WMS - Advanced Drainage Systems: The Picture Is Getting More Interesting

2023-08-18 18:28:58 ET

Summary

- Advanced Drainage Systems is experiencing weakness and underperforming the broader market, presenting a potential buying opportunity.

- The company's revenue and profitability metrics have declined, largely due to weaker demand in the US construction and housing markets.

- Management forecasts a decline in revenue for the 2024 fiscal year, but remains optimistic about the company's outlook.

It's always fascinating to see, when business conditions change, how the market reacts. One thing that excites me as an investor is seeing fundamental weakness that could make a company more attractive if you ignore the near-term pain and focus on long-term potential. In these cases, shares of the companies can, for a time, underperform the broader market. This leaves open a window of opportunity to slip in, pick up some shares, and wait for the market to turn. One company that is currently experiencing this kind of pain is none other than Advanced Drainage Systems ( WMS ), a firm that is focused on providing innovative water management solutions to both stormwater and on-site septic wastewater industries.

After a very solid 2023 fiscal year, the firm has started showing some weakness. That pain has led to shares of the company languishing while the broader market moves higher. Conceptually, this draws me in because it could mean some upside is just around the corner. But given the state of industry conditions, combined with how shares are priced even with a recovery, I am not yet prepared to become all that bullish just yet.

The tide is turning

I am no stranger to Advanced Drainage Systems. Prior to this article, I have written about the company on three separate occasions. The first time was in early 2022. This was followed up by a second article in July of that year. In both of those articles, I rated the company a 'buy' to reflect my view that shares should outperform the broader market for the foreseeable future. The results were quite solid. From the time of the publication of the first article to the time of the publication of the second , the S&P 500 had dropped by 13% while shares of Advanced Drainage Systems dropped a more modest 8.6%. And then from July until my third article in October of last year, shares spiked 13.2% compared to the 20% decline the broader market saw. It was in that third article, however, that I felt it appropriate to downgrade the company to a 'hold', largely because I felt as though the easy money had been made.

