IWM - ADP Jobs Blowout Improves Risk/Reward For Non-Farm Payrolls Report Tomorrow

2023-07-06 15:40:21 ET

Summary

- The U.S. market experienced a selloff on Thursday, with the VIX spiking to its highest level in months before retreating significantly. I believe this collapse in volatility is bullish.

- Many Dow components have behaved as if a recession is priced in, but increasing odds of avoiding a recession could lead to a significant upside. The upcoming Q2 earnings season could see many cyclical companies outperforming on earnings.

- There are potential risks that could derail his bullish thesis, including escalation in Ukraine or Taiwan and Fed policy errors.

Markets sold off Thursday, and the S&P VIX Index (VIX) spiked to its highest level in months. As of 2 pm, the initial spike had retreated significantly, and markets were off their lows. The infamous fear index reached levels above $17 but then retreated back to the lower end of the $15 handle. This collapse in volatility is bullish, and I think it will resume Monday.

{kind=link}

I think many Dow Jones Industrial Average Index (DJI) components have behaved as if a recession is priced in, but the increasing odds that we avoid a recession would likely lead to a significant upside. I am preferential to the bullish thesis that we avoid a recession, or if we have one, it will be a minimum duration and severity. And if the consumer is still standing, then SPDR® Dow Jones Industrial Average ETF Trust (DIA) components can outperform expectations.

Seeking Alpha

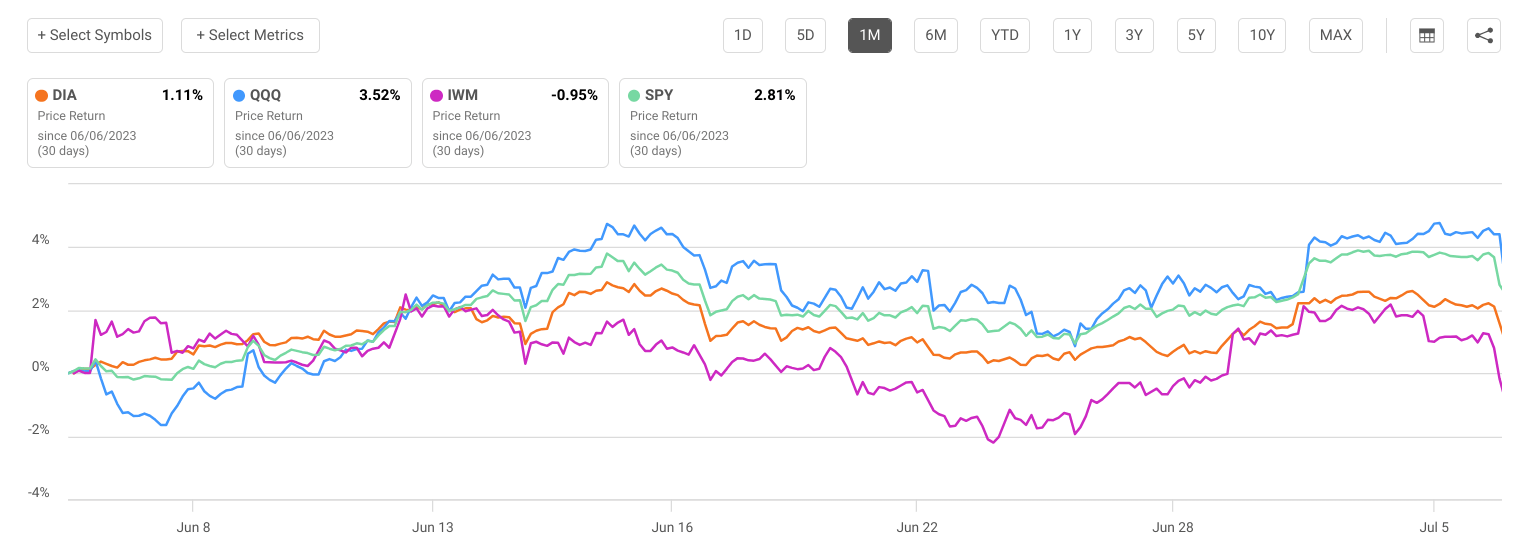

As the focus comes off of the Fed and whether there are one or two hikes left, which ultimately is a lot less consequential than the attention it gets implies, the Quarter 2 earnings season will resume. Despite frustrated bears saying that the rally was led by only large Tech stocks, over the last month, both the small-cap Russell 2000 Index (RTY) and the more cyclical Dow Jones Industrial Average have been leaders.

