AAP - Advance Auto Parts: New CEO Will Have His Work Cut Out For Him

2023-09-14 12:44:36 ET

Summary

- Advance Auto Parts continues to have gross margin issues as it looks to become more price competitive.

- The company's new CEO has a lot of distribution experience, but turning around AAP will take time.

- The stock is looking more intriguing, but I'd like to hear the new CEO's plan before jumping on board.

Back in July , I wrote that Advance Auto Parts ( AAP ) was struggling with margins and competitive pricing and that a quick recovery would not be easy. Since then the stock is down about -18%, trailing the -1% decline in the S&P 500. Let’s catch up on the name.

Company Profile

As a refresher, AAP is an aftermarket automotive parts provider that sells brand name, OEM, and its own brand automotive replacement parts to both professional and do it yourself (DIY) customers. Professionals accounted for about 59% of its 2022 sales.

AAP operates stores, branches, and e-commerce sites under its namesake brand, as well as the Carquest and Worldpac concepts. Worldpac and Carquest primarily serve professional customers, while Advance Auto Parts caters to both.

New CEO and Q2 Results

In late August, AAP reported a 0.8% increase in sales to $2.7 billion. Analysts were looking for revenue of $2.66 billion.

Same-store sales declined -0.6%. The company said it saw improvement the last month of the quarter, registering slightly positive comps during that time. It also noted that transactions rose during the quarter, although average ticket was down as it tried to stay price competitive.

Gross margins slipped -180 basis points to 42.7%. The company said this was a result of higher product costs and supply chain deleveraging. SG&A expenses as a percentage of sales, meanwhile, rose 80 basis points.

Adjusted EPS fell -40% to $1.43, missing the analyst consensus by 24 cents.

Cash flow from operations was $214.3 million, while free cash flow was $159.3 million.

