AMIGF - Admiral Group: On The Right Track Reiterate Buy

2023-09-05 23:46:03 ET

Summary

- Admiral released a generally upbeat set of figures for H1, with strong sequential improvement in most of its business lines after a tough end to 2022.

- The outlook for the all-important U.K. Motor segment should continue to brighten as price hikes feed through and volume declines begin to stabilize.

- The 90% payout policy should remain in force for the foreseeable future; the implied dividend yield is close to 5% for FY23 with attractive growth potential in FY24 and beyond.

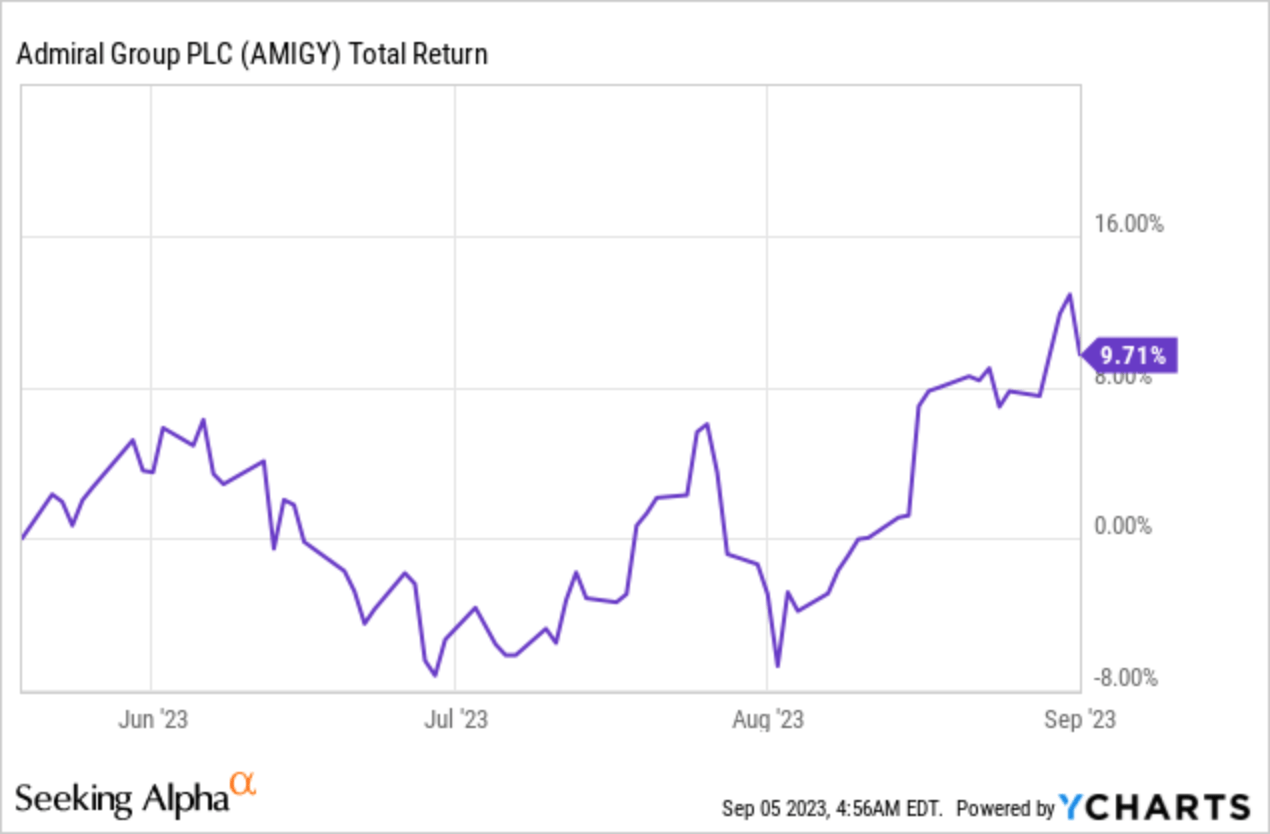

Shares of U.K. motor insurer Admiral Group ( AMIGY ) ( AMIGF ) have performed well since my first piece on the company back in May, gaining close to 10% in both GBP and USD terms inclusive of dividends.