- The extreme strength in the economy will create an opportunity for many cyclical companies to outperform on earnings in the upcoming season.

- The persistent economic strength of the U.S. consumer will eventually come into starker relief if earnings expectations are raised after Q2 results.

- The Fed is the most powerful actor in the market, but it is not omnipotent; the strength of the economy is ably pushing back against monetary policy.

- This may eventually become a problem if it reignites inflation expectations, but it will be months before we know if that is occurring, and there'll likely be a lot of gains between now and then.

I know the implications of a strong labor market and what that could mean for the Fed hiking, but I also am starting to see so much strength in the economy that the Fed's hikes might not do much to derail it. There is also building evidence that despite the strong report that caused markets to sell off this morning, traditional labor market correlations used to inform policy may be less useful in the current environment.

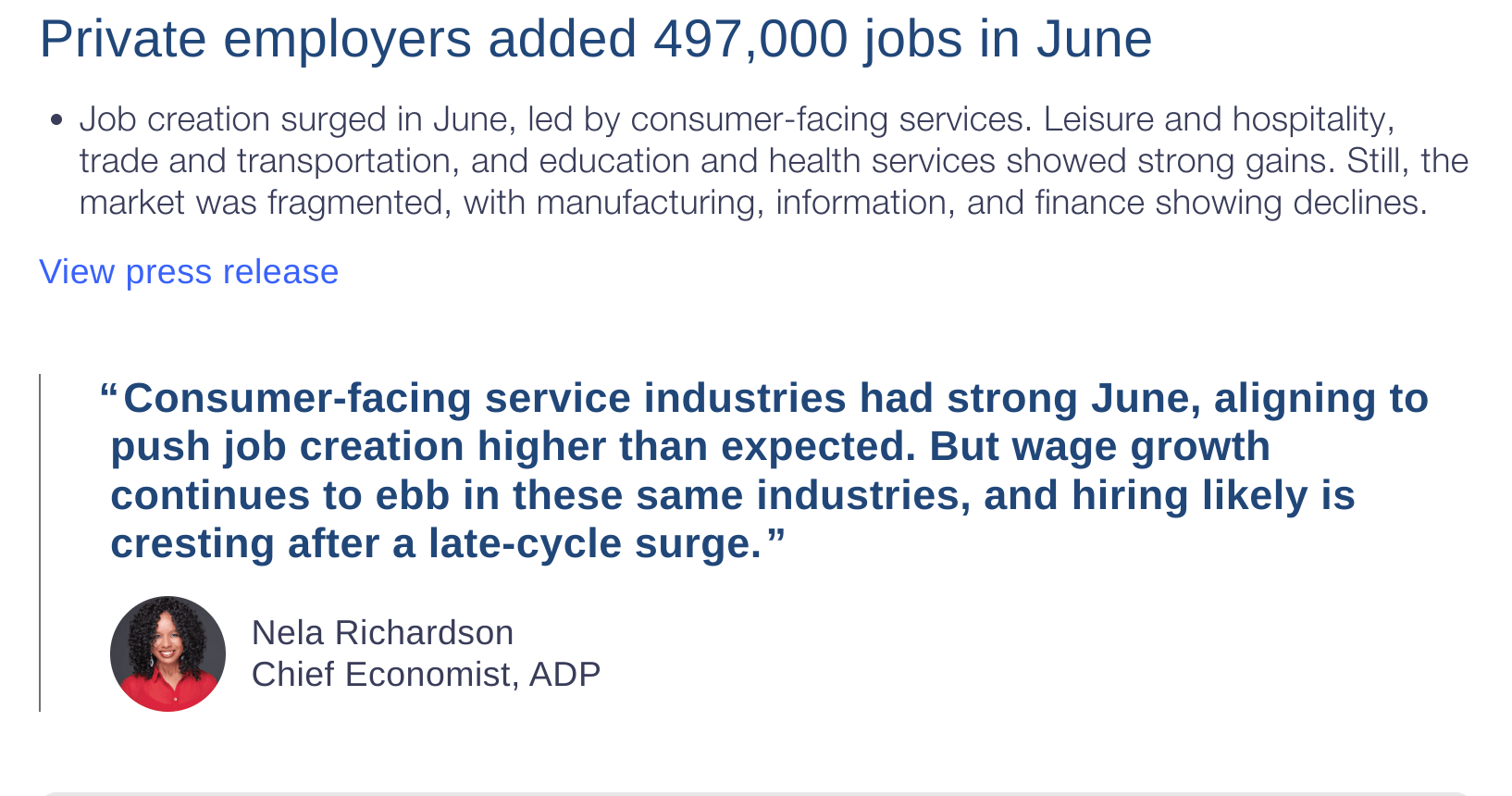

The usually innocuous ADP Report startled markets this morning after their projections were far too low. The actual gains in jobs were more than twice what was expected. One of the reasons the market freaked out is because this report has typically been reporting fewer job gains than the more important Payrolls report that comes out tomorrow.