{kind=link}

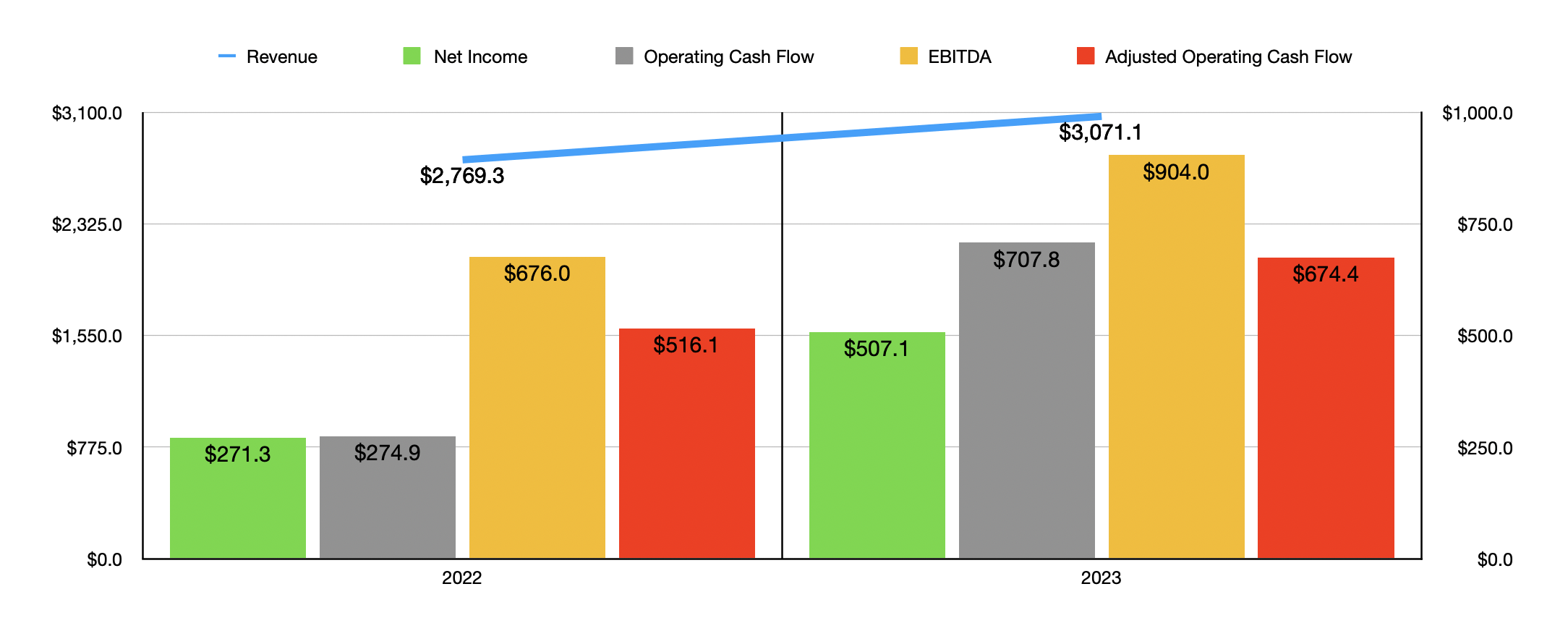

Since that time, things have not gone exactly well for Advanced Drainage Systems. While the S&P 500 is up 19.8% since the publication of that article, shares are actually down 3.9%. If you look at data covering the complete 2023 fiscal year, you might be surprised about this. As you can see in the chart above, revenue for that year totaled $3.07 billion. That represents an increase of 10.9% over the $2.77 billion the company reported one year earlier. All the major profitability metrics for the business also improved year over year. Net income almost doubled from $271.3 million to $507.1 million. Operating cash flow almost tripled from $274.9 million to $707.8 million, while the adjusted figure for it grew from $516.1 million to $674.4 million. And finally, EBITDA for the business expanded from $676 million to $904 million.

{kind=link}

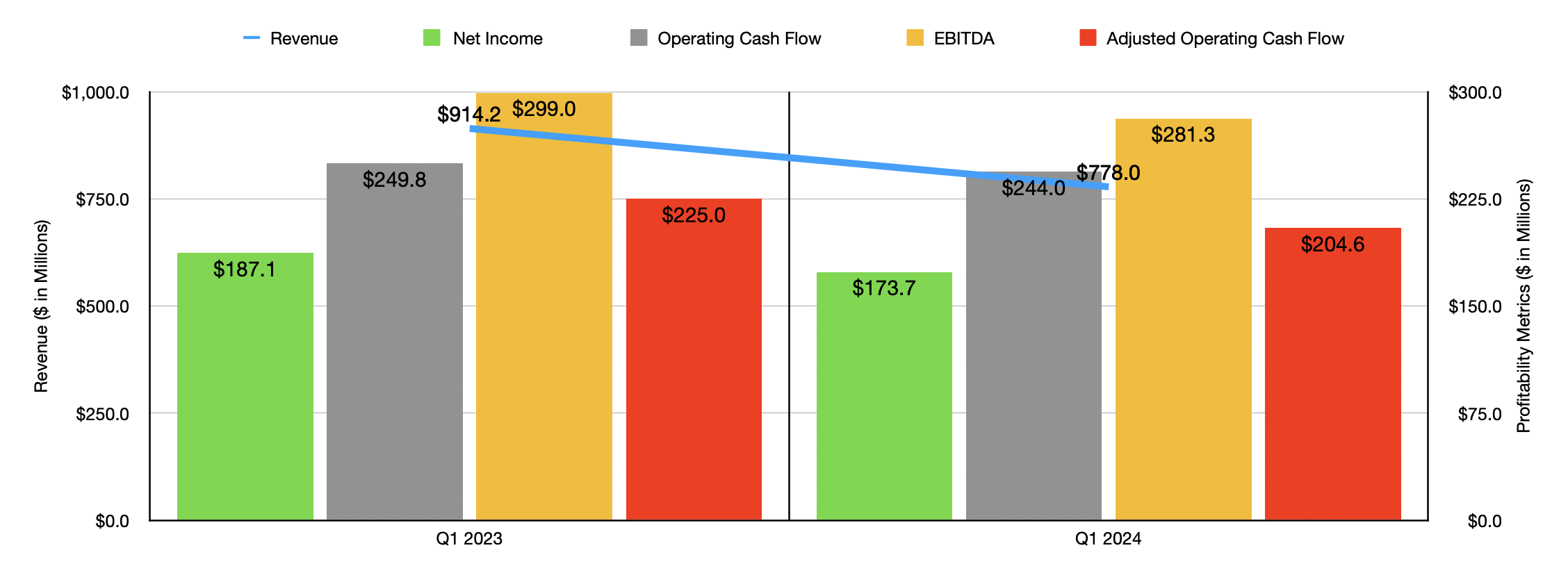

Fast forward to the present day, however, and the picture has changed. And not in a great way. Revenue in the first quarter of the year totaled $778 million. That's 14.9% lower than the $914.2 million the company generated one year earlier. According to management, this was driven by pain across all of the company's reportable segments. The segment that was hurt the worst from a monetary perspective was undeniably the Pipe segment. This is the largest portion of the company, accounting for roughly 56% of overall revenue. Through this segment, the company sells a wide variety of pipes that are used for liquid transportation. Revenue for that segment dropped 18.4%, or $94.6 million. That decline, management said, was largely the result of weaker demand in the US construction and markets.

