AEIS - Advanced Energy Industries: Great Company A Little Expensive

2023-04-06 10:19:30 ET

Summary

- Great FY2022 results prompted me to investigate the company further.

- A tough economic environment in the next year or two suggests that the company is not going to grow at such high rates as before.

- A solid balance sheet suggests the company will survive a potentially upcoming downturn; however, the share price is slightly overvalued currently.

- I’m waiting for a better entry point.

Investment Thesis

With the recent stellar performance seen for FY2022, I wanted to have a look at Advanced Energy Industries ( AEIS ) in more detail to see if it may be a good investment in the long run. After just doing some superficial research by looking at the company’s forward P/E ratio, which is around 20x according to Seeking Alpha, I am already getting a feeling that the company may be a little overvalued for my liking unless the company's growth numbers are truly impressive going forward, in which case the P/E ratio would be reasonable. The slowdown in growth in the semiconductor sector in '23 suggests that the company will not grow anywhere near the same speed as it did in FY2022 and so I believe the company is slightly overvalued right now. Furthermore, the economic environment is not very clear and may present a much better entry point in the next 6 months or so.

The company has been on my watchlist for quite a few years, and I completely forgot about it. Back then it was still slightly overvalued, which was a good few years ago and I haven’t looked at it since. I thought now would be a good time considering the full-year results have come out recently.

FY2022 Results

The company managed to improve on its record year in 2021 by a long mile. Net revenues were up 27% y-o-y. All the company's segments performed well and showed solid double-digit increases, with the semiconductor segment growing 31% while the rest were all over 20% also. Even though the gross margin in Q4 saw a slight contraction of 90bps, on a yearly basis margins were flat. Overall, the company had one of the best years it had ever seen in terms of percentage growth in revenues, and in terms of total revenues.

What’s In Store in the Future?

I wasn't surprised to hear that the company is not predicting growth at such a rate for the next year. The management expects the semiconductor segment, which is around 50% of their total revenue, to perform a little better than the overall market. Let's look at the global semiconductor market in a bit more detail. A forecast done by Gartner suggests that the industry will contract by around 3.6%. The main reason for this forecast is the faltering demand for the products, a buildup of inventories, and a worsening economic outlook. The company is working on the backlog, which is very elevated compared to where they want to be. It has decreased from around $1B to $875m which is good progress. The management is aiming to reduce it to around $400m-$500m, which is still a little elevated compared to their historical levels but it is much better.

So, to combat the overall market’s slowdown, the company will focus on cost-cutting measures to improve margins going forward. The management expects margin headwinds to persist for the first half of ’23 and then slightly start to improve and stabilize going forward. Margins have taken a bit of a beating in the last couple of years, and I would like to see the company starting to improve these back to their previous levels of around 40% on average.

What is the management going to do to achieve better efficiency and profitability? I like that they are focusing on becoming more efficient in the tough economic environment that we are currently experiencing and continue to experience going forward for a little while longer by focusing on the R&D. The company wants to become the leader in all the segments that it operates in.

Another way the company is going to improve efficiency is by looking at all its suppliers and seeing which ones provide the best bang for the buck and focusing on those suppliers while cutting out the ones that are not as efficient. This will certainly have a good impact on the company's margins. Another way of increasing margins that the company is going to utilize is cutting the workforce by around 10%. Seems like the company, just like many other companies, has over-hired during the last couple of years and now the restructuring may be a decent way of getting back to better efficiency and profitability.

The above solutions to improve are admirable, however, it is hard to put a number on any of those actions. In theory the above should be able to improve efficiency and profitability, the question is, by how much? As with all financial forecasting, we can only take on reasonable assumptions. In this case, the company is aiming to get back to 40% margins over the next while. The management is probably aiming to improve those numbers by ’27 or so, but as I would like to be more on the conservative side, I will assume such an improvement will happen by ’32. It is tough for me to be more optimistic than that because in 2018, the company’s gross margins were 51% and since then the contraction has been quite considerable. In the long run, if the company manages to implement all of the cost-cutting measures successfully, and if the economic environment improves, the company may be able to achieve better profitability, but I would have to see a couple of more annual reports in the future to see how it all develops.

