ADMA - ADMA Biologics: Growth Trends Pointing To Profitability

2023-03-29 15:52:09 ET

Summary

- ADMA Biologics, Inc. recently reported their Q4 and Full-Year 2022 earnings, which revealed a beat on EPS and revenue. The company believes 2023 will be a significant “inflection point.”.

- The company is establishing strong growth trends, which are pointing towards the possibility of hitting positive EBITDA in the second half of this year.

- ADMA is now well-funded with a growing plasma collection network to help fuel growth. As result, ADMA will remain a “Top Idea” in my Compounding Healthcare Service.

- Admittedly, I have booked profit on my ADMA position and have moved it to “house money” status. However, I am looking to recalibrate my Buy Targets and Sell Targets following the positive earnings.

- I provide an updated game plan for my ADMA Biologics stock position.

ADMA Biologics, Inc. ( ADMA ) recently reported their Q4 and Full-Year 2022 earnings, which revealed a beat on EPS and revenue. Management expects 2023 will be a significant “ inflection point ” for the company. The company is establishing strong growth trends, which are pointing towards the possibility of hitting positive EBITDA in the second half of this year.

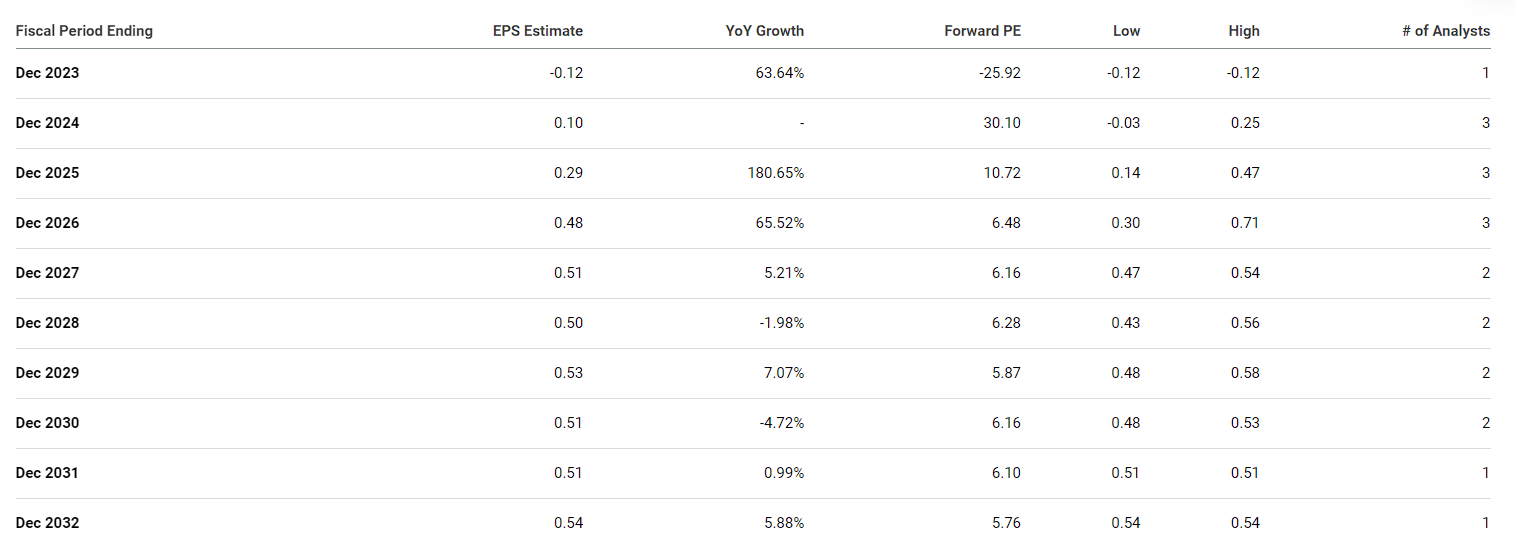

I believe ADMA has the ingredients to hit their goals and report a positive EPS for 2024. Obviously, this is a major catalyst for the company and the ticker. ADMA is now well-funded, with competitive IVIG products and a growing plasma collection