DIISF - Admiral: H1 Results Show Why It Is The Best U.K. Motor Insurance Stock

- Admiral shares rose 12.6% in London on Wednesday after the company released H1 2022 results that were much stronger than expected.

- Uniquely among U.K. motor insurers, Admiral profits were larger than in 2019, despite elevated claim cost inflation so far in 2022.

- We believe Admiral benefited from more disciplined pricing and a narrower past price gap between new business and renewals.

- With large price increases across the U.K. motor sector, we expect customer churn to rise and Admiral to gain share even faster.

- With shares at 2,237.0p, the dividend Yield is 7%, and we expect a total return of 101% (26.3% annualized) by 2025 year-end. Buy.

Introduction

Admiral Group plc ( AMIGY ) shares rose 12.6% in London on Wednesday (August 10) after better-than-expected H1 2022 results.

We upgraded our rating on Admiral to Buy in October 2020. Shares fell to a multi-year low in late July after two of its peers issued profit warnings , blaming elevated claim cost inflation. Even with Wednesday's rebound, Admiral stock remains at a level previously seen in April 2020, representing a loss of 5.7% (after dividends) since our upgrade:

{kind=link}

H1 results strongly support our investment case. Unlike its competitors, Admiral made a bigger profit than in H1 2019, driven by its U.K. Motor business, where underwriting margin was only slightly worse while Admiral's vehicle count has continued to grow. This outperformance likely resulted from disciplined pricing and a narrower historical price gap between new business and renewals. Even more positively, there are signs that the U.K. motor pricing cycle has finally turned, and Admiral should see even faster market share gains from H2 onwards.

Relative to pre-COVID 2019, when Admiral was insuring 19% fewer U.K. vehicles, shares are at a 15.1x P/E. Our updated forecasts show a total return of 101% (26.3% annualized) by 2025 year-end, and a 7.0% Dividend Yield. Buy.

H1 Profits Exceeded Pre-COVID Level

Admiral generated £251.3m in group Profit Before Tax ("PBT") in H1 2022. This was 47.9% down year-on-year, unsurprising given 2021 benefited from significantly lower claim frequency amidst pandemic restrictions. More relevantly, group PBT was 19.4% higher than in H1 2019:

| Admiral Profit Before Tax by Segment (H1 2022 vs. Prior Years) Source: Admiral company filings. |

Group PBT continued to be primarily driven by the U.K. Motor business, where H1 2022 PBT was 25.9% higher than in 2019. H1 2019 U.K. Motor PBT was negatively impacted (by £33.3m) by a government-mandated reduction in the Ogden discount rate used to calculate the present value of future claims liabilities. However, excluding the Ogden rate change, U.K. Motor PBT was still 11% (£32.0m) higher in H1 2022 than in pre-COVID H1 2019.

This was a sharp contrast with Admiral's competitors. Direct Line's ( DIISY ) U.K. Motor business saw a 60% decline in Operating Profit versus H1 2019 while Sabre Insurance ( SBIGY ) saw an 82.6% collapse in its PBT:

| U.K. Motor Profits at Key Players (H1 2022 vs. Prior Years) Source: Company filings. |