{kind=link}

The buy case for Admiral back then was fairly straightforward: that FY22 would mark a low point for earnings, with that year impacted by a relatively tough macro environment for its motor and non-motor insurance lines.

Results covering the first half of FY23 show that Admiral is on the right track. Profits were up in most of its business segments including U.K. Motor, which is by far the most important part of its business. With the company in position to carry on paying out 90% of its earnings by way of dividends, these shares continue to offer an attractive combination of current yield and growth potential as the earnings recovery continues into H2 and FY24. Buy.

H1 Results Were Solid

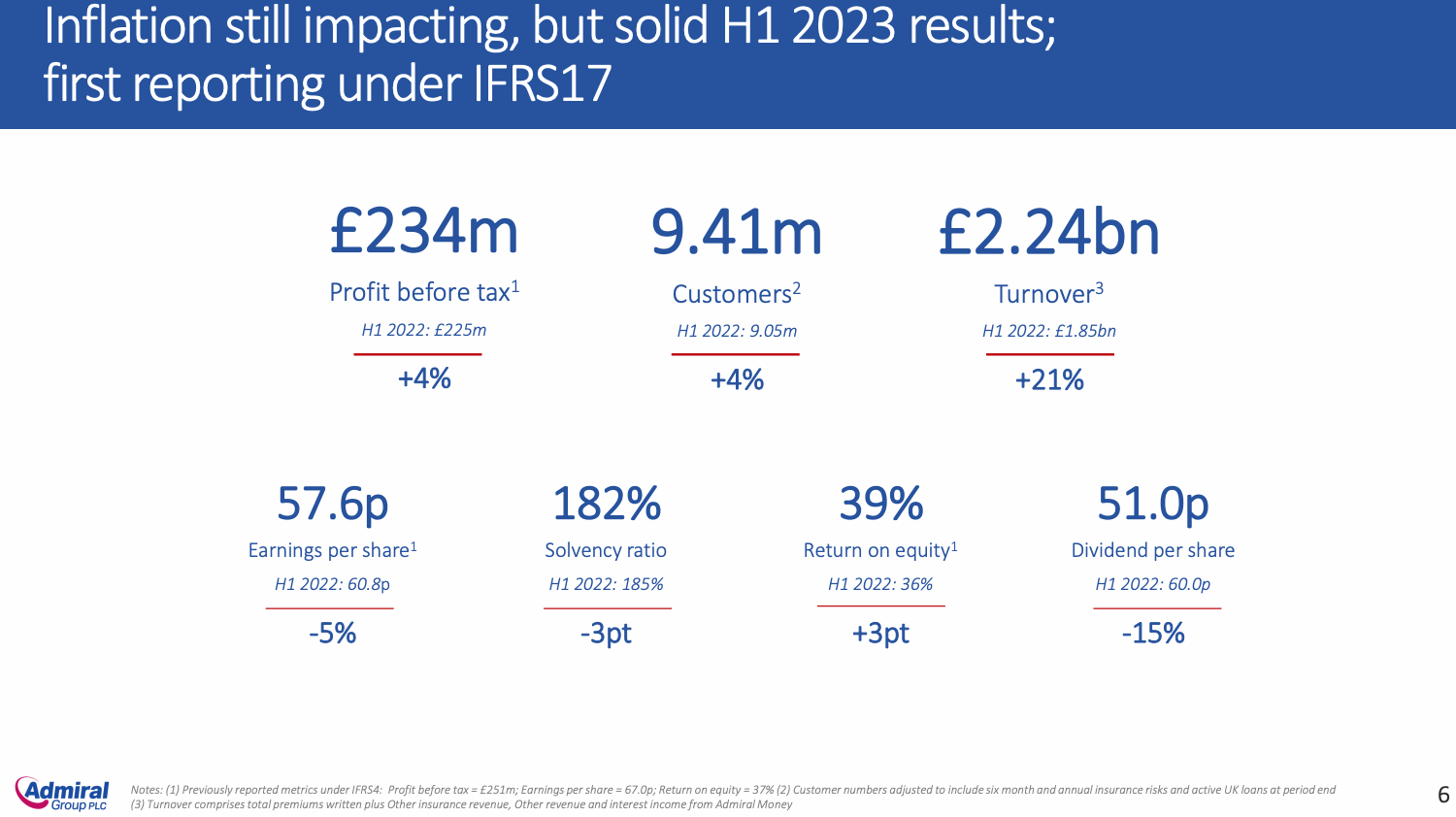

Admiral posted a resilient set of results for the first half of FY23. Although EPS fell 5% to 57.6 pence, this was entirely due to higher taxes as the headline U.K. corporation tax rate increased from 19% to 25%. Underlying profits grew, with group profit before tax ("PBT") up by 4% year-on-year to £233.9m.

Source: Admiral Group plc 1H 2023 Results Presentation

{kind=link}

UK and International insurance, plus Admiral Money, its unsecured consumer lending business, all reported higher year-on-year PBT. International insurance is not a material part of Admiral's overall business - in fact it is collectively loss making - but in FY22 losses widened by a much greater amount than the modest growth reported by U.K. insurance, which itself is driven by U.K. Motor. International Insurance losses narrowed in H1 to £7.6m (versus a £16.9m loss in H1 2022), while U.K. Insurance PBT increased 5% to £303.9m. U.K. Motor, Household and Travel & Pet all showed higher year-on-year PBT. Underwriting results did fall slightly, but this was more than offset by higher investment income due to higher interest rates.

U.K. Motor Outlook Has Improved

U.K. Motor is the most important part of Admiral's business. As a recap, higher claims cost inflation was a material drag on earnings in H2 2022 even though the company was actually quick to raise prices compared to competitors. This is because price hikes only come into effect with a lag, so although Admiral was aggressively raising prices in the middle part of last year this would not affect policies written before then. Raising prices ahead of the market also had an effect on the customer base, with the company seeing the first annual fall in vehicles insured in a decade.

