AAP - Advance Auto Parts: Undervalued With A Good Margin Of Safety

Summary

- The company recently announced their latest earnings report, which exceeded expectations for both revenue and profit.

- Despite current economic uncertainty, Advance Auto Parts remains optimistic about its future growth prospects and expects to see further improvements in inventory availability throughout 2023.

- The company appears undervalued based on earnings and stock chart.

- The combination of dividend payments and share buybacks is expected to contribute 8.67% per year in capital gains, and with low single-digit organic growth on top, low double-digit intrinsic growth is likely going forward.

Introduction

Advance Auto Parts (AAP) just announced their latest earnings report , which surpassed expectations for both revenue and profit. The company cited successful efforts in managing inventory and pricing as key factors behind the strong performance. Specifically, the revenue for the period stood at $2.47 billion, marking a YoY growth of 2.9% and exceeding projections by $50m, thanks in part to an increase in comparable store sales of 2.1%. The earnings per share also outperformed predictions by $0.46, reaching $2.88, which was attributed to a combination of pricing strategies and expanding their proprietary product lines. Despite current economic uncertainty, Advance Auto Parts remains optimistic about their future growth prospects.

We expect to see further improvements in inventory availability throughout 2023, which we view as the single most important driver to accelerate topline growth.

- Tom Greco, President and Chief Executive Officer

In my opinion, the company's strong financial results, provide strong evidence to support a higher valuation for the company. This is further supported by both the company's stock chart and its underlying fundamentals.

Capital Allocation

It seems that the company has shifted strategy regarding its approach to capital allocation. Previously, all earnings were reinvested by the company through business acquisitions, capital equity reinvestment, or share buybacks. However, in recent years, the company has prioritized greater dividend payouts. Currently, the dividend accounts for approximately half of the earnings, yielding 4.23%.

If the company continues to repurchase shares at the current earnings multiple, a yearly return of 4.44% can be expected. In addition, organic growth through small price increases is anticipated to persist without requiring reinvestment, as demonstrated by the recent earnings report showing a 2.1% increase in comparable store sales.

A conservative annual capital return of ~11.67% can therefore be expected. This is in line with the average growth the company has had since 2004. The large drop in ROE from 2012 to 2020 makes it clear that the ability to reinvest was diminishing. I therefore expect the current capital allocation to continue with an increased focus on dividends and share buybacks.

