AAP - Advance Auto Parts: Shares Have Fallen Too Far

2023-05-23 03:37:57 ET

Summary

- The shares of Advance Auto Parts have fallen too far taking the shares below their fair value. AAP is a fairly good business available at an attractive price.

- The stock is trading 20-50% below its average five-year multiples and is at a significantly lower value than its better-performing peers.

- Analysts are expecting earnings to decline this year. If the company performs better than the market expects there could be a significant upside in the upcoming quarters.

- Advance Auto Parts pays a large dividend offering a 5.1% dividend yield. Together with buybacks, the total shareholder yield provides a good level of downside protection.

The vehicle spare part distribution is dominated by four companies in the United States. One of them is Advance Auto Parts (AAP). Due to its inferior financial performance, its share price has lagged the three others which have propelled higher and higher. Currently, Advance Auto Parts is trading 25-50 percent below its historical averages, pays a hefty dividend and the shares are attractively priced after a long sell-off.

The laggard among the big four

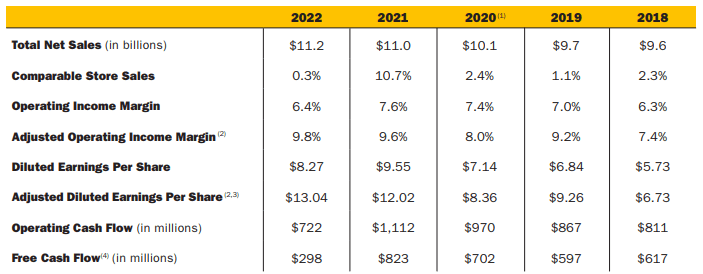

Advance Auto Parts operates approximately 5,000 company owned stores and serves 1,300 independent stores operating under the Carquest brand. Last year Advance Auto Parts revenue was $11.2 billion and it has 54,000 employees.

Advance Auto Parts is one of the four large auto parts distributors, the three others being AutoZone, O'Reilly and Genuine Parts. In comparison the other three have 7000, 6000 and 10 000 stores in total. In 2022 their revenues were $16.3, $16.4 and $9.3 billion (42% of Genuine Parts revenue is automotive).

Competitiveness in the replacement parts distribution is a question of scale, being able to offer a wide selection of products, fast and competitively priced. AAP has been a laggard in the industry and it needs to sharpen its execution not to deteriorate its market share further.

Financial history of the company. (Advance Auto Parts)

{kind=link}

Making sense of the share price decline

Advance Auto Parts is the only company among the four incumbents, of which earnings are expected to decline (-18%) this year. AAP's CEO Tom Greco called the year 2022 challenging and results being unsatisfactory. However, the company took several actions to change the course. It invested in digital capabilities, opened 114 new stores (net), adapted pricing policies and sharpened product selection. The challenges with inflation and supply chain challenges are weakening and therefore analyst estimates could be exaggerated to the downside.