Financials

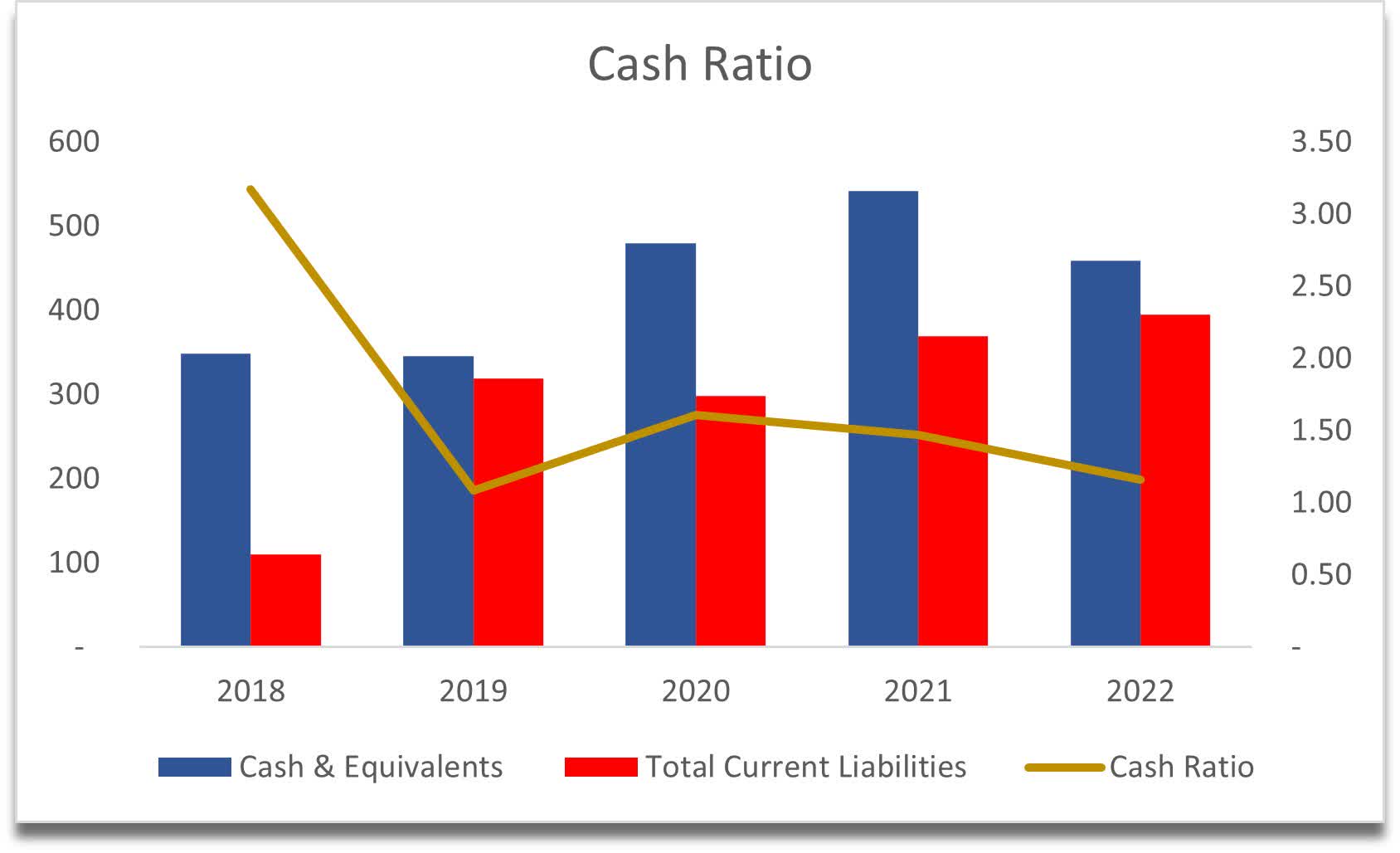

The company at the end of ’22 had a very healthy cash position of $459m, $353m in long-term debt, and $20m of short-term debt, giving a net cash position of $86m. It is not often that I find a company that can cover its short-term obligations solely with cash on hand. AEIS is one of these rare companies. The cash ratio is a much more stringent liquidity measure that looks at the company's ability to pay off total current liabilities with cash on hand only. If a company is not able to cover CLs with cash on hand, I would look for the next best thing which is the current ratio to be at least 1.0. The cash ratio for the company is above one, which is fantastic.

