AAP - Advance Auto Parts: Oversold And Primed For Value

2023-08-11 10:58:49 ET

Summary

- Advance Auto Parts' stock fell from $112 to around $70 after a dividend cut and a search for a new CEO; the aftermarket auto segment remains strong, with used car prices remaining high.

- Despite a revenue miss due to seasonality and a mild winter, management forecasts a 1.5% sales increase for FY2023; if the company grows revenues at a slow 4.5% per year, shares should be priced at $92.37.

- The automotive retail industry remains mature and undisturbed; AAP maintains its position by being close to its customer base and the demand for auto.

Editor's note: Seeking Alpha is proud to welcome Cody Oeung as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Thesis

The market fell out of favor with Advance Auto Parts ( AAP ) after their recent earnings call when the dividend was slashed and the stock abruptly fell from $112 to hover around $70. The market reaction has been very focused on the dividend yield collapsing while the company searches for a new CEO. With a near-term outlook looking mediocre at best, the stock has fallen to a point where even unspectacular businesses-as-usual implies a valuation of the stock at $92.37.

The underlying market for the aftermarket auto segment remains strong as used car prices show to be sticky and the average age of used cars on the road continues to increase to 12.2 years and the percentage of cars in the 'sweet spot age of 4-11 yrs' for auto-repairs continues to climb . The automotive retail landscape is one with lots of competition where customers care about reasonable prices, proximity, and same-day availability. Mechanics that are working on automobiles, albeit hobby or professional, want the least amount of friction in getting the parts and supplies they need to get back on the road, which AAP has built a strong reputation around.

Company Overview

AAP is a leading automotive aftermarket parts provider in North America. Its customer base is composed of both professional installers and DIY customers and its stores offer a collection of brand names, OEM, and in-house brand replacement parts for cars, vans, SUVs, and light-duty trucks. As of December 2022, there were 5,086 total stores and branches.

59% of AAP's revenue comes from professional customers, where products from the store are delivered to the customer's place of business. DIY customers are primarily served through stores, but can order in-store and have items shipped to them. Stores also have a variety of free services for customers to investigate a 'check engine light' or other simple automotive tests.

AAP Locations (AAP 10-K (FY 2022))

{kind=link}

Financials

During the last earnings call , management projected the FY earnings to be $11.4 billion, implying a 2% growth in revenue YoY, citing a mild winter selling fewer batteries and windshield wipers. Same-store sales are expected to be flat, and new stores opening are expected to drive the most revenue growth. Operating margins were also down due to the mix of products sold, down from 6.4% at the end of 2022 to 2.6% in the latest quarter. An accounting mistake caught in the last year, correcting errors dating back from 2021, increased operating costs by $17M for the quarter. Adjusting for this, the operating margin for the quarter increases to 3.3%.

Capex guidance from the company reports that infrastructure upgrades for inventory management have been completed and capex spending will return to a normal schedule for repairing and strategically opening new locations to the tune of $250M-$300M for the next year.

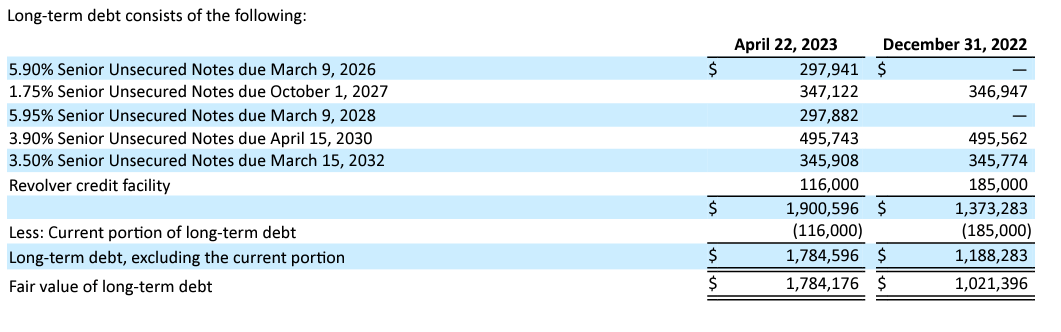

Company liquidity on the balance sheet does not pose any immediate concern as the interest coverage ratio is at 24.5x with the next maturity not until 2026 without any warnings of a downgrade from a BBB- status.

AAP Debt Schedule (AAP 10-Q (Q1 2023))