network to help fuel growth for several years. As result, ADMA is still a “Top Idea” in my Compounding Healthcare Seeking Alpha Marketplace Service and is now the only “Bio Boom” ticker with a conviction level of 4 out of 5. Admittedly, I have booked profits on ADMA as it hit both my Sell 1 and Sell 2 Targets and is now a “house money” position. Nevertheless, I am looking to adjust my Buy Targets and Sell Targets based on the strong likelihood that the company will report a net positive in the coming quarters and won’t turn back.

I intend to review the company’s Q4 and full-year 2022 earnings and will provide my opinion on their performance. In addition, I update my game plan for my ADMA position.

ADMA Biologics Q4 Earnings Review

For Q4, ADMA Biologics, Inc. pulled in about $50M in revenue verse $26.4M in Q4 of 2021, which is up $23.6M or about 90%. The company attributes this surge in revenue to the “commercial ramp-up” of their “IVIG product portfolio and the expanding customer base for BIVIGAM and ASCENIV.” In addition, their Q4 gross profit spiked to $14.2M verse the $3.5M, which was supported by ASCENIV’s performance against the lower-margin BIVIGAM. The company’s consolidated net loss of $12.2M, which was a $4.4M drop from the $16.6M net loss in Q4 of 2021.

ADMA’s balance sheet and financials have improved over the past year, with their total asset value finishing 2022 at around $348M. This includes $163M in total inventory, ~$87M of cash and cash equivalents, in addition to ~$15.5M in accounts receivable.

