AMIGF - Admiral: Shares At 16x 2022 EPS Likely The Trough This Cycle

2023-03-09 11:24:23 ET

Summary

- Admiral reported 2022 profits despite double-digit claim cost inflation and a key regulatory change, albeit 7% lower than in 2019.

- The core U.K. Motor business had 5% more profits than in 2019, but U.S. losses rose sharply and U.K. Household was hit by extreme weather.

- 2023 should see a substantial improvement in U.K. profits. Industry prices have already risen sharply and inflation is moderating.

- U.S. losses are "expected to strongly reduce in 2023" and the business may be sold. The European business is progressing.

- With shares at 2,003p, we expect a total return of 73% (24.6% annualized) by 2025 year-end. The Dividend Yield is 5.6%. Buy.

Introduction

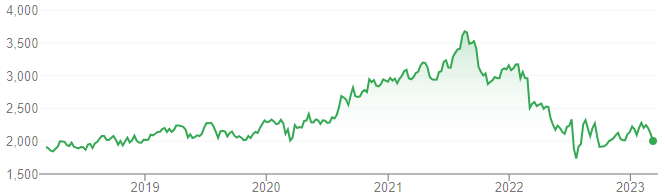

Admiral Group plc ( AMIGY ) released full-year 2022 results on Wednesday (March 8) morning. Shares fell 8% at the open but recovered to finish the day down 4.0%. At 2,003p, they are down nearly 50% from their 2021 peak:

{kind=link}

We upgraded our rating on Admiral to Buy in October 2020, and after Wednesday’s decline Admiral shares are currently down 10% (after dividends) since our upgrade.

Admiral’s 2022 results support our investment case. The core U.K. Motor business was strong, with 5.3% higher profits in 2022 than in pre-COVID 2019, despite double-digit claim cost inflation and a key regulatory change. Group profits were 7% below 2019, largely due to a sharp rise in U.S. losses; in addition, U.K. Household was affected by extreme weather and Europe incurred some costs related to new distribution channels. Management comments indicate that 2022 will be the trough – industry prices have already risen sharply, inflation is moderating and management is taking action to reduce losses in the U.S. (and may sell it). Admiral shares have a 16.2x P/E and a 5.6% Dividend Yield. Our forecasts indicate a total return of 73% (24.6% annualized) by 2025 year-end.

Admiral Buy Case Recap

Admiral is a U.K. insurer with a market capitalization of £5.9bn ($7.1bn). It generates most of its Profit Before Tax ("PBT") in U.K. motor insurance, where it is the market leader. It also offers household insurance, travel insurance and personal loans, and has small presences in Italy, France, Spain and the U.S.

Our investment case centers around the U.K. Motor business, where:

- The sector has continued to grow structurally, with the number of vehicles historically increasing at 1-2% annually, and premiums rising over time due to growing claim costs for both vehicles and medical treatment

- Admiral has continued to gain market share and generate solid profits because its lower Expense Ratio (from scale and efficiency) enables it to offer insurance at lower prices than competitors but achieve higher profits

- Admiral's growth differs during different parts of the insurance cycle, but we believe it can achieve a high-single-digit EPS CAGR. During 2015-19, which we believe represent an entire cycle, U.K. Motor had CAGRs of 6.8% in vehicles and 8.2% in both total premiums and profits

- 2022 regulatory reforms requiring insurers to offer the same prices to new and existing customers will lead to higher pricing on new business, improve sector profitability and entrench leaders like Admiral

Admiral's other businesses are small and generated just £5.2m in PBT in aggregate in 2021; some are loss-making. They can potentially create significant value in the long term, but this is not in our investment case.

COVID-19 boosted profitability for the whole motor insurance sector, because less driving meant fewer accidents, more than offsetting lower premiums and higher cost inflation. Admiral’s group PBT grew 52% between 2019 and 2021, primarily driven by higher profits in U.K. Motor. However, since 2021, driving frequency has begun to normalize while claim cost inflation has become even more elevated, creating pressure on industry profits.