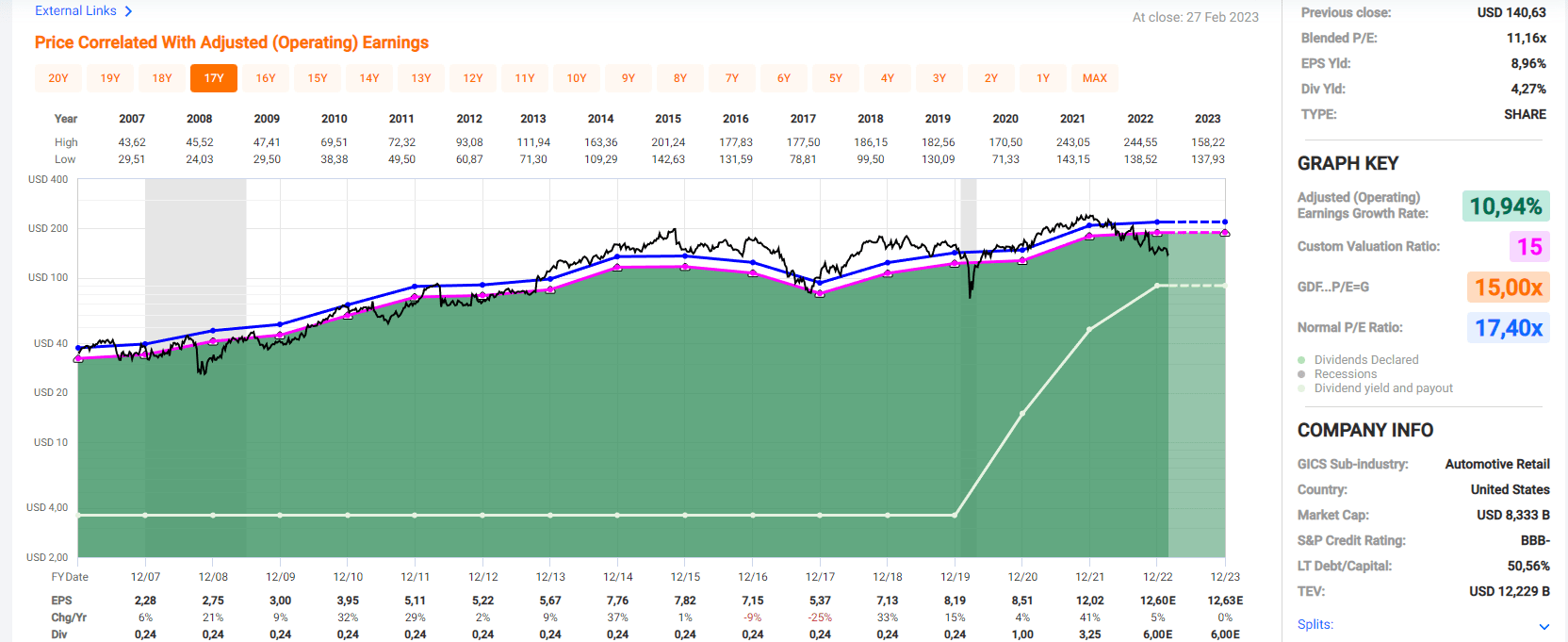

Valuation

Over the past twenty years, the company has achieved an average annual EPS growth of 11%. This growth has been relatively steady, with the only exception being a period of weakness following the Carquest brand acquisition boom in 2013. The company has achieved growth through a combination of acquisitions, share buybacks, reinvestments, and organic same-store sales. This diversified approach to growth has been successful, but it does pose challenges for projecting future growth.

Despite this, the current valuation of the company remains significantly below its average earnings multiple. Considering the fundamentals mentioned earlier remain unchanged and with management expecting further growth, particularly with anticipated improvements in inventory availability through 2023, a return to a reasonable earnings multiple is expected. This suggests that the stock could potentially be undervalued by as much as 55%.

However, the balance sheet appears to be somewhat strained, which weakens the argument for a higher earnings multiple. The company currently holds total debt of $3.6 billion and only around $200 million in cash, resulting in a net debt of $3.4 billion. It is important to be aware of this debt level when assessing the company's valuation. When the net debt is added to the market cap and the average earnings multiple is applied, the estimated price per share drops from $189 to $172. This calculation is more reliable for determining the company's intrinsic valuation than merely assuming that the average multiple reflects its intrinsic value.

To calculate a conservative price estimate that includes a margin of safety, I have used the net debt of $3.4 billion relative to the market capitalization of $11.2 billion at a standard P/E ratio of 15. This results in a price estimate of $143.59, which I consider to be very conservative. This calculation takes into account a below-average earnings multiple and the company's net debt.