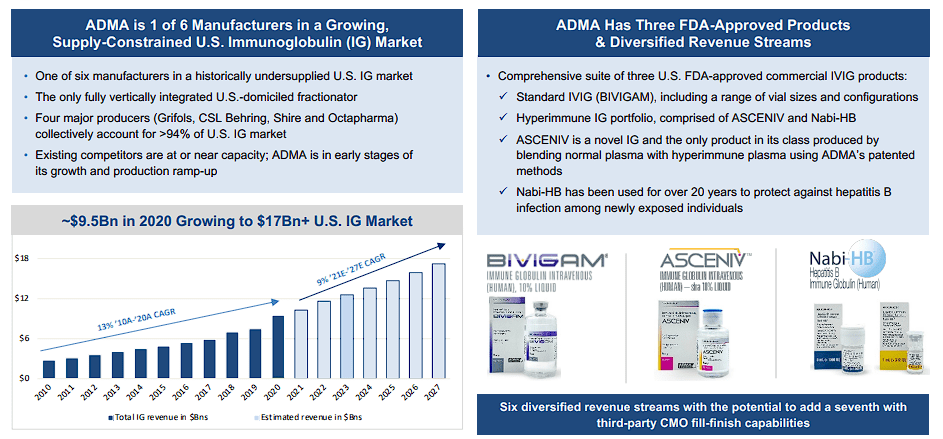

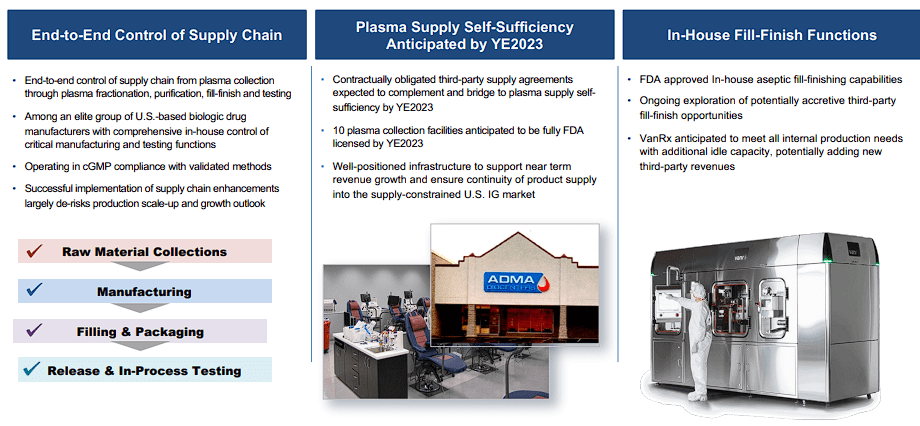

Furthermore, ADMA also updated us in regards to their BioCenters plasma collection network, which now comprises of 8 FDA-licensed centers with 2 more plasma centers operating and awaiting FDA licensure by year-end. What is more, the company forecasted that the projected raw material from their 10 BioCenters will provide them with the plasma supply to be self-sufficient for their current products.

Another important note to highlight is the “elevated ASCENIV utilization trends” with reassuring patient persistence with some beginning their third year on the product. In addition, ADMA publicized that there was a “record expansion of new accounts as well as reorder velocity among existing customers.” As a result, the company believes that these commercial trends “support product upside over the near term and longer term.” In anticipation of this growth, ADMA plans to start producing ASCENIV at the 4,400-liter production scale. This expansion should significantly improve ASCENIV's margins and production goals to hit their target revenues.

In terms of guidance, ADMA expects to exceed $210M in full-year 2023 total revenues, which is up 36% from the $154M mark in 2022. Plus, they expect to hit “EBITDA profitability no later than the second half of 2023.”

Lastly, management did reiterate that their “strategic alternatives process remains ongoing” and that they are “exploring value-creating opportunities.”

My Thoughts On ADMA's Earnings

For me, the earnings cemented my conviction in ADMA as the fastest-growing provider of immunoglobulin in the U.S. market thanks to their ability to target the fastest-growing cohort of immune-deficient patients. ADMA has the pulse of the U.S. immunoglobulin market and has the business model and IG products to accelerate their growth in the coming years. In fact, ADMA anticipates “2023 to be an inflection point” and will ”sustain top-tier revenue growth” and “achieve first-time EBITDA profitability and shortly thereafter, solidify the pathway to an ultimate margin profile at the upper bound of ADMA's plasma manufacturer peer group.” These projections appear to be feasible considering ASCENIV’s commercial trends, and increased production scale, and it becomes a larger portion of the company’s overall product mix.

The other item to note is that ADMA continues to outperform the Street’s and their own expectations.