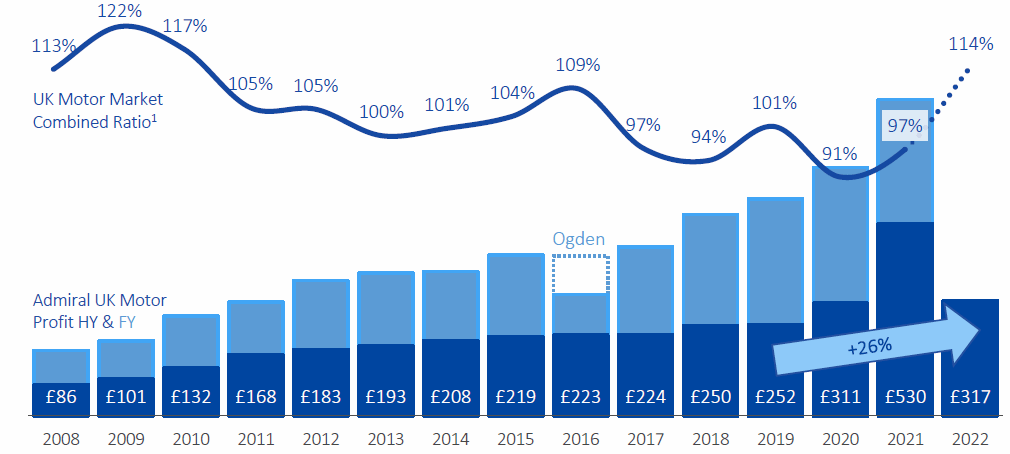

For Admiral, H1 2022 represented a continuation of its unbroken record (except the post-COVID normalization after 2021) in growing its U.K. Motor PBT in absolute terms, irrespective of how the sector Combined Ratio fluctuates:

| Admiral U .K. Motor PBT vs. Sector Combined Ratio ( Since 2008) Source: Admiral results presentation (H1 2022). |

{kind=link}

Admiral's consistent track record supports our belief that its U.K. Motor business is structurally superior to peers.

Digging Deeper Into U.K. Motor Profits

We dig deeper into the H1 2022 U.K. Motor profit to show that it is not distorted by any one-offs.

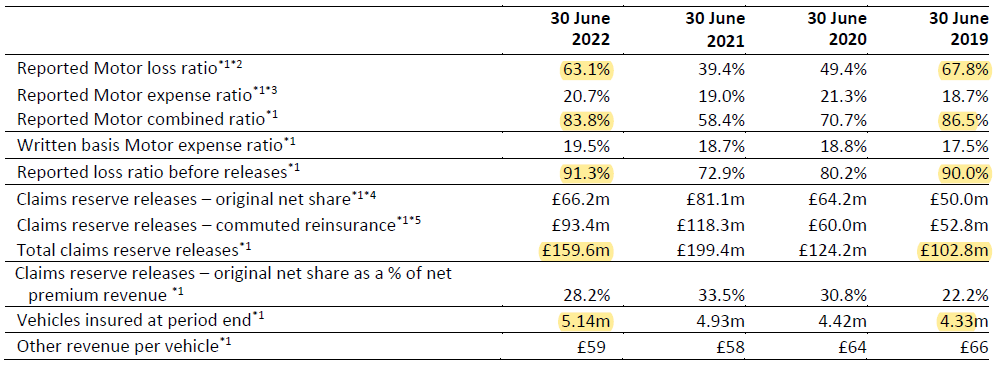

This 11% (£32.0m) growth in PBT from 2019 was the result of several moving parts. In simple terms, Admiral has been steadily insuring more vehicles (H1 2022 period-end vehicle count was 19% higher than in H1 2019 and 4% higher year-on-year), and this growth plus prudent reserving in prior years helped generate £56.8m more in reserve releases in H1 2022, which offset a slightly worse current-year Loss Ratio and lower Other Revenue:

| Admiral U.K. Motor Key Performance Indicators (H1 2022 vs. Prior Years) Source: Admiral results release (H1 2022). |

{kind=link}

Excluding reserves, the Loss Ratio in H1 2022 was 1.3 ppt worse than in 2019 (91.3% vs. 90.0%). Including reserve releases, however, the Loss Ratio was 4.7 ppt better (63.1% vs. 67.8%), and the Combined Ratio was 2.7 ppt better. If we also exclude the 6.8 ppt Ogden rate change impact in H1 2019, then the Combined Ratio was 4.1 ppt worse. However, all these figures show that U.K. Motor's profit margin has only changed modestly since 2019.

Reserve releases were at 28.2% of net premium revenue in H1 2022, larger than in 2019. Management attributed this to prudent reserving, the fading of COVID-related uncertainties, and a smaller denominator. The percentage is expected "to be pretty high for the short term", according to the CFO, which should mean continuing strong profits.