{kind=link}

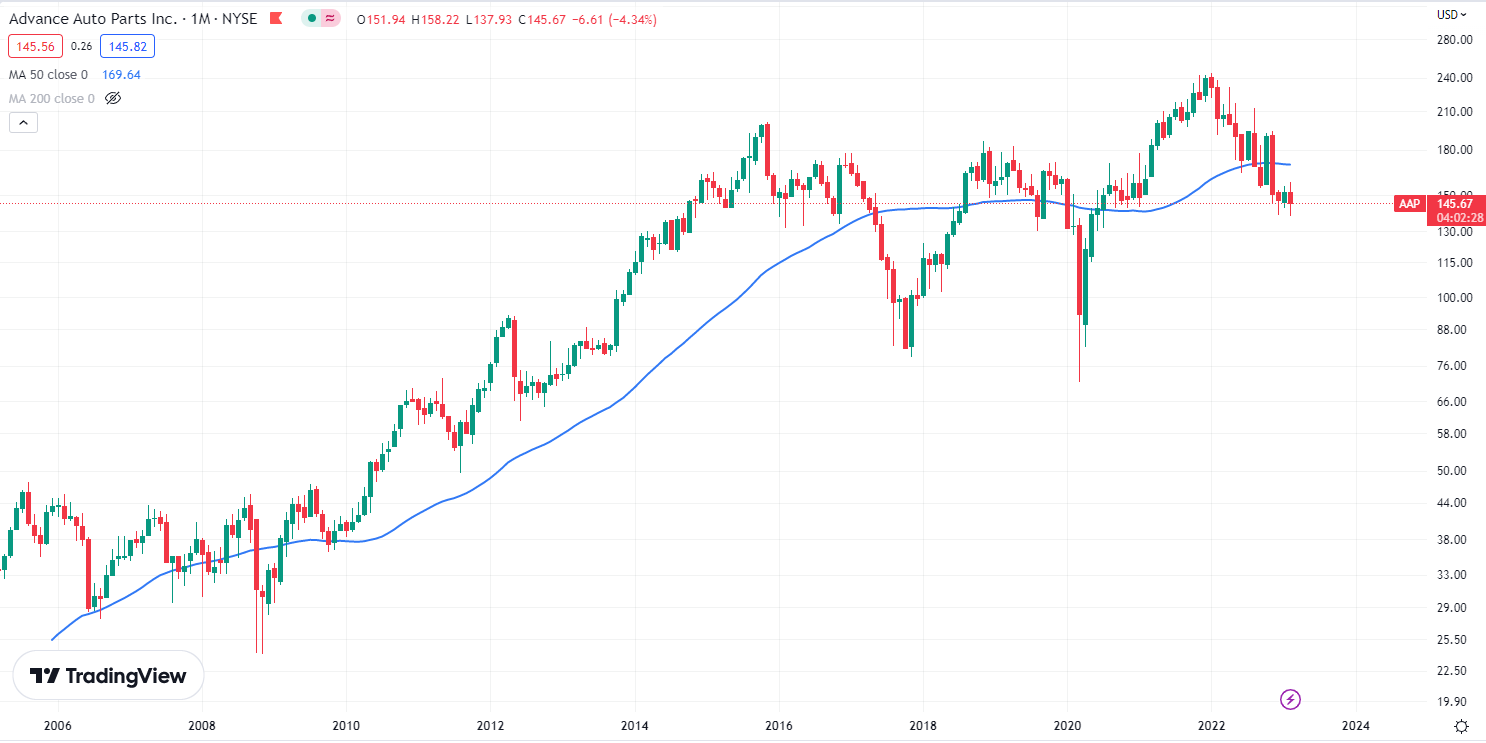

Stock Chart

Quick disclaimer: A technical analysis in itself is not a good enough reason to buy a stock, but combined with the company's fundamentals, it can greatly narrow your price target range when investing.

Based on the stock chart, the stock appears to be attractively valued as it is trading far below its 50-month moving average. A return to a price above the 50-month moving average could potentially put the stock at around $180, which is only slightly below its 15 earnings multiple of $188, and slightly above the calculated intrinsic valuation of ~$172.

The conservative estimate of $143.59 is only a few percentage points away from the current price of the stock. Given the current valuation and the fact that the stock is trading below its 50-month moving average, I believe there is a margin of safety in purchasing the stock at its current price. As the business continues to grow, the margin of safety will expand further.

{kind=link}

Final Thoughts

To summarize, the combination of dividend payments and share buybacks is expected to contribute at least 8.67% per year in capital gains, and with low single-digit organic growth on top, low double-digit intrinsic growth is likely going forward. The stock is currently trading at a discount of around 18% below the estimated intrinsic value, while appearing to have a good margin of safety at current prices.

These calculations are supported by the stock chart and the company's recent earnings beat. I therefore give the stock a "Buy".

For further details see:

Advance Auto Parts: Undervalued With A Good Margin Of Safety