ADTLF - Adriatic Metals: One Of Few Outperformers Lately

2023-04-05 17:49:17 ET

Summary

- The Vares project continues to be on track for the first production in Q3-23.

- The stock price has more than doubled from the lows in 2022, which is far better than most comparable mining companies.

- The risk-reward looks relatively attractive despite the recent strong stock price performance.

Investment Thesis

Adriatic Metals ( ADMLF ) is a polymetallic development company, with about 50% of projected revenues coming from precious metals, that is in the process of commissioning its Vares mine in Bosnia and Herzegovina in 2023. The company is listed in Australia, UK, and has an OTC listing in the U.S.

{kind=link}

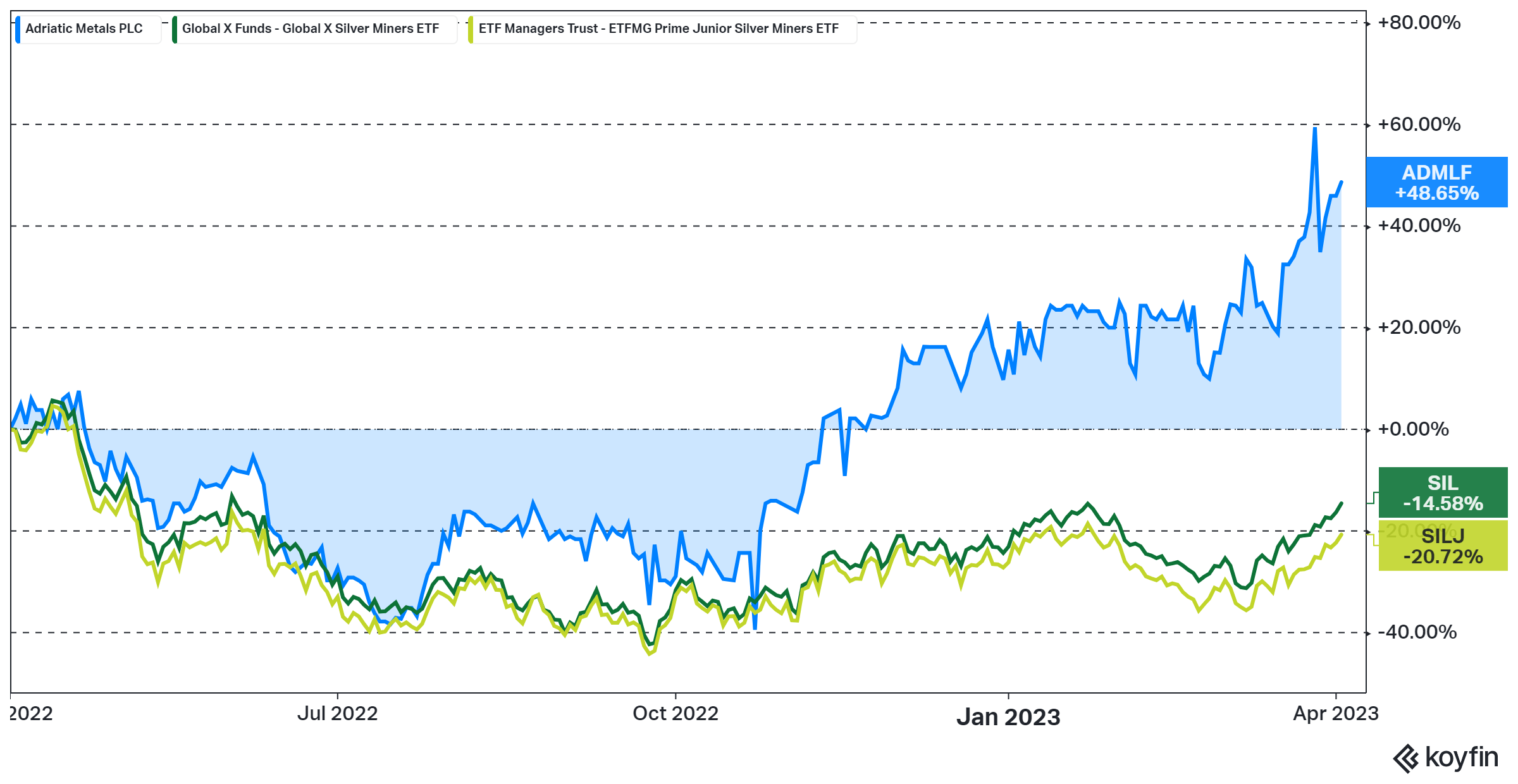

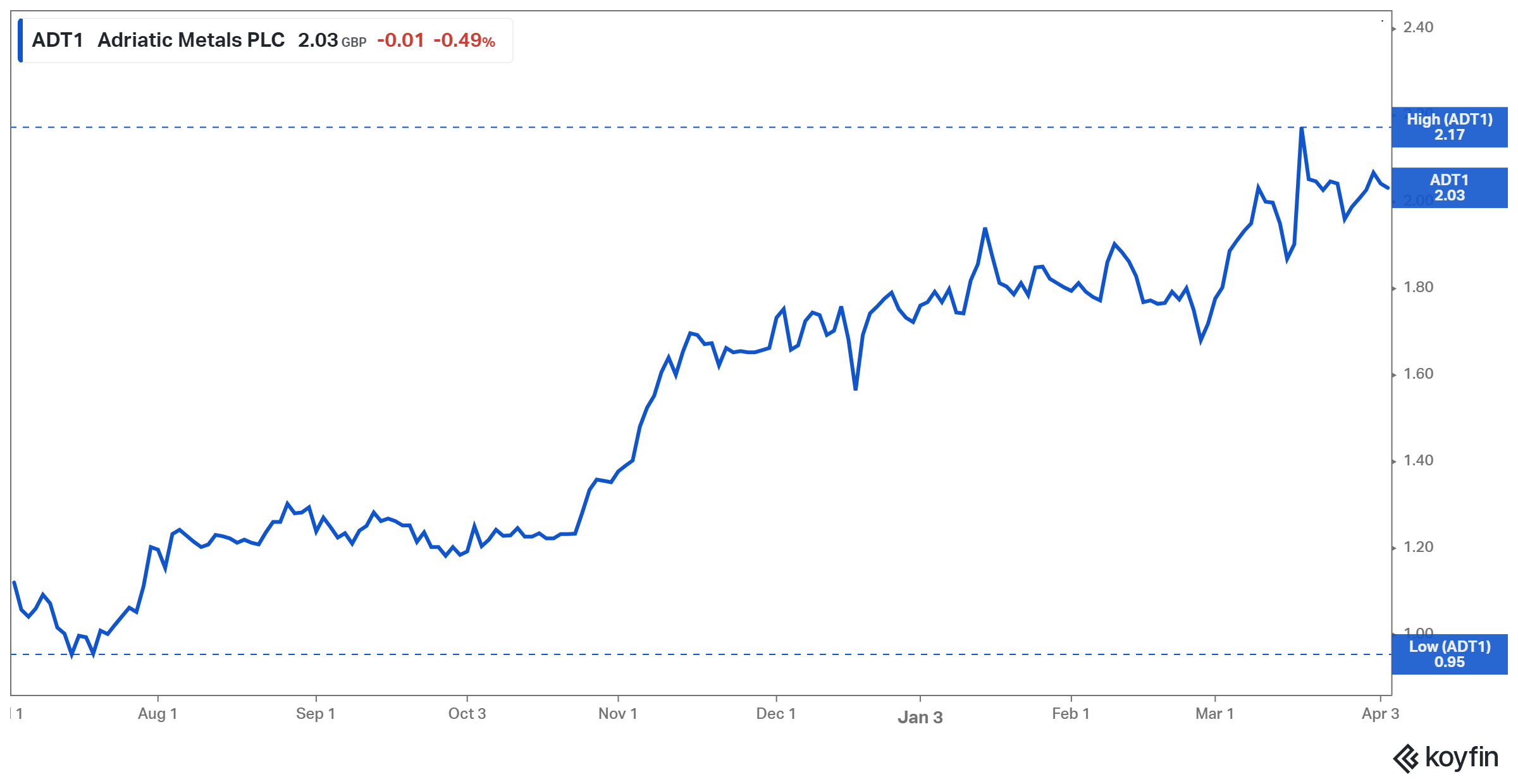

I have covered the company in the past and the stock has returned 60% since my strong buy article in October of last year. Adriatic Metals is one of the few precious metals development companies that has had a good performance over the last year. It has outperformed most silver miners by quite a lot. Note that some development companies have underperformed the producers over that period, so the relative outperformance against some other developers is even larger than what the chart above indicates.