Admiral’s 2022 results reflect the same dynamics, with a strong performance from its core U.K. Motor business.

Admiral 2022 Results Headlines

In 2022, Group PBT fell 39.0% year-on-year after an exceptionally strong 2021 (due to COVID-19 restrictions reducing claim frequency); compared to pre-COVID 2019, Group PBT was 7.1% (£36.1m) lower:

| Admiral K ey P&L Items (2022 vs. Prior Years) Source: Admiral company filings. |

The core U.K. Motor business generated 5.3% (£31.1m) more PBT in 2022 than in 2019. However, Group PBT was dragged down by sharply higher losses (£39.3m worse) in the U.S., as well as moderate deteriorations in the U.K. Household (£13.8m worse) and European (£10.6m worse) businesses.

The results were a demonstration of the underlying strength of Admiral’s U.K. Motor business, while weaker performances in its other businesses were either due to one-off factors or are in the process of being remedied.

Strong Core U.K. Motor Business

Admiral’s core U.K. Motor business remained strong in 2022, despite double-digit claim cost inflation and a key regulatory change.

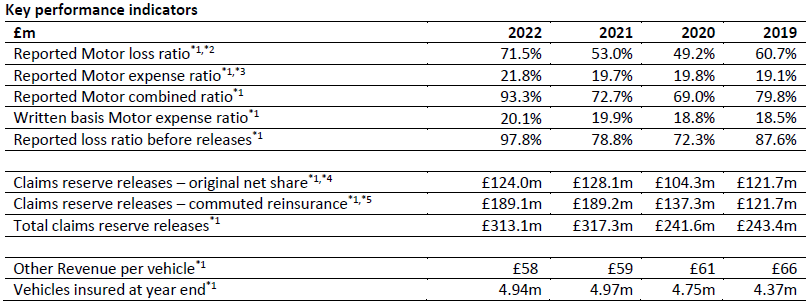

Combined Ratio was 93.3%, indicating a still positive profitability, compared to 79.8% in 2019:

| Admiral U.K. Motor Key Performance Indicators (2022 vs. Prior Years) Source: Admiral results release (H1 2022). |

{kind=link}

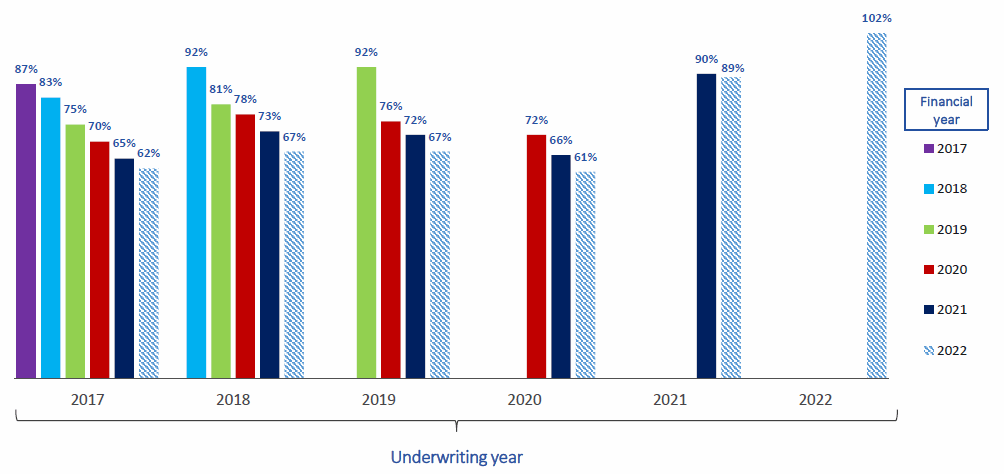

Loss Ratio was 71.5% after releases. Reported Loss Ratio Before Releases was 97.8%, 10 ppt worse than the 87.6% figure in 2019. Similarly, the year-1 Booked Loss Ratio for 2022 was 102%, 10 ppt worse than in 2019:

| Admiral U.K. Motor Booked Loss Ratio by Underwriting Year (2017-2 2 ) Source: Admiral results presentation (2022). |

{kind=link}

Profitability on policies written in 2022 (and 2021) should end up better than their initial Booked Loss Ratios indicate, though with a smaller improvement than for previous underwriting years.