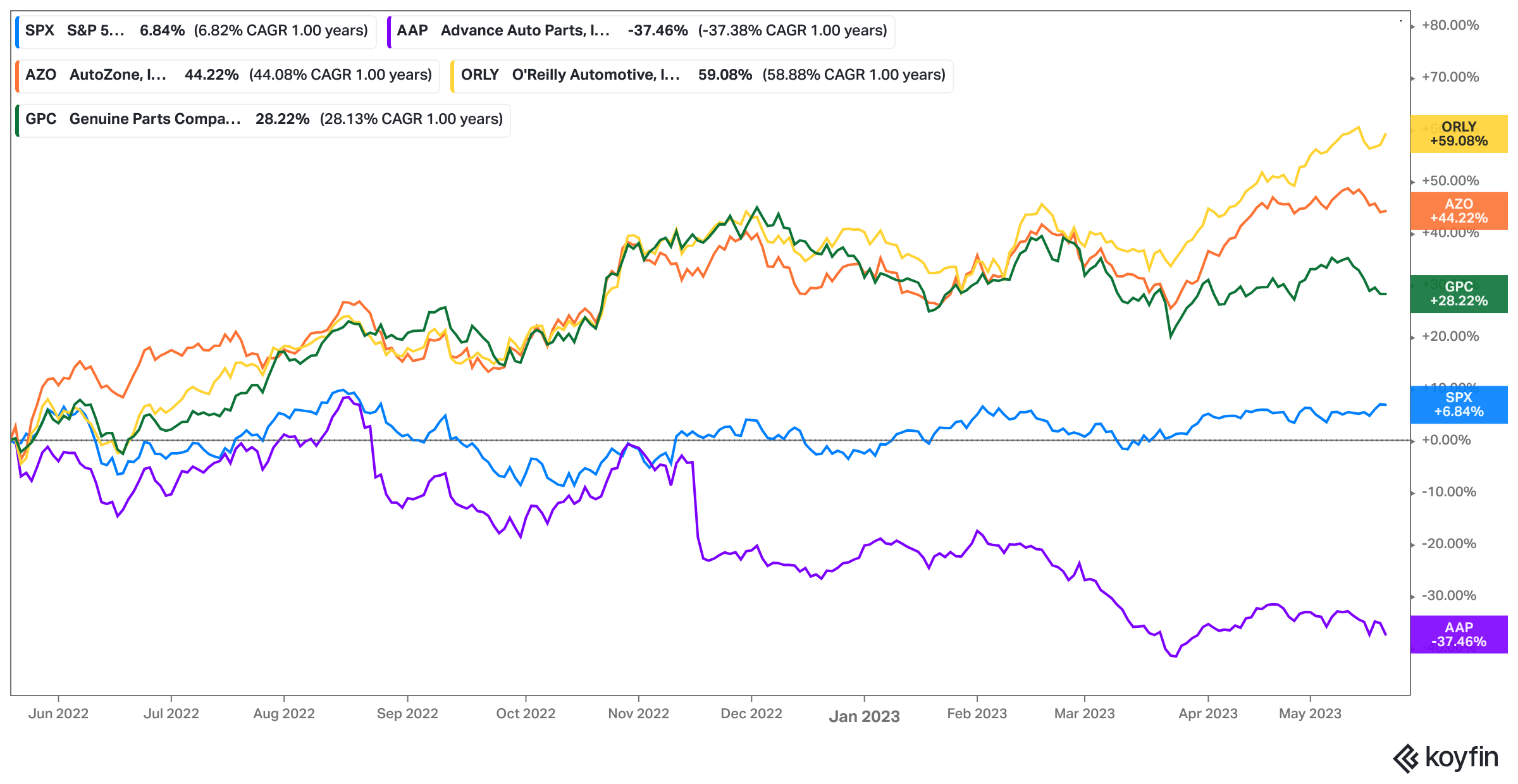

AAP has underperformed the peers and S&P500 in the last 12 months. (Koyfin.)

{kind=link}

Especially AutoZone and O'Reilly have benefited from the flight to quality. Investors have favoured stocks of companies that produce stable and predictable results and have strong characteristics of high quality business. Therefore, the multiple expansion of AutoZone and O'Reilly has been a big factor producing impressive share price appreciation.

