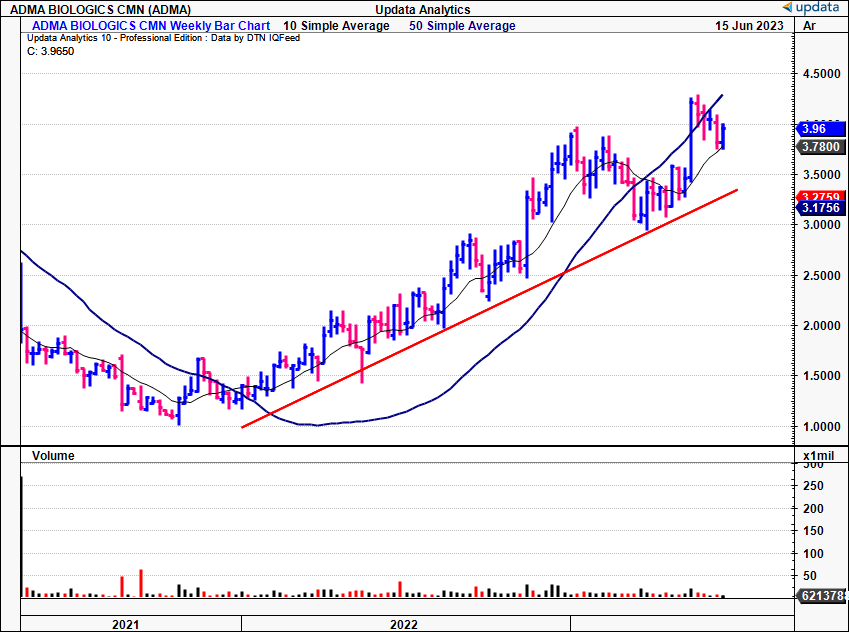

Figure 1. ADMA rally from 2021–date [weekly bars shown]

{kind=link}

Detailed summary of the buy thesis

For any stock price to outperform the market in my view, there should at least be a catalyst in one of three categories, fundamental, sentimental and/or valuation. It is rare to have a combination of all three, but can be lucrative if you get so lucky. More commonly, you get a combination of 1-2. But, as the recent singer Meatloaf sang, "two outta three ain't bad". Looking at ADMA's case, we've got evidence of at least 2, maybe 3 out of the lot.

Fundamental catalysts

Looking at the Q1 FY'23 numbers , ADMA booked its first non-GAAP EBITDA in the green at $2.5mm. This stemmed from the 96% YoY spike in Q1 turnover to $57mm. Growth was underscored by demand (volumes) of the company's immune globulin ("IG") products, evidence of the broad-based adoption in the marketplace. This is key in my view, as there had been some talk years back about the viability of IG products, with plasma collection at the forefront of these criticisms, and this seems to have been proven wrong as I write.

Growth company, an alluring term, is cited as the central thesis for far too many investment portfolios. It is a term applied too liberally. ADMA qualifies as an actual growth company, evidenced by the following long-term record:

Table 1. ADMA revenue growth 2013-2023 TTM

Data: Author, ADMA SEC Filings

The growth percentages do the talking here. At the trailing $181.9mm in turnover, ADMA has compounded turnover at 50% annually since 2013, a true long-term growth name. And, there is all reason to believe this will continue into the future.

Highlights of Q1 operations

The operating highlights are as follows:

- The BioCenters segment clipped a $4mm increase in sales of normal source plasma, fulfilling the long-term plasma supply commitment for 2023 with a third-party. Plasma can be hard to come by, and ADMA anticipates using all the plasma collected from its BioCenters network to support IVIG production operations in H2 this year.

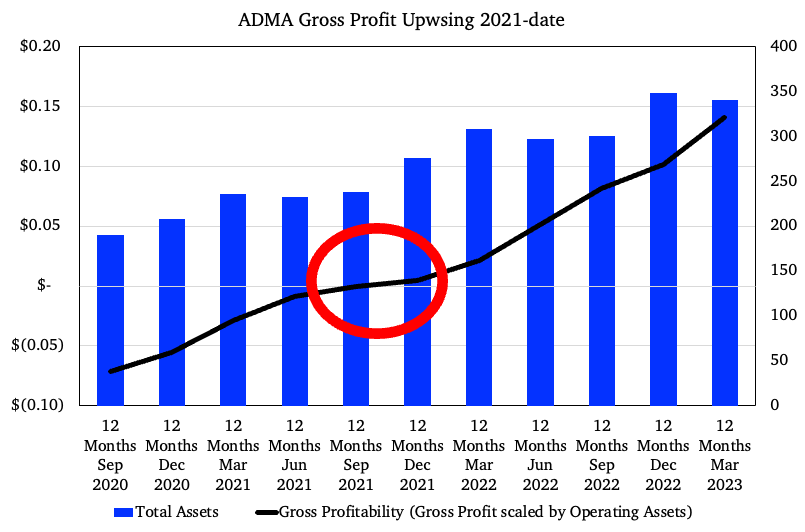

- Gross margin has been a negative for ADMA to date, as it hasn't yet benefited from economies of scale with the size of its business. This looks set to change going forward. Q1 gross pulled to $16.5mm, on a quarterly margin of 29%, up 12 percentage points on Q1 last year. As mentioned, the improvement in gross profit can be traced to the revenue upsides and a reduction in other manufacturing costs on a leaner business. Two additional points on gross profit. When you scale gross profit against operating capital, you can see the trend has been a linear progression. The break-through point was late FY'21, precisely when the stock caught its first bids to price higher.

- Related to point (2), the company is shifting its product mix to higher-margin segments. Primary evidence of this is the transition to the 4,400-litre- BIVIGAM product (mentioned extensively in the last publication)– this is complementary to the gross margin in my models.