Figure 2 - Source: My long Adriatic Metals article return

{kind=link}

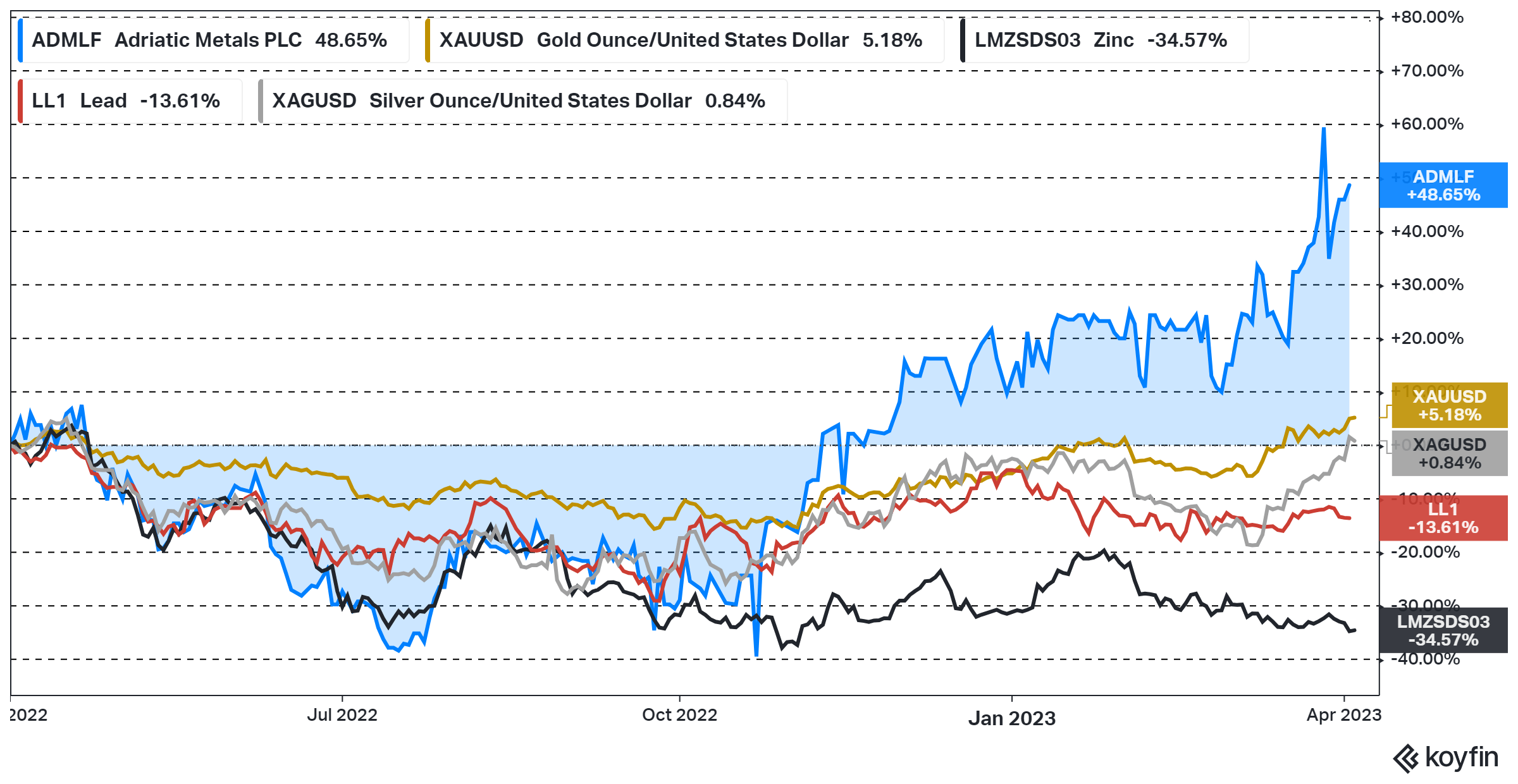

Also, the prices of the main base metal components of the project: zinc and lead, have declined over the last year, so the NPV of the project has not been getting a boost from there lately.

{kind=link}

I have recently liquidated my holdings in Adriatic Metals to invest in peers with even more depressed valuations. That said, Adriatic Metals is far from expensive at this level, provided the commissioning and ramp of Vares goes according to plan in 2023. The share price is just not as depressed as we saw during part of 2022.