{kind=link}

The logic of the market reaction is since this report has been lower than the nonfarm payrolls, tomorrow could be a major wake-up call for the Fed on the strength of employment. However, something that was very improbable yesterday has become a lot more likely today. The market could rally tomorrow on a hot nonfarm payrolls report.

Given the exorbitant miss today, if there's a marginal surprise to the upside, I think the market still rallies, particularly since Fridays have typically seen volatility collapse. This makes the risk/reward going into tomorrow's report much more favorable. Remember, the market freaked out today, but there are many reasons why nonfarm payrolls could not echo the pattern seen over the previous month.

In an uber-bullish scenario, a reading that is lower than expected tomorrow could lead to a substantial rally that not only reverses today's reversals in stocks but leads to new local highs. But for there to be a major selloff tomorrow, I think what would be needed would be a miss that is way outside of expected numbers like that which occurred in the ADP report, which is possible but necessarily likely.

Economic Strength Making Soft, or No, Landing More Likely

The upcoming Nonfarm Payrolls Report and Unemployment number have an added importance as it is one of the last major data points before the Fed's next meeting on July 25-26. Labor has become particularly important as a gauge for the Fed, and it is even more so now that the Fed meeting minutes have shown a divided Fed .

- Most members are convinced more hikes will need to take place this year

- Most members appreciate policy has become near sufficiently restrictive, and the pace should be slowed

- Whether or not the labor market shows persistent strength will be key to the Fed's decision on hikes later this month.

- Remember, normally, strong employment is good, but in this case, it means the Fed will raise rates more, which diminishes economic activity.

- This means, counterintuitively, that a weaker employment reading showing a greater balance between job vacancies and job seekers would be welcome for markets.

I think there's building evidence that reporting anomalies may have been making the labor market look stronger than it has been in reality. This would mean the Fed is closer to restrictive than some of the more hawkish members on the committee might have thought. Markets sold off on Thursday

The economy has been very strong lately, coupled with positive news on inflation, which has been somewhat of a "Goldilocks" scenario for the stock market. Here is some of the recent data supporting a new bull market has begun:

- The recent PCE reading , the Fed's preferred inflation gauge, came in at the lowest reading since April 2021, but the core elements remained sticky.

- Durable goods orders experienced a high-than-expected rise last month.

- Economic numbers were revised higher , and strength in the labor market was shown with low layoffs.

- Strength in the housing market has been particularly notable given the environment of high rates and that an earlier slump has reversed.

- Consumer confidence also reached a 17-month high.

- Stock market performance has been broadening out in the Nasdaq ( QQQ ), and the Russell 2000 ( IWM ) has begun participating as well.

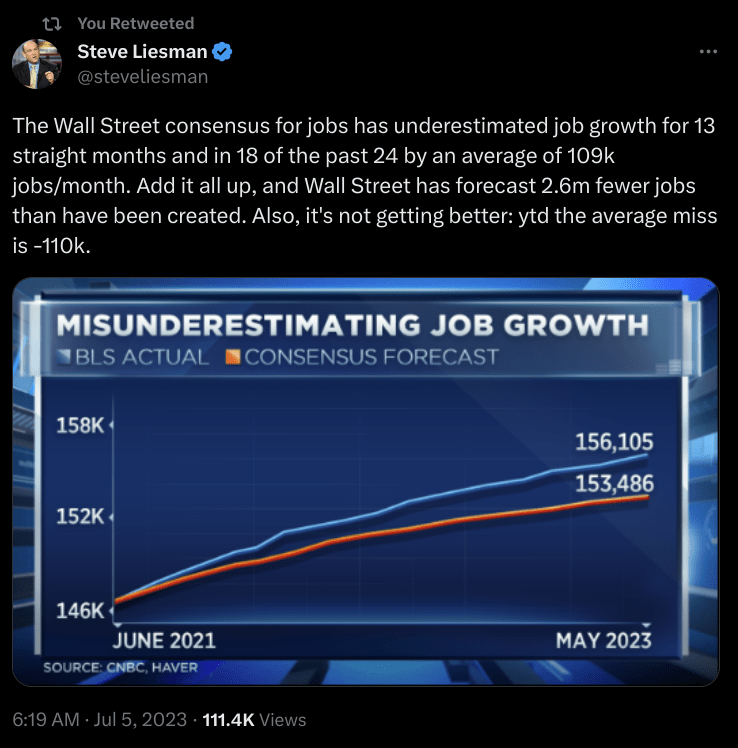

This nonfarm payrolls report, in particular, has been confounding experts over the past months. As CNBC Economist Steve Liesman pointed out below, there has been a significant undershooting of expected payroll results versus actual results.