{kind=link}

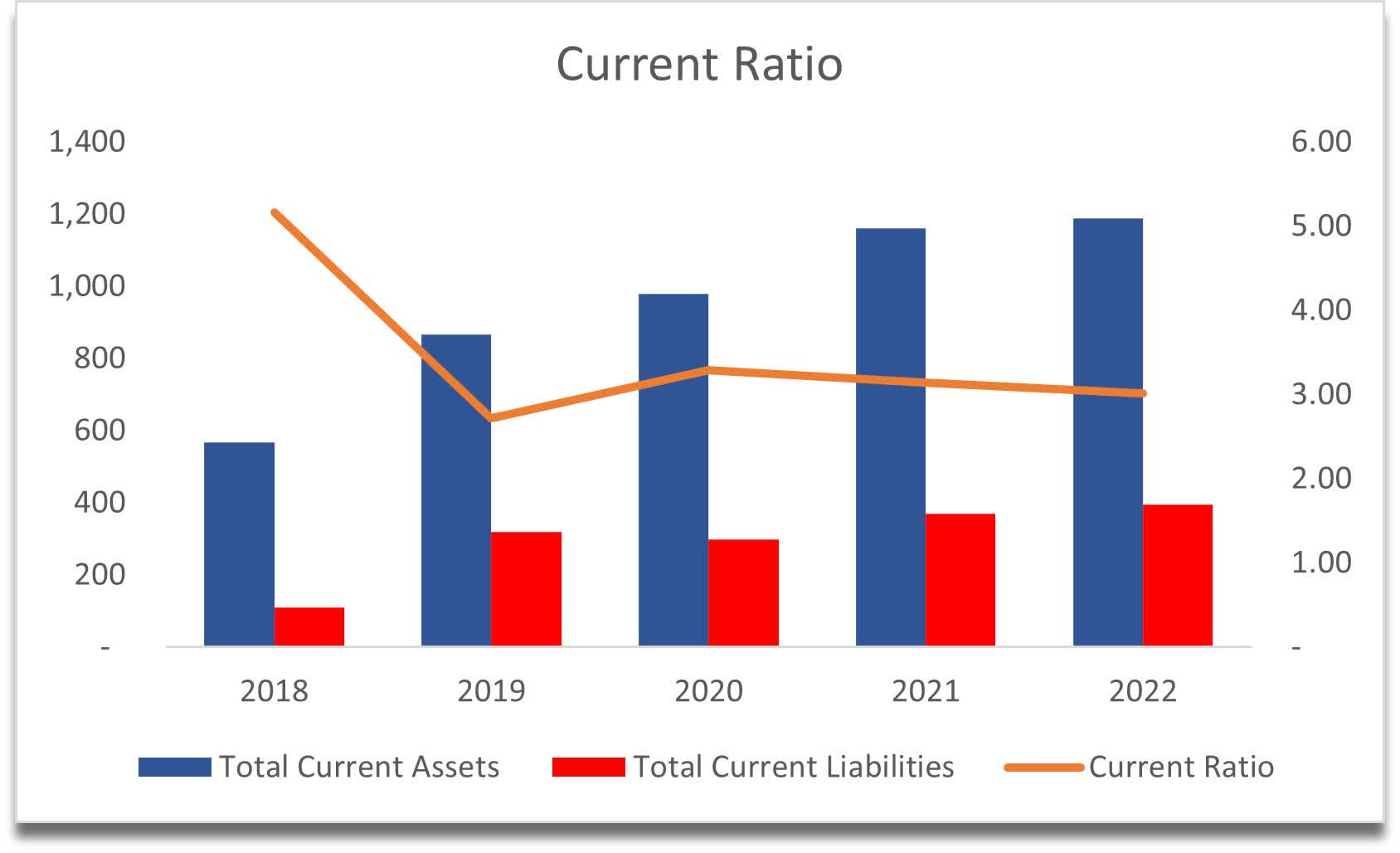

Speaking of the current ratio, it is no surprise that the company is very liquid and will have absolutely no problem paying off its short-term obligations because the current ratio has been well over 2.0 for the last 5 years at least.

