AZO - Advance Auto Parts: Attractive Valuation After Losing Half Its Value In 2023

2023-08-09 14:41:16 ET

Summary

- Following a full-year guidance cut in May 2023 and a 35%+ drop post-earnings, we believe current share price levels for Advance Auto parts reflect an attractive valuation.

- AAP’s business is supported by favorable automotive aftermarket trends, including record high average vehicle age and strong used vehicle sales.

- Recent dividend cuts (~$297 million annually) and expected reductions in CapEx (~$150 million over the next year) will free up cash and give Advance the breathing room it needs.

Editor's note: Seeking Alpha is proud to welcome Sample Space Research as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Introduction

Following a full-year guidance cut in May 2023 and a 35%+ drop post-earnings, we believe current share price levels of Advance Auto Parts (AAP) reflect an attractive valuation (both historically and relative to peers) with most if not all the downside already baked in. Recent dividend cuts (~$297 million annually) and expected reductions in CapEx (~$150 million over the next year) will free up cash and give Advance the breathing room it needs to transition to higher-margin, owned brands .

AAP's business is supported by favorable automotive aftermarket trends, including record high average vehicle age and strong used vehicle sales.

Thesis

{kind=link}

When evaluating an investment opportunity, we believe it is critical that investors consider the risk-reward tradeoff of the opportunity under consideration. Like buying a home, you want to know what the last buyer paid per unit of measurement. With this information in hand, you establish somewhat of a mental floor for what you would be willing to pay for your new purchase. With this concept in mind, AAP is a great deal at its current price relative to its historical valuation and relative to the recent performance of its peers. Note, the valuation metrics and scenarios discussed herein reflect the full-year guidance cuts as part of their most recent earnings release, and the stock's closing price as of August 4, 2023.

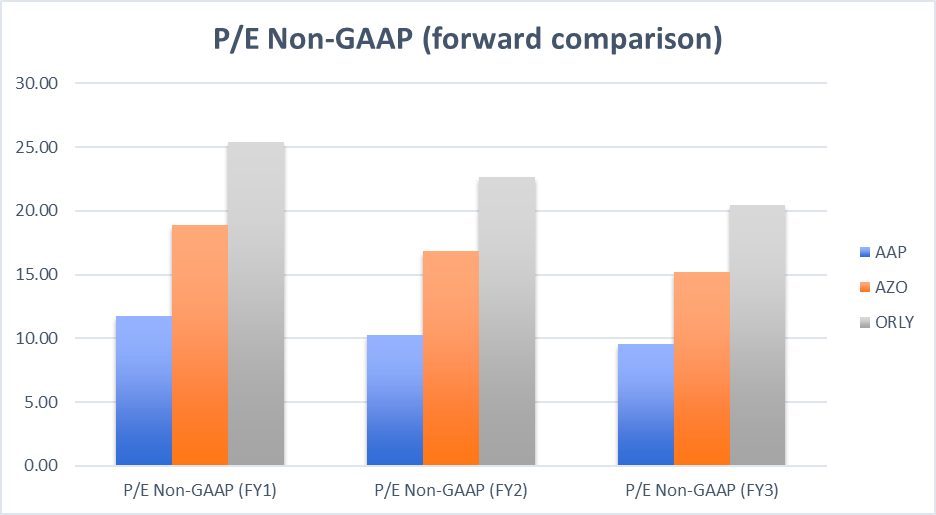

Following such a drastic move lower in the stock of AAP year-to-date ("YTD"), we see that the stock is trading at ~12x forward GAAP earnings, or 30% below its 10-year historical average of ~18x. Relative to peers AutoZone and O'Reilly , AAP's valuation represents a 35%-50% discount over the next 3 years. Given the bullish tailwinds outlined in the above summary, we think the selloff in the stock is overdone, and current price levels provide for a significant margin of safety at these multiples.

{kind=link}

Corporate Overview

The Business

Headquartered in Raleigh, North Carolina, Advance Auto Parts is one of the largest specialty retailers of automotive parts and maintenance items, based on store count and sales. As of December 31, 2022, it had 5,086 stores and branches, primarily under the trade names Advance Auto Parts (4,440), Carquest (330), and WorldPac (316), up from 4,972 stores a year earlier.