Figure 2.

Data: Author, ADMA SEC Filings

{kind=link}

Given the higher revenue clip, management upped guidance to $220mm for the full-year, and calls for >$220mm at the top line. That would build another. c.$65mm on top of FY'22, and my estimate is that the company can get there, based on the culmination of factors raised in this analysis.

Unit economics

Chief to seeing ADMA growing further is its capacity to build its book of operating centres to collect plasma. The company saw favourable business trends for its plasma centres on aggregate in Q1, as it made more "mature" (higher samples) collections at a higher number of centres. That is simple economic rhetoric in my eyes– collect more plasma, and do it at more centres. I'd also add these inflection points for the plasma collection segment:

- The number of operating centres increased from 7 to 10 in Q1 FY'22–'23, with all centres now open and actively collecting plasma.

- As mentioned, most of the company's centres have entered the maturity phase, enabling the collection of plasma in more significant numbers.

- Another highlight, is that ADMA expects quarterly OpEx to remain flat at c.$1.8-$2mm (as it was in Q1) for the remainder of the year. I'd point out that it is capitalizing more costs on its inventory (keep an eye on this, not for ADMA to 'over do it'), and charging the sales fee against revenues versus operating costs to support this claim.

Liquidity and current position

ADMA's net loss for the quarter was $6.8mm, a more than significant decrease of $18.2mm from last year. The current ratio is 7.3x, and still 1.91x on cash alone. Further, $145mm in equity is holding up $340mm in assets, with just $144mm in long-term debt on the books via a $151mm notes issue in FY'22. Importantly, receivables have tracked behind revenues, indicating that the firm isn't getting too far ahead of itself in terms of cash (un)collection. In my view, the company has sufficient cash runway to get itself through the next 2-years. Cash used in operations was $48mm in the TTM to Q1 FY'23, primarily due to inventory purchases of $25mm and the combined OpEx.

I would also opine that ADMA's recent credit amendment with Hayfin has introduced favourable changes to the company's capital structure. The modification entails a 100bps reduction in the nominal interest expense on ADMA's current note issues. This results, a lowered borrowing rate of SOFR plus 8.5%, not a terrible commercial rate for a corporation doing ADMA's amount of business. Moreover, the amendment offers a newly structured 50% waiver of the prepayment fee if the company is involved with an acquisition. This could reduce the firm's cost of capital going forward– essential to seeing it obtain growth capital at critical junctures in the future. Plus, if you think about it, in the current rates regime, any cards that can be pulled to control interest rate risk are a plus, in my view.

Sentiment and valuation

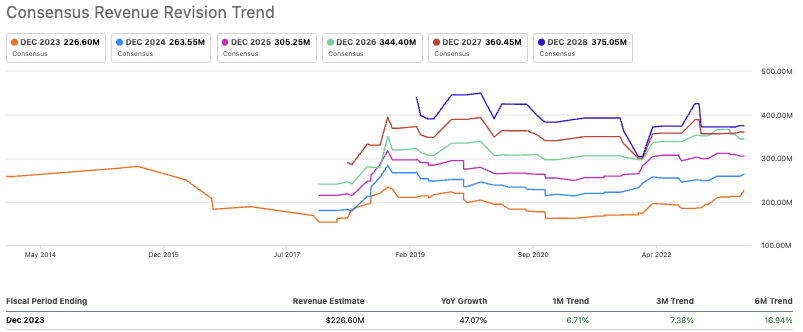

I estimate there are sentimental factors that are catalytic to ADMA's stock price as well. There's been 3 earnings and 4 revenue upgrades in the last 2 months, contrasting to zero downgrades. Consensus projects, surprise, 47% YoY growth in revenue for FY'23, not far off long-term range discussed above.

Figure 3.

{kind=link}

The stock also trades above its 50, 100 and 200 day moving averages , meaning investors are paying higher multiples to buy the company. That tells me of revised expectations, also indicated in the price action over the last 12-months. It is up across all time frames, except the last month of trade. There is reason to believe it will continue at this pace, given the factors discussed thus far. These changes in sentiment are valuable to the investment thesis.

Investors are selling their ADMA stock at 3.8x forward sales , which is actually a 14% discount to the sector. Given that asset factors and earnings power are reflected in a company's equity value, importance must be placed on the market's view of this. The market has placed a ~6x multiple on the company's book value of equity, indicating its expectations on asset growth going forward. Each of these factors are telling. One, investors are paying higher multiples for ADMA as time goes on, evidenced by both the momentum and valuation factors. Two, at just 3.8x sales, and 14% discount to the sector, there is plenty of scope to see ADMA rate higher on relative value alone, in my view.

Point is, each of these points are supportive of a buy. At the sector 4.4x multiple to management's $220mm estimate, you get to ~$4.40 valuation, and if you work another 10% on management's view (which is correctly conservative, as admitted on the call) you get to $4.80. Both are respectable gains in market valuation to expect for the coming 6-months or so, another 20% at the upper end.

In short

With all the factors raised on ADMA today, there is enough evidence to remain bullish in my view. Findings suggest the company has the good part of its growth ahead of itself. That, and that it has another 3 quarters to do $220mm in turnover on management's forecasts, 42% YoY growth. It has compounded revenues at 50% on average since 2013, so this isn't unsurprising. Looking ahead, I believe if you value the company at the sector multiple of 4.4x expected sales, you get to a range of $4.40–$4.80. Further upsides from ADMA would add more value to this. Hence, in my view, ADMA is a buy.

For further details see:

ADMA Biologics: Adding Intrinsic Value Based On The Catalysts