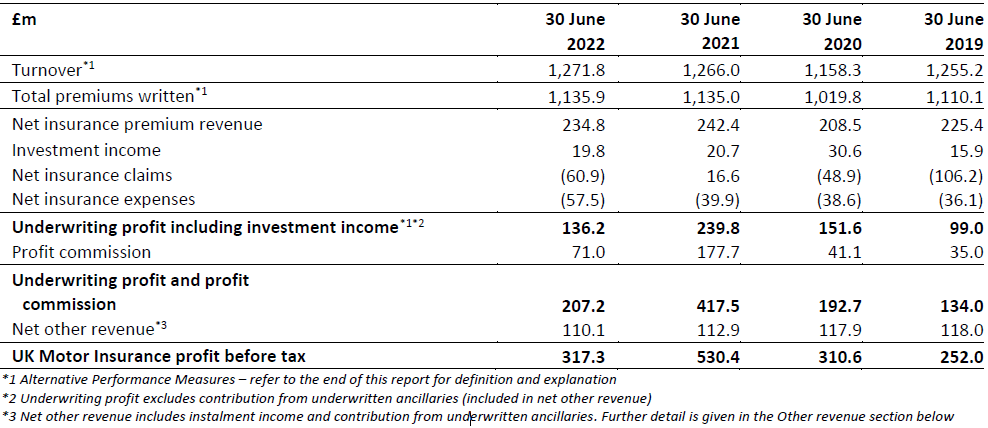

Below is the actual Admiral U.K. Motor P&L. Comparing H1 2022 with H1 2019, Investment Income was £3.9m better but Net Other Revenue was £7.9m worse, largely offsetting each other. Total premiums were only 2.3% higher and, with the Loss Ratio Before Releases only 1.3 ppt worse, underwriting profits before releases were also similar between H1 2022 and H1 2019. So it was higher reserve releases, feeding into both higher underwriting profits and higher profit commissions, that gave U.K. Motor its much higher PBT in H1 2022:

{kind=link}

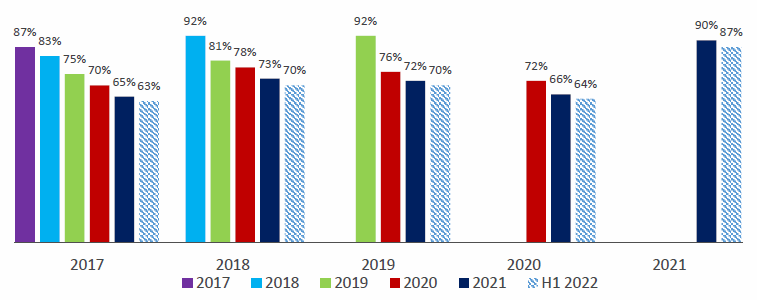

Finally, we look at U.K. Motor's Booked Loss Ratio by underwriting year. This was 93% in H1 2022, within the narrow range of around 90% in the preceding years, except the much better 2020 that benefited from COVID lockdowns:

| Admiral U.K. Motor Booked Loss Ratio by Underwriting Year (2017-21) Source: Admiral results release (H1 2022). |

{kind=link}

Note also the relatively consistent reduction in Booked Loss Ratio for each underwriting year in subsequent years, which is evidence that Admiral has maintained the same underwriting discipline over time.

We are comfortable Admiral did maintain similar U.K. Motor underwriting margins in H1 2022 as in pre-COVID years.

How Admiral Maintained Margins in U.K. Motor

Admiral appears to have maintained its margins in U.K. Motor mostly from disciplined pricing and a narrower historical price gap between new business and renewals. While we believe it has advantages in claims management, Its estimate of current claim cost inflation is 11%, similar to those of its peers.