{kind=link}

Valuation

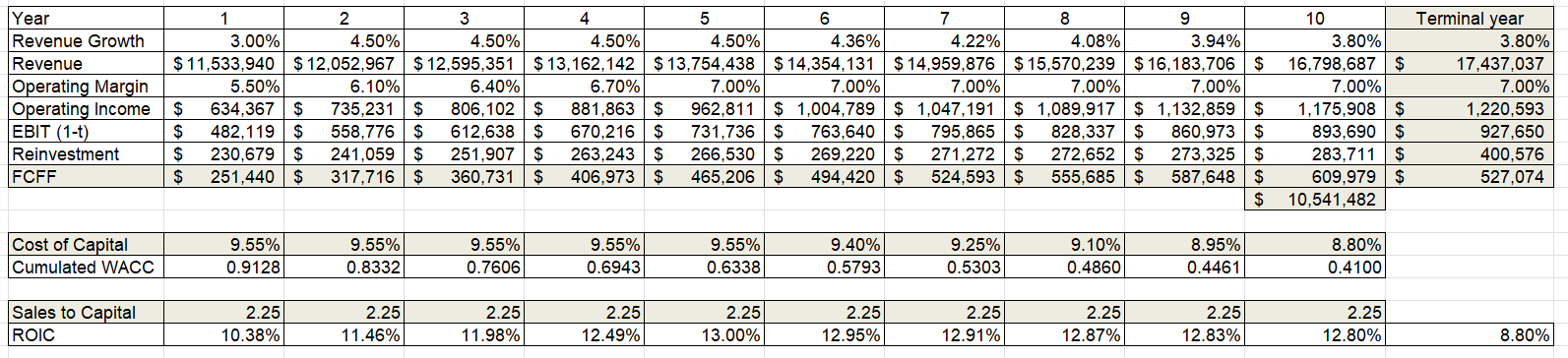

My valuation for AAP comes in 3 parts: Growth, profitability, and efficiency. Assuming slow revenue growth on the back of industry average reinvestment and ROIC, AAP has a very reasonable path to pre-2022 profitability and an intrinsic value of $92.37 per share.

Growth: The growth story from the topline I assumed was modest. Given growth this year of 2%, growth in the following year bounces back to 4.5% and holds at 4.5% YoY for 5 years until 2028 before tapering down to 3.8% in the terminal year, reaching $16.8B in revenues. The current interest rate environment is what drove my projections in revenue as 6-month US treasuries yield roughly 5.5% and 10-year notes hover close to 4%.

Profitability: Operating margins in the automotive retail sector average 5.06%, but the peers of AAP such as O'Reilly Automotive ( ORLY ) and AutoZone ( AZO ) have operating margins in the 3rd quartile of distribution. AAP has also historically been close in operating margins to its peers as well, given its similar operating profile. My projections assume that AAP will return to its past operational margins of 7% in the next few years. Looking back at the past 10 years, AAP has reported operating margins between 10.2% and 6.1%. This lower operating margin adds to the buffer of AAP's growing revenues modestly and providing quality services to its customers without making quick cuts to achieve more profitability in the short term.

Efficiency: Instead of directly forecasting capex, depreciation, and change in working capital to arrive at free cash flow to the firm (FCFF), I assumed a healthy reinvestment rate to fuel the company's growth. In the turnaround years, the reinvestment rate is 40% of NOPAT, reducing to 31% as AAP stabilizes. ROIC from the reinvestment stays close to the global industry average of 12.5%.

{kind=link}

AAP Share Price (Cody Oeung)

Risks

The largest risk factor for the automotive retail industry is hybrid and EVs. The typical hybrid or EV uses many fewer parts and has longer maintenance intervals than a traditional gasoline vehicle. However, hybrid and EV affordability maintain a key issue for many consumers and despite the seemingly large upcoming changes in transportation, gasoline-powered vehicles remain a sticky part of the new-auto market. Even as more new vehicles are electric or hybrid, the 'sweet spot' for car repairs lags new-car sales by at least 4 years. The tide may be turning but according to the Bureau of Transportation Statistics :

Hybrid vehicle sales began in 1999 and plug-in electric vehicle sales began in 2010. Hybrids captured 3.2% of the light vehicle market in 2013 and again 5.5% in 2021. All-electric vehicles accounted for 3.2% of the light vehicle market in 2021.

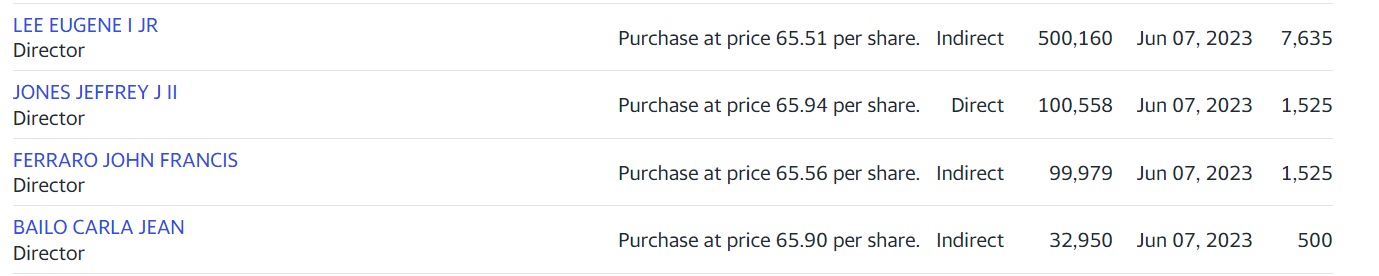

Management change going badly would be another risk involving AAP. TRC Capital recently placed a mini-tender offer at $65.75 per share, representing a 9% discount to the share price when it was offered. A proxy battle for control of the company will give more uncertainty for the company, but an activist signal is good for the company as it provides a floor price for activists or other companies looking for an acquisition target.

In addition to TRC Capital's interest, there has been insider buying, which is always a positive sign. While executives sell stock for a number of reasons not pertaining to the company, there is only one reason to buy stock: for it to appreciate.

Insider Buying (Yahoo Finance)

{kind=link}

Conclusion

Advance Auto Parts is oversold since its last earnings call. The company trades at the lowest multiples in the peer group but maintains profitability and maintains its competitive advantage with its strong retail presence and commercial sales. Keeping revenue growth modest and in line with treasury yields, I believe the company just needs to return back to business-as-usual for the share price to increase 25% to $92.37.

For further details see:

Advance Auto Parts: Oversold And Primed For Value