Long-Term Outlook

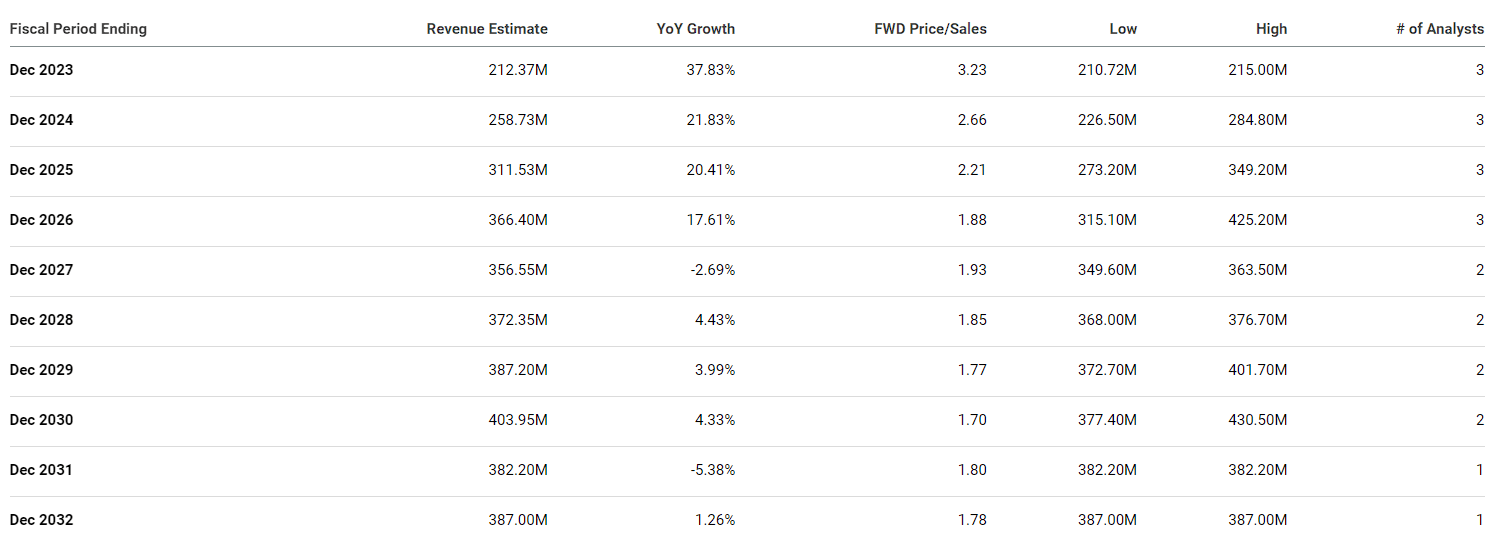

Over the past few years, I have taken a conservative approach to ADMA's financial guidance. However, ADMA is optimistic that they might surpass their top and bottom line guidance if the demand trends and margins sustain. It is important to note, that ADMA is including potential new growth initiatives when they forecasted them exceeding $210M in total revenues and generating positive EBITDA this year. So, there is some potential that ADMA crushes those goals by year-end.

{kind=link}

ADMA believes the company investments in the supply chain and commercial infrastructure in recent years have created a solid foundation for maintaining best-in-class revenue growth and potentially achieving an ultimate margin profile at the upper bound among the company plasma product manufacturing peers. This execution has created a solid win streak on very bullish top and bottom-line trends. As a result, I believe that they've got an opportunity to achieve EBITDA sooner than the second half of this year thanks to the demand trends and if the utilization that ADMA is reporting continues. In fact, CEO Adam Grossman stated that they “should meet or exceed all of our previously stated targets.”

The fact remains that ADMA’s products are efficacious and their strong utilization comments lead me to believe that demand is not going to dry up in the near term. Thankfully, ADMA reported that their efforts to get their raw material in-house have provided them with the plasma needed to “support all upwardly revised revenue forecasts” and “may provide for opportunistic external plasma sales.” What is more, the company’s yields and manufacturing process has been refined, so the company should see improved revenues and margins down the road.