Disciplined U.K. Motor Pricing

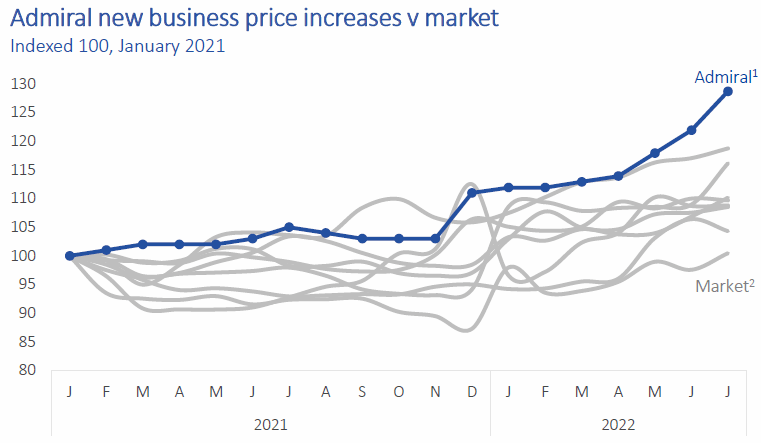

Admiral has largely been pushing higher prices than the rest of the market since 2021, as shown in the chart for new business pricing below (where each grey line represents a competitor). In particular, Admiral raised its prices by 16% (for both new business and renewals) between March and the end of July, taking it even further ahead of the market:

| Admiral U.K. Motor New Business Pricing - Indexed (Since 2021) Source: Admiral results presentation (H1 2022). |

{kind=link}

While year-on-year changes in Admiral's vehicle count (up 4%) and Total Premiums Written (up 0.1%) imply an approximately 5% reduction in average premium in H1 2022, management stated that this was due more to mix than pricing. Admiral's mix shifted towards vans (car-only policy count grew by "less than 3%") and renewing customers (retention rose 7 ppt year-on-year).

Historically Narrower Renewal Price Gap

We believe Admiral also benefited from having a lower price gap historically between new business and renewals.

With the implementation of FCA "price laddering" reforms in January 2022, Admiral has moved its prices in line with the market in the December 2021 to February 2022 period, raising new business prices by double-digits and reducing renewal prices by a mid-single-digit.

Association of British Insurers data showed that, for the market as a whole, the average motor premium in Q1 2022 was 12.8% lower year-on-year. We suspect this means there were larger reductions in renewal premiums among Admiral's competitors outside the December 2021 to February 2022 period. However, a like-for-like comparison is difficult given most companies do not disclose their pricing changes.

Example Comparison with Direct Line Motor

A comparison of U.K. motor underwriting ratios with Direct Line shows how the points above help Admiral in practice:

| U.K. Motor U nderwriting Ratios - Admiral vs. Direct Line Source: Company filings. |

Excluding reserve releases, the Loss Ratio for Direct Line's motor business in H1 2022 was 1.3 ppt worse than in H1 2019, whereas Admiral's was 3 ppt better - we believe this comes from better prices at Admiral this year.

Reserve releases margin for Direct Line's motor business was 3.8 ppt lower in H1 2022 compared to H1 2019, whereas Admiral's was 6.0 ppt higher - likely coming from more disciplined pricing at Admiral in prior years.

Signs That U.K. Motor Pricing Cycle Has Turned

Admiral has observed some signs of the U.K. motor market pricing cycle turning:

We have seen signs of the market increase in prices… for new business, price comparison market has increased 7% prices from March to July"

Cristina Nestares, Admiral's Head of U.K. ( H1 2022 earnings call )

This is consistent with what we have seen at Admiral's competitors like Direct Line and Sabre Insurance, both of which claim to have added price increases during Q2 to fully price in claim cost inflation as of July 2022.

While FCA "price laddering" reforms have customer retention sector-wide and reduced Admiral's new business volume by approximately 17%, management expects churn to increase again with recent price increases. This should enable Admiral to grow even faster, given its record as a consistent net market share gainer.

Businesses Outside U.K. Motor

Admiral's businesses outside U.K. Motor are still small, and are stable in aggregate:

| Admiral P BT Outside U.K. Motor (H1 2022 vs. Prior Years) Source: Admiral company filings. |

U.K. Household PBT was down £7.0m year-on-year, primarily due to a £9.9m impact from storms in H1 2022. Even including this exceptional weather impact, PBT was 64.3% higher than in 2019, as the business has increased its policy count by 59% and premiums by 55% while maintaining a broadly similar Combined Ratio (97.4% vs. 96.9%).