The Strategy

In recent years, Advance has focused on growing its DIFM ("do-it-for-me") business by increasing parts availability and delivery time. AAP currently holds less than 5% of the DIFM market but has made solid progress over the last few years. Other key focuses for the business include enhancing and expanding its product line, with the goal of improving margins. Other initiatives include returning capital to shareholders through its share repurchase program.

The Market

The U.S. automotive aftermarket was estimated to be a $325 billion industry in 2021, up 11.2% from 2020. Current statistics provided by the Auto Care Association forecast the market to grow to $477 billion (~47%) by 2024. As outgoing CEO Tom Greco hinted on the most recent earnings call, the industry is highly fragmented, with competition from small and large firms being indistinguishable. The industry is mature and driven by the following factors: number of licenses issued, count, and age of automobiles in use, average number of miles driven annually, and the percentage of commercial vehicle fleets represented by light trucks and SUVs (generate higher average purchases). According to S&P Global , the average vehicle age has increased about 1.5% annually to 12.5 years from 10.3 years in 2008. We expect the average age to increase further given the current backdrop for consumers, as well as continued advancements in technology and engineering.

The Story

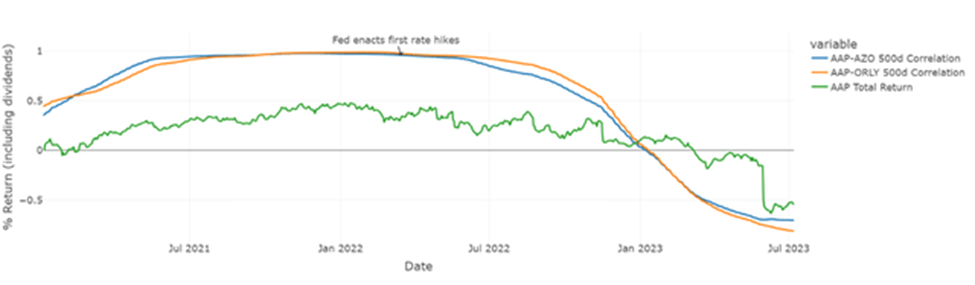

Dating back to 2015, value investors such as Starboard Value have had their eye on AAP, when Starboard CEO and CIO, Jeff Smith (aka, "The Substitute Warren Buffett" ), told investors at the Sohn Canada Conference that he believed the stock could nearly double to $350 from ~$190 over the next several years. At the time of this writing, the company's stock is nearing $70.

Starboard's case was as reasonable then as it is today: bring AAP's margins up to snuff with industry peers. Unfortunately, that never happened, and to make matters worse, the Fed rate hikes beginning in early 2022, tied with global supply chain disruptions, further dampened investors' confidence in Advance's ability to weather the storm with what were already dwindling margins.