{kind=link}

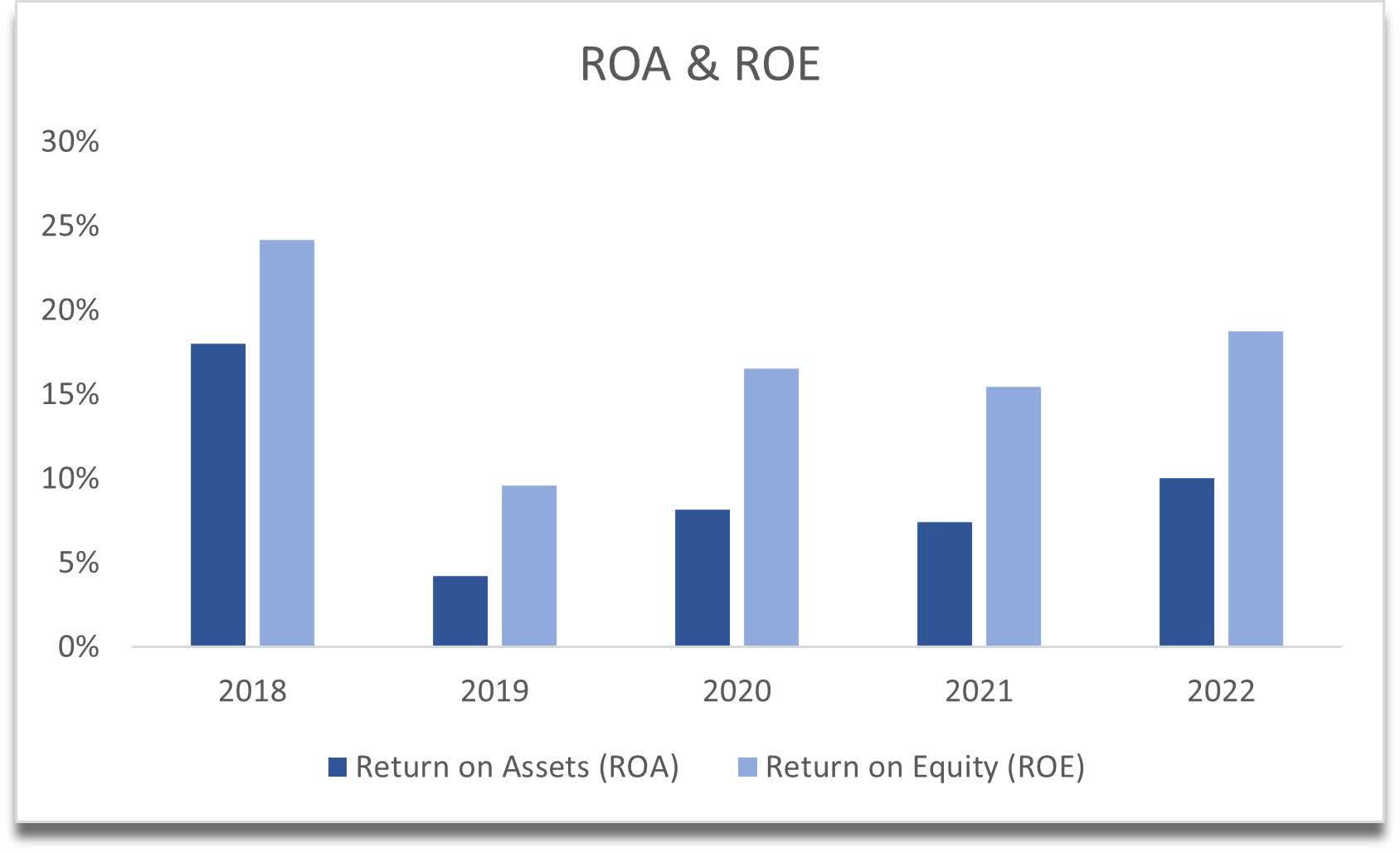

In terms of profitability and efficiency, the company has performed decently there too. ROA and ROE have been going steady for the last few years and within an acceptable minimum, with a slight uptrend in 2022, which I hope continues, although, with the economic uncertainties and margin contractions, I wouldn't be surprised if we see a slight dip.