{kind=link}

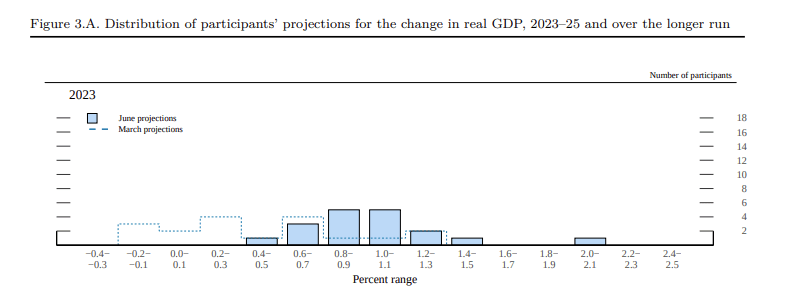

While nearly all members agreed on the June pause, nearly all members also now agree that further hikes will be needed before the year is out. One of the confusing things, though, is that the Federal Reserve has gotten considerably more optimistic about the economy from the March SEP to the June SEP, as you can see below.

{kind=link}

This seems to imply the committee is mostly concerned that persistent economic strength has a chance to reignite inflationary pressure if the gas is taken off the peddle too quickly. Data has been seemingly contradictory in several areas.

Risks and Where I Could Be Wrong

The jobs market is particularly hard to predict. I am certainly not a labor economist, and my honest opinion is that I don't have any better idea of what the jobs report will bring tomorrow than you do. However, I do try to pay attention to market volatility around data releases. I get the sense that the risk/reward favors the bulls tomorrow after the ADP release. However, I could definitely be wrong.

My recent market calls have rested on an assumption, and that assumption is that we will either avoid recession completely or that it will be very shallow and of minimal impact. If anything derails this thesis, then much of the rally is probably at risk, and new lows are even possible.

The exacerbation of any of the below risks could cause my thesis to be painfully wrong.

- Escalation in Ukraine or Taiwan.

- Fed Policy Error.

- Banking Issues Worsen.

- Return of Inflation.

- CRE meltdown.

- Write-downs of Private Assets.

However, my belief that the unforeseen blowout today in the ADP numbers reduces the potential for adverse market reactions to the numbers tomorrow should withstand even the emergence of these risks, and it is a very short-term thesis built on building economic strength. I am confident in issuing a BUY on the Dow because cyclical economic strength is underappreciated and all the data keeps telling us to respect it.

Conclusion: Fulfilling a Mandate that Demands Precision With Blunt Tools

While the blunt force trauma the tool can cause is certainly awe-inspiring, it is not generally precise. Without the direct enforcement mechanism of the Reg Q ceiling that used to exist, the Fed is much more dependent on maintaining the psychological upper hand against the market. What does it look like when the Fed loses the upper hand and when the market is "fighting the Fed?"

Well, the verbal lashing Fed Chair Powell gave at the Jackson Hole Summit is a good example of what Powell can do with the considerable market bully pulpit he has as master of rates. Still, ultimately the Fed is more powerful than any other market participant, but it is certainly not all-powerful, and that is an important distinction.

{kind=link}

But still, as powerful as the Fed is, managing the world's largest economy and having a great effect abroad simultaneously demands the precision skills of Tiger Woods, and what Congress has given the Federal Reserve makes it more ungainly on the course, like the famed fictional character Happy Gilmore. Powell and friends have a monstrous drive, but the Fed has historically lacked in its short game like Mr. Gilmore.

The question will be whether or not the Fed has learned to put. I think their handling of the banking crisis using new tools that weren't previously available shows the committee has more precise methods available than before. This, paired with building economic strength from the alleviation of COVID dynamics and a strong US consumer, means that for the short and medium term, the price movement in DIA is likely to the upside.

For further details see:

ADP Jobs Blowout Improves Risk/Reward For Non-Farm Payrolls Report Tomorrow