Vares Update

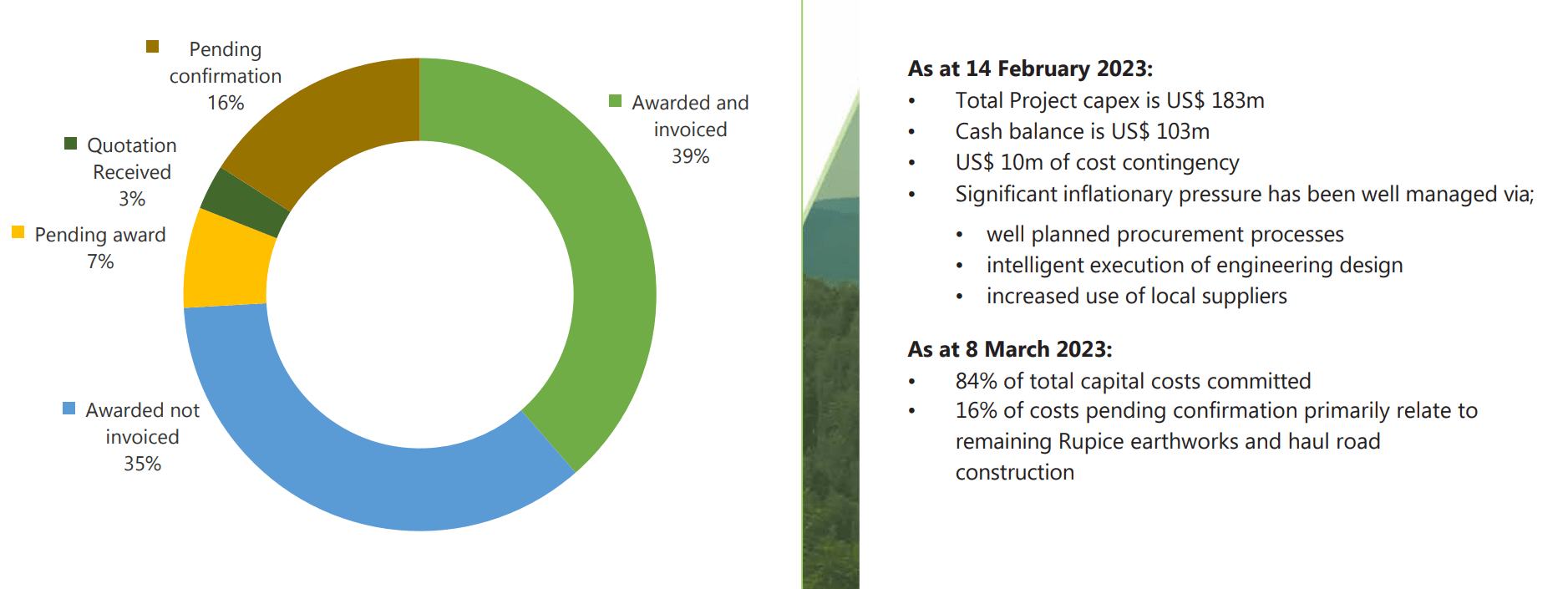

Vares was about 60% complete in January, where only 16% of total cost is now pending confirmation. That means there is very little chance for any substantial cost overruns at this stage.

Figure 4 - Source: Adriatic Metals Presentation

{kind=link}

Total project capex is now estimated to be $183M, which is about 9% above the initial estimate in the feasibility study . The company has in my view done an excellent job keeping costs under control in the current inflationary environment.

While I am not overly concerned about a larger cost overrun, we have still seen supply chain issues in many parts of the world. So, there is always a chance of delays due to some critical components missing. Adriatic Metals has a decent size cash buffer on top of the contingency, so if delays were to happen, that would be very manageable for the company.