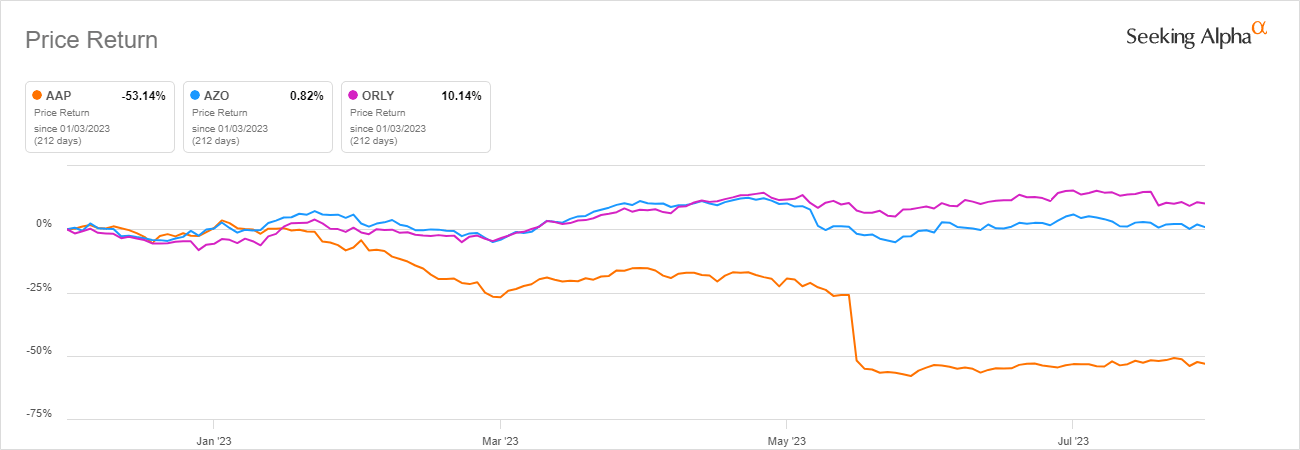

As it turns out, investors were right; EBIT and net income margins have fallen by more than 30% since January 2022. Investors spoke with their wallets, sticking with the safer bets of AZO and ORLY, all the while contributing to a complete breakdown in the historical price relationship of Advance and its peers.

{kind=link}

The Fundamentals

Revenue

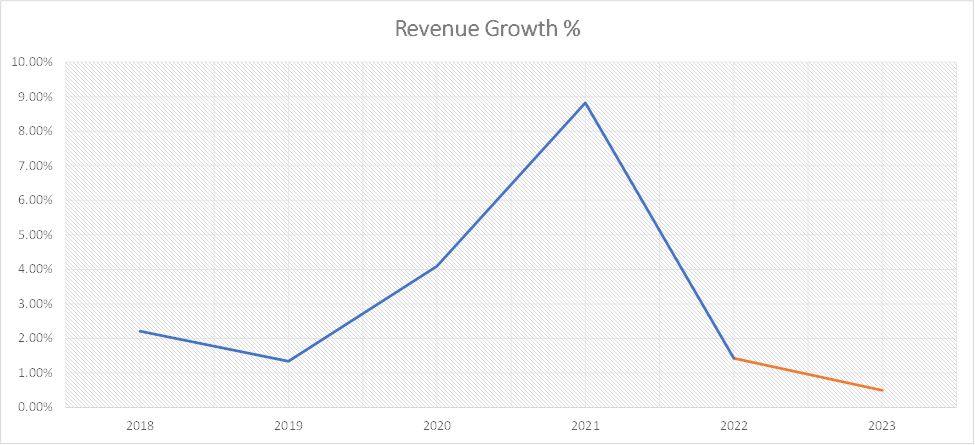

Top line growth remains stable and unlike the margin story, not a top priority for management. AAP expects to open 40-60 new stores in 2023, ~40 less than in 2022. The company's most recent guide estimates FY2023 revenues of $11.2 billion - $11.3 billion, an increase of ~0.50% from 2022.

{kind=link}

Though still lagging the growth of peers AZO and ORLY, the company tends to operate more efficiently on a per employee basis. The company generates higher revenue per employee than its peers, despite offering lower-margin products. We view this as a great backstop for much needed margin improvement, specifically Advance's ability to capitalize on the transition into higher-margin, owned brands.

{kind=link}

Gross Margins

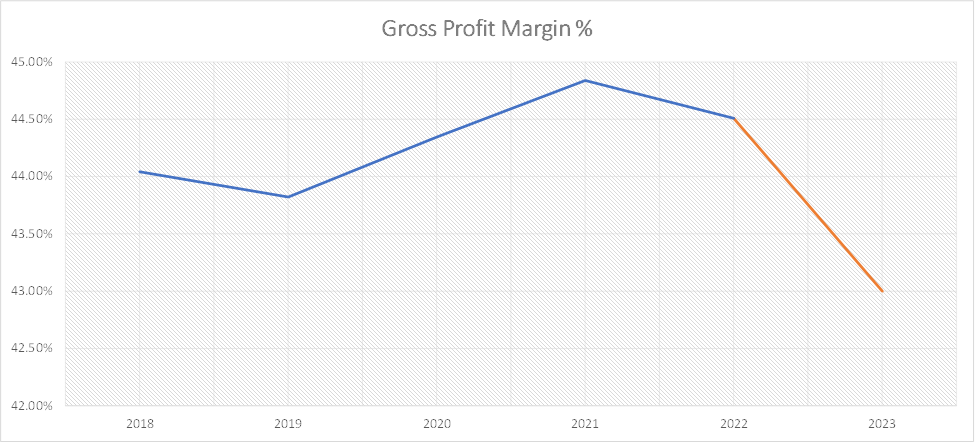

During Q12023, the firm experienced headwinds stemming from the competitive landscape. "It's important to point out that we remain committed to maintaining the competitive price targets we've established and have now attained in key categories, we were unable to price to cover product costs in the quarter." said CEO, Tom Greco on the most recent earnings call.