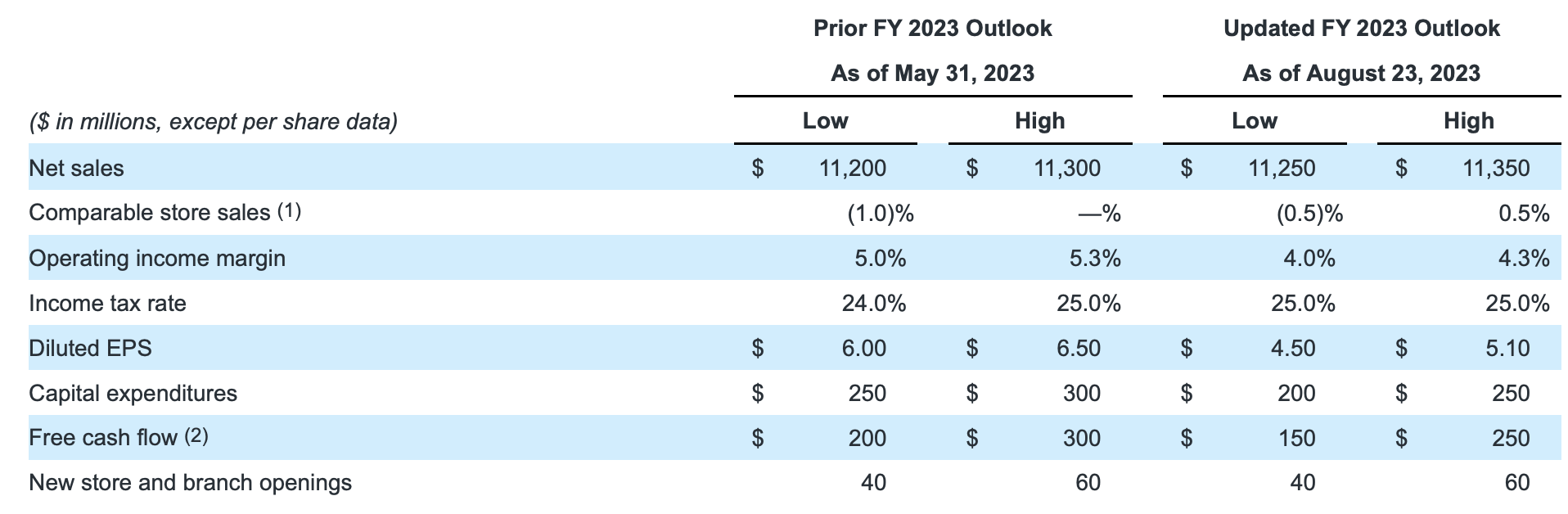

Looking ahead, AAP updated its full-year outlook. It now expects revenue of between $11.25-11.35 billion on same-store sales of -0.5% to 0.5% up from a prior outlook of $11.2-11.3 billion in revenue on -1.0% to flat comparable-store sales.

EPS is now projected to come in at $4.50-5.10, down from a prior forecast of $6.00-6.50. Free cash flow is now expected to be between $150-250 million, down from a previous outlook to $200-300 million.

{kind=link}

On the Q2 earnings call , outgoing CEO Thomas Greco said:

“Our top-line sales continued to improve into the third quarter as we delivered low single-digit comparable sales growth during the first 4 weeks. Our performance benefited from the initiatives we've talked about earlier this year to drive improved transactions in both DIY omnichannel and Pro. First, our improved availability was driven by the inventory investments we made, along with year-to-date improvements in supply chain fill rates and store on hand rates. As in-stocks improved in the quarter, we saw sequential sales growth in key hard parts categories. Second, our category management actions continued in Q2 to ensure we sustained competitive price targets. In addition, we've discussed in the past the opportunity to increase owned brand penetration to improve margins.”

Gross margins continue to be one of the main issues for AAP, as it looks to remain price competitive versus its competition. These pricing initiatives are keeping sales about flat, but it is coming at the cost of lower gross markets, which is hurting its EPS and cash flow outlooks. This will be no easy fix, but the company also announced a new CEO to help tackle the problem.

In conjunction with its earnings, AAP named Shane O'Kelly as CEO effect September 11 th . O’Kelly comes from HD Supply, a distributor of maintenance, repair and operations products and a subsidiary of Home Depot ( HD ). He served as CEO of the company since December 2020. O’Kelly has also been the CEO of several other distributors through the years, including Interline Brands, PetroChoice, and AH Harris.

While a seasoned vet, O’Kelly will have his work cut out for him. Before he was announced as CEO, the company was removed from the S&P 500 , and earlier this week S&P downgraded its credit rating to BBB- from BB+. The move takes the company’s debt to junk status.

In its downgrade, S&P wrote:

“We believe the company's misguided strategic decision to preserve and attempt to expand margins while its competitors invested in price has eroded its value proposition. Over the past eighteen months, Advance's sales have largely been flat, while its peers' revenues have grown in a low-teen percent. We believe Advance has ceded market share and its competitive standing in the industry has weakened. We accordingly have revised our business risk assessment to fair from satisfactory."

This assessment pretty much hits the nail on the head, albeit it is a bit backwards looking. The job of O’Kelly is now to somehow fix the mess that AAP has gotten itself into. He’s only officially been on the job a few days, so we'll have to wait for him to articulate his plan.

However, I’d be surprised if he didn’t follow the difficult steps of continuing to walk back margins to try to stay competitive and take back share. Keeping margins at the expense of market share no longer looks like a viable strategy. The company likely will try to push more sales to its own brands, which can help, but it will also need to invest in supply chain technology as well. Enacting things like dynamic and geographic pricing could be the way to go.