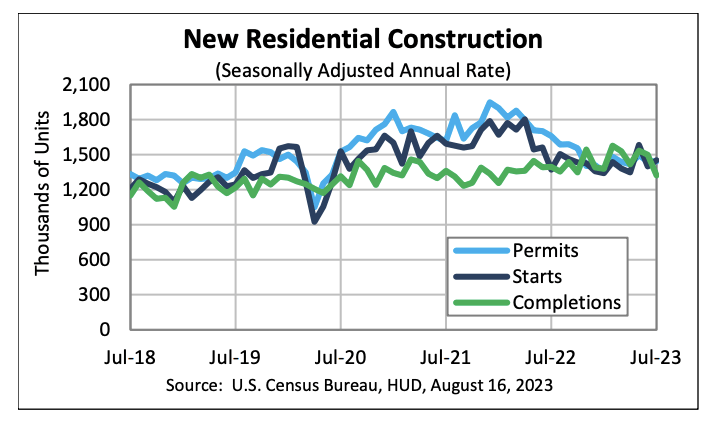

This should not be a surprise. The fact of the matter is that the housing market, which the company definitely relies on, has been seeing some weakness this year. Inflationary pressures, combined with high interest rates aimed at combating those pressures, have caused home construction to grind to a halt. This is something I have written about in other articles such as here and here . I would encourage you to dig more into those details. But one interesting data point that illustrates the pain the market is going through involves housing starts and housing permits. For the month of July, new residential construction permits were down 13% year over year, while housing starts are up 5.9%. This disparity stems from the fact that homebuilders are still pumping out homes that they contracted previously. But eventually, the massive backlog declines that they have experienced will push sales lower. The housing starts data should be viewed as more or less an indicator of past activity, while the building permits should be viewed as a leading indicator.

{kind=link}

This drop in revenue was bound to have an impact on bottom line results. Net income, for instance, fell from $187.1 million to $173.7 million. Other profitability metrics weren't hit as hard. For instance, operating cash flow declined only modestly from $249.8 million to $244 million. If we adjust for changes in working capital, we get a decline from $225 million to $204.6 million. And finally, EBITDA for the company fell from $299 million to $281.3 million.