For every underwriting year, insurers typically book a higher Loss Ratio that includes reserves based on conservative estimates of actual losses, and then release reserves and reduce the Booked Loss Ratio when actual losses turn out to be smaller than estimated. For example, the Booked Loss Ratio for the 2019 underwriting year was 92% in year 1 but has now been reduced to 67%, indicating a profitable Combined Ratio of about 87% (assuming an Expense Ratio of around 20%). The Booked Loss Ratio for the 2021 and 2022 underwriting years should improve for similar reasons.

However, with claim cost inflation being much higher than expected in 2022, Booked Loss Ratios for the 2021 and 2022 underwriting years are likely to improve much less than for previous underwriting years. Already the Booked Loss Ratio for 2021 has shown a much smaller year-2 progression. This will be a temporary headwind for Admiral’s profitability in the next few years, offset by continuing reserve releases from the stronger years before 2021.

Admiral CFO Geraint Jones reassures investors on this subject on the earnings call :

“What we would say is that there is plenty of reserve release to come on years that are currently enormously profitable. So 2019 and 2020 underwriting years, for example, we'll still continue to release ... But this is a cyclical business at the end of the day. And '21 and '22 underwriting years will be lower profitability underwriting years than the preceding ones, influenced by the pandemic partly…. beyond that, really, we've got plenty of reserve releases to come”

Expense Ratio was 20.1%, only 20 bps worse year-on-year despite overall U.K. inflation running at about 9%.

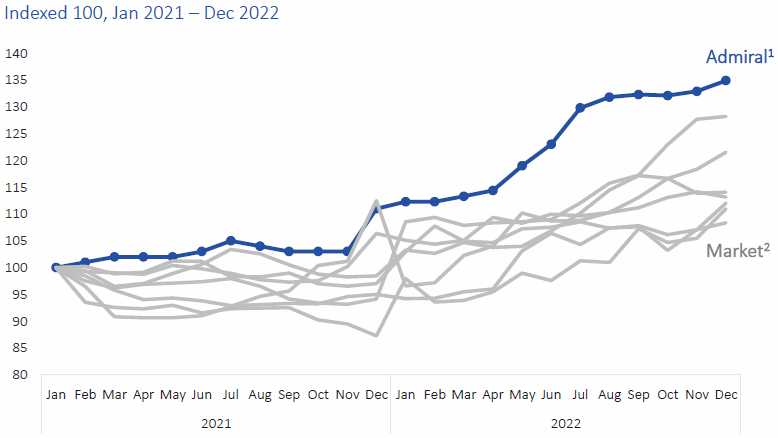

Vehicles Insured was 4.94m at 2022 year-end, down 0.6% year-on-year and down 3.9% from H1 2022. 2022 was the first year since 2013 when Admiral’s U.K. vehicle count did not grow. Admiral has raised its new business prices significantly ahead of the market since March 2022, and this has cost it a small amount of market share.

| Admiral U.K. Motor New Business Pricing – Indexed (Since 2021) Source: Admiral results presentation (2022). |

{kind=link}

Other Revenue Per Vehicle , which consisted of revenues from ancillary and other products, administrative fees and interest on installment payments, again declined slightly, though they rose slightly on a net basis after internal costs.