That said, product costs were mid-single digits compared to Q12022, higher than originally forecasted by management. Additional headwinds for the quarter included the weather, which provided for a milder winter, resulting in lower than anticipated battery and wiper sales. The geopolitical environment played a role as well, with increases in motor oil (historically a low margin product) further stinging margins. The more interesting, and certain to be one-off, is the hit taken because of lower-than-expected tax refunds for consumers.

Current guidance is to end the year with gross margins of 43%. We view this as extremely conservative given it would provide for a 10-year low in terms of gross margins. Excluding the competitive environment, we view most of the pain experienced (weather, oil prices and tax refunds) as temporary. We expect to see improvements as we enter the summer driving season. Additionally, history leads us to believe that we should see lower oil prices as we enter this part of the presidential election cycle.

{kind=link}

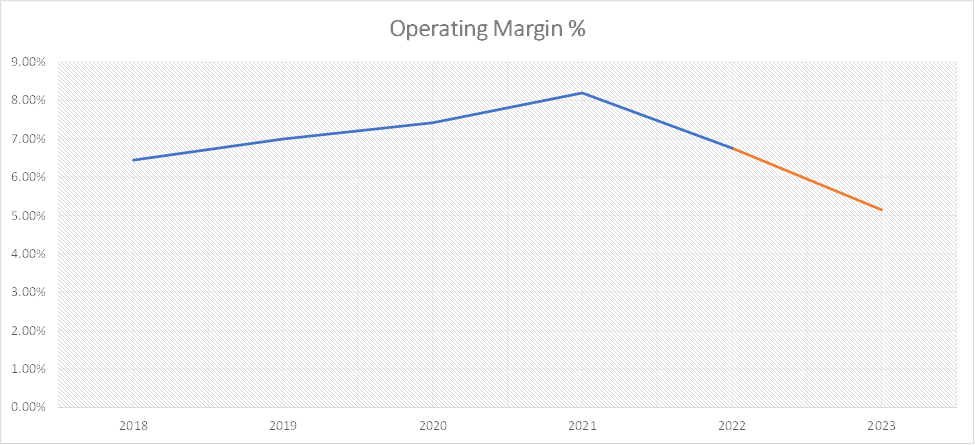

Operating Margins

With stable top-line growth and margins, AAP's problems arise between gross profit and pre-tax income. It is tough for any business to function with operating margins below 10%; somehow AAP has managed to do it for a decade. Peers AZO and ORLY have historically operated around 20%.

The key drivers of this have been (1) a poor performing, low-margin product mix, and (2) Advance's endeavors to enter the commercial, or "Pro" business, which has required them to discount inventory to remain competitive and grow out the category.

{kind=link}

The first prong (poor performing, low-margin owned inventory) is being addressed by management, as management details current and future discounting to clear inventory and transition to higher margin alternatives. The second prong of investing in the Pro space is a great long-term investment, and part of the reason management has stressed the need for financial flexibility and slashed the dividend to $1 from $6. We view both forces as positive for the stock, and believe operating margins have a fair amount of support at these levels given the company has operated above 6% since 2013.

Cash & Equivalents

As part of their most recent earnings release, AAP announced that it was slashing its annual dividend rate to $1 per share from $6. The company cited the need for enhanced financial flexibility and a commitment to improving its operational performance. We believe the market oversold the stock with this announcement when the underlying messaging from the company was a stronger focus on improving its operational efficiency.

The $5 per share in savings for the company is equivalent to ~$297 million, or ~7% of AAP's market cap. Those cash savings should go a long way in improving AAP's overall profitability. The most straightforward way that Management could deliver improvements is via lower interest expense by paying down debt. Assuming a WACC of 7%, interest expense would fall by $20.8 million annually, or 3.2% of TTM operating income.

Valuation

When working through the valuation process, I like to start at the bottom and work my way up. This allows me to think through potential headwinds or inherent risk before worrying about the future growth of the business. For a historically profitable firm such as AAP, let's start with earnings and work our way up to operating profits.