{kind=link}

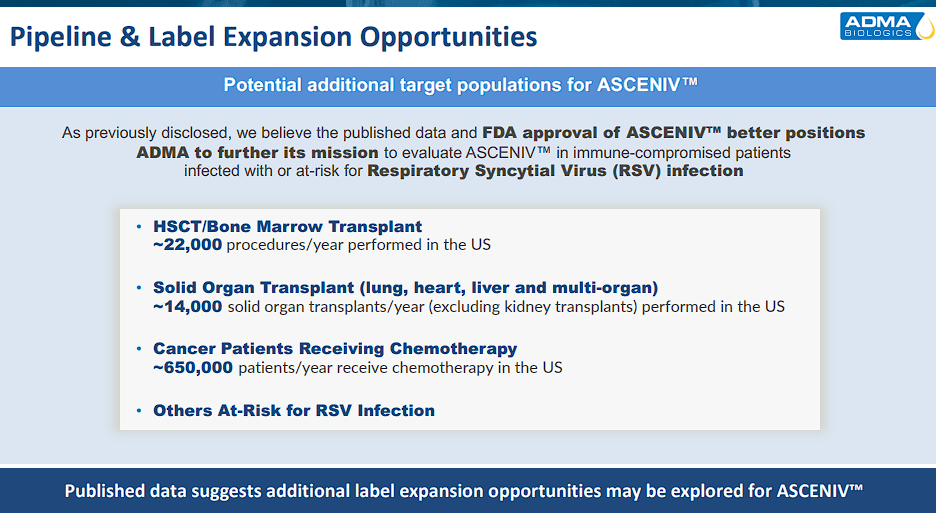

Last but not, least, ADMA still has ongoing post-marketing clinical studies that should eventually provide prospects for label expansion for both BIVIGAM and ASCENIV in a growing U.S. IVIG market that is projected to grow at a 7.1% CAGR and expected to hit $12.24B by 2030.

ADMA Biologics ASCENIV Potential Label Expansions (ADMA Biologics)

{kind=link}

Keep in mind that a large percentage of patients who use IVIG have conditions/diseases that might require them to be on IG for the rest of their life including AIDS, CDIP, leukemias, and other immunodeficiency diseases, which comprises of 150 rare disorders. This segment made up 22% of the market in 2020 attributable to the fact these patients have to remain on the IVIG. So demand for IVIG is not fading anytime soon.

Considering that ADMA is only one of several players in this market, they are positioned with three FDA-approved drugs to benefit from this growing demand, and now they have the raw materials to help meet the demand.

So, I believe the company’s forecasts are attainable in their timeframes, and I wouldn’t be surprised if they exceeded them.

{kind=link}

Luckily, ADMA is not alone in their positive outlook. The Street expects ADMA to report solid growth for the next few years and will report a positive EPS in 2024 and will maintain it into the next decade.

Downside Risks

Admittedly, ADMA Biologics, Inc. is not in the clear yet and they only have ~$87M in cash. So, a major setback could move their EBITDA timeline back and prolong their cash burn, which might force them to raise funds through dilution. ADMA relies on donors for their raw materials, so a reduction in quality donors could force them to reduce their output, or possibly look to other suppliers for the raw materials, thus, hurting margins. In addition, it is possible one or more of their BioCenters or manufacturing facilities lose compliance. Indeed, I don’t foresee this happening, however, the point is that ADMA still has some risks and investors need to manage their positions appropriately.

As a result, I am giving ADMA a conviction level of 4 out of 5 in my Compounding Healthcare investors group. It is important to note, ADMA is the only ticker in my speculative “Bio Boom” portfolio with this level of conviction.