Valuation

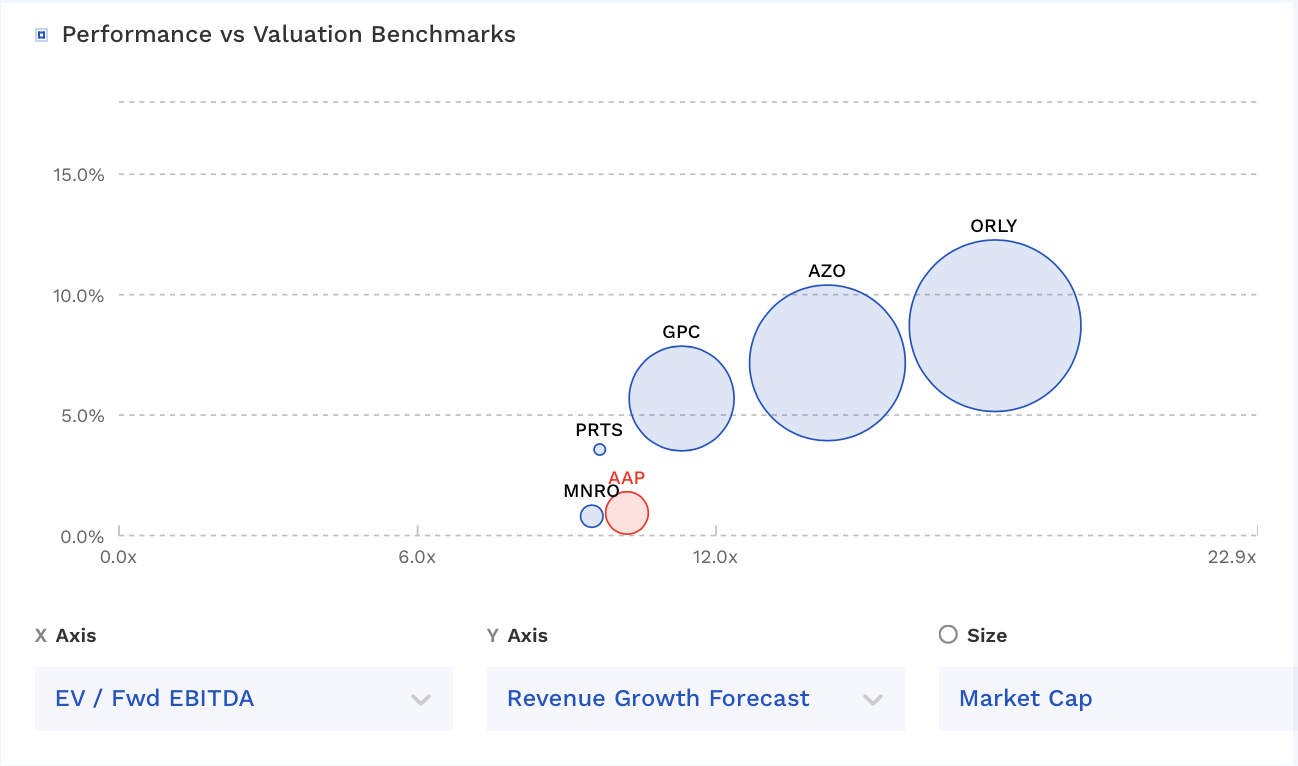

AAP trades at a 10.2x EV/EBITDA multiple based on the 2023 EBITDA consensus of $759.6 million. Based off of the 2024 EBITDA consensus of $814.4 million, it trades at around 9.5x.

On an EV/EBITDAR basis based on 2024 estimates, it trades at 5.4x.

It trades at 12.2x forward EPS, with analysts projecting 2023 EPS of $4.75 and 10x based on 2024 estimates of $5.77.

It’s projected to grow revenue under 1% in 2023, increasing to 2% growth in 2024.

It’s one of the cheapest stocks among peers, but also one of the slowest growers.

{kind=link}

Conclusion

From a valuation perspective, AAP seems to have found a place it has settled into. The big question is what its EBITDA and earnings will look like moving forward. It’s not uncommon for a company to kitchen sink guidance ahead of a new CEO taking over so that they can get off to a good start. I wouldn’t be surprised if this turns out to be the case for AAP.

That said, this isn’t a quick fix, and the company’s valuation still isn’t in the bargain bin. The turnaround potential is there, and I like the background of O’Kelly, who has a lot of distribution experience. I’m going to stay on the sidelines for now, and the stock could see some tax-loss selling later this year.

However, I am getting more interested in the stock and will continue to monitor the name. A lower valuation or the articulation of a turnaround strategy around more tech investments could get me more interested in starting a position.

For further details see:

Advance Auto Parts: New CEO Will Have His Work Cut Out For Him