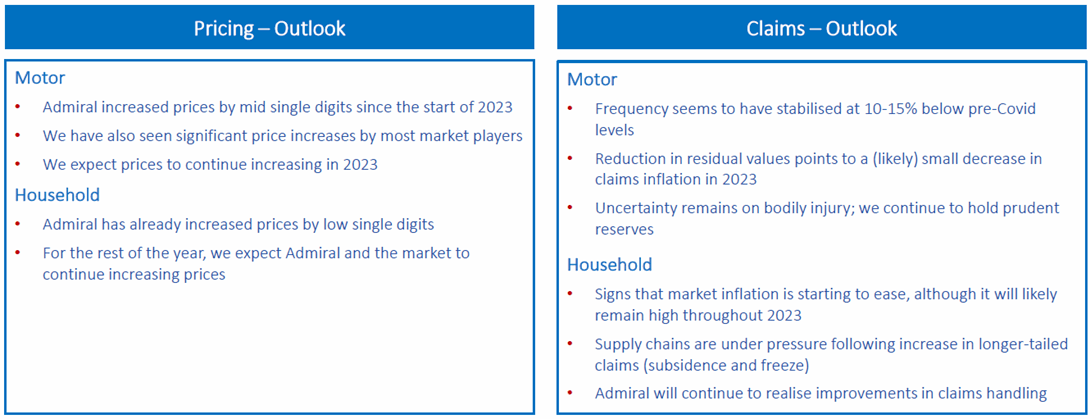

U.K. Motor Profitability to Improve in 2023

Management believes 2022 will be the trough year in U.K. insurance profitability, thank to prices having risen sharply and inflation moderating. Claim frequency has also stabilized.

“We think 2022 is the worst year in the cycle, and we expect a better outlook for '23.”

Cristina Nestares, Admiral Head of U.K. (2022 earnings call)

In U.K. Motor, Admiral started 2022 by raising new business prices by double-digits and reducing renewal prices by mid-single-digits, in response to the new FCA “price walking” ban (implemented in January 2022) that requires insurers to offer the same pricing to new and renewing customers. Subsequently, from March 2022, Admiral has raised its prices by around 25% for both new business and renewals.

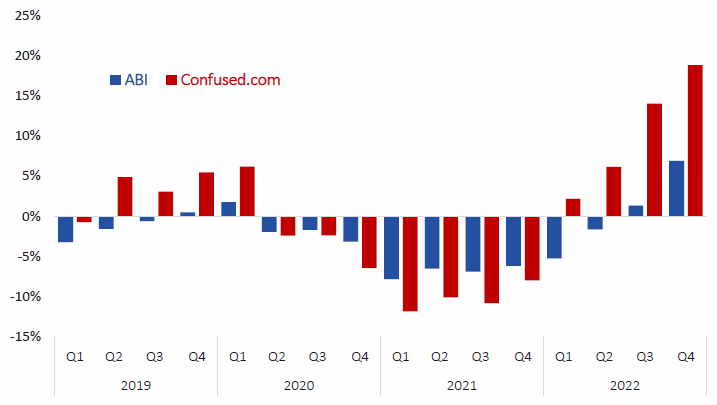

Industry prices have also risen sharply, with new business prices (as measured by Confused data) having risen by 19% year-on-year and renewal prices (as measured by ABI data) having risen by 7% as of Q4; this includes sequential rises of 7% and 8% respectively in Q4. Admiral expects “prices to continue increasing in 2023”.

| U.K. Motor Insurance Industry Premiums Year-on-Year Change (2019-22) Source: Admiral results presentation (2022). |

{kind=link}

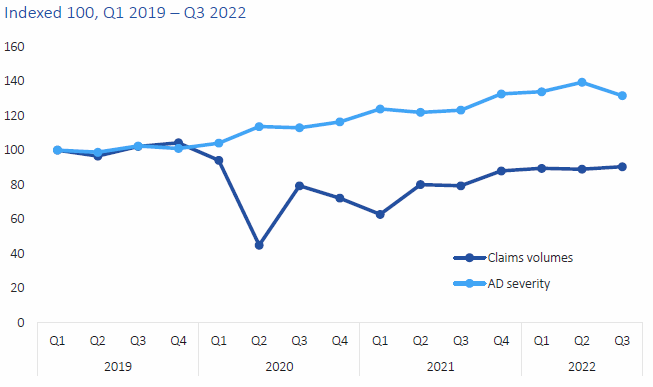

Claim cost inflation has started to moderate. Overall claim cost inflation is estimated to be running at 11%, unchanged from H1 results. Residual car values, a leading indicator for property claim costs, have started to decline, though third-party property damage costs may continue to accelerate for a time due a time lag associated with their processes.