Admiral Group plc: U.K. Motor Vehicles Insured

Data Source: Admiral Group plc Results Releases

{kind=link}

The macro environment for U.K. Motor has begun to improve as expected last time out. The loss ratio before releases did increase 3.1ppt year-on-year (to 92.7% from 89.6%), but remember this represents a significant sequential improvement on H2 2022 given that the full-year loss ratio for FY22 hit 97.8% (implying materially weaker performance in the second half of last year compared to H1).

Source: Admiral Group plc 1H 2023 Results Presentation

{kind=link}

H2 2023 should see further improvement still, with Admiral raising prices by 23% YTD. H2 will also benefit from price hikes that were administered last year, as H1 2023 still contained policies that were written before the company started increasing prices in around March of last year. Claims cost inflation does remain quite high at circa 10%, but management expects this to be weighted more toward H1, implying improvement in the second half of the year.

Volume performance should also start to improve. Vehicles insured did fall another 3.6% sequentially in H1 (to 4.76m), but management has reported tentative signs of stabilization:

Now a key question that you might be asking is when are we going to go back to growth. Good news is that in the past few weeks, we are seeing our number of customers in Motor stabilizing. So we expect to return to growth in the near future. Now exactly when it's hard to tell, and it will depend on what the rest of the market does with prices. We will continue putting pricing up to account for inflation.

Cristina Nestares, CEO Admiral UK, 1H 2023 Earnings Call

There is good reason to take this at face value, as Admiral's volume losses are likely a function of its increasing prices ahead of competitors. With the market now catching up in terms of pricing, Admiral's competitive position will only improve versus peers.