{kind=link}

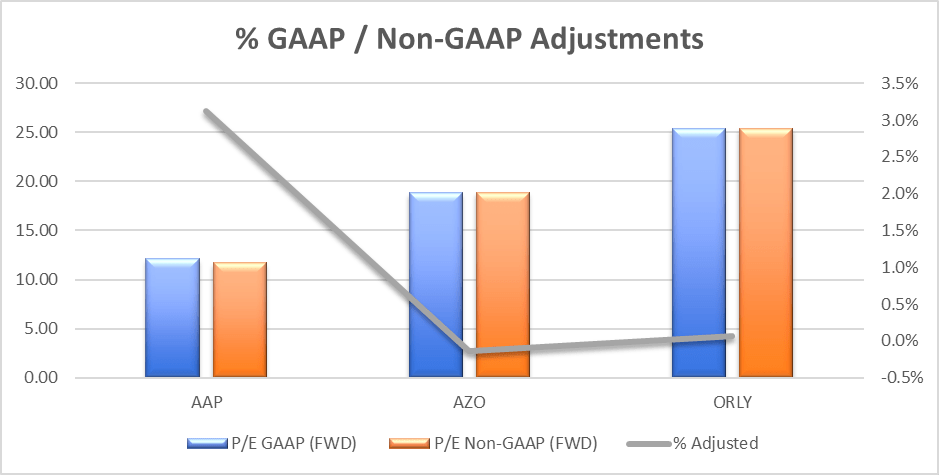

A lot can be said about the prospects for a company by comparing its GAAP earnings to its non-GAAP earnings. The difference between the two numbers indicates the magnitude of adjustments made for non-recurring or non-cash expense items. The greater the difference is, the more opportunity there is for a company to reduce non-recurring adjustments and have better GAAP earnings.

{kind=link}

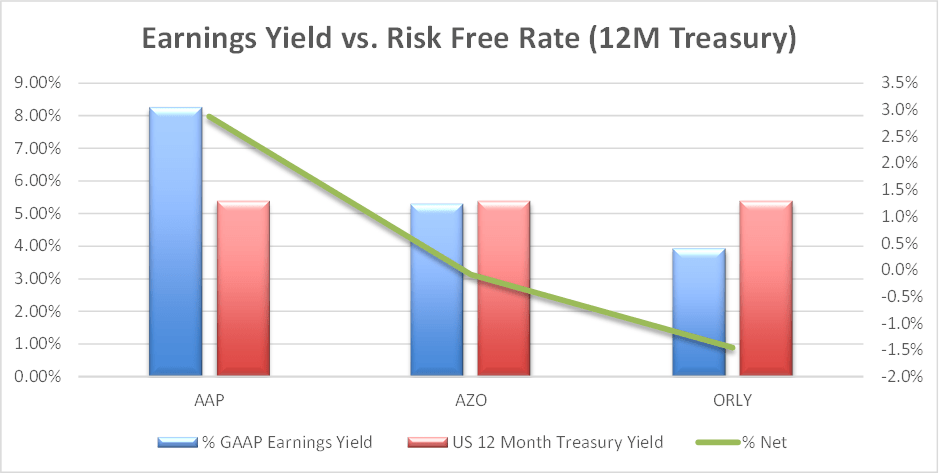

In addition to AAP's discount on both GAAP and non-GAAP measures, the chart above indicates that AAP has a higher percentage of non-recurring expenses relative to its peers, thereby indicating the relative upside opportunity for AAP. Another key takeaway from this part of our analysis is the overall earnings yield (100% divided by GAAP P/E minus 12M Treasury Rate) offered by AAP relative to its competitors. Noting the negative net earnings yields of AAP's peers, this should indicate that AAP is a better buying opportunity than its peers.

