AAP - Advance Auto Parts: Fairly Valued After Recent Drawdown

2023-06-03 03:36:22 ET

Summary

- Advance Auto Parts Inc. is down 40% after struggling in Q1 2023.

- Management should focus on optimizing operations, closing poor-performing stores, and improving product mix to increase cash flow for future buybacks and dividends.

- My valuation model estimates a fair value of $62.06, in line with the current market price.

- The factors above lead me to a hold rating for AAP.

Introduction

Advance Auto Parts Inc. (AAP) is down ~ 40% after they continued to struggle in Q1 2023. AAP has compounded revenue at 3.54% over the past 5 years and EPS at 5.26% over the same period. The balance sheet is okay for now as most of their debt is long term. They currently have a d/e ratio of 1.36. My valuation approach estimates a fair value of $62.06, in line with the current market price.

Management's Strategic Business Plan

In the recent Q1 transcript , management stated that they are dedicating themselves to their key initiatives of topline growth and operational performance. AAP is increasingly relying on the opening of new stores to drive growth as same store sales have been either flat or declining recently. However, I don't believe that there is much more growth to be had for AAP in this area as they already operate around 5,000 stores. Current guidance is that AAP will open 40 to 60 new stores this year. I would like to see less focus on new store openings and more focus on operational efficiency. SG&A as a % of revenue continues to increase. Q1 SG&A % of revenue came in at 40.4%. My view is that management should focus on optimizing their costs by closing poor performing stores, improving their product mix with higher margin products, and continuing to negotiate favorable contracts with their vendors. Once they optimize operations, they can use the excess cash flow to buy back shares and reinstate their dividend to previous levels.