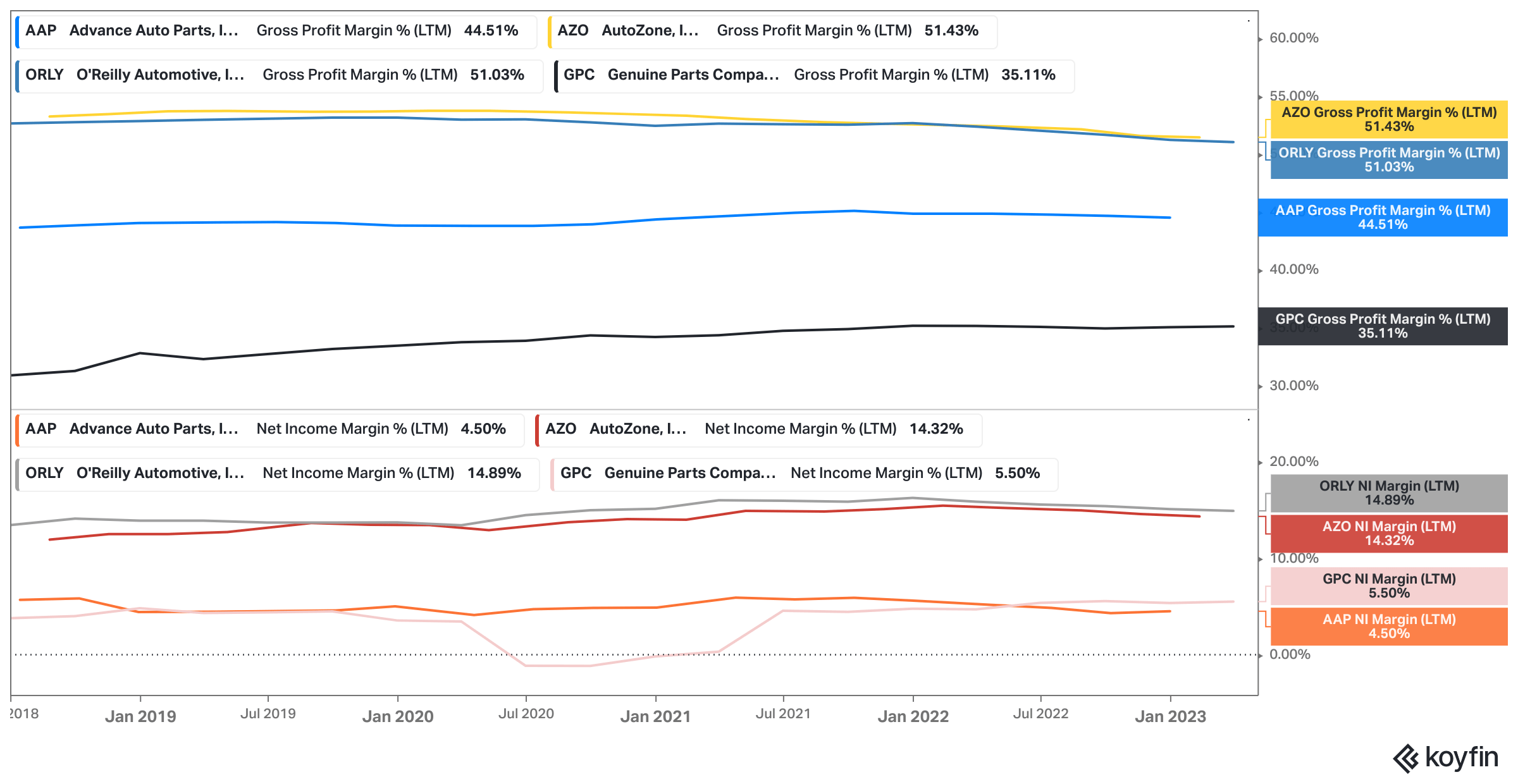

AAP's margins are stable but lower than most of its peers. (Koyfin.)

{kind=link}

The market could be discounting the fact that electric vehicles become predominant types of cars and they require less spare parts. Although the International Energy Agency, IEA, expects the EV sales to quadruple during the current decade, the transition will take enough time for the distributors to adapt. There's also business left with the EVs as the cars get more complex. At the same time the average American car is getting older every year and consumers are in a difficult situation to purchase more expensive EVs, pressured by inflation and higher financing costs.

Advance Auto Parts is addressing the industry transformation. For example, in the end of 2019, Advance Auto Parts announced an acquisition of a company called DieHard, which supplies replacement battery systems to electric vehicles. Last year sales of the DieHard brand grew in double-digits.