{kind=link}

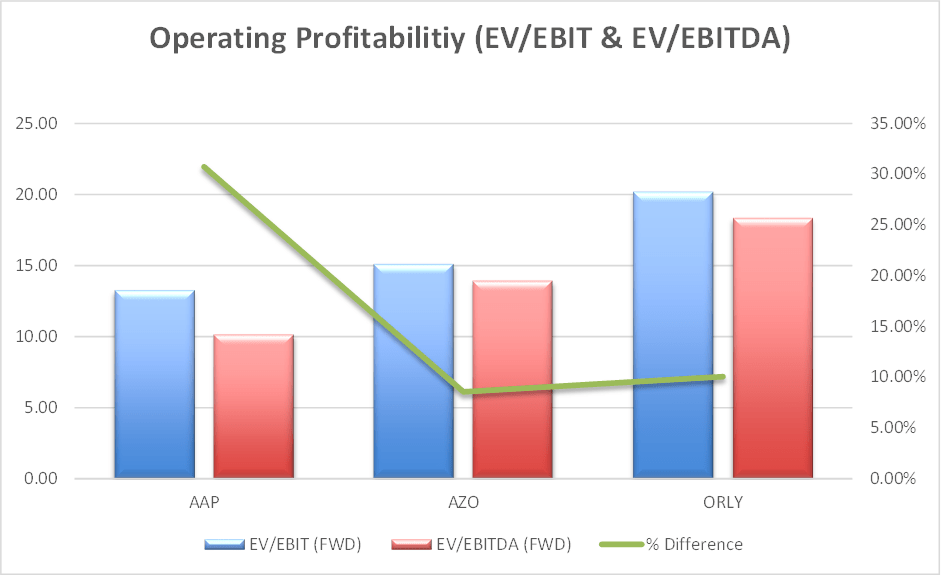

Next, let's make our way to operating profits and evaluate our key proxies for operating profit: EBIT and EBITDA. It is important to evaluate both EBIT and EBITDA as they provide crucial insight into a key driver of free cash flow: Capital Expenditures.

{kind=link}

As you can take from the above chart, Advance's current operations account for a significantly larger portion of D&A relative to its peer group. This difference is driven by above average CapEx in certain IT-related investments from the prior year and new store openings. This trend is expected to reverse going forward, as management is currently guiding for ~$150 million less in CapEx FYE2023 and beyond. Net of the add-back from Depreciation & Amortization (~60% of CapEx), free cash flow should increase by ~$60 million annually. This improvement is one of the two key drivers for our bull case on AAP's valuation as it should help to buffer free cash flow as they build towards higher margin product lines (i.e., improving EBIT margins).

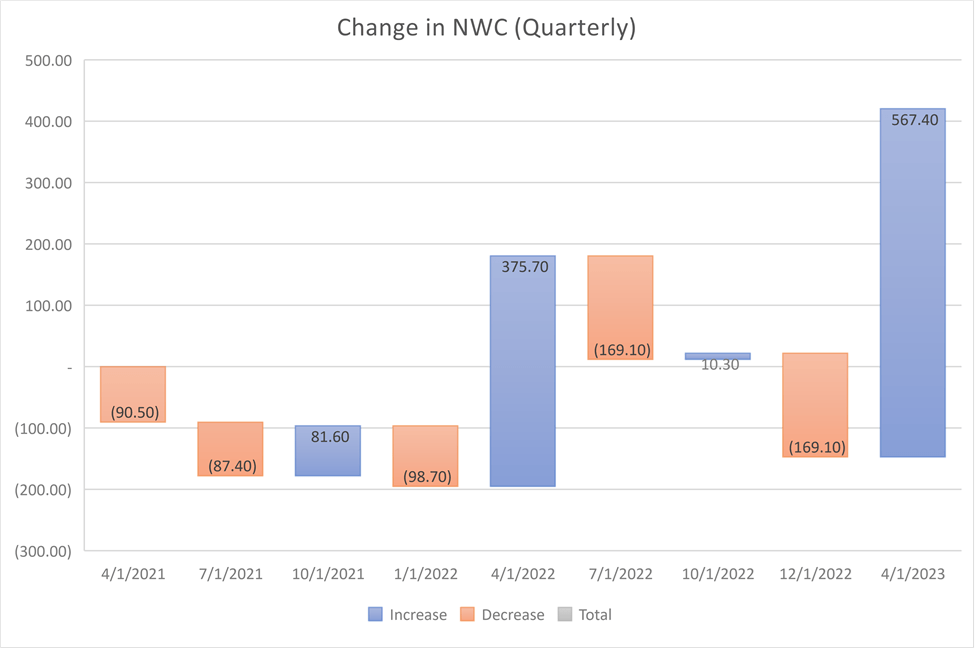

Further, we should consider the firm's working capital position. The most recent quarter reflected a $567 million increase in net working capital, a dramatic move relative to historical norms.