{kind=link}

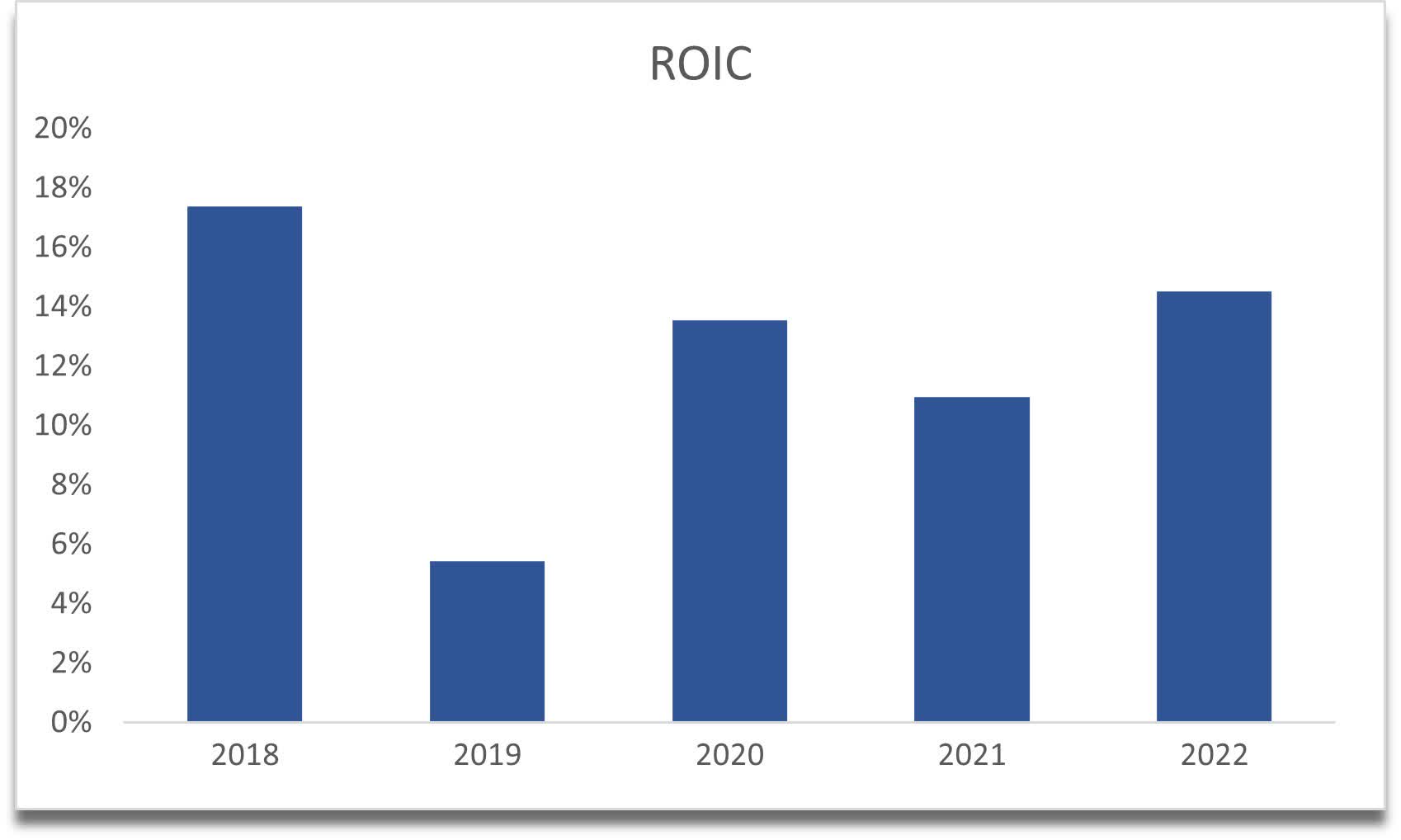

If a company, in my opinion, manages to achieve an ROIC of over 10%, it deserves a slight premium. In other words, I will be ok with paying slightly more for such a company because it suggests that the company has a competitive advantage and a decent moat. Now it doesn't mean that I will buy at any price, because if the price is still a little too high, I can lose money even if the company is worthy of investment in the long run. AEIS is a company that seems to have a competitive advantage and a decent moat. As with the above metrics mentioned, we could see a slight dip in profitability in the short run.

{kind=link}

Overall, the company seems to be running quite efficiently. The management knows how to operate this business and gets as much out of the segments as possible that will turn into positive NPV. The health of the balance sheet may be a good enough reason to invest in the company as it seems like a potential upcoming economic downturn will have little effect on it, but as I said earlier, it is possible to overpay for a great company. Let’s have a look at a valuation according to my conservative estimates.

Valuation

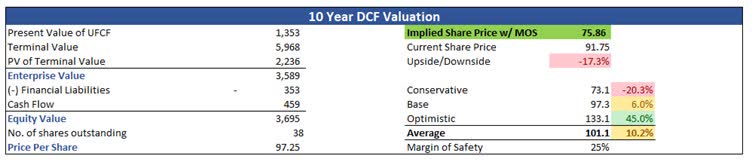

For the valuation model, I will present a simple and conservative forecast of the company's revenue growth and margin improvements over the next ten years. The company's revenues increased by over 500% in the last 10 years. That is some growth. Can we project something similar for the next 10? I don't think it's possible given the high probability of an economic downturn in the next 12-24 months, supply chain issues not fully resolved, and the decrease in demand for the products. For the base case, I decided to go with a linear growth approach for the revenues which sees revenues almost double in 10 years from $1.8B in ’22 to $3.4B by ’32. This gives us around 6.5% growth annually. It is hard to assume higher growth than this because we don’t know what the environment is going to look like in the next couple of years and beyond, so I think these numbers are quite conservative.