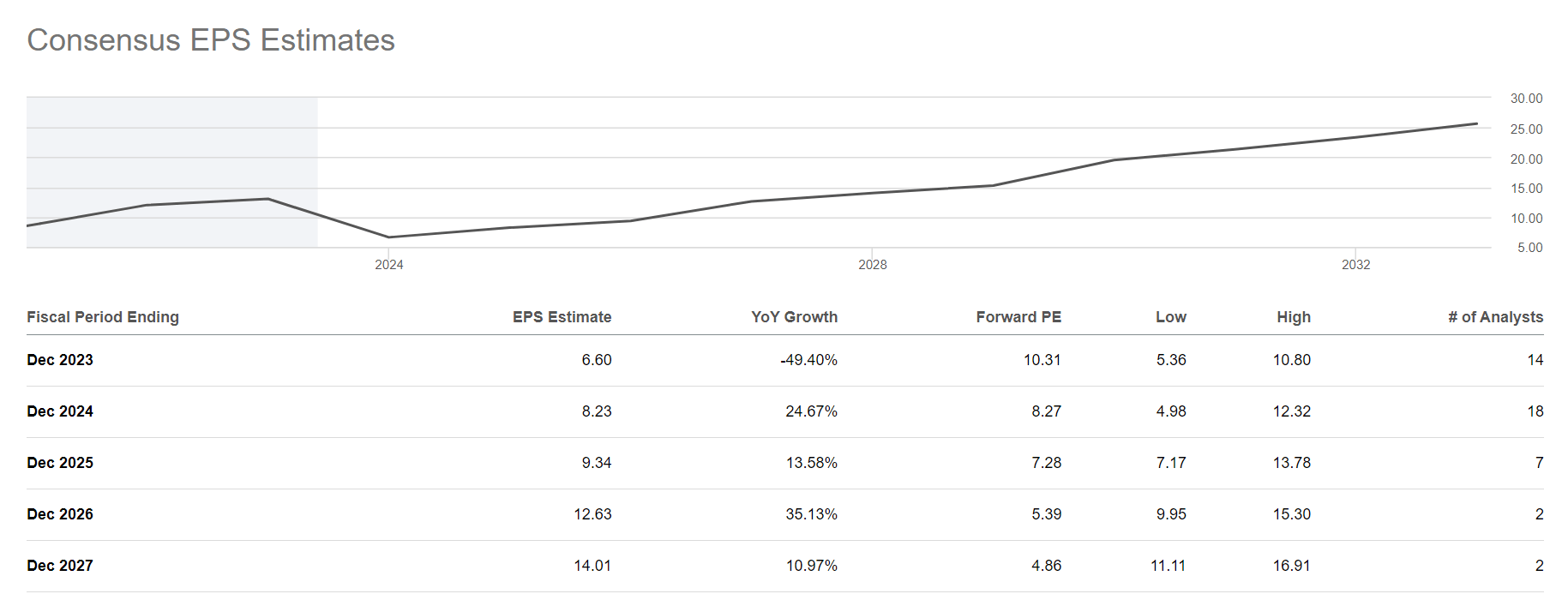

Earnings Expectations

{kind=link}

Before I dive into my scenario analysis, I will use this section to explain how I chose my growth assumptions. As we can see from the chart above , consensus expectations are for EPS to decrease substantially in 2023 and then rebound from there. Overall, the implied EPS CAGR from 2022 to 2027 is 11.12. I will use 12% as the growth rate in my best case scenario, which is only assigned a probability of 10%. I will use a growth rate of 10% for my base case to be roughly in line with consensus.

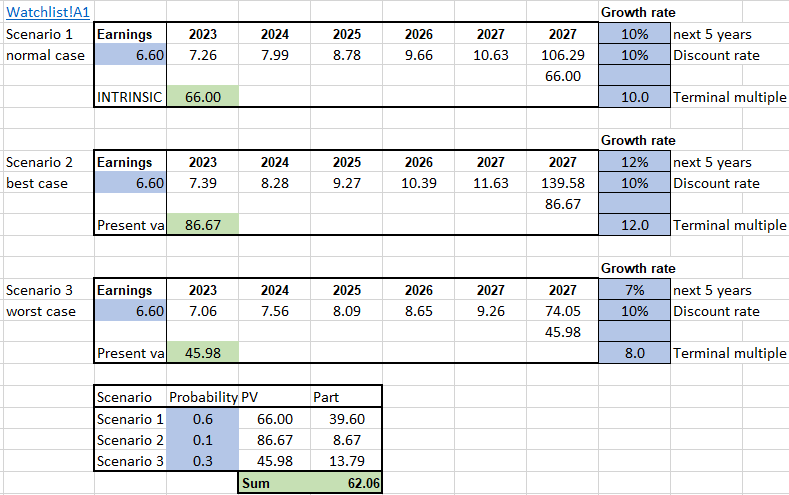

Valuation & Scenario Analysis

{kind=link}

For all my calculations of value, I will be using a discount rate of 10%. 10% is my minimum required return because this has historically been the return you can expect if you decide to just put your money in an index fund that tracks the S&P 500. Lastly, keeping the discount rate the same allows for comparability between different investments.

Also, I assign a weight of 60% to my base case, 10% to the best case, and 30% to my worst-case scenario. With that out of the way, I will move to the individual scenarios.

Scenario 1 is my base case, which assumes 10% growth for the next 5 years with a terminal multiple of 10x. Discounting the 2027 sales price back to present value yields a fair value of $66.00 for an investor with a target return of 10%.

Scenario 2 is my best case, which assumes 12% growth for the next 5 years with a terminal multiple of 12x. Discounting the 2027 sales price back to present value yields a fair value of $86.67 for an investor with a target return of 10%.

Scenario 3 is my worst case, which assumes 7% growth for the next 5 years with a terminal multiple of 8x. Discounting the 2027 sales price back to present value yields a fair value of $45.98 for an investor with a target return of 10%.

The sum of the weighted PVs is $62.06, implying the stock is currently trading around fair value.

PEG Analysis

I like to use PEG analysis to compare what the market is pricing in and compare that to consensus estimates. Based on the chart from my earnings expectations section, the average EPS that AAP is expected to earn in the next five years is 10.16. Currently, AAP trades at 6.65x this number. However, consensus estimates imply that EPS will grow at ~11% over this same 5-year period. Based on these numbers, you could argue that AAP is undervalued due to the fact that its PEG ratio is below 1. However, I believe that the average is being skewed by the 2026 and 2027 estimates and would still argue that the stock is fairly valued.

Risks

Continued Dividend Cuts

Part of the reason that AAP has declined so much is that they cut their dividend in Q1 2023. Future dividend cuts could cause further declines in the stock.

Debt Burden

AAP currently has a debt to equity ratio of 1.36. Although currently manageable, if the business begins to decline more seriously, then this could become a bigger issue as their debt begins to mature.

Inflation

Inflation could continue to harm AAP's margins as the cost of parts continues to rise.

Conclusion

Overall, AAP is experiencing a down year and is fairly valued based on current expectations. If they are able to optimize operations in the near term, there may be an opportunity to deliver value through buybacks in the long term.

I rate AAP a hold.

For further details see:

Advance Auto Parts: Fairly Valued After Recent Drawdown