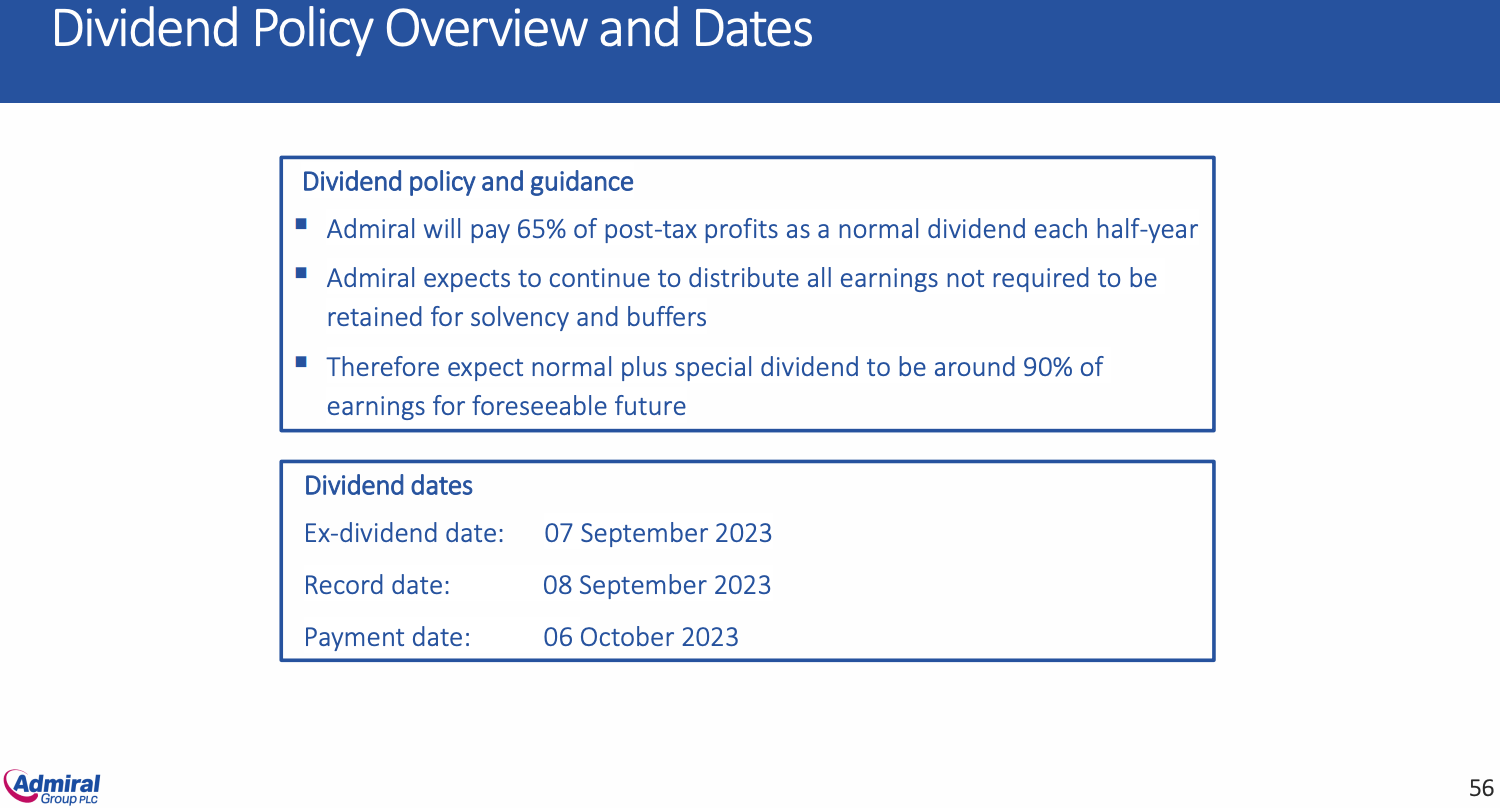

Attractive Dividend Policy Remains In Place

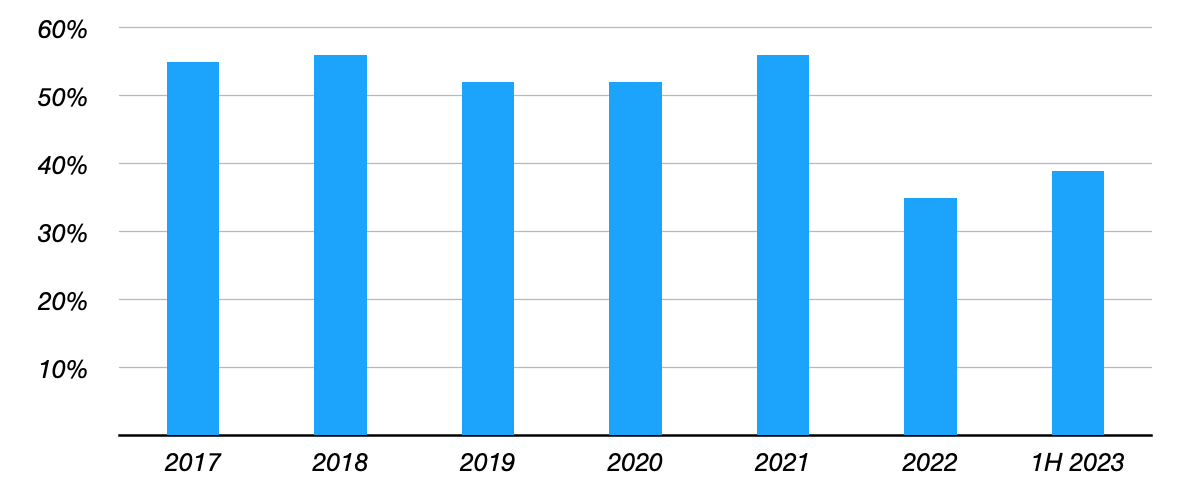

As per last time, Admiral's dividend potential remains highly attractive as its structurally high ROE means it only needs to retain around 10% to fund growth. This results in a very high payout ratio, which is typically 90% of net earnings (65ppt of which is attributable to the ordinary payout and the residual paid out as special dividends).

Admiral Group plc: Return on Equity

Data Source: Admiral Group plc Results Releases

{kind=link}

Special dividends are subject to the usual caveats on solvency and so on, but its solvency ratio of 182% remains well in excess of both the regulatory requirement (by 82ppt) and its own internal risk appetite (by 32ppt). This means the 90% payout policy is likely to continue, as confirmed by management:

Source: Admiral Group plc 1H 2023 Results Presentation

{kind=link}

With H1 results demonstrating that Admiral is on course to resume earnings growth, I am maintaining my EPS estimates for FY23 (129 pence) and FY24 (140 pence) from last time. My DPS estimates are therefore also unchanged at 116 pence (FY23) and 126 pence (FY24) respectively, with both figures assuming a 90% payout ratio. This would map to a 4.9% yield in respect of FY23 given the current 2,372 pence share price in London trading, with around 8-9% growth on top implied for FY24.

I am also sticking with my mid-single-digit per annum longer-term growth target thereafter. This may prove a tad conservative: the pre-COVID FY10-FY19 era was marked by 8.5% annualized EPS growth as per the chart below, but if nothing else it will allow for a margin of safety.

Admiral Group plc: Annual Earnings Per Share

Data Source: Admiral Group plc Annual Reports

{kind=link}

Discounting all that back to the present at a 9% hurdle rate gets me to a fair value of around 2,600 pence ($32.60/per "AMIGY" ADR), implying around 10% upside from the current quote. These shares still hold some capital returns potential, but given the current mid-single-digit dividend yield and the likely resumption of dividend growth they may hold particular appeal to income seekers. Buy.

For further details see:

Admiral Group: On The Right Track, Reiterate Buy