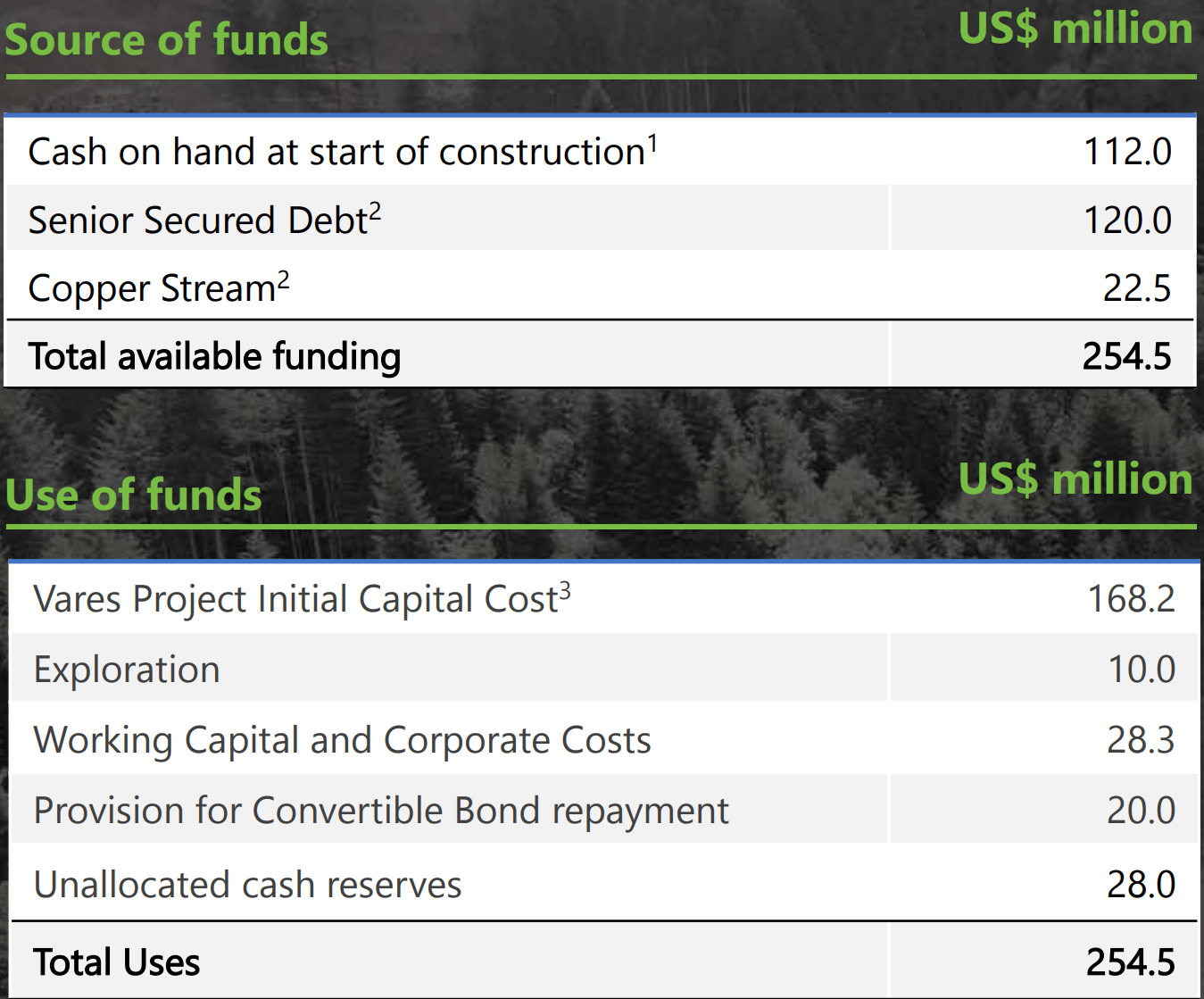

Figure 5 - Source: Adriatic Metals Presentation

{kind=link}

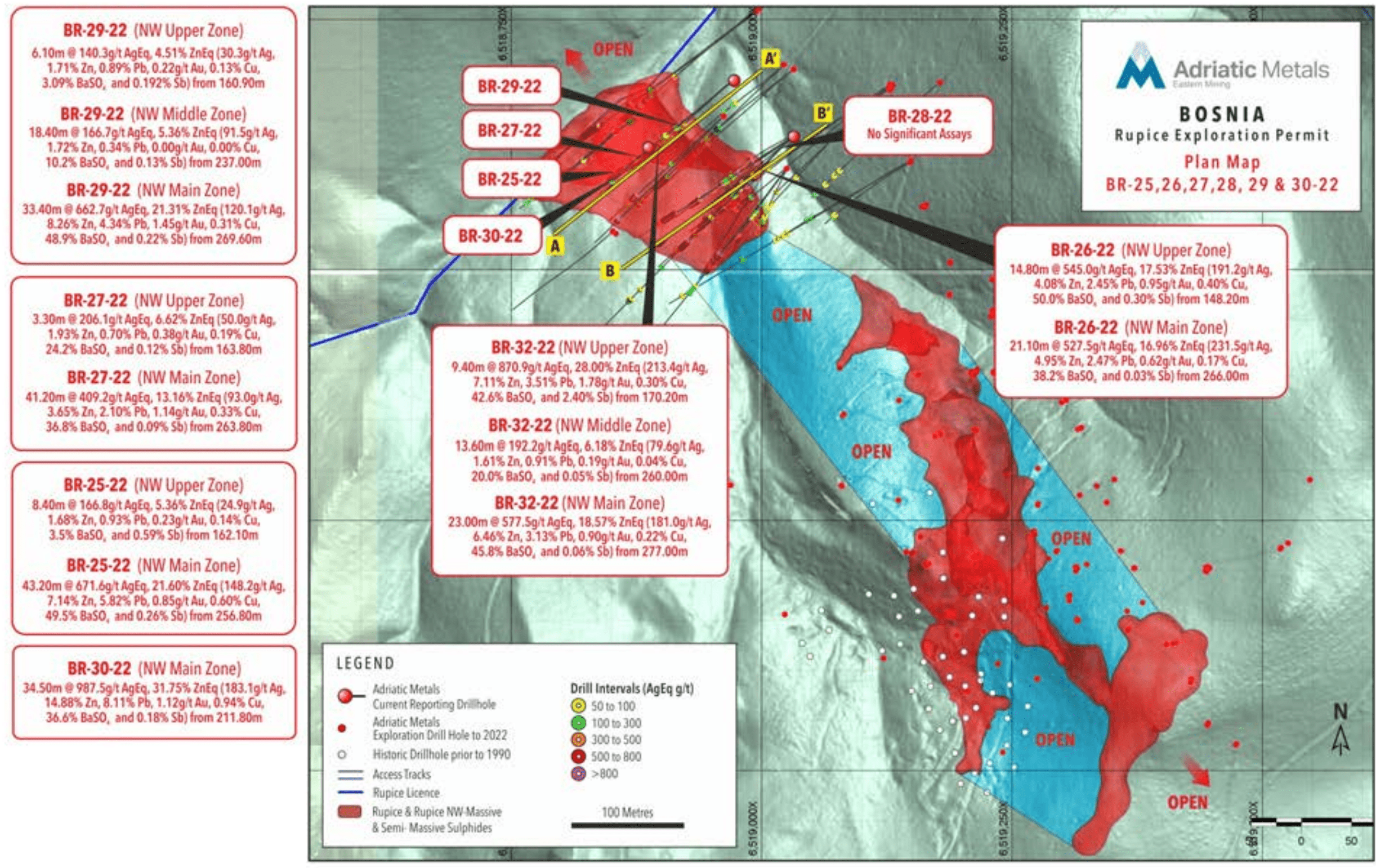

Another positive aspect with Adriatic Metals is the ongoing drilling at Vares, where the results have continued to be very good. There is a resource update due to be released around Q2-Q3 2023. So, the total resource is likely to expand this year as are reserves, with some conversion from resources. Exactly how much resources and reserves will grow, remains to be seen, but there is a good chance the growth will be substantial based on what we have seen from the exploration results.

Figure 6 - Source: Adriatic Metals Presentation

{kind=link}

Valuation

Adriatic Metals has a fully diluted share count of 291M, which in turn gives us a market cap of around $720M using the latest share price. The company will also have a manageable debt load of around $120M once Vares is in production.

For the valuation, I have relied on the NPV in the feasibility study, then adjusted for the changes in commodity prices since it was released. The commodity prices I have used today are the following: gold $2,000/oz, silver $25/oz, zinc $2,800/t, and lead $2,100/t, which are close to today's spot prices.

We then get an estimated NPV of $1,026M. So, we are consequently looking at a market cap to NPV of 0.7.

Conclusion

A market cap to NPV of 0.7 is far from expensive for a project that is about to start producing, with very healthy growth prospects going forward as well. However, the attractiveness has decreased compared to nine months ago, when the stock was trading at about half the current stock price.

{kind=link}

Commissioning and ramping up production from a mine are far from riskless, where it is common to see both delays and prolonged periods before reaching nameplate capacity.

Another minor concern is the fact that about half of the projected revenues come from base metals, where the near-term future looks more uncertain, even if that is more of a subjective opinion.

If one were to look purely on the absolute risk-reward for Adriatic Metals, it still looks relatively good, but the fact is that there are many other precious metals miners, with less base metal exposure, that are trading at much more depressed levels than Adriatic Metals. So, I have recently sold my holdings in Adriatic and deployed the money elsewhere, where the risk rewards are in my view even more attractive.

For further details see:

Adriatic Metals: One Of Few Outperformers Lately