To get a range of possible outcomes from which then I can take an average, I also have a conservative case, where I made the growth 200bps less, and the optimistic case where the growth is 200bps more than the base case, 4.5% and 8.5% respectively.

In terms of margins, I believe the management is capable of increasing profitability and efficiency over time, which lead me to improve margins to 40% by '32 on the base case, 39.25% in the conservative case, and almost 41% on the optimistic case. I know these may look like not much, however, these numbers make quite a big difference in terms of valuations.

To be even more on the safe side, I always add a margin of safety, and the amount of safety depends on the company’s balance sheet and how well I believe the company can weather downturns. AEIS in my opinion is going to do just fine in an upcoming recession and so it gets my minimum margin of safety requirement of 25%. With these assumptions, the company’s implied intrinsic value is $75.86 per share, which suggests the company is currently a little pricy and has a downside of around 17%.

{kind=link}

Closing Remarks

As I mentioned at the beginning of the article, the company is trading at around 20x earnings, which after looking into the revenue projections and possible outcomes, seems a little expensive to me. If the company was to trade at the above intrinsic value of $75.86 that would put the P/E ratio at around 14x, which is much more reasonable in my opinion. To justify the current valuation, the company needs to grow its revenues from $1.8B to $6.8B in the next 10 years, which is an average growth of 14% per year. I don’t think it’s very possible without some massive catalyst or a solid improvement in supply and demand environments.

The company is a great investment if the share price comes down to around $75 for me. It is hard to know if it'll come back to around 14x earnings. The last time it was there was back in October of last year, which is not that long ago, and given the current volatility in the global economy, I believe we will see a better price point in the future.

For further details see:

Advanced Energy Industries: Great Company, A Little Expensive