| U.K. Motor Industry Accidental Damage Frequency & Severity (since 2019) Source: Admiral results presentation (2022). |

{kind=link}

The cost of small bodily injuries will likely benefit from recent “whiplash reforms” following a recent court case on multi-site injuries. The cost of long-term care has experienced similar inflation to overall wages, but affects Admiral much less because these costs are concentrated in a small number of cases already covered by excess of loss reinsurance.

Claim frequency was 10-15% below COVID levels in 2022 and appears to have stabilized there.

Sharp U.S. Deterioration Will Be Remedied

Admiral’s U.S. business deteriorated sharply but this will be remedied, potentially with a sale.

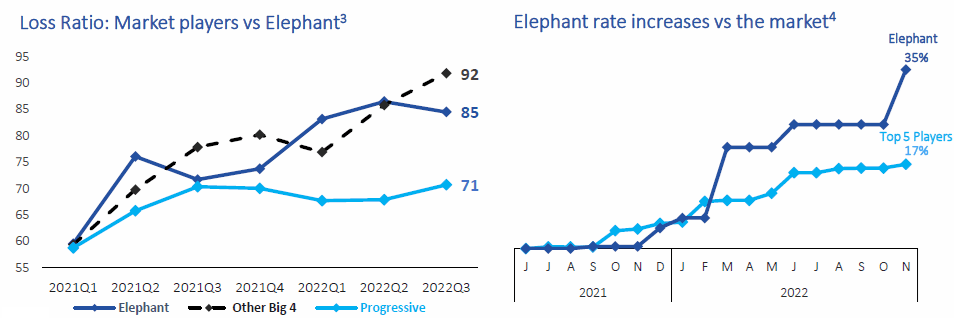

Losses at Elephant, Admiral’s U.S. business, jumped from $17.8m in 2021 to $60.6m, despite significant price increases. In addition to the same claim cost inflation issues described above, management also blamed a larger time tag in price hikes (due to U.S. regulations) and a change in reinsurance arrangements at the start of 2022 (that reduced Admiral’s capital requirement but increased its share of losses). Elephant also has a relatively large cost base, given its turnover of just £268.5m, which means a disproportionate impact from any fall in underwriting margins.

| Admiral U.S. Loss Ratio & Price Increases vs. Peers (Since 2021) Source: Admiral results presentation (2022). |

{kind=link}

Admiral has taken significant actions to reduce Elephant’s losses. Prices had been raised by 35% by November, acquisition spending was cut by 41% and the underwriting footprint was reduced. Management stated that “losses are expected to strongly reduce in 2023”.

Management also indicated the business may be sold. The results release acknowledged that the U.S. “is a challenging market … for which we are considering options”. CEO Milena Mondini said on the call:

“At the moment we are early stage exploring a very large set of options. Nothing is off the table”

We believe the U.S. business is an unprofitable distraction and any sale would be viewed positively by the market.