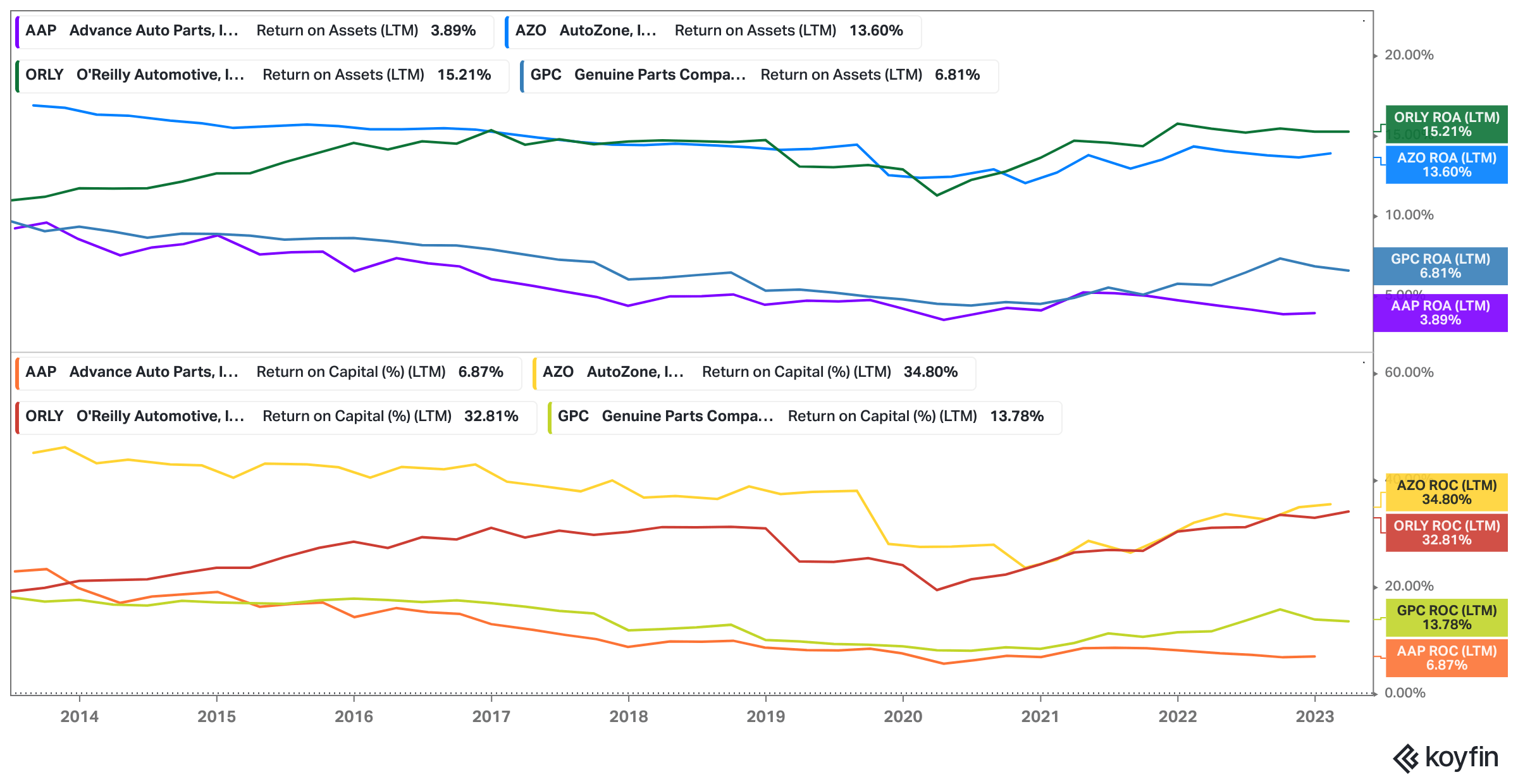

The most important task of the management is to allocate capital. When comparing the capital return rates of Advance Auto Parts and its competitors, it's clear that the management at Advance Auto Parts has not succeeded. In February the company announced a plan to find a successor to the retiring CEO Tom Greco. Obviously a new CEO is not a quick fix, but in the longer term a successful hire could bring new life to the company and the stock.

Capital returns have lagged the peers. (Koyfin.)

{kind=link}

Trading below the fair value

The peers and competitors of Advance Auto Parts trade at significantly higher multiples. There are clear reasons for it and a peer comparison makes only a little sense. The comparison could either argue that the peers are overvalued or AAP is undervalued. Here, the investment thesis implies that the AAP stock has been oversold, and peer comparison provides here some support.

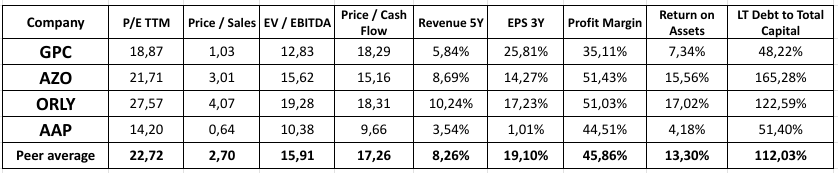

Selected multiples and performance metrics of AAP and its peers. (Seeking Alpha.)

{kind=link}

Advance Auto Parts is trading at a significant discount on all of the selected multiples above - explained by the performance metrics. However, especially when compared to Genuine Parts, AAP doesn't come too far behind in terms of performance. Overall, Advance Auto Parts continues to have a decent business, which is not priced to perfection. A fairly good company can be a great investment at the right price. Currently AAP stock is trading 20-50 percent below its five year average multiples.