{kind=link}

The NWC increase was driven by the timing of certain payables to suppliers, which resulted in a $1B decrease to current liabilities. Management expects to see improvement over the balance of the year, which should reflect positively on free cash flow. With that, we anticipate YoY changes in net working capital to decline slightly into year end, but still elevated relative to historical norms. Both the significant reduction in capex as well as the expected change in NWC are expected to improve AAP's free cash flow, thereby generating a higher valuation in a traditional discounted cash flow valuation model.

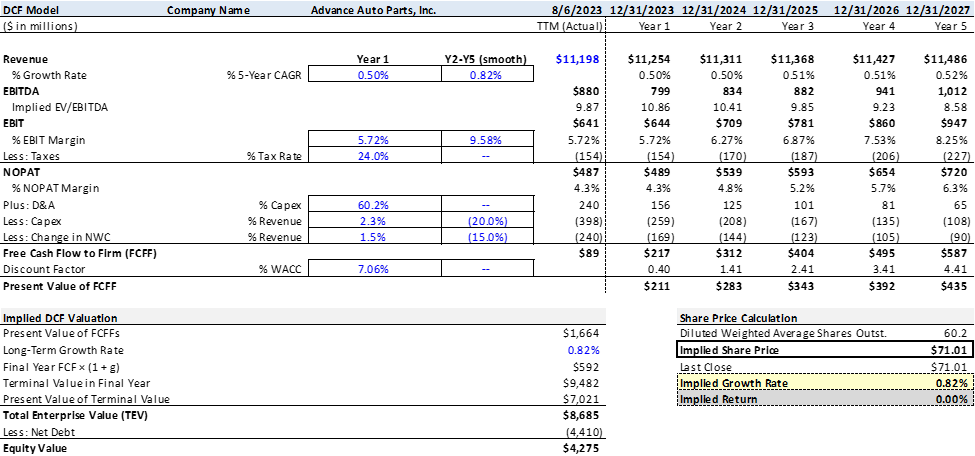

For my DCF calculations, I will be using a WACC of 7.06%, evenly split, with cost of equity and cost of debt of 5.50% and 8.5%, respectively. The cost of equity assumption is supported by the implied earnings yield of AAP discussed previously, and the cost of debt assumption is supported by ((A)) the timeframe of our price target (~5-6 months) and ((B)) the 6-month Treasury Rate .

Management's current guidance for FYE2023 FCFF is $200M-$300M. This includes the reductions in CapEx discussed previously, as well as more reasonable changes in net working capital going forward (5-year average of $50 million). We anticipate revenue will be flat (0.5%-1%) as new store openings level off. With that, let's see where EBIT margins need to be by year end to justify the current stock price.

{kind=link}

As reflected in the DCF model above, we see that based on the August 4, 2023 closing price for AAP, the stock would need to produce free cash flow FYE2023 of ~$217 million. This result reflects the lower end of management's guidance for revenue growth and operating margins, capital expenditures and working capital. This scenario implies forward EV/EBITDA of 10.9x compared to the 10.1x currently projected by analysts. The implied forward EV/EBITDA multiple also represents a 7.7% haircut to AAP's 5-year average of 11.8x, thereby indicating there is significant opportunity for upward movement from its current share price.

Risks

The key risks to our optimism around Advance's prospects are an economic slowdown, higher than anticipated fuel prices, fewer cars on the road and fewer miles driven. Additional considerations include global warming and the potential of permanently milder winters, leading to depressed margins in certain categories.

Conclusion

It is fair to say that 2023 has been a tough year for Advance. In our view, the stock's decline has been driven by market sentiment, and not the fundamentals. For intermediate to long-term buyers (4 to 6+ months), this entry point allows for substantial upside with little downside potential. As reflected in our valuation scenario, we believe $70 is a solid floor for the stock given ((a)) the low likelihood of management missing guidance again following such drastic cuts in May, ((b)) secular tailwinds favoring used vehicles over new vehicles, ((c)) the upside potential for margins as the company builds out its Pro business and higher margin product lines, and ((d)) the implied EV/EBITDA (~10.9x) at $70 per share, a significant discount to historical averages and analysts' expectations.

For further details see:

Advance Auto Parts: Attractive Valuation After Losing Half Its Value In 2023