U.K. Household Affected by Extreme Weather

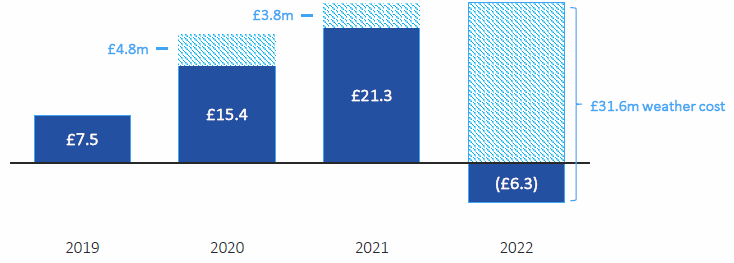

Admiral’s U.K. Household business went from a £21.3m PBT in 2021 to a £6.3m loss in 2022, entirely due to weather costs jumping from less than £5m in prior years to £31.6m, related to extreme weather in the U.K.

| Admiral U .K. Household PBT vs. Weather Costs (2019-22) Source: Admiral results presentation (2022). |

{kind=link}

Excluding severe weather and subsistence costs, U.K. Household would have had a Combined Ratio of 92.7% (compared to 98.0% in 2019). The business has continued to expand, expanding its customer count from 1.01m in 2019 to 1.58m by 2022 (growing 0.26m in 2022), and its Net Written Premium by 49% in the same period.

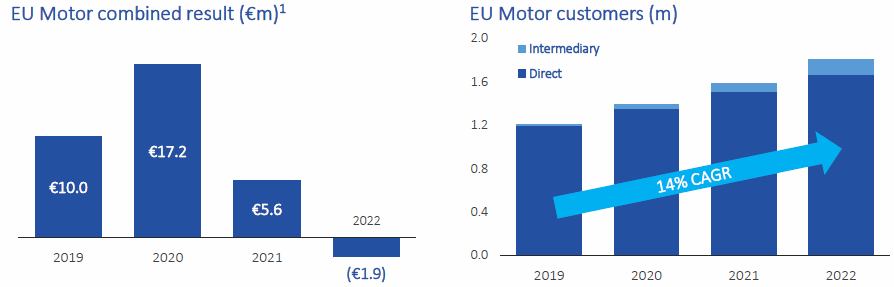

Europe Swung to Loss After Investments

Admirals’ European business swung from a €5.6m PBT in 2021 to a €1.9m loss in 2022, affected by the same claim cost inflation issues described above as well as €3-4m of costs invested into new distribution channels. The vehicle count grew by 13.9% across Europe (and grew in each of the 3 markets), despite 10%+ price increases.

{kind=link}

We believe Admiral’s European expansion makes more business sense than its U.S. venture, though its contribution remains marginal. We expect profitability to improve in 2023 and, at worst, it will make another small loss.

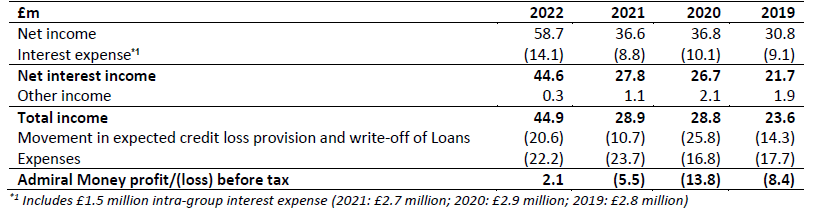

Admiral Money Has Turned Profitable

Admiral Money generated a £2.1m PBT in 2022 as revenues continued to grow on relatively fixed expenses:

{kind=link}

Admiral’s loan book grew 46% in 2022 to £888m, and is expected to grow to £950-1,000m in 2023. Credit losses are a risk but credit provisions are already at 7.2% (£63.7m). Cost/Income ratio of 49.4% is comparable to good U.K. banks.

Admiral Money is likely to be using Admiral’s own capital (the group’s investment portfolio is only £3.71bn and mostly in investment-grade bonds or equivalents), which implies a low Return on Equity (“ROE”) at present, but we expect Admiral to utilize third-party funds for this business at some stage, which would improve the ROE significantly.

Admiral 2023 Forecasts

Admiral expects “slightly better market conditions” in 2023, with continuing industry price increases in both Motor and Household, and a slight easing of inflation from current high levels:

{kind=link}

CEO Milena Mondini explicitly referenced a reverting of the insurance cycle and Admiral’s ability to benefit from it:

“The market trends we are observing over the past few months allow us to believe that the insurance cycle in the U.K. market is likely reverting. And with the underwriting discipline we showed this year, we are well positioned for that.”