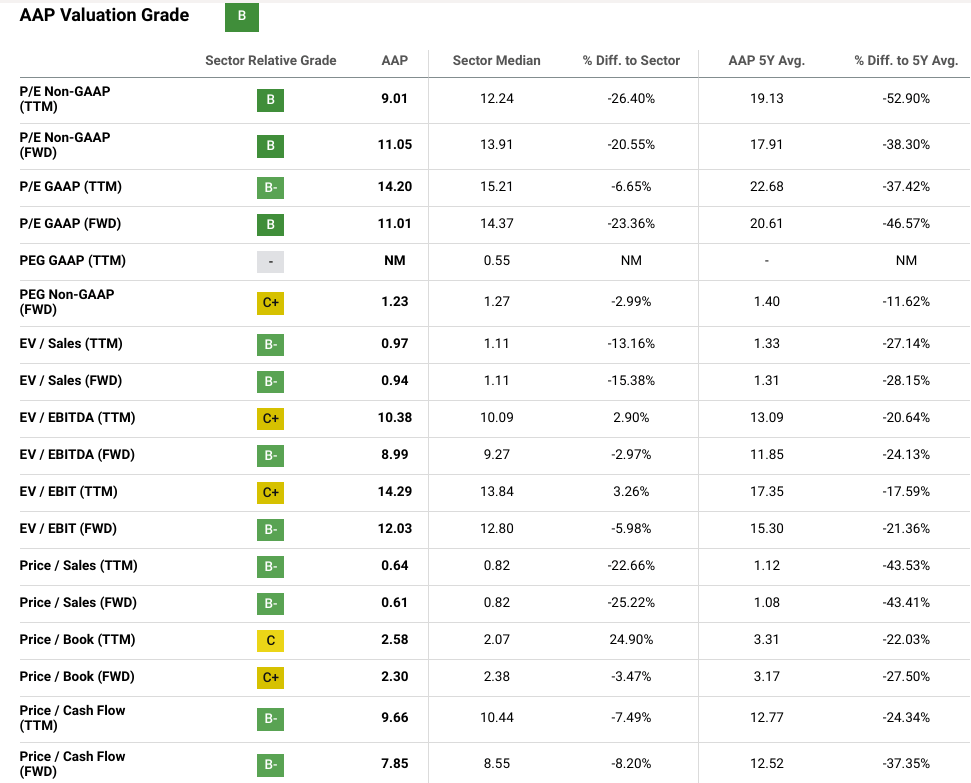

Significant discount to historical valuation. (Seeking Alpha.)

{kind=link}

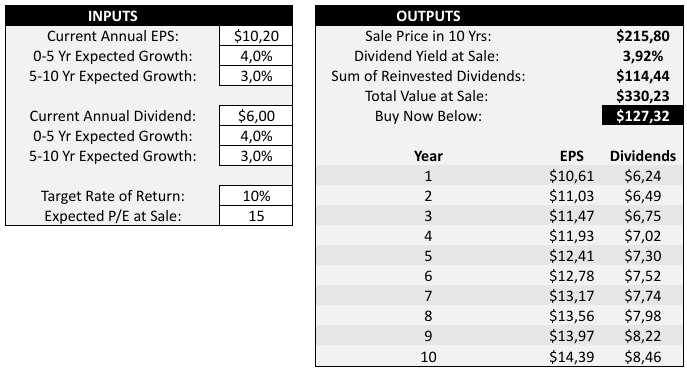

Analysts estimate this year's EPS to decline 18% to $10.64 from $13.04 last year. The company is guiding for $10.2 to $11.2. We can take the lower end of the guidance as a starting point and apply a 4% growth rate for the first five years and a one percentage point less for the following years. The average EPS growth has been approximately five percent.

We expect the dividend to grow in line with the earnings and apply a 10% discount rate and a terminal multiple of 15. AAP has typically traded at a P/E of 18-22 averaging 19 on non-GAAP basis. With these assumptions, which includes plenty of safety margin, the stock would be a buy below $127. The stock is therefore trading 8% below fair value by conservative assumptions.

Fair value based on earnings and dividend. (Author.)

{kind=link}

The current forward P/E for AAP is only 11, which implies the market doesn't expect much of growth. If the company would be able to grow its earnings a little bit slower than in the past, the 4% growth rate and a 5% dividend yield could justify a P/E of 15. The other less important argument is that the stock seems oversold in the light of the earnings outlook by the company and relatively steady business performance.

Analysts have an average target price of $145 for AAP with a high variance ranging from $110 to $190. Most of the analysts rate the stock as a hold.

An attractive dividend yield

Unlike its peers Advance Auto Parts pays a large dividend. Its annual payout is $6 per share translating to a dividend yield of 5.1% and a payout ratio of 46%. In June 2020 the company increased the quarterly dividend first to $0.25, then a year later to $1 and a few quarters later to the current $1.50.

On top of the dividend AAP is buying back its own shares. In the past five years the number of shares outstanding has come down by 18%. At the end of the previous year, the company had $947.3 million remaining under the share repurchase program. Thanks to the large dividend and buybacks the shareholder yield currently stands at around 8.5%.

Conclusion

Advance Auto Parts faces a tough competition among the four large incumbents. AAP doesn't have a great track record in comparison. Nevertheless, it enjoys healthy margins, capital returns and is addressing its competitiveness. After the selloff the stock is trading below its fair value and at attractive multiples. If the following quarterly results turn out to be better than the market expects, the share could quickly rebound. The dividend and the buybacks offer a good level of downside protection.

For further details see:

Advance Auto Parts: Shares Have Fallen Too Far