Updated Plan

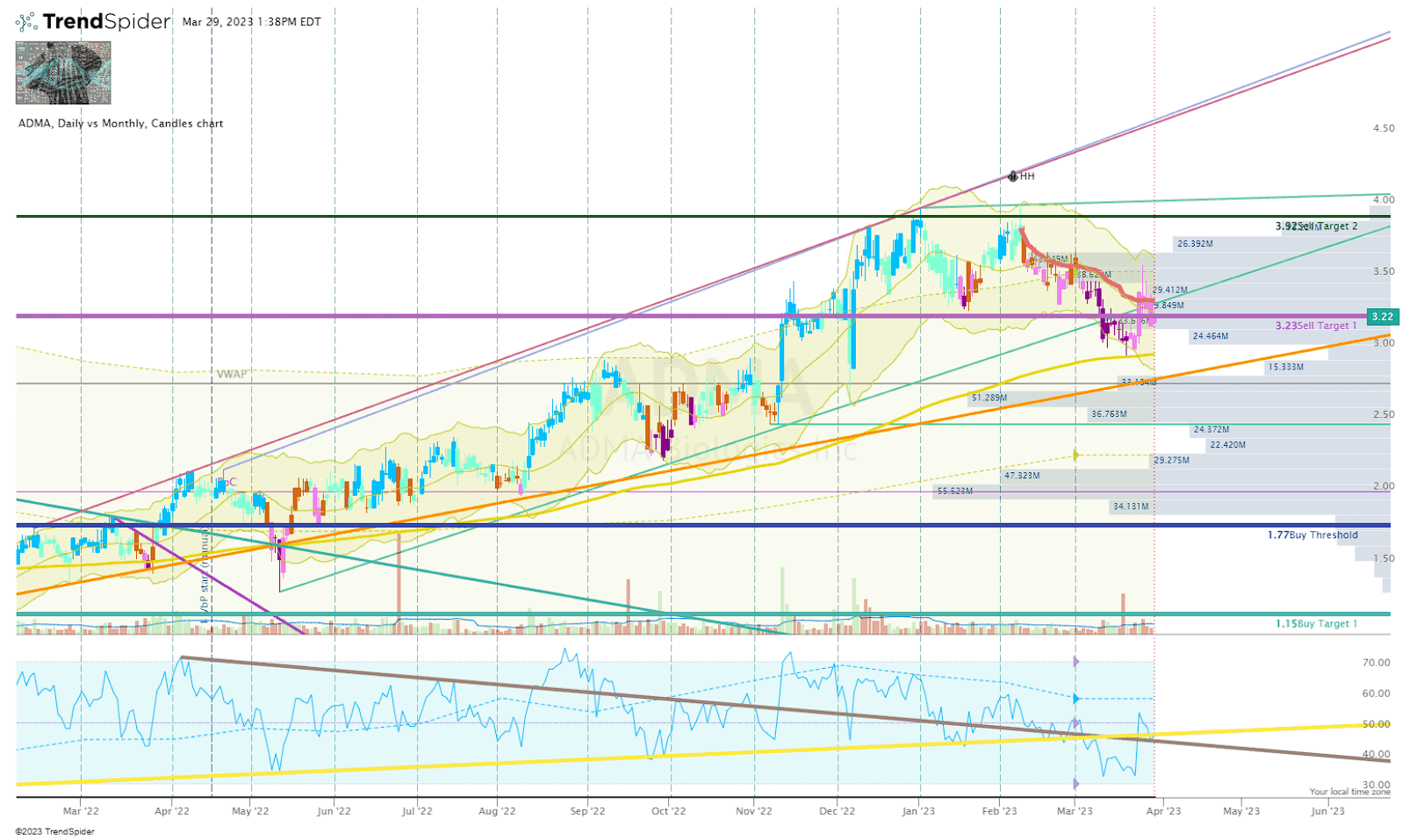

My ADMA position is now a “house money” position after taking profits at my Sell Target 1 and Sell Target 2. Typically, I wait for the ticker to perform a mean reversion and return to my Buy Threshold before I restart my accumulation for another compounding cycle. This time, I am adjusting my Buy Targets and Sell Targets to account for the potential for ADMA to hit the breakeven point in the coming quarters.

{kind=link}

Normally, I use a few different fundamental valuation models or metrics to determine my threshold, however, ADMA is trading at a significant discount for their 2023 revenue estimates. ADMA is trading around a 3.23 forward price-to-sales, which is under the industry’s average of 4x-5x.

{kind=link}

In addition, the ticker’s technicals are indicating it is losing momentum after nearly a year and a half of steadily grinding higher. So, we are getting a bit of a dichotomy that is forcing me to decide to put more weight into the fundamentals or technical analysis.

After some thought, I am going to lean toward the technicals, and will move my Buy Threshold from $1.77 per share to $2.60, and my Sell Target 1 from $3.23, to $5.15 per share. ADMA is currently trading above that Buy Threshold, but below that Sell Target, so I am sitting on my hands for the time being.

For the long-term, I plan on keeping ADMA Biologics, Inc. as a "Top Idea" in my Compounding Healthcare Seeking Alpha Investor Group and will maintain a position for at least five more years in anticipation that the company will hit breakeven in the coming quarters and report a positive EPS in 2024. Subsequently, ADMA Biologics, Inc. will graduate to my “Bioreactor” growth portfolio.

For further details see:

ADMA Biologics: Growth Trends Pointing To Profitability