We expect U.K. Motor PBT to continue to grow, driven by recent and ongoing price increases, U.S. losses not to repeat their 2022 highs and no extreme weather losses in U.K. Household this year. Applying reasonable assumptions we believe Group PBT will recover by 20% year-on-year in 2023:

| Admiral Profit By Segment (2021-23E) Source: Admiral company filings, Librarian Capital estimates. |

U.K. corporation tax is set to rise from 19% to 25% this year. Admiral’s effective tax rate has been higher than the U.K. headline rate, partly due to the non-tax-deductibility of U.S. losses. Net of the higher tax rate, we believe Admiral’s Profit After Tax can still recover by nearly 12% in 2023.

Admiral Group plc Valuation

With shares at 2,003p, Admiral has a 16.2x P/E on 2022 financials:

| Admiral Earnings & Valuation (2019-2 2 ) Source: Admiral company filings. |

2022 Net Profit was 16% lower than in pre-COVID 2019 despite Admiral insuring 13% more vehicles in the U.K., primarily due to a large U.S. loss and extreme weather in the U.K. as described above.

Admiral has declared 112.0p of dividends for 2022, which represents a 5.6% Dividend Yield. This represents a 90% Payout Ratio on 2022 basic EPS (124.2p), in line a 90-95% long-term target (management is guiding to 90% at present). An addition 45.0p will be paid as the third and final distribution of sale proceeds from the Price Comparison Website business.

Admiral’s Solvency Ratio was 180% at 2022 year-end, compared to a 150% target.

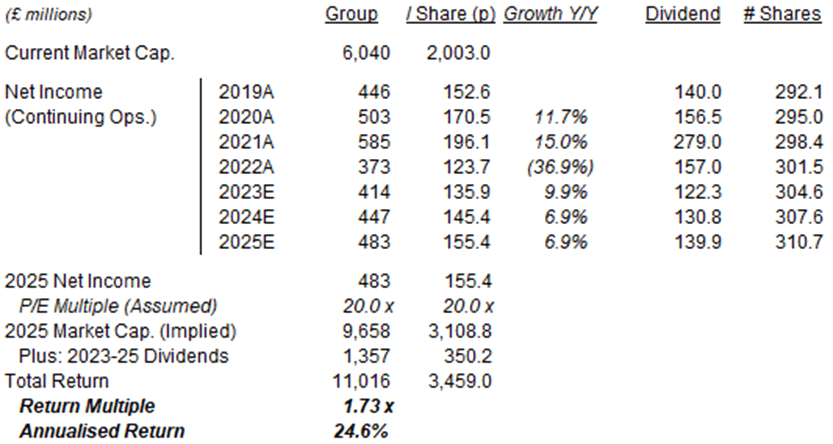

Admiral Return Forecasts

Admiral’s 2022 Net Income was 17% lower than we expected, though largely due to one-offs.

We reduce our 2023 forecasts to reflect a slower recovery. Our assumptions now include:

- 2023 Net Income to be £414m (was £529m), 11% higher year-on-year

- From 2024, Net Profit to grow at 8% annually (unchanged)

- Share count to grow at 1% annually (unchanged)

- Dividends to generally be 90% of EPS (unchanged)

- 2025 P/E of 20.0x, implying a 4.5% Dividend Yield (unchanged)

Our new 2025 EPS forecast is 22% lower than before (was 198.7p):

{kind=link}

With shares at 2,003p, we expect an exit price of 3,109p and a total return of 73% (24.6% annualized) by 2025 year-end.

Conclusion: Is Admiral Stock A Buy?

We reiterate our buy rating on Admiral Group plc stock.

For further details see:

Admiral: Shares At 16x 2022 EPS, Likely The Trough This Cycle