U.K. Travel remained a small business, with a pre-tax loss of £2.4m. Its customer count rose to 340k in H1 2022, compared to less than 100k in prior years. The business is likely impacted by COVID and related travel disruptions.

European Motor PBT shrunk to just £0.2m in H1 2022 due to "accelerated growth, increasing frequency, a weather event in France, and lower average market premiums, particularly in Italy". The business grew its vehicle count by 14% year-on-year in total, including increases in all three of its markets (Spain, Italy and France). Management described all three as "competitive", and Admiral is expanding in new channels such as brokers.

U.S. Motor saw a much bigger loss of £19.8m, despite growing vehicles by 10% and turnover by 16% in USD. The larger loss was "largely due to the very strong increase in severity inflation seen across the U.S. market", where the sector's Loss Ratio rose 14 ppt. Management is taking "strong action", including a price increase of 23% and "substantial tightening of footprint and direct distribution".

Admiral Money broke even for the first time in H1 2022, after growing its loan book by 68% year-on-year to £787m (gross). The business is on track to reach its loan balance target of £800-950m by 2022 year-end, and is expected to see a balance of £1.2-1.3bn in 18 months.

Some of these businesses do have natural synergies with U.K. Motor, though we are more cautious on others. Not all of them will succeed, but losses are limited and they represent an optional upside in the stock.

Valuation: 7%+ Dividend Yield

With shares at 2,237.0p, Admiral is trading at a 15.1x P/E with respect to 2019 and an 11.5x P/E with respect to 2021:

| Admiral Earnings & Valuation (2019-21) Source: Admiral company filings. |

2019 financials are more representative, as 2020 and 2021 benefited from lower claims frequency due to COVID-19; 2021 also included cash proceeds from the Price Comparison Website ("PCW") disposal. However, Admiral now insures 18% more U.K. vehicles than at 2019 year-end and, as described above, PBT was 19% higher by H1 2022.

Admiral's Dividend Yield is somewhat subjective because of the one-off component in recent dividends. The dividend was 140p in 2019 and 279p in 2021, but the latter included 92p funded by the PCW disposal. For H1 2022, the total interim dividend is 105p, or 60p excluding the final 45.0p funded by the PCW disposal; the 60p figure represents a small decline from the 63p declared in H1 2019:

| Admiral EPS and Dividend Per Share ( S ince 2014) Source: Admiral company filings. |

Admiral targets paying out 65% of its EPS as regular dividends and has been paying special dividends every year. Including special dividends but excluding the PCW disposal proceeds, the Payout Ratio has been near 90%. If we apply this ratio to our forecasts, we arrive at dividends of 192.4p for 2022 (including 45p from PCW) and 156.6p for 2023.

On balance, we believe the 2023 forecasted dividend of 156.6p is the most representative. This implies a Dividend Yield of 7.0%.

Illustrative Return Forecasts

We increased our forecasts to reflect better-than-expected H1 results:

- 2022 Net Profit of £490m (was £437m), 10% higher than in 2019

- From 2023, Net Profit to grow at 8% annually (unchanged)

- Share count to grow at 1% annually (unchanged)

- Dividends to generally be 90% of EPS (unchanged)

- 2025 P/E of 20.0x, implying a 4.5% Dividend Yield (unchanged)

Our new 2025 EPS forecast is 12% higher than before (177.2p):

| Illustrative Admiral Return Forecasts Source: Librarian Capital estimates. |

With shares at 2,237.0p, we expect an exit price of 3,978p and a total return of 101% (26.3% annualised) by 2025 year-end.

Conclusion: Is Admiral Stock A Buy?

We reiterate our rating on Admiral Group plc stock.

For further details see:

Admiral: H1 Results Show Why It Is The Best U.K. Motor Insurance Stock