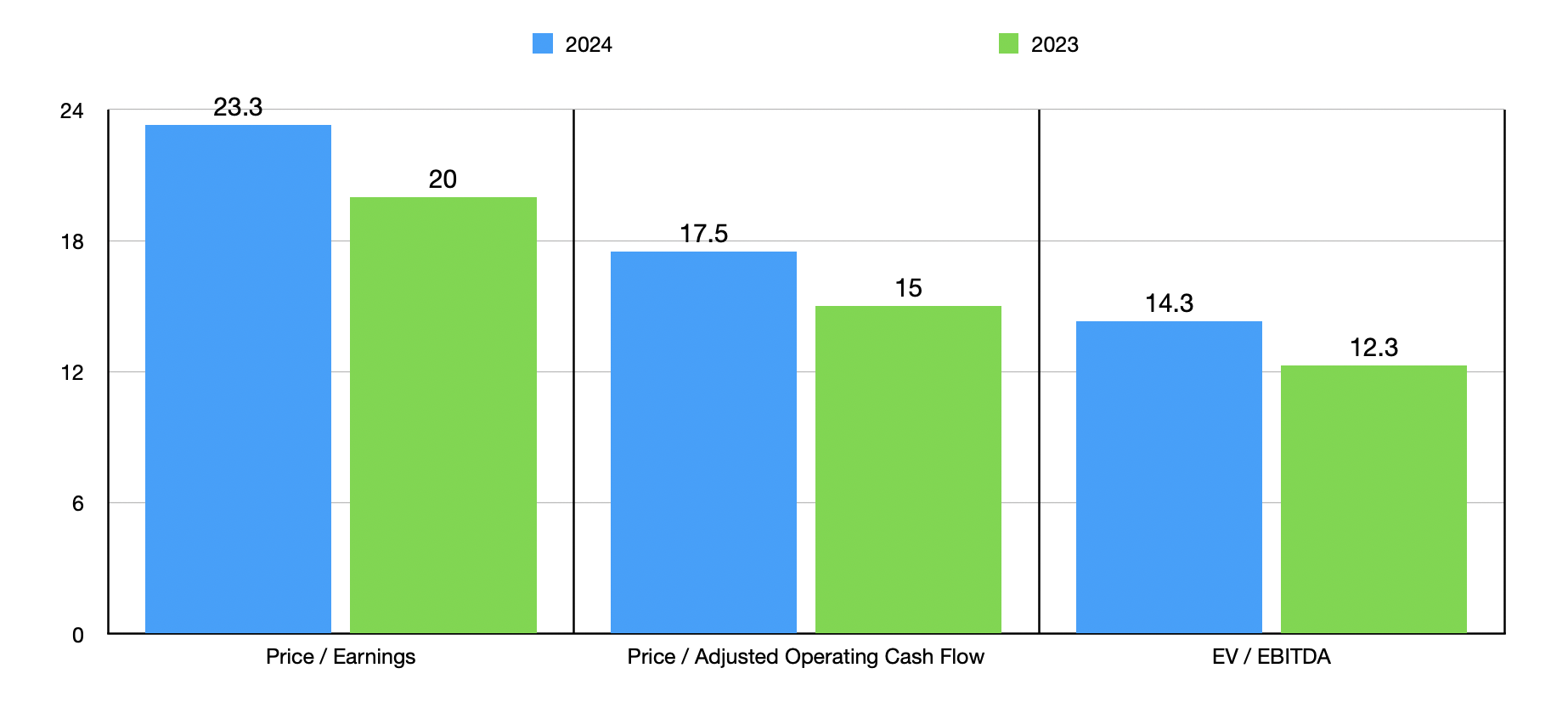

When it comes to the 2024 fiscal year in its entirety, management is forecasting revenue of between $2.6 billion and $2.8 billion. That does represent a decline compared to what was seen in 2023. The only profitability metric that management gave guidance for was EBITDA. That should come in at between $725 million and $825 million. If we assume that other profitability metrics change at the same rate that it is forecasted to at the midpoint, we would anticipate net profits of $434.7 million and adjusted operating cash flow of $578.2 million.

{kind=link}

Using these figures, I priced the company as shown in the chart above. I also priced the company using data from the 2023 fiscal year. As you can see, the stock does look a bit more expensive on a forward basis. But I wouldn't exactly call the stock pricey. In either scenario, the firm looks to be sitting in what I would consider to be the fair value range. Relative to similar firms, it does look to be more or less fairly valued as well. As you can see in the table below, I compared the business to five similar enterprises. Using the price to earnings approach, four of the five companies were cheaper than our target. This drops to three of the five if we use the price to operating cash flow approach and to two of the five if we use the EV to EBITDA approach.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Advanced Draining Systems |

| 20.0 |

| 15.0 |

| 12.3 |

| Builders FirstSource ( BLDR ) |

| 9.9 |

| 5.3 |

| 7.0 |

| Masco ( MAS ) |

| 16.0 |

| 11.5 |

| 12.8 |

| Allegion ( ALLE ) |

| 18.1 |

| 16.1 |

| 14.2 |

| Lennox International ( LII ) |

| 22.8 |

| 29.9 |

| 12.8 |

| Owens-Corning ( OC ) |

| 9.6 |

| 8.7 |

| 6.2 |

Takeaway

From the data that's available, I would make the case that Advanced Drainage Systems is a solid company that is experiencing the early stages of what will be a sustained downturn for at least a couple more quarters. It could last even a bit longer than that. Management does still seem optimistic that the picture for the company won't be awful. But of course, that could change. Coming into this article, I really would have liked to have been able to say that the stock was now cheap enough to upgrade again to a 'buy'. But I'm not there yet. I would need to see the stock drop at least 10% from where it is today for that to occur. And depending on market conditions, I might need to see it drop even further. Of course, if that does occur, or if fundamental performance comes in stronger than anticipated, then my stance might change. But for now, I believe that a 'hold' rating is still appropriate.

For further details see:

Advanced Drainage Systems: The Picture Is Getting More Interesting